|

시장보고서

상품코드

2023779

장갑차 시장(2026-2036년)Global Armored Vehicle Market 2026-2036 |

||||||

세계의 장갑차 시장

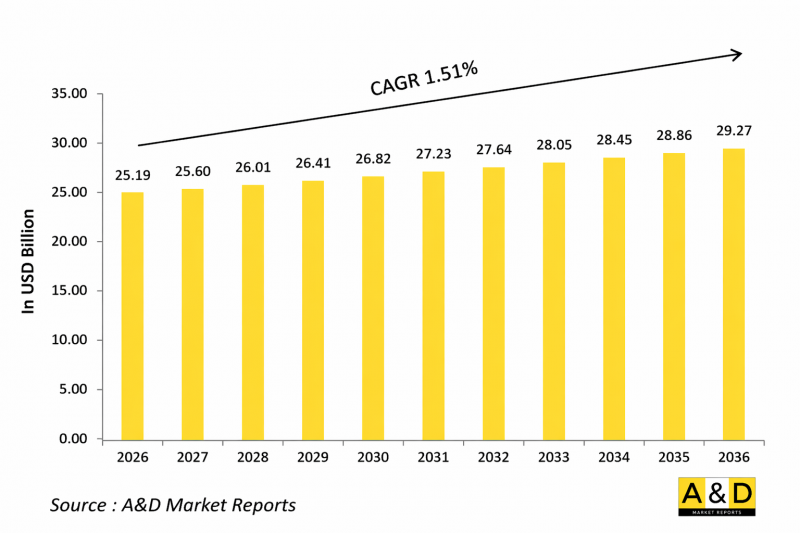

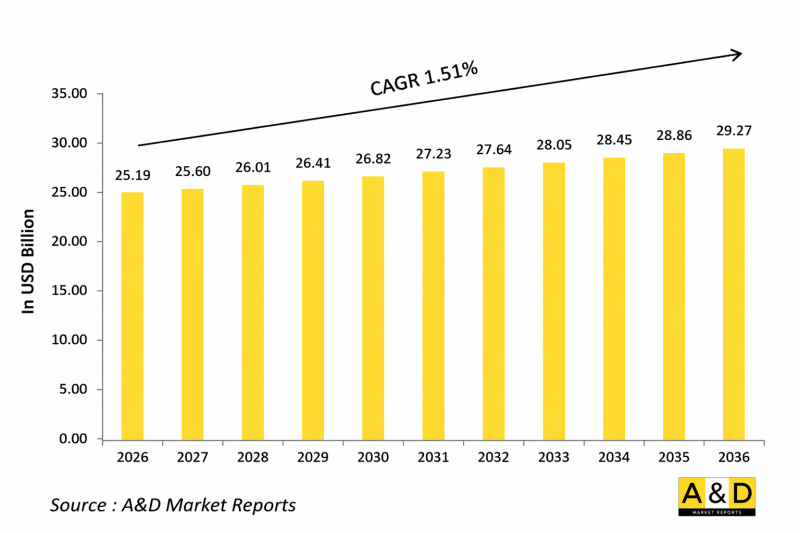

전 세계 장갑차 시장 규모는 2026년 251억 9,000만 달러로 추정되며, 2026년부터 2036년까지 예측 기간 동안 CAGR 1.51%로 성장하여 2036년에는 292억 7,000만 달러에 달할 것으로 예상됩니다.

1. 소개

전 세계 장갑차 시장은 전체 방위 및 보안 산업에서 매우 중요한 부문으로, 전장에서 생존성, 기동성 및 전투 효율성을 향상시키기 위해 설계된 플랫폼에 초점을 맞추고 있습니다. 장갑차에는 주력전차, 보병전투차, 장갑수송차, 대지뢰차량 등 다양한 시스템이 포함됩니다. 이러한 플랫폼은 적대적이고 위험한 환경에서 활동하기 때문에 군대, 법집행기관 및 보안 조직에 의해 광범위하게 배치되고 있습니다. 비대칭 위협과 도심 전투 시나리오 등 현대 전쟁의 복잡성이 증가함에 따라 첨단 장갑 기동 솔루션에 대한 의존도가 크게 증가하고 있습니다. 또한, 국방력 현대화를 위한 노력과 노후화된 차량 교체에 대한 요구가 전 세계 조달 전략을 형성하고 있습니다. 방어 시스템의 기술 발전, 기동성 향상, 디지털 전장 통합은 시장을 더욱 변화시키고 있으며, 장갑차는 일반 전쟁과 하이브리드 전쟁 환경 모두에서 필수적인 자산으로 자리매김하고 있습니다.

