|

시장보고서

상품코드

1892828

가이드와이어 시장 기회, 성장요인, 업계 동향 분석 및 예측(2025-2034년)Guidewires Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

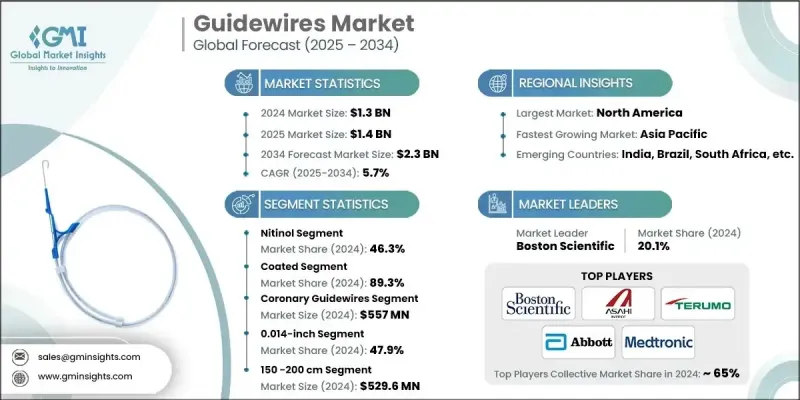

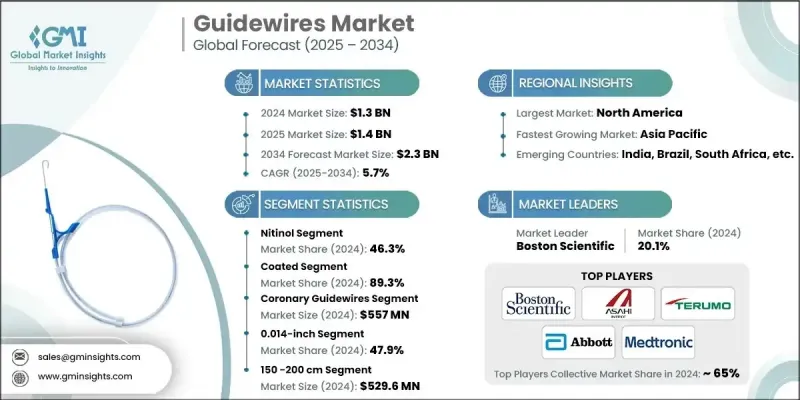

세계의 가이드와이어 시장은 2024년에 13억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 5.7%로 성장하여 23억 달러에 이를 것으로 예측됩니다.

시장 확대의 주요 요인으로는 고령화 인구 증가, 생활습관병 유병률 증가, 선진국의 의료보험제도 지원책, 심혈관질환 유병률 증가 등을 꼽을 수 있습니다. 또한, 스마트 가이드와이어, 생체 흡수성 모델과 같은 설계 기술의 발전이 도입을 촉진하고 있습니다. 의료 현장에서 기존 수술에서 경피적 관상동맥 중재술(PCI), 신경혈관 중재술, 혈관 내 치료 등 저침습적 시술로의 전환이 시장 성장에 크게 기여하고 있습니다. 이러한 시술은 신체에 가해지는 부담을 줄이고, 입원 기간을 단축하며, 회복을 촉진합니다. 가이드와이어는 임상의가 복잡한 혈관 구조를 정밀하게 탐색하는 데 중요한 역할을 하여 시술 성공률과 환자 결과를 개선하는 데 도움을 줍니다. 신흥국의 의료 인프라 확충도 가이드와이어 도입의 새로운 기회를 창출하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 기간 | 2025-2034년 |

| 개시 연도 시장 규모 | 13억 달러 |

| 예측 금액 | 23억 달러 |

| CAGR | 5.7% |

2024년 니티놀 부문은 46.3%의 점유율을 차지했습니다. 이 부문은 유리한 상환 정책과 형상기억 특성 및 초탄성과 같은 우수한 재료 특성으로 인해 심혈관, 말초혈관, 신경혈관 수술에서 복잡한 혈관 내를 탐색할 때 유연성과 굴곡 저항성을 높여주기 때문에 앞으로도 계속 성장할 것으로 예측됩니다.

코팅 부문은 2024년 89.3%의 점유율을 차지할 것으로 예측됩니다. 친수성, 항혈전성, 소수성, 실리콘 기반 기술을 이용한 코팅된 가이드와이어는 임상적 효율성과 인터벤션 시술에 광범위하게 사용되어 선호되고 있습니다.

