|

시장보고서

상품코드

1959604

질량유량계(MFC) 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Mass Flow Controller Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

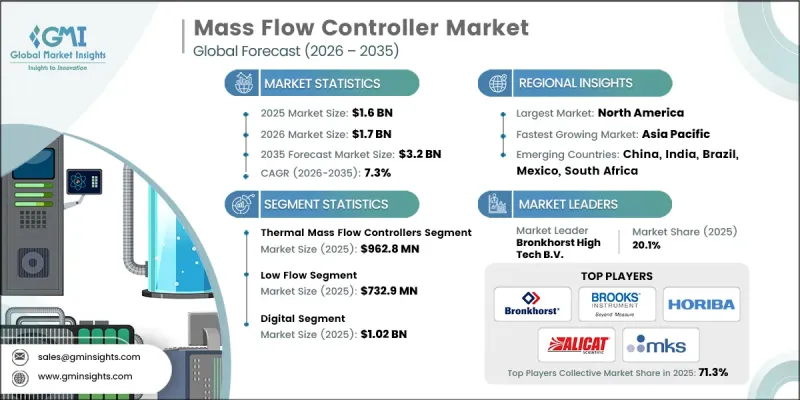

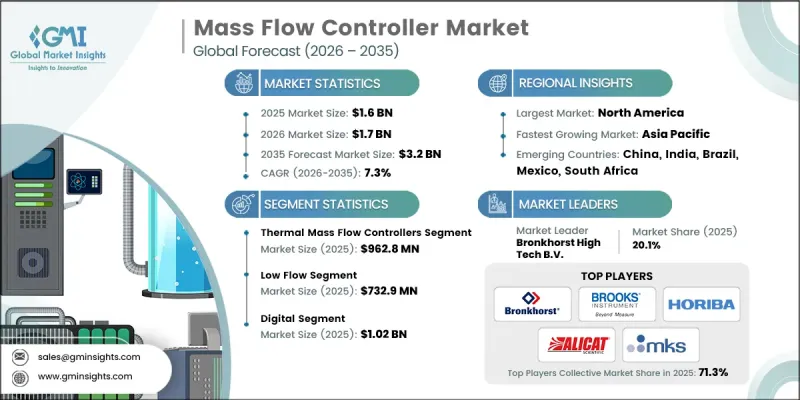

세계의 질량유량계(MFC) 시장은 2025년에 16억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 7.3%로 성장하여 32억 달러에 이를 것으로 예측됩니다.

이러한 성장은 반도체, 항공우주, 화학, 에너지, 제조 등의 산업 분야에서 자동화 및 정밀 제어 기술 채택이 확대되면서 성장하고 있습니다. 산업 공정이 더욱 복잡해지고 생산량에 대한 수요가 증가함에 따라 정밀하고 신뢰할 수 있는 유량 측정 시스템의 필요성이 증가하고 있습니다. 질량유량계(MFC)는 가스 및 액체의 유량을 정확하게 조절하고 공정 안정성, 품질 일관성 및 안전 표준 준수를 보장하는 데 필수적입니다. 반도체 제조 및 첨단 제조 작업의 확장은 시장을 더욱 가속화하고 있습니다. 성막, 에칭, 화학 기상 성장과 같은 중요한 공정에서는 높은 재현성과 컴팩트한 통합성이 요구됩니다. 또한, 인더스트리 4.0 및 스마트 제조로의 전환은 디지털 및 IIoT 호환 질량유량계(MFC)에 대한 수요를 주도하고 있으며, 실시간 모니터링, 다운타임 감소 및 운영 효율성 향상을 통해 고정밀 산업 전반에 걸쳐 MFC 도입의 가치를 강화합니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 가치 | 16억 달러 |

| 예측 금액 | 32억 달러 |

| CAGR | 7.3% |

열식 질량 유량 제어기(Thermal MFC) 부문은 2025년 9억 6,280만 달러 시장 규모를 형성할 것으로 예측됩니다. 이 컨트롤러는 반도체 제조, 화학제품 생산, 청정 기술 운영에서 정밀한 유량 측정을 유지할 수 있는 능력으로 시장을 독점하고 있습니다. 열식 MFC는 열악한 공정 환경에서도 빠른 응답 시간, 일관된 재현성, 장기적인 내구성을 제공합니다. 다양한 조건에서 가스 유량을 정확하게 제어할 수 있는 능력은 중요한 용도에서 공정 안정성과 운영 효율성을 유지하는 데 필수적입니다.

저유량 부문은 2025년 7억 3,290만 달러로 반도체 제조, 제약, 분석 공정에서 중요한 응용 분야로 인해 가장 큰 시장 점유율을 유지했습니다. 저유량 MFC는 소량의 액체나 가스를 조절할 때 빠른 응답성, 정확성, 반복성을 제공하므로 고정밀 작업에 선호됩니다. 이러한 특성으로 인해 작은 편차도 품질과 수율에 영향을 미치는 공정에서 없어서는 안 될 존재가 되었습니다.