2. 세계 장갑차 시장에서 기술의 영향력

기술 혁신은 장갑차의 운용 능력을 재정의하고 적응성, 생존성, 네트워크 중심성을 높이고 있습니다. 현대의 플랫폼에는 점점 더 많은 능동형 방어 시스템이 탑재되어 접근하는 위협을 감지하고 무력화시켜 탑승자의 안전이 크게 향상되고 있습니다. 하이브리드 및 전기 추진 기술은 연료 효율성 향상, 열 시그니처 감소, 전술 환경에서 정숙한 기동성 구현을 목표로 연구되고 있습니다. 또한, 모듈식 장갑 설계의 발전으로 임무 요구 사항에 따라 신속한 업그레이드와 커스터마이징이 가능해졌습니다. 디지털화는 매우 중요한 역할을 하고 있으며, 차량은 이제 네트워크 중심의 전술 시스템에 통합되어 실시간 데이터 공유, 상황 인식 및 협업 작전을 가능하게 합니다. 자율 및 선택적 유인 차량 기술도 확산되고 있으며, 부대는 인적 위험을 줄이면서 고위험 임무를 수행할 수 있게 되었습니다. 인공지능과 첨단 센서는 항법, 위협 감지 및 의사결정 능력을 더욱 강화하여 점점 더 복잡해지고 데이터에 기반한 전투 시나리오에서도 장갑차가 계속 효과를 발휘할 수 있도록 보장합니다.

3. 세계 장갑차 시장의 주요 시장 촉진요인

세계 장갑차 시장의 성장은 몇 가지 전략적 및 운영적 요인에 의해 주도되고 있습니다. 지정학적 긴장이 고조되고 지역 분쟁이 격화됨에 따라 첨단 육상 전투 시스템에 대한 수요가 증가하고 있으며, 각국 정부는 현대화 프로그램에 대한 투자에 박차를 가하고 있습니다. 즉발폭발물(IED) 및 탄도 위협에 대한 부대 보호 강화의 필요성도 주요 촉진요인 중 하나이며, 이로 인해 중장갑 및 대지뢰 내성 플랫폼의 채택이 증가하고 있습니다. 또한, 군대는 기동성과 신속한 배치 능력 향상에 주력하고 있으며, 이는 다목적 경량 장갑차에 대한 수요를 가속화하고 있습니다. 비대칭 전쟁과 대반란 작전의 증가는 적응력이 뛰어나고 기술적으로 진보된 플랫폼의 중요성을 더욱 강조하고 있습니다. 국내 방산 제조업을 강화하고 수입 의존도를 낮추기 위한 정부의 노력도 시장 확대에 기여하고 있습니다. 또한, 전장 요구 사항의 변화와 첨단 무기 시스템의 통합은 차세대 장갑차에 대한 수요를 지속적으로 자극하고 있습니다.

4. 세계 장갑차 시장의 지역적 동향

세계 장갑차 시장의 지역별 동향은 국방 우선순위, 예산 배분, 지정학적 환경의 차이에 따라 형성되고 있습니다. 북미는 현대화 및 첨단 전투차량 프로그램에 대한 지속적인 투자로 인해 여전히 중요한 시장으로 남아 있습니다. 유럽에서는 차량 갱신 노력과 역내 국가 간 국방 협력 강화에 힘입어 강한 수요를 보이고 있습니다. 아시아태평양은 안보 우려 증가, 국경 긴장, 인도와 중국 등의 국가들의 대규모 조달 프로그램에 힘입어 주요 성장 지역으로 부상하고 있습니다. 중동에서는 계속되는 지역 분쟁에 대응하고 군사력을 강화하기 위해 장갑차에 대한 막대한 투자가 계속되고 있습니다. 한편, 라틴아메리카와 아프리카에서는 국내 치안 강화와 평화유지 활동을 위해 장갑 플랫폼의 도입이 점진적으로 진행되고 있습니다. 이러한 지역적 추세는 각 지역이 특정 운영 요건과 전략적 우선순위에 초점을 맞추고 있지만, 수요는 세계한 성격을 띠고 있다는 점을 강조합니다.

