|

시장보고서

상품코드

2060411

주력전차용 열 카메라 시장(2026-2036년)Main Battle Tank Thermal Camera 2026-2036 |

||||||

세계의 주력전차용 열 카메라 시장

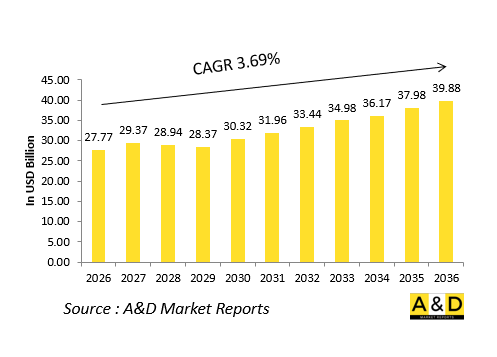

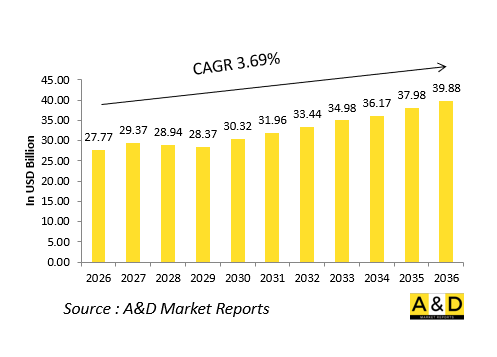

주력전차용 열 카메라 시장 규모는 2026년에 277억 7,000만 달러로 추계되고 있으며, 2026-2036년의 예측 기간에 CAGR 3.69%로 성장하며, 2036년에는 398억 8,000만 달러에 달할 것으로 전망되고 있습니다.

서론

주력 전차용 열화상 카메라는 완전한 암흑이나 연기, 안개, 그 밖의 전장에서 시야를 가리는 조건에서도 선명한 시야를 제공하도록 설계된 첨단 전기광학 감지 시스템입니다. 이러한 시스템은 물체에서 방출되는 적외선을 감지하여 가시광선 이미지로 변환함으로써, 전차 승무원이 표적을 식별하고 열악한 환경에서도 정확하게 항행할 수 있게 해줍니다. 이를 통해 상황 인식 능력이 크게 향상되어, 기갑 부대는 가시광선에 의존하지 않고 주야를 가리지 않고 효과적으로 작전을 전개할 수 있게 됩니다. 열화상 시스템은 일반적으로 현대 전차의 사격 통제 아키텍처에 통합되어 있으며, 표적 포착, 추적 및 교전을 지원합니다. 인원, 차량, 장비에서 발산되는 열 신호를 탐지하는 이 능력은 현대 장갑전에서 결정적인 전술적 우위를 가져다줍니다. 전장 환경이 점점 더 복잡해짐에 따라 열화상 카메라는 해상도 향상, 탐지 거리 확대, 그리고 대응 조치에 대한 내성 강화와 함께 지속적으로 발전하고 있으며, 장갑차 현대화 프로그램에서 필수적인 구성 요소로 자리 잡고 있습니다.

주력 전차용 열화상 카메라 시장에 미치는 기술적 영향

기술의 발전에 따라 장갑 플랫폼에 탑재된 열화상 시스템의 성능과 용도는 근본적으로 변화했습니다. 현대식 센서는 더욱 선명한 영상, 향상된 열 감도, 그리고 빠른 처리 속도를 구현하고 있으며, 승무원들은 다양한 환경에서도 표적을 보다 정확하게 식별할 수 있게 되었습니다. 디지털 통합을 통해 열화상 데이터와 레이저 거리 측정기, 주간용 카메라 등 다른 전장 센서와의 원활한 융합이 가능해짐에 따라 통합 전투 시각 시스템이 구축되고 있습니다. 인공지능(AI)을 활용한 이미지 처리는 표적 인식 능력을 한층 더 향상시키고, 작업자의 업무 부담을 줄여줍니다. 부품의 소형화로 인해 차량 중량을 늘리지 않고도 콤팩트한 포탑 시스템으로 통합할 수 있게 되었습니다. 또한 소재 및 냉각 기술의 발전으로 인해 가혹한 조건 하에서도 운용 신뢰성이 향상되었습니다. 이러한 발전은 반응 시간을 단축하고 교전 정확도를 높임으로써 종합적인 전투 효과를 향상시키고 있습니다. 방위 부대가 장갑차량군을 현대화하는 가운데, 열화상 기술은 더 높은 자율성, 네트워크화된 전장 통합, 그리고 전자전 간섭에 대한 내성 강화를 위해 지속적으로 발전하고 있습니다.