북미 질량유량계(MFC) 시장은 자동화, 스마트 제조, 디지털 공정 제어의 높은 도입률에 힘입어 2025년 31.4%의 점유율을 차지할 것으로 예측됩니다. 반도체, 화학, 에너지, 제약 등의 산업 분야에서는 IIoT 지원 MFC, 예지보전, 고급 분석을 활용하여 운영 최적화, 다운타임 감소, 공정 안정성 유지를 위해 노력하고 있습니다. 에너지 효율성, 지속가능성, 규제 준수에 대한 관심이 높아지면서 지역 전체에서 신뢰할 수 있는 고정밀 질량유량계(MFC)에 대한 수요가 더욱 증가하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

제4장 경쟁 구도

제5장 시장 추산 및 예측 : 기술별, 2022-2035

제6장 시장 추산 및 예측 : 접속 방식별, 2022-2035

제7장 시장 추산 및 예측 : 매체 유형별, 2022-2035

제8장 시장 추산 및 예측 : 유량 용량별, 2022-2035

제9장 시장 추산 및 예측 : 최종 용도별, 2022-2035

제10장 시장 추산 및 예측 : 지역별, 2022-2035

제11장 기업 개요

LSH 26.03.16The Global Mass Flow Controller Market was valued at USD 1.6 billion in 2025 and is estimated to grow at a CAGR of 7.3% to reach USD 3.2 billion by 2035.

The growth is fueled by increasing adoption of automation and precision control technologies across industries such as semiconductors, aerospace, chemicals, energy, and manufacturing. As industrial processes become more complex and output demands rise, the need for precise, reliable flow measurement systems has intensified. Mass flow controllers are essential for accurately regulating gas and liquid flows, ensuring process stability, quality consistency, and adherence to safety standards. The expansion of semiconductor fabrication and advanced manufacturing operations is further accelerating the market. Critical processes such as deposition, etching, and chemical vapor applications require high repeatability and compact integration. In addition, the push toward Industry 4.0 and smart manufacturing drives demand for digitally enabled and IIoT-compatible mass flow controllers, offering real-time monitoring, reduced downtime, and increased operational efficiency, ultimately reinforcing the value of MFC adoption across high-precision industries.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $1.6 Billion |

| Forecast Value | $3.2 Billion |

| CAGR | 7.3% |

The thermal mass flow controllers segment generated USD 962.8 million in 2025. These controllers dominate because of their ability to maintain precise flow measurements in semiconductor fabrication, chemical production, and clean technology operations. Thermal MFCs provide rapid response times, consistent repeatability, and long-term durability even in demanding process environments. Their capability to control gas flows accurately under varying conditions makes them indispensable for maintaining process stability and operational efficiency in critical applications.

The low flow segment accounted for USD 732.9 million in 2025, maintaining the largest market share due to its critical applications in semiconductor manufacturing, pharmaceuticals, and analytical processes. Low flow MFCs are preferred for high-precision tasks, offering fast response, accuracy, and repeatability when regulating small volumes of liquids or gases. These features make them essential for processes where even minor deviations can affect quality and yield.

North America Mass Flow Controller Market held a 31.4% share in 2025, driven by high adoption of automation, smart manufacturing, and digital process control. Industrial sectors, including semiconductors, chemicals, energy, and pharmaceuticals, leverage IIoT-enabled MFCs, predictive maintenance, and advanced analytics to optimize operations, reduce downtime, and maintain process stability. Growing emphasis on energy efficiency, sustainability, and regulatory compliance is further boosting demand for reliable, high-precision mass flow controllers across the region.

Key players in the Global Mass Flow Controller Market include Brooks Instrument, Alicat Scientific, Inc., MKS Instruments, Inc., Azbil Corporation, Bronkhorst High Tech B.V., Christian Burkert GmbH & Co. KG, Fujikin Incorporated, HORIBA Ltd., KOFLOC Corporation, Parker Hannifin Corporation, Sensirion AG, Sierra Instruments, Inc., Teledyne Hastings Instruments, Tokyo Keiso Co., Ltd., and Vogtlin Instruments GmbH. Companies are strengthening their Global Mass Flow Controller Market presence through continuous R&D and technology development, focusing on high-precision, reliable, and digitally compatible controllers. Strategic partnerships with semiconductor, chemical, and energy firms enable tailored solutions for complex industrial applications. Firms are investing in IIoT-enabled controllers, real-time monitoring, predictive maintenance, and analytics to enhance operational efficiency and minimize downtime. Expansion into emerging markets, flexible pricing models, and customer support services improve accessibility. Companies are also emphasizing sustainability, energy efficiency, and compact designs for space-limited applications.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Sensor type trends