북미 가이드와이어 시장은 2024년 37.7%의 점유율을 차지했습니다. 이 지역은 선진화된 의료 인프라, 높은 시술 건수, 저침습적 중재 치료의 급속한 보급, 지속적인 기술 혁신의 혜택을 누리고 있습니다. 심혈관질환, 말초동맥질환, 신경혈관질환, 비뇨기질환의 높은 유병률이 진단용 및 치료용 가이드와이어 수요를 견인하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 미국

- 캐나다

- 유럽

- 중국

- 북미

- 기술과 혁신 동향

- 현재 기술 동향

- 강화된 친수성·소수성 코팅 기술

- 토크 제어와 조종성 최적화

- 다층 복합재료 통합

- 신기술

- 나노테크놀러지 강화 표면 처리 기술

- 자기유도 내비게이션 시스템

- 3D 프린팅에 의한 개별 대응 가이드와이어 시작품

- 현재 기술 동향

- 향후 시장 동향

- 완전 통합형 디지털 인터벤션 스위트에의 이동이 가속

- 일회용·멸균 상태 및 비용 효율이 뛰어난 가이드와이어 수요 증가

- 저침습 및 외래 기반 치료법 확대

- 상환 시나리오

- 지역별 가격 분석 2024

- 소재별

- 용도별

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추산 및 예측 : 재료별, 2021-2034

- 주요 동향

- 니티놀

- 스테인리스 스틸

- 하이브리드

- 기타 재료

제6장 시장 추산 및 예측 : 코팅별, 2021-2034

- 주요 동향

- 코팅

- 친수성 코팅

- 항혈전성/헤파린 코팅

- 소수성 코팅

- 실리콘 코팅

- 테트라 플루오르 에틸렌(TFE) 코팅

- 무코팅

제7장 시장 추산 및 예측 : 용도별, 2021-2034

- 주요 동향

- 관상동맥용 가이드와이어

- 말초용 가이드와이어

- 비뇨기과용 가이드와이어

- 신경혈관용 가이드와이어

- 기타 용도

제8장 시장 추산 및 예측 : 직경별, 2021-2034

- 주요 동향

- 0.014인치

- 0.018인치

- 0.025인치

- 0.032인치

- 0.035인치

- 0.038인치

제9장 시장 추산 및 예측 : 길이별, 2021-2034

- 주요 동향

- 80-145cm

- 150-200cm

- 210-300cm

- 305cm 이상

제10장 시장 추산 및 예측 : 최종 용도별, 2021-2034

- 주요 동향

- 병원

- 외래수술센터(ASC)

- 기타 용도

제11장 시장 추산 및 예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트(UAE)

제12장 기업 개요

- Abbott Laboratories

- AngioDynamics

- ASAHI INTECC

- B. Braun SE

- Becton, Dickinson and Company

- Boston Scientific

- Cordis

- Cook Medical

- Medtronic

- Merit Medical Systems

- Olympus

- Stryker

- Teleflex

- Terumo

The Global Guidewires Market was valued at USD 1.3 billion in 2024 and is estimated to grow at a CAGR of 5.7% to reach USD 2.3 billion by 2034.

Market expansion is driven by the rising elderly population, increasing prevalence of lifestyle-related disorders, supportive reimbursement policies in developed countries, and growing rates of cardiovascular diseases. Technological advancements in guidewire design, such as smart and bioresorbable models, are further fueling adoption. The shift in healthcare from traditional open surgeries to minimally invasive procedures, including Percutaneous Coronary Intervention (PCI), neurovascular interventions, and endovascular therapies, is significantly contributing to market growth. These procedures reduce trauma, shorten hospital stays, and accelerate recovery. Guidewires play a critical role in enabling clinicians to navigate complex vascular structures with precision, improving procedural success and patient outcomes. Expansion of healthcare infrastructure in emerging economies is also creating new opportunities for guidewire deployment.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $2.3 Billion |

| CAGR | 5.7% |

In 2024, the nitinol segment held a 46.3% share 2024. This segment is expected to continue growing due to favorable reimbursement policies and superior material properties, including shape-memory and super-elasticity, which provide enhanced flexibility and kink resistance for navigating tortuous vessels in cardiovascular, peripheral, and neurovascular procedures.

The coated segment held a 89.3% share in 2024. Coated guidewires, using hydrophilic, anti-thrombogenic, hydrophobic, and silicone-based technologies, are preferred for their clinical efficiency and widespread use in interventional procedures.

North America Guidewires Market accounted for a 37.7% share in 2024. The region benefits from advanced healthcare infrastructure, high procedural volumes, rapid adoption of minimally invasive interventions, and continuous technological innovation. High prevalence of cardiovascular diseases, peripheral artery disease, neurovascular conditions, and urological disorders drives demand for guidewires for both diagnostic and therapeutic applications.