주력 전차용 열화상 카메라 시장의 주요 성장 동인

주력 전차에 대한 첨단 열화상 시스템에 대한 수요는 주로 모든 기상 조건 하에서 뛰어난 전장 상황 파악 능력과 작전상의 우위를 확보하려는 요구가 높아짐에 따라 주도되고 있습니다. 현대 전쟁에서는 신속한 표적 탐지와 정밀한 공격이 중요시되고 있으며, 이로 인해 군은 첨단 전기광학 시스템의 도입을 요구받고 있습니다. 지정학적 긴장이 고조되고 국경 경비에 대한 우려도 커지면서, 장갑차 현대화 프로그램에 대한 투자가 가속화되고 있습니다. 야간 작전이나 시야가 불량한 전투 환경으로의 전환은 신뢰성이 높은 적외선 영상 시스템의 필요성을 더욱 강조하고 있습니다. 또 다른 주요 촉진요인은 수명과 전투 능력을 연장하기 위해 기존 장갑차량을 첨단 사격 통제 시스템 및 센서 시스템으로 지속적으로 업그레이드하고 있다는 점입니다. 디지털 전장 네트워크 및 자동 조준 시스템과의 통합을 포함한 기술의 융합 또한 도입을 지원하고 있습니다. 또한 일부 국가에서 국방 예산이 증가함에 따라 고성능 열화상 카메라를 탑재한 차세대 장갑 플랫폼의 조달이 지원되고 있으며, 이는 복잡한 전투 상황에서 생존성과 임무 수행 능력을 확실히 향상시키고 있습니다.

주력 전차용 열화상 카메라 시장의 지역별 동향

주력 전차에 대한 열화상 시스템의 지역별 도입 현황은 국방 현대화의 우선순위와 전략적 요건에 따라 달라집니다. 북미에서는 장갑차 부대의 지속적인 현대화와 첨단 센서 통합에 대한 중점이 고해상도 열화상 시스템의 대대적인 도입을 주도하고 있습니다. 유럽에서는 공동 방위 프로그램과 기존 전차 플랫폼의 현대화에 중점을 두고 있으며, 멀티센서 융합 기술에 막대한 투자가 이루어지고 있습니다. 아시아태평양에서는 국방비 증가와 영토 안보에 대한 우려가 커짐에 따라 첨단 열화상 기능을 갖춘 최신형 장갑차량의 조달이 가속화되고 있습니다. 또한 이 지역의 각국은 외부 공급업체에 대한 의존도를 낮추기 위해 국내 개발과 기술 이전을 중시하고 있습니다. 중동 지역에서는 가혹한 환경 조건과 안보상 과제로 인해, 폭염이나 시야 불량 상황에서도 정상적으로 작동하는 열화상 시스템에 대한 수요가 증가하고 있습니다. 한편, 그 밖의 신흥 지역에서는 보다 광범위한 국방 능력 강화 프로그램의 일환으로 이러한 기술들이 점차 도입되고 있습니다.

