|

시장보고서

상품코드

1936037

능동 방어 체계(APS) 시장(2026-2036년)Global Active Protection Systems Market 2026-2036 |

||||||

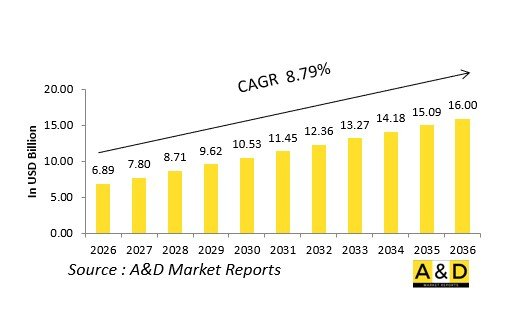

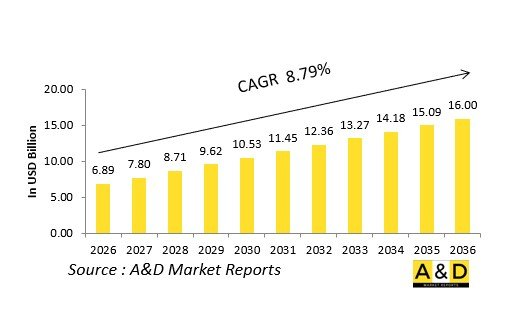

세계 능동 방어 체계(APS) 시장 규모는 2026년 68억 9,000만 달러로 추정되며, 2036년까지 160억 달러에 달할 것으로 예상되며, 2026-2036년 예측 기간 동안 8.79%의 CAGR을 보일 것으로 예상됩니다.

소개

세계 APS(Active Protection System) 시장은 장갑차 방어의 최전선에 있으며, 자동화된 탐지 및 무력화를 통해 정교한 대 장갑 위협에 대응합니다. APS는 센서, 발사기, 이펙터를 활용하여 비행 중인 투사체를 요격함으로써 탱크, 보병 수송차, 포병을 미사일, 로켓, 드론으로부터 보호합니다. 하이브리드 전쟁이 격화되는 가운데, 이러한 시스템은 수동 장갑의 취약점을 보완할 수 있습니다.

시장 성장은 지상전 수요의 증가를 반영하고 있으며, APS는 지점 방어에서 전투 관리 시스템과 통합된 네트워크 중심 솔루션으로 진화하고 있습니다. 주요 구성품으로는 레이더 탐색기, 운동에너지 요격탄, 저부수적 피해를 목적으로 하는 도시 작전을 위한 소프트 킬 재머 등이 있습니다. 제조사들은 기존 차량의 개조와 새로운 플랫폼 모두에 적용 가능한 모듈성을 강조하여 수출의 매력을 강화하고 있습니다.

지정학적 긴장이 조달을 촉진하고 있으며, 군대는 정밀유도무기에 대한 비대칭적 우위를 추구하고 있습니다. 무인 시스템과의 융합을 통해 APS는 로봇 전투 차량으로까지 확장되고 있습니다. 공급망은 내결함성 전자기기와 고속 이펙터에 초점을 맞추고, 표준화를 통해 동맹 간의 상호 운용성을 보장합니다. 경쟁 역학에서는 주요 기업들이 스타트업과 협력하여 AI 기반 위협 분류 시스템을 개발하고 있습니다.

시장은 지배적인 기동전을 목표로 APS를 디지털 사격 및 센서 융합과 통합하는 능동적 생존성으로의 패러다임 전환을 강력히 시사하고 있습니다.

능동 방어 체계(APS)의 주요 촉진요인

장갑 위협의 증가는 능동 방어 체계(APS) 시장을 주도하고 있습니다. 휴대용 대전차 유도 미사일과 배회 탄약의 확산은 기존 장갑의 취약성을 드러내어 군대가 APS를 탑 어택 프로파일에 대한 하드 킬 능력으로 채택하도록 강요하고 있습니다.

전 세계 군대의 현대화 물결이 개조를 촉진하고 있으며, 반응형 장갑 및 트로피형 이펙터와 결합된 시스템이 선호되고 있습니다. 도시전이나 하이브리드 전쟁의 교리에서는 주변 민간인이나 아군 부대를 위험에 빠뜨리지 않고 위협을 무력화할 수 있는 저부수적 피해 솔루션이 요구되고 있습니다.

