|

시장보고서

상품코드

1913304

자동차 운영체제 시장 예측 : 기회 , 성장 요인, 업계 동향 분석(2026-2035년)Automotive Operating System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

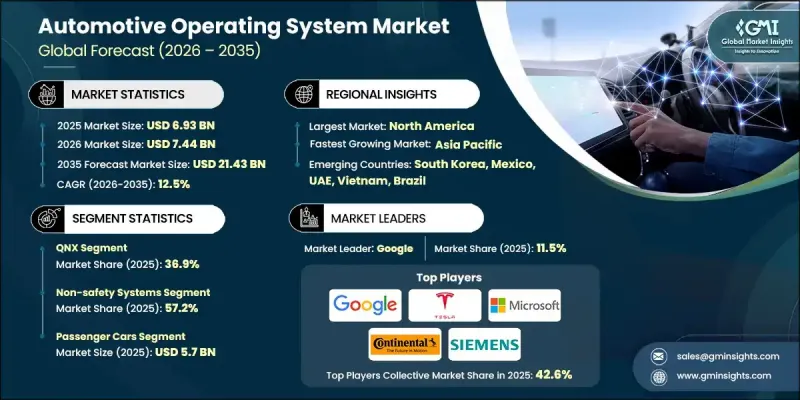

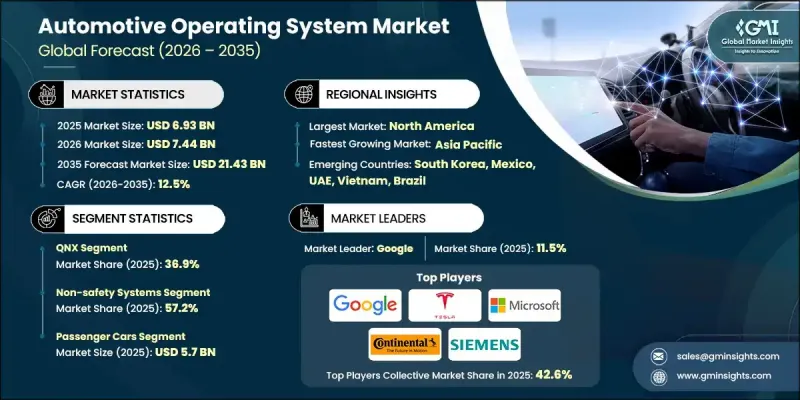

세계 자동차 운영체제 시장은 2025년 69억 3,000만 달러로 평가되었으며, 2035년까지 연평균 복합 성장률(CAGR) 12.5%로 성장하고 214억 3,000만 달러에 이를 것으로 예측됩니다.

시장 확대는 차량이 소프트웨어 정의 아키텍처로 빠르게 이동하고 있으며 차량 기능에서 디지털 플랫폼의 역할이 증가하고 있음을 반영합니다. 여러 지역의 정부는 ADAS의 통합을 촉진하는 규제 체제를 가속화하고 있으며, 이는 견고한 자동차 운영체제에 대한 수요를 직접적으로 증가시키고 있습니다. 동시에 차량 판매량 증가와 디지털 디스플레이의 보급 확대가 함께 시스템 레벨의 소프트웨어 요건을 강화하고 있습니다. 현대 차량은 연결성, 자동화, 사용자 인터페이스 및 실시간 처리를 지원하기 때문에 통합 운영 체제에 대한 의존도를 높이고 있습니다. 자동차 제조업체는 증가하는 시스템의 복잡성을 관리하기 위해 안전하고 확장 가능하고 효율적인 소프트웨어 환경을 우선적으로 도입하고 있습니다. 무선 업데이트 기능은 이제 기본 요구 사항이 되어 소프트웨어 및 펌웨어 업데이트를 원활하게 제공하는 동시에 사이버 보안과 성능 최적화를 강화합니다. 이러한 변화를 통해 제조업체는 문제를 원격으로 해결하고 향상된 기능을 신속하게 배포하고 물리적 서비스 없이 새로운 수익 모델을 도입할 수 있습니다. 차량이 연결된 디지털 플랫폼으로 진화함에 따라 운영 체제는 세계 자동차 생태계 전반에서 혁신, 규정 준수 및 장기적인 경쟁을 지원하는 핵심 기둥이되었습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 시작 금액 | 69억 3,000만 달러 |

| 예측 금액 | 214억 3,000만 달러 |

| CAGR | 12.5% |

QNX 부문은 2025년에 36.9%의 점유율을 차지했으며 전 세계 차량 플랫폼의 높은 보급률로 주도적인 지위를 유지했습니다. 경쟁 플랫폼은 혁신의 가속화에 따라 기세를 늘리고 있으며, 전체 시장 확대에 적극적으로 기여하고 있습니다.