주력 전차용 열화상 카메라의 주요 프로그램

전 세계 방위 현대화 노력의 일환으로, 주력 전차 플랫폼에 첨단 열화상 시스템을 통합하는 것이 매우 중요하게 여겨지고 있습니다. 이러한 프로그램들은 일반적으로 표적 탐지 능력, 생존성 및 교전 정확도의 향상을 통해 전투 준비 태세 강화에 중점을 두고 있습니다. 많은 현대화 사업에서 고해상도 열화상 카메라를 핵심 구성 요소로 하는 차세대 화기 관제 시스템을 활용하여 구형 전차를 개량하고 있습니다. 동맹국 간의 공동 방위 프로젝트는 종종 장갑차량군 전체에 걸친 센서 기술의 표준화를 목표로 하며, 상호 운용성과 작전 능력의 공유를 보장하고 있습니다. 국내 개발 프로그램도 탄력을 받고 있으며, 전략적 자율성을 강화하기 위해 여러 국가가 적외선 영상 시스템의 국내 생산에 투자하고 있습니다. 또한 장기적인 조달 전략에서는 모듈식 업그레이드 경로가 중시되고 있으며, 차량 시스템 전체를 재설계하지 않고도 열화상 장치를 교체하거나 기능을 강화할 수 있습니다. 이러한 프로그램들은 전반적으로 디지털 기술을 활용한 장갑전으로의 광범위한 전환을 반영하고 있으며, 그중에서도 열화상 기술은 전장에서의 우위와 작전상의 유연성을 확보하는 데 핵심적인 역할을 하고 있습니다.

목차

주력전차용 열 카메라 시장 - 목차

주력전차용 열 카메라 시장 보고서의 정의

주요 전투용 열 카메라 시장 세분화

향후 10년간의 주요 전투용 열 카메라 시장 분석

세계의 주력 전투용 열 카메라 시장 예측

지역별 주요 전투용 열 카메라 시장의 동향과 예측

시장 예측과 시나리오 분석

주요 전투용 열 카메라 시장의 국가별 분석

시장 예측과 시나리오 분석

주력전차용 열 카메라 시장의 기회 매트릭스

결론

KSA 26.06.24Global Main Battle Tank Thermal Camera Market

The Main Battle Tank Thermal Camera is estimated at USD 27.77 billion in 2026, projected to grow to USD 39.88 billion by 2036 at a Compound Annual Growth Rate (CAGR) of 3.69% over the forecast period 2026-2036.

Introduction

Main Battle Tank thermal cameras are advanced electro-optical sensing systems designed to provide clear vision in complete darkness, smoke, fog, and other battlefield obscurants. These systems detect infrared radiation emitted by objects and convert it into a visible image, enabling tank crews to identify targets and navigate challenging environments with precision. They significantly enhance situational awareness, allowing armored units to operate effectively during day and night operations without reliance on visible light. Thermal imaging systems are typically integrated into the fire control architecture of modern tanks, supporting target acquisition, tracking, and engagement. Their ability to detect heat signatures from personnel, vehicles, and equipment provides a critical tactical advantage in modern armored warfare. As battlefield environments become more complex, thermal cameras continue to evolve with improved resolution, longer detection range, and better resistance to countermeasures, making them an essential component of armored vehicle modernization programs.

Technology Impact in Main Battle Tank Thermal Camera Market

Technological advancements have fundamentally reshaped the performance and application of thermal imaging systems in armored platforms. Modern sensors now deliver higher image clarity, improved thermal sensitivity, and faster processing speeds, allowing crews to distinguish targets more accurately in cluttered environments. Digital integration has enabled seamless fusion of thermal imaging with other battlefield sensors such as laser range finders and day cameras, creating a unified combat vision system. Artificial intelligence assisted image processing further enhances target recognition and reduces operator workload. Miniaturization of components has allowed integration into compact turret systems without increasing vehicle weight. Additionally, improved materials and cooling technologies have extended operational reliability under extreme conditions. These advancements collectively enhance combat effectiveness by reducing reaction time and improving engagement accuracy. As defense forces modernize armored fleets, thermal imaging technology continues to evolve toward higher autonomy, networked battlefield integration, and enhanced resistance to electronic warfare interference.

Key Drivers in Main Battle Tank Thermal Camera Market

The demand for advanced thermal imaging systems in main battle tanks is primarily driven by the growing need for superior battlefield awareness and operational superiority in all weather conditions. Modern warfare emphasizes rapid target detection and precision engagement, pushing armed forces to adopt advanced electro-optical systems. Increasing geopolitical tensions and border security concerns have also accelerated investments in armored vehicle modernization programs. The shift toward night operations and low visibility combat environments further strengthens the need for reliable infrared imaging systems. Another major driver is the continuous upgrade of legacy armored fleets with advanced fire control and sensor systems to extend service life and combat capability. Technological convergence, including integration with digital battlefield networks and automated targeting systems, also fuels adoption. Additionally, rising defense budgets in several countries support procurement of next generation armored platforms equipped with high performance thermal cameras, ensuring enhanced survivability and mission effectiveness in complex combat scenarios.

