|

시장보고서

상품코드

1664899

자동차용 연속 가변 용량(CVC) 오일 펌프 시장 기회, 성장 촉진 요인, 산업 동향 분석, 예측(2025-2034년)Automotive Continuously Variable Capacity (CVC) Oil Pump Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

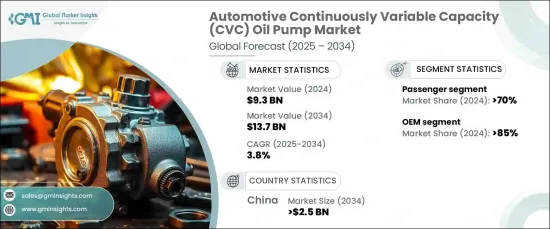

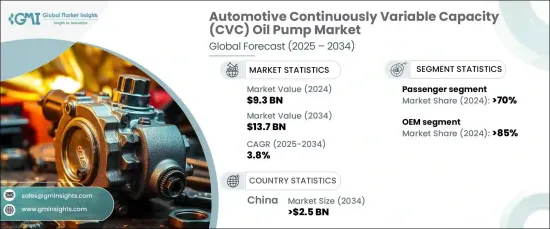

자동차용 연속 가변 용량(CVC) 오일 펌프 세계 시장은 2024년에는 93억 달러에 달했으며, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 3.8%를 나타낼 것으로 예측됩니다.

이 성장은 연비 향상과 점점 더 엄격해지는 배기 가스 규제에 대한 대응에 중점을 두고 있는 것이 주요 요인입니다. 세계 각국의 정부가 보다 친환경적인 운송 솔루션을 제창하는 가운데 자동차 제조업체는 CVC 오일 펌프와 같은 고급 구성 요소를 빠르게 채택하고 있습니다. 이러한 펌프는 연료 효율 향상, 엔진 성능 최적화, 하이브리드 및 전기 파워트레인 지원에 매우 중요한 역할을 합니다.

또한 소비자와 산업계가 에너지 효율이 높은 기술을 요구하는 가운데 전기자동차의 도입이 급증하고 있는 것도 이 시장의 추풍이 되고 있습니다. 변화하는 엔진 부하에 적응하는 능력으로 알려진 CVC 오일 펌프는 지속가능성과 성능을 선호하는 자동차의 표준 장비가되고 있습니다. 이 분야의 기술 혁신은 가속화되고 있으며 제조업체는 세계 기준을 충족하고 진화하는 소비자의 기대에 부응하기 위해 펌프 설계 개선에 주력하고 있습니다. 또한 이러한 펌프에 스마트 시스템과 첨단 재료를 통합하면 전반적인 효율과 수명이 향상되고 최신 자동차 시스템에 필수적입니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024년 |

| 예측연도 | 2025년-2034년 |

| 시작금액 | 93억 달러 |

| 예측 금액 | 137억 달러 |

| CAGR | 3.8% |

차량 유형별로는 승용차와 상용차로 분류됩니다. 2024년에는 승용차가 전체 시장의 70%를 차지하며 수익에 크게 기여합니다. 이 부문은 2034년까지 80억 달러로 성장할 것으로 예상됩니다. 승용차의 장점은 생산량 증가와 연비가 좋은 차량에 대한 소비자 선호도 증가로 인한 것입니다. 자동차 제조업체는 엄격한 환경 규제를 준수하고 환경 의식이 높은 소비자의 성능 요구 사항을 충족하기 위해 CVC 오일 펌프와 같은 고급 기술을 도입했습니다. 이러한 노력은 규제 준수를 보장 할뿐만 아니라 제조업체가 시장에서 경쟁 우위를 차지하는 데에도 도움이 됩니다.

판매 채널에 따라 시장은 OEM과 애프터마켓으로 구분됩니다. 2024년에는 OEM 부문이 시장 점유율의 85%를 차지하고 예측 기간을 통해 주도적 지위를 유지할 것으로 예상됩니다. OEM은 CVC 오일 펌프와 같은 고급 시스템의 채택에 필수적이며 제조 공정에서 이러한 기술을 통합하는 리소스를 가지고 있기 때문입니다. R&D 투자 능력은 진화하는 배출 기준을 충족하면서 차량 성능을 향상시키는 최첨단 시스템의 채택을 보장합니다. 대규모 제조 능력과 지속가능성을 중시한 파트너십은 시장에서 OEM 부문의 우위를 더욱 향상시키고 있습니다.