비안전 시스템 부문은 2025년에 57.2%의 점유율을 차지했고, 2026년부터 2035년에 걸쳐 CAGR 11.9%로 성장이 예상되고 있습니다. 규제상의 제약이 적고 개발 사이클이 빠르기 때문에 이 부문 전체에서의 급속한 채택이 진행되고 있습니다.

미국 자동차 운영체제 시장은 2025년 18억 6,000만 달러에 달했습니다. 이 나라의 자동차 제조업체들은 무선 업데이트(OTA)와 크로스 도메인 통합을 지원하는 중앙 집중식 소프트웨어 아키텍처로의 전환을 빠르게 진행하고 있으며, 유연성과 확장성을 갖춘 운영 체제에 대한 수요를 이끌고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 현황

- 수익률

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 차량의 급속한 전동화

- 소프트웨어 정의 차량(SDV)의 보급 확대

- ADAS(첨단 운전 지원 시스템)의 통합 확대

- 차재 인포테인먼트 및 커넥티비티에 대한 수요 증가

- 업계의 잠재적 위험 및 과제

- 소프트웨어 통합 및 검증의 고급 복잡성

- 차량 사이버 보안 및 데이터 프라이버시에 대한 우려 사항

- 시장 기회

- 구독 모델에 의한 소프트웨어 기능의 수익화

- Vehicle-to-Everything(V2X) 통신의 보급 확대

- 상용차 및 플릿 차량에 있어서의 자동차 OS의 활용 확대

- 스마트 모빌리티와 공유 교통 플랫폼의 성장

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- ISO 26262(ASIL D)

- NHTSA 사이버 보안 모범 사례

- SAE J3061

- FMVSS(연방 자동차 안전 기준)

- 유럽

- 유엔규칙 제155호(R155)

- Automotive SPICE(ASPICE)

- EU 일반안전규제(GSR)

- 아시아태평양

- JASO(일본 자동차 표준화 기구)

- MLIT 규제(일본)

- AIS-189/AIS-190(인도)

- 라틴아메리카

- CONTRAN 결의

- NOM-194-SE-2021

- UNECE WP.29 무결성

- 중동 및 아프리카

- GSO(만안 표준화 기구) 규격

- 아랍에미리트(UAE) 국가 EV 정책

- 사우디아라비아 SASO 규제

- 북미

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 전망

- 현재의 기술 동향

- 신규기술

- 가격 동향

- 지역별

- 제품별

- 지속가능성과 환경에 미치는 영향

- 환경 영향 평가

- 사회적 영향과 커뮤니티에의 공헌

- 거버넌스와 기업의 사회적 책임

- 지속 가능한 금융 및 투자 동향

- 코스트 내역 분석

- OS용 하드웨어 플랫폼 및 컴퓨팅 비용

- OS 개발 및 통합 비용

- 사이버 보안 및 기능 안전 컴플라이언스 비용

- 무선 업데이트(OTA) 인프라 및 클라우드 서비스 비용

- 라이선싱, 구독 및 타사 소프트웨어 에코시스템 비용

- 유지 보수, 버그 수정, 기능 갱신의 라이프 사이클 비용

- 사례 연구

- 전망과 기회

- SDV 제공에 있어서의 실행상의 과제

- 소프트웨어 커스터마이즈와 플러그 앤 플레이 기능의 불일치

- 격차 해소를 위한 기업 전략

- 이용 사례

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획과 자금 조달

제5장 시장추정 및 예측 : 운영체제별, 2022-2035

- Android

- Linux

- QNX

- Windows

- 기타

제6장 시장 추정 및 예측 : 자동차 시스템별, 2022-2035

- 비안전 시스템

- 안전 핵심 시스템

제7장 시장 추정 및 예측 : 차량별, 2022-2035

- 승용차

- 해치백

- 세단

- SUV

- 상용차

- 경상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

제8장 시장추정 및 예측 : 추진력별, 2022-2035

- 내연기관(ICE)

- 전기자동차(EV)

- 하이브리드

제9장 시장추정 및 예측 : 용도별, 2022-2035

- 인포테인먼트 시스템

- ADAS 및 안전 시스템

- 자율주행

- 통신 시스템

- 접속 서비스

- 텔레매틱스

- 파워트레인 제어

- 기타

제10장 시장추정 및 예측 : 판매채널별, 2022-2035

- OEM

- 애프터마켓

제11장 시장추정 및 예측 : 지역별, 2022-2035

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 베네룩스

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- ANZ

- 싱가포르

- 말레이시아

- 인도네시아

- 베트남

- 태국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 콜롬비아

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제12장 기업 프로파일

- 세계기업

- Microsoft

- Tesla

- NVIDIA

- Hyundai

- Mercedes-Benz

- BlackBerry

- Wind River

- Green Hills Software

- Apple

- Huawei

- Baidu

- Alibaba

- Red Hat

- Volkswagen

- 지역 기업

- Elektrobit

- Continental

- Robert Bosch

- Siemens

- Vector Informatik

- ETAS

- Panasonic Automotive

- Denso

- Toyota Motor

- Aptiv

- 신흥기업

- Xpeng Motors

- NIO

- BYD

- Geely Automobile

- SAIC Motor

The Global Automotive Operating System Market was valued at USD 6.93 billion in 2025 and is estimated to grow at a CAGR of 12.5% to reach USD 21.43 billion by 2035.

Market expansion reflects the rapid shift of vehicles toward software-defined architectures and the increasing role of digital platforms in vehicle functionality. Governments across multiple regions are accelerating regulatory frameworks that encourage the integration of advanced driver assistance technologies, which directly elevates demand for robust automotive operating systems. At the same time, rising vehicle sales combined with growing adoption of digital displays are strengthening system-level software requirements. Modern vehicles increasingly rely on integrated operating systems to support connectivity, automation, user interfaces, and real-time processing. Automotive manufacturers are prioritizing secure, scalable, and efficient software environments to manage growing system complexity. Wireless update capabilities are now a baseline expectation, enabling seamless delivery of both software and firmware updates while enhancing cybersecurity and performance optimization. This transformation allows manufacturers to resolve issues remotely, deploy enhancements faster, and introduce new revenue models without physical servicing. As vehicles evolve into connected digital platforms, operating systems have become a central pillar supporting innovation, compliance, and long-term competitiveness across the global automotive ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2025 |

| Forecast Year | 2026-2035 |

| Start Value | $6.93 Billion |

| Forecast Value | $21.43 Billion |

| CAGR | 12.5% |

The QNX segment accounted for 36.9% share in 2025 and maintained a leading position due to its strong penetration across global vehicle platforms. Competing platforms are gaining momentum as innovation accelerates, contributing positively to overall market expansion.

The non-safety systems segment held 57.2% share in 2025 and is expected to grow at a CAGR of 11.9% between 2026 and 2035. Fewer regulatory constraints and faster development cycles are enabling rapid adoption across this segment.

U.S. Automotive Operating System Market reached USD 1.86 billion in 2025. Automakers in the country are rapidly transitioning toward centralized software architectures that support over-the-air updates and cross-domain integration, driving demand for flexible and scalable operating systems.

Key companies active in the Global Automotive Operating System Market include BlackBerry, NVIDIA, Google, Apple, Microsoft, BMW, Mercedes-Benz, Siemens, Continental, and Tesla. Companies operating in the Automotive Operating System Market are strengthening their competitive position through platform innovation, ecosystem partnerships, and long-term collaborations with vehicle manufacturers. Investment in cybersecurity, real-time processing, and scalable architectures is helping vendors address increasing software complexity. Many players are focusing on modular system designs that enable faster deployment across vehicle models. Strategic alliances with semiconductor firms and cloud providers are improving system performance and integration capabilities. Continuous enhancement of update management, lifecycle support, and developer tools is expanding adoption.

Table of Contents

Chapter 1 Methodology

- 1.1 Research approach

- 1.2 Quality commitments

- 1.2.1 GMI AI policy & data integrity commitment

- 1.3 Research trail & confidence scoring

- 1.3.1 Research trail components

- 1.3.2 Scoring components

- 1.4 Data collection

- 1.4.1 Partial list of primary sources

- 1.5 Data mining sources

- 1.5.1 Paid sources

- 1.6 Base estimates and calculations

- 1.6.1 Base year calculation

- 1.7 Forecast model

- 1.8 Research transparency addendum

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Operating System

- 2.2.3 Auto system

- 2.2.4 Vehicle

- 2.2.5 Propulsion

- 2.2.6 Application

- 2.2.7 Sales Channel

- 2.3 TAM analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rapid electrification of vehicles

- 3.2.1.2 Growing adoption of software-defined vehicles (SDVs)

- 3.2.1.3 Rising integration of Advanced Driver Assistance Systems (ADAS)

- 3.2.1.4 Increasing demand for in-vehicle infotainment and connectivity

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High complexity of software integration and validation

- 3.2.2.2 Concerns related to vehicle cybersecurity and data privacy

- 3.2.3 Market opportunities

- 3.2.3.1 Monetization of software features through subscription models

- 3.2.3.2 Increasing adoption of Vehicle-to-Everything (V2X) communication

- 3.2.3.3 Expansion of automotive OS use in commercial and fleet vehicles

- 3.2.3.4 Growth of smart mobility and shared transportation platforms

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.1.1 ISO 26262 (ASIL D)

- 3.4.1.2 NHTSA Cybersecurity Best Practices

- 3.4.1.3 SAE J3061

- 3.4.1.4 FMVSS (Federal Motor Vehicle Safety Standards)

