|

시장보고서

상품코드

1936046

방어 항공기 터빈 및 압축기 시장(2026-2036년)Global Defense Aircraft Turbines and Compressors Market 2026-2036 |

||||||

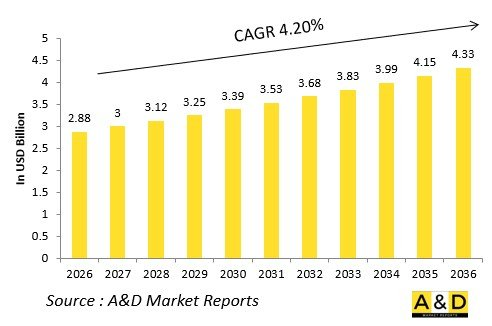

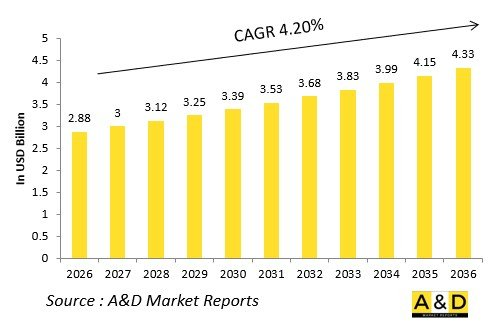

세계 방어 항공기 터빈 및 압축기 시장 규모는 2026년 28억 8,000만 달러에서 2026년부터 2036년까지 예측 기간 동안 4.20%의 CAGR로 성장하여 2036년에는 43억 3,000만 달러에 달할 것으로 예상됩니다.

소개

세계 방어 항공기 터빈 및 압축기 시장은 군용 터보팬, 터보프롭, 터보샤프트에서 추력을 생성하기 위한 압축 공기 및 추출 에너지를 공급하여 추진 성능의 우위를 뒷받침하고 있습니다. 다단식 고압 압축기는 연소기에 공기를 공급하고, 동력 터빈은 샤프트 구동 액세서리 및 벡터 노즐에 동력을 공급합니다.

시장의 발전은 차세대 전투기에 대한 요구를 반영하고 있으며, 가변형 지오메트리와 브리스크 기술은 가혹한 열 부하 하에서 압축 효율을 향상시키고 있습니다. 핵심 기술로는 후퇴 날개 팬 블레이드, 단간 블리드 밸브, 애프터버너 작동 시 산화를 방지하는 세라믹 매트릭스 코팅 등이 있습니다. 저 가시성 배기에 중점을 두고 적외선 억제 기술과의 통합이 진행되고 있습니다.

또한, 지정학적 영공권 경쟁이 개발을 가속화하고 있으며, 전체 함대의 신속한 업그레이드를 가능하게 하는 모듈식 코어가 우선시되고 있습니다. 개방형 아키텍처로 전면적인 재설계 없이 기술 도입이 가능합니다. 공급망은 내화 초합금과 정밀 단조품에 초점을 맞추고 있습니다. 경쟁 측면에서는 Pratt & Whitney, GE, Safran 등이 제3의 조류인 적응형 엔진의 선구자 역할을 하고 있습니다.

방어 항공기의 기술적 영향 : 터빈 및 압축기

추가 제조 기술을 통해 내부 냉각 채널이 있는 복잡한 압축기 브리스크가 제조되어 부품 수를 줄이면서 공기역학적 효율을 향상시켰습니다. 가변 정적 날개는 비행 영역 전체에 걸쳐 각도를 조정하여 슈퍼크루즈 및 대기 비행 시 서지를 방지합니다.

고압 터빈에 채택된 세라믹 기반 복합재료는 연소 온도를 견딜 수 있고, 블레이드 크리프 없이 고압비를 실현합니다. 플라즈마 분무식 내열 코팅은 애프터버너 작동 시 고온부 수명을 연장합니다. 디지털 트윈 기술을 통한 실속 한계 및 버드 스트라이크 거동 시뮬레이션으로 인증 프로세스를 가속화합니다.