지역별 역학에서 중국은 2024년 자동차용 CVC 오일 펌프 시장에서 60%의 압도적 점유율을 차지했습니다. 이 지역은 2034년까지 25억 달러를 창출할 것으로 예상되어 자동차 제조의 세계적 리더로서의 지위를 굳히고 있습니다. 환경 문제를 해결하기 위해 중국이 하이브리드 자동차 및 전기자동차 생산에 주력하는 것이 효율적인 오일 펌프 기술에 대한 수요의 큰 원동력이되었습니다. 중국의 자동차 제조업체는 폐가스에 대한 규제 지침을 준수하면서 최신 파워트레인의 성능 요구 사항을 지원하는 첨단 시스템을 채택하고 있습니다.

목차

제1장 조사 방법과 조사 범위

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 기본 추정과 계산

- 기준연도의 산출

- 시장추계의 주요 동향

- 예측 모델

- 1차 조사와 검증

- 1차 소스

- 데이터 마이닝 소스

- 시장 정의

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 공급자의 상황

- OEM CVC 오일 펌프 제조업체

- 애프터마켓 프로바이더

- 유통업체

- 최종 사용자

- 이익률 분석

- 가격 분석

- 특허 상황

- 코스트 내역 분석

- 기술 혁신의 상황

- 주요 뉴스 및 이니셔티브

- 규제 상황

- 영향요인

- 성장 촉진요인

- 연비와 배출가스에 관한 정부의 엄격한 규제

- 하이브리드차와 전기차(HEV와 EV) 수요 증가

- 차량 성능의 최적화와 열 관리에 대한 주목의 향상

- 자동차 파워트레인 시스템의 기술 진보

- 업계의 잠재적 리스크 및 과제

- 연속 가변 용량 오일 펌프의 초기 비용의 높이와 복잡성

- 시장 경쟁 격화에 의한 가격 압력

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추정 및 예측 : 유형별, 2021년-2034년

- 주요 동향

- 가변 용량 오일 펌프

- 전동 오일 펌프

- 기계식 오일 펌프

제6장 시장 추정 및 예측 : 용도별, 2021년-2034년

- 주요 동향

- 엔진 윤활

- 변속기

- 하이브리드 파워트레인

제7장 시장 추정 및 예측 : 차량별, 2021년-2034년

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV차

- 상용차

- 소형 상용차(LCV)

- 대형 상용차(HCV)

제8장 시장 추정 및 예측 : 기술별, 2021년-2034년

- 주요 동향

- 유압 제어

- 전자제어

제9장 시장 추정 및 예측 : 판매 채널별, 2021년-2034년

- 주요 동향

- OEM

- 애프터마켓

제10장 시장 추정 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 스페인

- 이탈리아

- 러시아

- 북유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 뉴질랜드

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- UAE

- 남아프리카

- 사우디아라비아

제11장 기업 프로파일

- Aisin Seiki

- BorgWarner

- Bosch

- Continental

- Cummins

- Denso

- FTE Automotive

- Hanon Systems

- Hitachi Astemo

- Johnson Electric

- Magna International

- Mahle GmbH

- Melling Tool Company

- Mikuni

- Pierburg

- Rheinmetall Automotive

- Shw Automotive

- SKF Group

- Stackpole

- Yamada Manufacturing

The Global Automotive Continuously Variable Capacity Oil Pump Market was valued at USD 9.3 billion in 2024 and is projected to grow at a CAGR of 3.8% between 2025 and 2034. This growth is largely driven by a heightened focus on improving fuel efficiency and meeting increasingly stringent emission regulations. As governments worldwide advocate for greener transportation solutions, automakers are rapidly adopting advanced components such as CVC oil pumps. These pumps play a pivotal role in enhancing fuel efficiency, optimizing engine performance, and supporting hybrid and electric powertrains.