Key players operating in the Global Guidewires Market include Boston Scientific, Medtronic, Abbott Laboratories, Cook Medical, Stryker, B. Braun SE, AngioDynamics, Teleflex, Cordis, Olympus, Merit Medical Systems, ASAHI INTECC, Becton Dickinson and Company, and Terumo. Companies in the Global Guidewires Market are strengthening their position by focusing on technological innovation and product differentiation, including the development of smart, coated, and bioresorbable guidewires. Collaborations with hospitals, research centers, and medical device distributors enhance market penetration and clinical adoption. Firms are expanding their footprint in emerging markets by establishing local manufacturing and distribution networks to meet growing procedural demand. Regulatory compliance and securing favorable reimbursement policies also play a vital role in driving sales. Strategic mergers and acquisitions enable companies to consolidate expertise, expand product portfolios, and access advanced R&D capabilities.a

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends (USD Mn & 000' Units)

- 2.2.2 Material trends (USD Mn & 000' Units)

- 2.2.3 Coating trends

- 2.2.4 Application trends (USD Mn & 000' Units)

- 2.2.5 Diameter trends (USD Mn & 000' Units)

- 2.2.6 Length trends (USD Mn & 000' Units)

- 2.2.7 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising adoption of minimally invasive surgical procedures

- 3.2.1.2 Increasing number of lifestyle disorders in developing countries

- 3.2.1.3 Various reimbursement policies in developed countries

- 3.2.1.4 Growing geriatric population base across the globe

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of guidewires

- 3.2.2.2 Dearth of skilled professionals in developing economies

- 3.2.2.3 Risks associated with guidewires

- 3.2.3 Opportunities

- 3.2.3.1 Expansion of healthcare infrastructure in emerging economies

- 3.2.3.2 Growing adoption of image-guided and robotic-assisted interventions

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 U.S.

- 3.4.1.2 Canada

- 3.4.2 Europe

- 3.4.3 China

- 3.4.1 North America

- 3.5 Technology and innovation landscape

- 3.5.1 Current technological trends

- 3.5.1.1 Enhanced hydrophilic and hydrophobic coating technologies

- 3.5.1.2 Torque-control and steerability optimization

- 3.5.1.3 Integration of multi-layered composite materials

- 3.5.2 Emerging technologies

- 3.5.2.1 Nanotechnology-enhanced surface engineering

- 3.5.2.2 Magnetically guided navigation systems

- 3.5.2.3 3D-printed personalized guidewire prototypes

- 3.5.1 Current technological trends

- 3.6 Future market trends

- 3.6.1 Rising shift toward fully integrated digital interventional suites

- 3.6.2 Growing preference for single-use, sterile, and cost-efficient guidewires

- 3.6.3 Expansion of minimally invasive and outpatient-based interventions

- 3.7 Reimbursement scenario

- 3.8 Pricing analysis, by region, 2024

- 3.8.1 By Material

- 3.8.2 By Application

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 Latin America

- 4.3.6 MEA

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Material, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Nitinol

- 5.3 Stainless steel

- 5.4 Hybrid

- 5.5 Other materials

Chapter 6 Market Estimates and Forecast, By Coating, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Coated

- 6.2.1 Hydrophilic coating

- 6.2.2 Anti-thrombogenic/Heparin coating

- 6.2.3 Hydrophobic coating

- 6.2.4 Silicone coating

- 6.2.5 Tetrafluoroethylene (TFE) coating

- 6.3 Non-coated

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn and Units)

- 7.1 Key trends

- 7.2 Coronary guidewires

- 7.3 Peripheral guidewires

- 7.4 Urology guidewires

- 7.5 Neurovascular guidewires

- 7.6 Other applications

Chapter 8 Market Estimates and Forecast, By Diameter, 2021 - 2034 ($ Mn and Units)

- 8.1 Key trends

- 8.2 0.014 inch

- 8.3 0.018 inch

- 8.4 0.025 inch

- 8.5 0.032 inch

- 8.6 0.035 inch

- 8.7 0.038 inch

Chapter 9 Market Estimates and Forecast, By Length, 2021 - 2034 ($ Mn and Units)

- 9.1 Key trends

- 9.2 80 - 145 cm

- 9.3 150 - 200 cm

- 9.4 210 - 300 cm

- 9.5 Above 305 cm

Chapter 10 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 10.1 Key trends

- 10.2 Hospitals

- 10.3 Ambulatory surgical centers

- 10.4 Other End use

Chapter 11 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Abbott Laboratories

- 12.2 AngioDynamics

- 12.3 ASAHI INTECC

- 12.4 B. Braun SE

- 12.5 Becton, Dickinson and Company

- 12.6 Boston Scientific

- 12.7 Cordis

- 12.8 Cook Medical

- 12.9 Medtronic

- 12.10 Merit Medical Systems

- 12.11 Olympus

- 12.12 Stryker

- 12.13 Teleflex

- 12.14 Terumo