5. 세계 장갑차 시장에서의 주요 프로그램

세계 장갑차 시장의 경쟁 구도는 전통적 방위 산업체들과 혁신과 전략적 제휴에 주력하는 신생업체들의 존재로 특징지어집니다. 주요 기업들은 보호 성능, 기동성, 디지털 통합성을 강화한 첨단 플랫폼을 도입하기 위해 연구개발에 투자하고 있습니다. 방위 산업체와 정부와의 협력 관계는 장기 계약을 확보하고 맞춤형 솔루션을 개발하는 데 있어 매우 중요한 역할을 하고 있습니다. 주요 시장 진입 기업들은 또한 다양한 임무 요건에 대응하기 위해 모듈식 설계와 확장 가능한 아키텍처에 중점을 두고 있습니다. 또한, 세계 사업 전개와 기술력 확대를 위해 합병, 인수, 합작투자 등의 전략이 광범위하게 채택되고 있습니다. 시장은 경쟁이 치열하고, 각 업체들은 혁신, 신뢰성, 라이프사이클 지원 서비스를 통해 차별화를 꾀하고 있습니다. 국방부대가 장비 현대화를 추진함에 따라 차세대 장갑 솔루션을 제공하는 주요 업계 진입자의 역할은 시장의 성장과 발전에 여전히 매우 중요합니다.

목차

장갑차 시장 - 목차

장갑차 시장 보고서의 정의

장갑차 시장 세분화

지역별

유형별

이동식 성별

구성요소별

향후 10년간의 장갑차 시장 분석

본 장에서는 10년간의 장갑차 시장 분석을 토대로 장갑차 시장의 성장, 변화하는 동향, 기술 도입 개요, 시장의 매력에 대해 상세히 조사하여 전해드립니다.

장갑차 시장의 시장 기술

이 섹션에서는 이 시장에 영향을 미칠 것으로 예상되는 상위 10가지 기술과 이러한 기술이 시장 전체에 미칠 수 있는 영향에 대해 설명합니다.

세계 장갑차 시장 전망

본 시장의 10년간 장갑차 시장 전망은 위에서 언급한 각 부문에 걸쳐 상세히 다루고 있습니다.

지역별 장갑차 시장 동향 및 전망

본 섹션에서는 지역별 장갑차 시장 동향, 촉진요인, 억제요인, 과제, 그리고 정치, 경제, 사회, 기술 측면에 대해 설명합니다. 또한 지역별 시장 예측 및 시나리오 분석에 대해서도 자세히 설명합니다. 지역 분석의 마지막 부분에서는 주요 기업 프로파일링, 공급업체 현황, 기업 벤치마킹을 다루고 있습니다. 현재 시장 규모는 일반적인 시나리오를 기준으로 추정한 것입니다.

북미

촉진요인, 억제요인, 도전과제

PEST

시장 예측 및 시나리오 분석

주요 기업

공급업체 계층 현황

기업 벤치마크

유럽

중동

아시아태평양

남미

장갑차 시장 국가별 분석

이 장에서는 이 시장의 주요 방어 프로그램에 대한 설명과 함께 이 시장에서 출원된 최신 뉴스와 특허에 대해 다룰 것입니다. 또한, 국가별 10년 시장 전망과 시나리오 분석에 대해서도 설명합니다.

미국

국방 계획

최신 뉴스

특허

이 시장의 현재 기술 성숙도

시장 예측 및 시나리오 분석

캐나다

이탈리아

프랑스

독일

네덜란드

벨기에

스페인

스웨덴

그리스

호주

남아프리카공화국

인도

중국

러시아

한국

일본

말레이시아

싱가포르

브라질

장갑차 시장의 기회 매트릭스

기회 매트릭스는 독자들이 이 시장에서 기회가 높은 부문을 이해하는 데 도움이 됩니다.

장갑차 시장 보고서에 대한 전문가의 의견

이 시장에 대한 분석 가능성에 대해 당사 전문가들의 의견을 정리해 보았습니다.

결론

항공 및 방위 시장 보고서 정보

KSM 26.05.14Global Armored Vehicle Market

The Global Armored Vehicle Market is estimated at USD 25.19 billion in 2026, projected to grow to USD 29.27 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 1.51% over the forecast period 2026-2036.

1. Introduction

The Global Armored Vehicle Market represents a critical segment within the broader defense and security industry, focusing on platforms designed to enhance battlefield survivability, mobility, and combat effectiveness. Armored vehicles include a wide range of systems such as main battle tanks, infantry fighting vehicles, armored personnel carriers, and mine-resistant vehicles. These platforms are extensively deployed by military forces, law enforcement agencies, and security organizations to operate in hostile and high-risk environments. The growing complexity of modern warfare, including asymmetric threats and urban combat scenarios, has significantly increased the reliance on advanced armored mobility solutions. Additionally, defense modernization initiatives and the need to replace aging fleets are shaping procurement strategies worldwide. Technological advancements in protection systems, mobility enhancements, and digital battlefield integration are further transforming the market, positioning armored vehicles as indispensable assets in both conventional and hybrid warfare environments.