The market is also benefitting from a surge in electric vehicle adoption, with consumers and industries alike demanding energy-efficient technologies. CVC oil pumps, known for their ability to adapt to varying engine loads, are becoming a standard feature in vehicles that prioritize sustainability and performance. Innovation in this sector is accelerating, with manufacturers focusing on improving pump designs to meet global standards and address evolving consumer expectations. Furthermore, the integration of smart systems and advanced materials in these pumps is enhancing their overall efficiency and lifespan, making them indispensable in modern automotive systems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $9.3 Billion |

| Forecast Value | $13.7 Billion |

| CAGR | 3.8% |

By vehicle type, the market is categorized into passenger and commercial vehicles. In 2024, passenger vehicles dominated the market, capturing 70% of the overall share and contributing significantly to revenue. This segment is forecasted to grow to USD 8 billion by 2034. The dominance of passenger vehicles can be attributed to higher production volumes and a growing consumer preference for fuel-efficient vehicles. Automakers are incorporating advanced technologies like CVC oil pumps to comply with stringent environmental regulations and meet the performance demands of environmentally conscious consumers. These efforts not only ensure regulatory compliance but also help manufacturers gain a competitive edge in the market.

Based on sales channels, the market is segmented into OEMs and aftermarket. In 2024, the OEM segment accounted for 85% of the market share and is expected to maintain its leading position throughout the forecast period. OEMs are integral to the adoption of advanced systems like CVC oil pumps as they have the resources to integrate these technologies during the manufacturing process. Their ability to invest in research and development ensures the adoption of cutting-edge systems that enhance vehicle performance while meeting evolving emission standards. Large-scale manufacturing capabilities and sustainability-focused partnerships further bolster the OEM segment's dominance in the market.

In terms of regional dynamics, China held a commanding 60% share of the automotive CVC oil pump market in 2024. The region is anticipated to generate USD 2.5 billion by 2034, cementing its position as a global leader in automotive manufacturing. China's emphasis on producing hybrid and electric vehicles to address environmental concerns is a significant driver of demand for efficient oil pump technologies. Automakers in China are adopting advanced systems to support the performance requirements of modern powertrains while adhering to regulatory guidelines on emissions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 OEM CVC oil pump manufacturers

- 3.2.2 Aftermarket providers

- 3.2.3 Distributors

- 3.2.4 End users

- 3.3 Profit margin analysis

- 3.4 Pricing analysis

- 3.5 Patent Landscape

- 3.6 Cost Breakdown analysis

- 3.7 Technology & innovation landscape

- 3.8 Key news & initiatives

- 3.9 Regulatory landscape

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Stringent government regulations on fuel efficiency and emissions

- 3.10.1.2 Increasing demand for hybrid and electric vehicles (HEVs and EVs)

- 3.10.1.3 Rising focus on vehicle performance optimization and thermal management

- 3.10.1.4 Technological advancements in automotive powertrain systems

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 High initial cost and complexity of continuously variable capacity oil pumps

- 3.10.2.2 Intense competition among market players leading to pricing pressures

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter’s analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Variable displacement oil pumps

- 5.3 Electric oil pumps

- 5.4 Mechanical oil pumps

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Engine lubrication

- 6.3 Transmission systems

- 6.4 Hybrid powertrains

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger vehicles

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles

- 7.3.1 Light Commercial Vehicles (LCV)

- 7.3.2 Heavy Commercial Vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By Technology, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Hydraulic control

- 8.3 Electronic control

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Aisin Seiki

- 11.2 BorgWarner

- 11.3 Bosch

- 11.4 Continental

- 11.5 Cummins

- 11.6 Denso

- 11.7 FTE Automotive

- 11.8 Hanon Systems

- 11.9 Hitachi Astemo

- 11.10 Johnson Electric

- 11.11 Magna International

- 11.12 Mahle GmbH

- 11.13 Melling Tool Company

- 11.14 Mikuni

- 11.15 Pierburg

- 11.16 Rheinmetall Automotive

- 11.17 Shw Automotive

- 11.18 SKF Group

- 11.19 Stackpole

- 11.20 Yamada Manufacturing