- 2.2.2 Technology trends

- 2.2.3 Connectivity trends

- 2.2.4 End Use industry trends

- 2.2.5 Regional trends

- 2.3 TAM analysis, 2025-2035

- 2.4 CXO perspectives: Strategic imperatives

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Expansion of Semiconductor and Electronics Manufacturing

- 3.2.1.2 Integration of Digitalization and Industry 4.0 Technologies

- 3.2.1.3 Growth in Renewable Energy and Clean Technology Applications

- 3.2.1.4 Expansion in Pharmaceuticals, Chemical Processing and Biotechnology Sectors

- 3.2.1.5 Regional Industrialization & Manufacturing Investment

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High Cost of Advanced MFCs

- 3.2.2.2 Complex Integration with Existing Systems

- 3.2.3 Market opportunities

- 3.2.3.1 IoT-Enabled and Smart MFC Solutions

- 3.2.3.2 Expansion in Emerging Markets

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Pricing Strategies

- 3.10 Emerging Business Models

- 3.11 Compliance Requirements

- 3.12 Geopolitical and trade dynamics

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East & Africa

- 4.2.1 By region

- 4.3 Competitive benchmarking of key players

- 4.3.1 Financial performance comparison

- 4.3.1.1 Revenue

- 4.3.1.2 Profit margin

- 4.3.1.3 R&D

- 4.3.2 Product portfolio comparison

- 4.3.2.1 Product range breadth

- 4.3.2.2 Technology

- 4.3.2.3 Innovation

- 4.3.3 Geographic presence comparison

- 4.3.3.1 Global footprint analysis

- 4.3.3.2 Service network coverage

- 4.3.3.3 Market penetration by region

- 4.3.4 Competitive positioning matrix

- 4.3.4.1 Leaders

- 4.3.4.2 Challengers

- 4.3.4.3 Followers

- 4.3.4.4 Niche players

- 4.3.1 Financial performance comparison

- 4.4 Key developments, 2022-2025

- 4.4.1 Mergers and acquisitions

- 4.4.2 Partnerships and collaborations

- 4.4.3 Technological advancements

- 4.4.4 Expansion and investment strategies

- 4.4.5 Digital transformation initiatives

- 4.5 Emerging/ startup competitors landscape

Chapter 5 Market Estimates and Forecast, By Technology, 2022 - 2035 (USD Million)

- 5.1 Key trends

- 5.2 Thermal mass flow controllers

- 5.3 Coriolis mass flow controllers

- 5.4 Differential pressure mass flow controllers

- 5.5 Ultrasonic / emerging mass flow controllers

Chapter 6 Market Estimates and Forecast, By Connectivity, 2022 - 2035 (USD Million)

- 6.1 Key trends

- 6.2 Analog

- 6.3 Digital

Chapter 7 Market Estimates and Forecast, By Media Type, 2022 - 2035 (USD Million)

- 7.1 Key trends

- 7.2 Gas

- 7.3 Liquid

Chapter 8 Market Estimates and Forecast, By Flow Rate Capacity, 2022 - 2035 (USD Million)

- 8.1 Key trends

- 8.2 Low flow

- 8.3 Medium flow

- 8.4 High flow

Chapter 9 Market Estimates and Forecast, By End-use Application, 2022 - 2035 (USD Million)

- 9.1 Key trends

- 9.2 Semiconductor & Electronics

- 9.2.1 Chemical Vapor Deposition (CVD)

- 9.2.2 Physical Vapor Deposition (PVD)

- 9.2.3 Thermal processing & diffusion

- 9.2.4 Others

- 9.3 Chemicals & specialty chemicals

- 9.3.1 Chemical reaction control

- 9.3.2 Spray & coating processes

- 9.3.3 Gas blending & mixing

- 9.3.4 Others

- 9.4 Environmental & utilities

- 9.4.1 Water & wastewater treatment

- 9.4.2 Air quality monitoring & emissions

- 9.4.3 Others

- 9.5 Pharmaceuticals & biotechnology

- 9.6 Energy & advanced materials

- 9.7 Metals & mining

- 9.8 Food & beverage

- 9.9 Aerospace & defense

- 9.10 Medical & healthcare

- 9.11 Others

Chapter 10 Market Estimates and Forecast, By Region, 2022 - 2035 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Alicat Scientific, Inc.

- 11.2 Azbil Corporation

- 11.3 Bronkhorst High-Tech B.V.

- 11.4 Brooks Instrument

- 11.5 Christian Burkert GmbH & Co. KG

- 11.6 Fujikin Incorporated

- 11.7 HORIBA Ltd.

- 11.8 KOFLOC Corporation

- 11.9 MKS Instruments, Inc.

- 11.10 Parker Hannifin Corporation

- 11.11 Sensirion AG

- 11.12 Sierra Instruments, Inc.

- 11.13 Teledyne Hastings Instruments

- 11.14 Tokyo Keiso Co., Ltd.

- 11.15 Vogtlin Instruments GmbH