동맹 간 상호운용성 표준이 채택을 가속화하고 있으며, 공동 작전에서 APS를 의무화하는 프로그램도 존재합니다. 신흥 강국들이 라이선싱과 기술이전을 통해 지역 라이벌들과 경쟁하는 가운데, 수출 시장은 급성장하고 있습니다. 물류적 요청으로 인해 액티브 서스펜션 및 파워 시스템과 통합 가능한 경량화 및 자동화 시스템이 중요시되고 있습니다.

지속가능성 측면에서 재사용 가능한 요격탄과 에너지 절약형 레이저가 추진되고 있으며, 이는 녹색방위 구상과 일치합니다. 사이버 내성 설계는 전자전에 대응하기 위해 강화된 프로세서를 내장하고 있습니다. 인간 중심 설계는 탑승자 보호에 중점을 두어 스탠드 오프 요격으로 인한 폭발에 대한 노출을 줄입니다.

긴박한 상황에서의 방어태세 강화는 APS와 지향성 에너지 및 극초음속 기술을 융합하는 연구개발을 지속하고 있습니다. 이러한 촉진요인들은 이펙터 차세대 장갑의 우위에 필수적인 요소로 작용하고 있습니다.

능동 방어 체계(APS)의 지역적 동향

지역별 차이가 능동 방어 체계(APS)의 시장 상황을 형성하고 있습니다. 유럽에서는 NATO의 조화가 주력 전차를 위한 성숙한 네트워크화 APS를 추진하고 있으며, 고강도 분쟁에서 정밀 공격에 대한 소프트 킬 통합이 강조되고 있습니다.

세계의 능동 방어 체계(APS) 시장에 대해 조사 분석했으며, 시장에 영향을 미치는 기술, 향후 10년간의 예측, 각 지역별 동향 등의 정보를 전해드립니다.

목차

시장 정의

능동 방어 체계(APS) 시장 세분화

능동 방어 체계(APS)의 10년 후 시장 전망

능동 방어 체계(APS) 시장 기술

능동 방어 체계(APS) 세계 시장 예측

능동 방어 체계(APS) 지역 시장 동향 및 예측

시장 예측 및 시나리오 분석

시장 예측 및 시나리오 분석

결론

Aviation and Defense Market Reports 소개

KSM 26.03.05The Global Active protection system market is estimated at USD 6.89 billion in 2026, projected to grow to USD 16.00 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 8.79% over the forecast period 2026-2036.

Introduction

The global Active Protection Systems (APS) market stands at the forefront of armored vehicle defense, countering sophisticated anti-armor threats through automated detection and neutralization. APS employ sensors, launchers, and effectors to intercept projectiles mid-flight, safeguarding tanks, infantry carriers, and artillery from missiles, rockets, and drones. As hybrid warfare intensifies, these systems bridge vulnerabilities in passive armor.

Market growth mirrors escalating ground combat demands, with APS evolving from point-defense to network-centric solutions integrated with battle management systems. Key components include radar seekers, kinetic interceptors, and soft-kill jammers, designed for low-collateral urban operations. Manufacturers prioritize modularity for retrofitting legacy fleets alongside new platforms, enhancing export appeal.

Geopolitical flashpoints drive procurement, as armies seek asymmetric advantages against precision-guided munitions. Convergence with unmanned systems extends APS to robotic combat vehicles. Supply chains focus on resilient electronics and high-speed effectors, while standards ensure interoperability across alliances. Competitive dynamics feature primes collaborating with startups on AI-driven threat classifiers.

This market underscores a paradigm shift toward proactive survivability, intertwining APS with digital fires and sensor fusion for dominant maneuver warfare.

Technology Impact in Active Protection Systems

Technological leaps redefine Active Protection Systems (APS), elevating them from reactive countermeasures to predictive shields. Multi-spectral sensors-fusing radar, infrared, and electro-optical-enable 360-degree threat tracking, discerning decoys from live munitions amid clutter. AI algorithms process data in milliseconds, prioritizing intercepts and minimizing false alarms through machine learning trained on diverse threat libraries.

Kinetic effectors advance with high-velocity projectiles that fragment incoming warheads, while directed-energy variants like lasers promise unlimited "magazine" depth for drone swarms. Soft-kill measures deploy directed infrared countermeasures and electronic decoys, disrupting seeker heads without physical intercept. Networked APS share threat data across vehicle platoons, creating protective bubbles via mesh communications.