적응형 사이클 압축기는 바이패스 공기를 추력 또는 효율로 배분하여 공중전 및 침투 임무에 최적화합니다. 블렌디드 날개 동체 흡기구는 왜곡에 강한 계단식 설계가 요구됩니다. 전기 부스트 압축기는 항공모함에서 단거리 이륙을 위해 코어 유량을 증가시킵니다.

생성 설계를 통한 AI 최적화 날개 형상은 확산 계수를 극대화합니다. 루테늄 합금을 사용한 단결정 터빈 블레이드는 산화에 강합니다. 이러한 혁신은 추력 대 중량비 향상, 시그니처 감소, 항속거리 연장을 실현하여 경쟁에서 엔진 사이클을 재정의하고 있습니다.

방어 항공기 터빈 및 압축기 : 주요 촉진요인

차세대 전투기 프로그램은 슈퍼크루즈 능력을 갖춘 고추력 코어를 요구하고 있으며, 블레이드 디스크의 혁신을 추진하고 있습니다. 스텔스성 확보를 위해 냉각 배기 경로를 갖춘 저적외선 터빈 구조가 필수입니다.

유지관리 측면의 요청에 따라 엔진 탈착을 최소화하는 모듈식 고온부 구조가 강조되고 있습니다. 수출 오프셋을 통해 압축기 스테이지의 라이선스 생산이 촉진되고 있습니다. 원정 작전에서는 사막에서 극한의 추위까지 대응할 수 있는 다중 연료 호환성이 요구됩니다.

예산 재조정으로 인해 순수 출력보다 열역학적 효율이 우선시됩니다. 공급망 복원력 강화는 재활용을 통한 희토류 원소 제한 대책이 될 수 있습니다. 상호운용성 표준을 통해 동맹국 간 공통의 예비 부품을 사용할 수 있습니다.

도시 지역에서의 근접 항공 지원은 압축기 스톨을 피할 수 있는 반응성이 높은 압축기를 필요로 합니다. 이러한 요인으로 인해 첨단 코어는 전략적 자산으로 자리 잡았습니다.

세계의 방어 항공기 터빈 및 압축기 시장을 조사했으며, 주요 동향, 시장 영향요인, 주요 기술 및 그 영향력, 주요 지역 및 국가별 동향, 시장 기회 분석 등의 정보를 정리하여 전해드립니다.

목차

방어 항공기 터빈 및 압축기 시장 : 목차

방어 항공기 터빈 및 압축기 시장 : 보고서의 정의

방어 항공기 터빈 및 압축기 시장 : 세분화

향후 10년간의 방어 항공기 터빈 및 압축기 시장 분석

방어 항공기 터빈 및 압축기 시장 : 기술

세계 방어 항공기 터빈 및 압축기 시장 : 전망

방어 항공기 터빈 및 압축기 시장 동향 및 전망 : 지역별

시장 예측 및 시나리오 분석

방어 항공기 터빈 및 압축기 시장 : 국가별 분석

시장 예측 및 시나리오 분석

방어 항공기 터빈 및 압축기 시장 : 기회 매트릭스

방어 항공기 터빈 및 압축기 시장 : 보고서에 대한 전문가들의 의견

결론

Aviation and Defense Market Reports 소개

KSM 26.03.05The Global Defense Aircraft Turbines and Compressors Market is estimated at USD 2.88 billion in 2026, projected to grow to USD 4.33 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 4.20% over the forecast period 2026-2036.

Introduction

The global Defense Aircraft Turbines and Compressors market drives propulsion superiority, delivering compressed air and extracted energy for thrust in military turbofans, turboprops, and turboshafts. Multi-stage high-pressure compressors feed combustors, while power turbines extract work for shaft-driven accessories and vectored nozzles.

Market evolution mirrors next-generation fighter demands, where variable geometry and blisks enhance compression efficiency under extreme thermal loads. Core technologies include swept fan blades, interstage bleed valves, and ceramic matrix coatings resisting oxidation in afterburning modes. Emphasis on low-observable exhausts integrates with infrared suppression.