2. Technology Impact in Global Armored Vehicle Market

Technological innovation is redefining the operational capabilities of armored vehicles, making them more adaptive, survivable, and network-centric. Modern platforms are increasingly equipped with active protection systems that detect and neutralize incoming threats, significantly enhancing crew safety. Hybrid and electric propulsion technologies are being explored to improve fuel efficiency, reduce thermal signatures, and enable silent mobility in tactical environments. Additionally, advancements in modular armor design allow for rapid upgrades and customization based on mission requirements. Digitalization plays a crucial role, with vehicles now integrated into network-centric warfare systems, enabling real-time data sharing, situational awareness, and coordinated operations. Autonomous and optionally manned vehicle technologies are also gaining traction, allowing forces to conduct high-risk missions with reduced human exposure. Artificial intelligence and advanced sensors further enhance navigation, threat detection, and decision-making capabilities, ensuring that armored vehicles remain effective in increasingly complex and data-driven combat scenarios.

3. Key Drivers in Global Armored Vehicle Market

The growth of the Global Armored Vehicle Market is driven by several strategic and operational factors. Increasing geopolitical tensions and regional conflicts have heightened the demand for advanced land combat systems, prompting governments to invest in modernization programs. The need to enhance troop protection against improvised explosive devices and ballistic threats is another major driver, leading to the adoption of heavily armored and mine-resistant platforms. Additionally, military forces are focusing on improving mobility and rapid deployment capabilities, which has accelerated the demand for versatile and lightweight armored vehicles. The rise of asymmetric warfare and counterinsurgency operations further emphasizes the importance of adaptable and technologically advanced platforms. Government initiatives aimed at strengthening domestic defense manufacturing and reducing dependency on imports also contribute to market expansion. Furthermore, evolving battlefield requirements and the integration of advanced weapon systems continue to stimulate demand for next-generation armored vehicles.

4. Regional Trends in Global Armored Vehicle Market

Regional dynamics in the Global Armored Vehicle Market are shaped by varying defense priorities, budget allocations, and geopolitical environments. North America remains a significant market due to continuous investments in modernization and advanced combat vehicle programs. Europe is witnessing strong demand driven by fleet recapitalization efforts and increased defense cooperation among regional nations. The Asia-Pacific region is emerging as a key growth area, fueled by rising security concerns, border tensions, and large-scale procurement programs in countries such as India and China. The Middle East continues to invest heavily in armored vehicles to address ongoing regional conflicts and enhance military capabilities. Meanwhile, Latin America and Africa are gradually adopting armored platforms to strengthen internal security and peacekeeping operations. These regional trends highlight the global nature of demand, with each region focusing on specific operational requirements and strategic priorities.

5. Key Global Armored Vehicle Market Program

The competitive landscape of the Global Armored Vehicle Market is characterized by the presence of established defense manufacturers and emerging players focused on innovation and strategic partnerships. Leading companies are investing in research and development to introduce advanced platforms featuring enhanced protection, mobility, and digital integration. Collaboration between defense contractors and governments plays a crucial role in securing long-term contracts and developing customized solutions. Key market participants are also emphasizing modular designs and scalable architectures to cater to diverse mission requirements. Additionally, mergers, acquisitions, and joint ventures are common strategies used to expand global presence and technological capabilities. The market is highly competitive, with companies striving to differentiate themselves through innovation, reliability, and lifecycle support services. As defense forces continue to modernize their fleets, the role of key industry players in delivering next-generation armored solutions remains vital to market growth and evolution.

Table of Contents

Armored Vehicle Market - Table of Contents

Armored Vehicle Market Report Definition

Armored Vehicle Market Segmentation

By Region

By Type

By Mobility

By Components

Armored Vehicle Market Analysis for next 10 Years

The 10-year armored vehicle market analysis would give a detailed overview of armored vehicle market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Armored Vehicle Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Armored Vehicle Market Forecast

The 10-year armored vehicle market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Armored Vehicle Market Trends & Forecast

The regional armored vehicle market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Armored Vehicle Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Armored Vehicle Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Armored Vehicle Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports