|

시장보고서

상품코드

1665290

우주 경제 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Space Economy Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

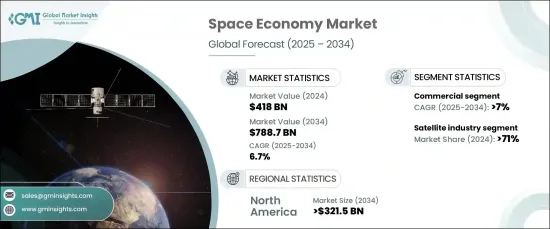

세계의 우주 경제 시장은 2024년에는 4,180억 달러로 평가되었고, 2025년부터 2034년까지 CAGR 6.7%로 확대될 전망이며 강력한 성장을 이룰 것으로 예측되고 있습니다. 이 성장의 원동력이 되고 있는 것은 다양한 산업에서 우주 기술의 도입이 진행되어, 업무에 혁명이 일어나고, 새로운 수익 기회가 태어나고 있는 것입니다.

위성과 로켓의 기술 혁신은 우주 접근과 비용 효율성을 높이고 시장 확대에 박차를 가하고 있습니다. 이러한 진보는 실시간 추적, 세계 통신, 첨단 기상 모니터링 등의 기능을 제공함으로써 운송, 물류, 재해 관리 등의 산업에 혜택을 제공합니다. 기업이 우주 기반 솔루션을 지속적으로 통합함에 따라 시장은 성장과 비즈니스 효율성의 잠재력을 더욱 확대할 태세를 갖추고 있습니다.

| 시장 규모 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 4,180억 달러 |

| 예측 금액 | 7,887억 달러 |

| CAGR | 6.7% |

우주 경제 시장은 주로 위성 산업, 비위성 산업, 우주 지속가능 활동의 세 가지 주요 부문으로 나뉩니다. 위성 산업은 2024년 시장에서 71%라는 큰 점유율을 차지했습니다. 통신, 항법, 지구관측에 있어서 위성 서비스 수요가 계속 증가하고 있기 때문에 이 우위성은 앞으로도 계속될 것으로 예상됩니다. 기업은 저궤도(LEO)에 소형 위성을 배치하는 데 점점 더 많은 노력을 기울이고 있으며, 이는 세계의 인터넷 연결 강화, 데이터 수집 및 원활한 통신 지원에 필수적입니다. 위성 기술은 또한 농업, 물류, 재해 대응 등 다양한 부문에서 중요한 역할을 하고 있으며, 조직이 데이터 중심의 의사 결정을 내리고 업무의 효율성을 높일 수 있습니다.

최종 사용자의 경우 우주 경제 시장은 상업 부문과 정부 및 방위 부문으로 나뉩니다. 상업 부문은 2034년까지 연평균 복합 성장률(CAGR) 7%로 성장할 것으로 예측됩니다. 이러한 급성장의 배경에는 위성을 이용한 서비스, 특히 세계 광대역 및 IoT 연결에 대한 수요가 증가하고 있습니다. 확장된 LEO 위성 별자리는 네트워크 커버리지와 응답 시간을 개선하여 보다 안정적인 통신과 고급 원격 감지 기능을 제공합니다. 이러한 기술적 약진은 기존의 인프라가 부족한 지역에 특히 유익하며, 산업에 관계없이 위성 서비스의 채용을 가속화하고 있습니다.

북미는 2034년까지 3,215억 달러의 우주 경제 시장 수익을 창출할 것으로 예상됩니다. 미국은 이 성장의 최전선에 있으며, 엄청난 정부 자금과 민간 관여에 의해 지원됩니다. 위성 배치의 주요 개발과 발사 비용 절감은 시장 확대를 가속화하고 있습니다. 미국은 세계 광대역 서비스를 위한 위성 네트워크 구축, 서비스가 미치지 못한 지역의 연결성 향상, 하이테크 부문의 기술 혁신을 촉진하는데 주도적인 역할을 계속하고 있습니다.