Geopolitical air superiority races accelerate development, prioritizing modular cores for rapid upgrades across fleets. Open architectures enable technology insertion without full redesigns. Supply chains focus on refractory superalloys and precision forgings. Competition features Pratt & Whitney, GE, and Safran pioneering third-stream adaptive engines.

This market fuels aerial dominance through thermodynamic edges.

Technology Impact in Defense Aircraft Turbines and Compressors

Additive manufacturing crafts complex compressor blisks with internal cooling channels, slashing part counts while boosting aerodynamic efficiency. Variable stator vanes adjust incidence angles across flight envelopes, preventing surge in supercruise or loiter.

Ceramic matrix composites in high-pressure turbines withstand combustor temperatures, enabling higher overall pressure ratios without blade creep. Plasma-sprayed thermal barrier coatings extend hot-section lives under afterburner excursions. Digital twins simulate stall margins and bird-strike dynamics, accelerating certification.

Adaptive cycle compressors divert bypass air for thrust or efficiency, optimizing for air combat or penetration. Blended wing-body inlets demand distortion-tolerant stages. Electric boost compressors augment core flow for short takeoffs from carriers.

AI-optimized airfoil shapes via generative design maximize diffusion factors. Single-crystal turbine blades with ruthenium alloys resist oxidation. These innovations yield higher thrust-to-weight, reduced signatures, and extended ranges, redefining engine cycles for peer competition.

Key Drivers in Defense Aircraft Turbines and Compressors

Next-generation fighter programs demand high-thrust cores with supercruise capability, driving bladed disk innovations. Stealth mandates low-infrared turbine architectures with cooled exhaust paths.

Sustainment imperatives favor modular hot sections minimizing engine removals. Export offsets spur licensed production of compressor stages. Expeditionary ops require multi-fuel compatibility from desert to arctic.

Budget realignments prioritize thermodynamic efficiency over raw power. Supply chain resilience counters rare earth constraints via recycling. Interoperability standards enable common spares across alliances.

Urban close air support needs responsive compressors avoiding compressor stalls. These forces embed advanced cores as strategic assets.

Regional Trends in Defense Aircraft Turbines and Compressors

North America dominates with adaptive cycle prototypes for sixth-generation platforms, emphasizing variable geometry.

Europe collaborates on FCAS cores with contra-rotating turbines for efficiency.

Asia-Pacific accelerates indigenous development-India's Kaveri derivatives, China's WS-15-tailored to high-altitude intercepts.

Middle East pursues afterburning turbofans for regional deterrence.

Russia advances high-temperature materials for Su-57 sustainment.

South Korea integrates with KF-21 for export competitiveness.

Trends favor ceramic turbines; Asia-Pacific captures manufacturing growth.

Key Defense Aircraft Turbines and Compressors Program

F-35's F135 powers three variants with shaft-driven lift fans and adaptive afterburners.

NGAD adaptive engines feature third-stream compressors for thrust vectoring.

Eurofighter EJ200 upgrades incorporate blisks for enhanced dry thrust.

India's Kaveri dry variant equips Tejas with indigenous compressors.

RQ-170 drone turbines prioritize low-signature cooled blades.

B-21 Raider cores emphasize endurance over peak power.

Safran's M88 for Rafale integrates modular hot sections.

T-7A trainer engines drive high-cycle compressor testing.

Table of Contents

Defense Aircraft Turbines and Compressors Market - Table of Contents

Defense Aircraft Turbines and Compressors Market Report Definition

Defense Aircraft Turbines and Compressors Market Segmentation

-By Platform

-By Application

-By Technology

-By Material

Defense Aircraft Turbines and Compressors Market Analysis for next 10 Years

The 10-year Defense Aircraft Turbines and Compressors Market analysis would give a detailed overview of Defense Aircraft Turbines and Compressors Market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Defense Aircraft Turbines and Compressors Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Defense Aircraft Turbines and Compressors Market Forecast

The 10-year Defense Aircraft Turbines and Compressors Market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Defense Aircraft Turbines and Compressors Market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Defense Aircraft Turbines and Compressors Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Defense Aircraft Turbines and Compressors Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Defense Aircraft Turbines and Compressors Market Report

Hear from our experts their opinion of the possible analysis for this market.