Modular architectures facilitate platform-agnostic integration, from light tactical vehicles to heavy tanks, with plug-and-play sensor pods. GaN-based radars boost range and resolution, resisting jamming. Hypersonic threat countermeasures emerge, incorporating plasma shields and adaptive optics. Digital twins accelerate development, simulating engagements for rapid iteration.

These innovations slash engagement timelines, boost hit probabilities, and reduce crew workload, transforming APS into force multipliers that enable aggressive tactics in high-threat zones.

Key Drivers in Active Protection Systems

Intensifying armored threats propel the Active Protection Systems (APS) market. Proliferation of man-portable anti-tank guided missiles and loitering munitions exposes vulnerabilities in traditional armor, compelling forces to adopt APS for hard-kill capabilities against top-attack profiles.

Modernization waves across global armies drive retrofits, prioritizing systems that layer with reactive armor and trophy-like effectors. Urban and hybrid warfare doctrines demand low-collateral solutions that neutralize threats without endangering civilians or friendly forces nearby.

Allied interoperability standards accelerate adoption, with programs mandating APS for joint operations. Export markets boom as emerging powers counter regional rivals through licensed production and technology transfers. Logistics imperatives favor low-weight, automated systems that integrate with active suspension and power systems.

Sustainability pushes for reusable interceptors and energy-efficient lasers, aligning with green defense initiatives. Cyber-resilient designs counter electronic warfare, embedding hardened processors. Human-centric factors emphasize crew protection, reducing exposure to blasts via standoff intercepts.

Rising defense postures amid tensions sustain R&D, blending APS with directed energy and hypersonics. Collectively, these drivers position APS as indispensable for next-era armored dominance.

Regional Trends in Active Protection Systems

Regional variations shape the Active Protection Systems (APS) market landscape. In Europe, NATO harmonization drives mature, networked APS for main battle tanks, emphasizing soft-kill integration against precision fires in high-intensity conflicts.

Middle East procurement surges, with desert-optimized systems countering asymmetric rocket threats; local assembly offsets bolster self-reliance amid prolonged engagements.

Asia-Pacific sees indigenous development, tailoring APS to mountainous and island terrains for anti-access/area-denial scenarios, fused with domestic radars.

North America pioneers directed-energy APS variants for expeditionary forces, leveraging vast R&D ecosystems for multi-domain operations.

Russia and allies focus on heavy armor-centric hard-kill suites, resilient to electronic countermeasures in peer fights.

Latin America adopts cost-effective retrofits for counter-narcotics vehicles, prioritizing urban collateral mitigation.

Africa trends toward light, vehicle-agnostic APS for peacekeeping, combating improvised threats with modular kits.

Indo-Pacific alliances emphasize swarm defense, integrating APS with air defense nets. Global trends converge on open architectures for upgrades, with supply chains shifting to diversified electronics hubs.

Key Active Protection Systems Programs

Landmark programs anchor the Active Protection Systems (APS) landscape. Trophy-like hard-kill systems equip elite tank brigades, launching explosive projectiles to shred incoming missiles, proven in urban combat validations.

Next-gen networked APS fuse vehicle sensors with overhead drones, sharing intercept cues for platoon-level shields against salvo attacks. Navalized derivatives protect amphibious assault vehicles, adapting effectors for maritime launch constraints. Light tactical APS programs outfit infantry carriers with compact radars and micro-interceptors, enabling convoy survivability in insurgent zones. Directed-energy prototypes mature, deploying high-power microwaves to fry drone electronics, extending to laser dazzlers for non-lethal options.

Retrofit initiatives upgrade legacy platforms with bolt-on pods, incorporating gallium nitride seekers for extended envelopes. Collaborative alliances develop common APS architectures, standardizing interfaces for multinational fleets. Export packages bundle APS with armor sales, including training simulators for operator proficiency. Emerging hypersonic countermeasures test plasma-based deflectors, paired with quantum sensors for ultra-fast detection.

Table of Contents

Active Protection Systems - Table of Contents

Market Definition

Market Segmentation of Active Protection Systems

By Region

By Application

By Material

10 Year Market Outlook of Active Protection Systems

The 10-year market outlook would give a detailed overview of changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Active Protection Systems

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Market Forecast of Active Protection Systems

The 10-year market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Market Trends & Forecast of Active Protection Systems

The regional market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Active Protection Systems

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix of Active Protection Systems

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions of Active Protection Systems

Hear from our experts their opinion of the possible outlook for this market.