목차

제1장 조사 방법 및 조사 범위

- 시장 범위 및 정의

- 기본 추정 및 계산

- 예측 계산

- 데이터 소스

- 1차 데이터

- 2차 데이터

- 유료 정보원

- 공적 정보원

제2장 주요 요약

제3장 산업 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 변혁

- 장래 전망

- 제조업체

- 유통업체

- 공급자의 상황

- 이익률 분석

- 주요 뉴스

- 규제 상황

- 영향 요인

- 성장 촉진요인

- 우주 기술의 진보

- 통신, 지구관측, 전 지구 측위를 위한 위성 용도의 급증

- 우주 상업화의 진전

- 국제협력 및 투자 증가

- 우주개발에 대한 정부자금 증가

- 산업의 잠재적 리스크 및 과제

- 높은 비용 및 투자 위험

- 환경 및 지속가능성 문제

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추정 및 예측 : 유형별(2021-2034년)

- 주요 동향

- 위성 산업

- 위성 발사

- 위성 서비스

- 위성 제조

- 위성 지상 설비

- 비위성 산업

- 정부 우주 예산

- 상업 유인 우주 비행

- 우주 지속가능 활동

제6장 시장 추정 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 상업

- 정부 및 방위

제7장 시장 추정 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제8장 기업 프로파일

- AeroVironment

- Airbus

- BAE Systems

- Blue Origin

- Boeing

- Elbit Systems

- General Dynamics

- Indian Space Research Organisation

- Israel Aerospace Industries

- Lockheed Martin

- Maxar Technologies

- Northrop Grumman

- Raytheon Technologies

- SpaceX

- Thales

- Viasat

The Global Space Economy Market was valued at USD 418 billion in 2024 and is projected to experience robust growth, expanding at a CAGR of 6.7% from 2025 to 2034. This growth is driven by the increasing adoption of space technologies across various industries, which is revolutionizing operations and opening up new revenue opportunities.

Technological innovations in satellites and rockets are making space more accessible and cost-effective, fueling market expansion. These advancements are benefiting industries such as transportation, logistics, and disaster management by providing capabilities like real-time tracking, global communication, and advanced weather monitoring. As businesses continue to integrate space-based solutions, the market is poised to unlock even more potential for growth and operational efficiency.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $418 billion |

| Forecast Value | $788.7 billion |

| CAGR | 6.7% |

The space economy market is primarily divided into three key segments: the satellite industry, the non-satellite industry, and space sustainability activities. The satellite industry dominated the market in 2024, accounting for a significant 71% share. This dominance is expected to continue as demand for satellite services in telecommunications, navigation, and Earth observation continues to rise. Companies are increasingly focusing on deploying small satellites in Low Earth Orbit (LEO), which are crucial for enhancing global internet connectivity, gathering data, and supporting seamless communication. Satellite technology also plays a vital role in various sectors, including agriculture, logistics, and disaster response, empowering organizations to make data-driven decisions that enhance operational effectiveness.

When it comes to end users, the space economy market is divided into the commercial sector and the government and defense sector. The commercial segment is projected to grow at a CAGR of 7% through 2034. This surge is driven by a growing demand for satellite-based services, particularly for global broadband and IoT connectivity. Expanding LEO satellite constellations are improving network coverage and response times, enabling more reliable communication and advanced remote sensing capabilities. These technological breakthroughs are especially beneficial for regions lacking traditional infrastructure, accelerating the adoption of satellite services across industries.

North America is expected to generate USD 321.5 billion in space economy market revenue by 2034. The U.S. is at the forefront of this growth, bolstered by substantial government funding and private-sector involvement. Key developments in satellite deployment and reduced launch costs are accelerating the expansion of the market. The U.S. continues to lead the way in building satellite networks for global broadband services, driving improved connectivity in underserved regions, and fostering innovation in the tech sector.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Technological advancements in space technologies

- 3.6.1.2 Surge in satellite applications for communication, Earth observation, and global positioning

- 3.6.1.3 Growing commercialization of space

- 3.6.1.4 Rising international collaboration and investments

- 3.6.1.5 Increasing government funding for space exploration

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High costs and investment risks

- 3.6.2.2 Environmental and sustainability issues

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Satellite industry

- 5.2.1 Satellite launch

- 5.2.2 Satellite services

- 5.2.3 Satellite manufacturing

- 5.2.4 Satellite ground equipment

- 5.3 Non-Satellite Industry

- 5.3.1 Government space budgets

- 5.3.2 Commercial human spaceflight

- 5.4 Space sustainability activities

Chapter 6 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Commercial

- 6.3 Government & defense

Chapter 7 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.6 MEA

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 AeroVironment

- 8.2 Airbus

- 8.3 BAE Systems

- 8.4 Blue Origin

- 8.5 Boeing

- 8.6 Elbit Systems

- 8.7 General Dynamics

- 8.8 Indian Space Research Organisation

- 8.9 Israel Aerospace Industries

- 8.10 Lockheed Martin

- 8.11 Maxar Technologies

- 8.12 Northrop Grumman

- 8.13 Raytheon Technologies

- 8.14 SpaceX

- 8.15 Thales

- 8.16 Viasat