- 3.4.2 Europe

- 3.4.2.1 UN Regulation No. 155 (R155)

- 3.4.2.2 Automotive SPICE (ASPICE)

- 3.4.2.3 EU General Safety Regulation (GSR)

- 3.4.3 Asia Pacific

- 3.4.3.1 JASO (Japan Automotive Standards Organization)

- 3.4.3.2 MLIT Regulations (Japan)

- 3.4.3.3 AIS-189/AIS-190 (India)

- 3.4.4 Latin America

- 3.4.4.1 CONTRAN Resolutions

- 3.4.4.2 NOM-194-SE-2021

- 3.4.4.3 UNECE WP.29 Alignment

- 3.4.5 Middle East & Africa

- 3.4.5.1 GSO (Gulf Standardization Organization) Standards

- 3.4.5.2 UAE National EV Policy

- 3.4.5.3 Saudi SASO Regulations

- 3.4.1 North America

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Sustainability and environmental impact

- 3.9.1 Environmental impact assessment

- 3.9.2 Social impact & community benefits

- 3.9.3 Governance & corporate responsibility

- 3.9.4 Sustainable finance & investment trends

- 3.10 Cost breakdown analysis

- 3.10.1 Hardware platform and compute cost for OS

- 3.10.2 OS development and integration cost

- 3.10.3 Cybersecurity and functional safety compliance cost

- 3.10.4 Over-the-air update infrastructure and cloud service cost

- 3.10.5 Licensing, subscription, and third-party software ecosystem cost

- 3.10.6 Maintenance, bug-fixing, and feature update lifecycle cost

- 3.11 Case studies

- 3.12 Future outlook & opportunities

- 3.13 Execution gaps in SDV delivery

- 3.13.1 Mismatches in software customization and plug-and-play capabilities

- 3.13.2 Company strategies for bridging the gaps

- 3.13.3 Use cases

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Operating System, 2022 - 2035 ($Mn)

- 5.1 Key trends

- 5.2 Android

- 5.3 Linux

- 5.4 QNX

- 5.5 Windows

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Auto System, 2022 - 2035 ($Mn)

- 6.1 Key trends

- 6.2 Non-safety system

- 6.3 Safety-critical System

Chapter 7 Market Estimates & Forecast, By Vehicle, 2022 - 2035 ($Mn)

- 7.1 Key trends

- 7.2 Passenger cars

- 7.2.1 Hatchbacks

- 7.2.2 Sedans

- 7.2.3 SUVs

- 7.3 Commercial vehicles

- 7.3.1 LCV

- 7.3.2 MCV

- 7.3.3 HCV

Chapter 8 Market Estimates & Forecast, By Propulsion, 2022 - 2035 ($Mn)

- 8.1 Key trends

- 8.2 ICE

- 8.3 EV

- 8.4 Hybrid

Chapter 9 Market Estimates & Forecast, By Application, 2022 - 2035 ($Mn)

- 9.1 Key trends

- 9.2 Infotainment system

- 9.3 ADAS & safety system

- 9.4 Autonomous driving

- 9.5 Communication system

- 9.6 Connected services

- 9.7 Telematics

- 9.8 Powertrain control

- 9.9 Others

Chapter 10 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 ($Mn)

- 10.1 Key trends

- 10.2 OEM

- 10.3 Aftermarket

Chapter 11 Market Estimates & Forecast, By Region, 2022 - 2035 ($Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 US

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.3.7 Nordics

- 11.3.8 Benelux

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 ANZ

- 11.4.6 Singapore

- 11.4.7 Malaysia

- 11.4.8 Indonesia

- 11.4.9 Vietnam

- 11.4.10 Thailand

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.5.4 Colombia

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Global companies

- 12.1.1 Google

- 12.1.2 Microsoft

- 12.1.3 Tesla

- 12.1.4 NVIDIA

- 12.1.5 Hyundai

- 12.1.6 Mercedes-Benz

- 12.1.7 BlackBerry

- 12.1.8 Wind River

- 12.1.9 Green Hills Software

- 12.1.10 Apple

- 12.1.11 Huawei

- 12.1.12 Baidu

- 12.1.13 Alibaba

- 12.1.14 Red Hat

- 12.1.15 Volkswagen

- 12.2 Regional companies

- 12.2.1 Elektrobit

- 12.2.2 Continental

- 12.2.3 Robert Bosch

- 12.2.4 Siemens

- 12.2.5 Vector Informatik

- 12.2.6 ETAS

- 12.2.7 Panasonic Automotive

- 12.2.8 Denso

- 12.2.9 Toyota Motor

- 12.2.10 Aptiv

- 12.3 Emerging companies

- 12.3.1 Xpeng Motors

- 12.3.2 NIO

- 12.3.3 BYD

- 12.3.4 Geely Automobile

- 12.3.5 SAIC Motor