Regional Trends in Main Battle Tank Thermal Camera Market

Regional adoption of thermal imaging systems in main battle tanks varies based on defense modernization priorities and strategic requirements. In North America, continuous upgrades to armored vehicle fleets and emphasis on advanced sensor integration drive strong adoption of high resolution thermal systems. Europe focuses on collaborative defense programs and modernization of existing tank platforms, with significant investments in multi sensor fusion technologies. In the Asia Pacific region, increasing defense spending and territorial security concerns are accelerating procurement of modern armored vehicles equipped with advanced thermal imaging capabilities. Countries in this region are also emphasizing domestic development and technology transfer to reduce dependency on external suppliers. In the Middle East, harsh environmental conditions and security challenges have led to strong demand for thermal systems capable of performing in extreme heat and low visibility conditions. Meanwhile, other emerging regions are gradually adopting these technologies as part of broader defense capability enhancement programs.

Key Main Battle Tank Thermal Camera Program

Global defense modernization initiatives have placed strong emphasis on integrating advanced thermal imaging systems into main battle tank platforms. These programs typically focus on enhancing combat readiness through improved target detection, survivability, and engagement accuracy. Many modernization efforts involve upgrading legacy tanks with next generation fire control systems that include high resolution thermal cameras as a core component. Collaborative defense projects between allied nations often aim to standardize sensor technologies across armored fleets, ensuring interoperability and shared operational capability. Indigenous development programs are also gaining momentum, with several countries investing in domestic production of infrared imaging systems to strengthen strategic autonomy. Additionally, long term procurement strategies emphasize modular upgrade paths, allowing thermal imaging units to be replaced or enhanced without redesigning entire vehicle systems. These programs collectively reflect a broader shift toward digitally enabled armored warfare, where thermal imaging plays a central role in ensuring battlefield dominance and operational flexibility.

Table of Contents

Main Battle Thermal Camera Market - Table of Contents

Main Battle Thermal Camera Market Report Definition

Main Battle Thermal Camera Market Segmentation

By Type

By Technology

By Region

Main Battle Thermal Camera Market Analysis for next 10 Years

The 10-year Main Battle thermal camera market analysis would give a detailed overview of Main Battle thermal camera market growth, changing dynamics, technology adoption overviews and the overall market attractiveness is covered in this chapter.

Market Technologies of Main Battle Thermal Camera Market

This segment covers the top 10 technologies that is expected to impact this market and the possible implications these technologies would have on the overall market.

Global Main Battle Thermal Camera Market Forecast

The 10-year Main Battle thermal camera market forecast of this market is covered in detailed across the segments which are mentioned above.

Regional Main Battle Thermal Camera Market Trends & Forecast

The regional counter drone market trends, drivers, restraints and Challenges of this market, the Political, Economic, Social and Technology aspects are covered in this segment. The market forecast and scenario analysis across regions are also covered in detailed in this segment. The last part of the regional analysis includes profiling of the key companies, supplier landscape and company benchmarking. The current market size is estimated based on the normal scenario.

North America

Drivers, Restraints and Challenges

PEST

Market Forecast & Scenario Analysis

Key Companies

Supplier Tier Landscape

Company Benchmarking

Europe

Middle East

APAC

South America

Country Analysis of Main Battle Thermal Camera Market

This chapter deals with the key defense programs in this market, it also covers the latest news and patents which have been filed in this market. Country level 10 year market forecast and scenario analysis are also covered in this chapter.

US

Defense Programs

Latest News

Patents

Current levels of technology maturation in this market

Market Forecast & Scenario Analysis

Canada

Italy

France

Germany

Netherlands

Belgium

Spain

Sweden

Greece

Australia

South Africa

India

China

Russia

South Korea

Japan

Malaysia

Singapore

Brazil

Opportunity Matrix for Main Battle Thermal Camera Market

The opportunity matrix helps the readers understand the high opportunity segments in this market.

Expert Opinions on Main Battle Thermal Camera Market Report

Hear from our experts their opinion of the possible analysis for this market.

Conclusions

About Aviation and Defense Market Reports