|

시장보고서

상품코드

1876794

인공와우 시장 비즈니스 기회, 성장요인, 업계 동향 분석 및 예측(2025-2034년)Cochlear Implants Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

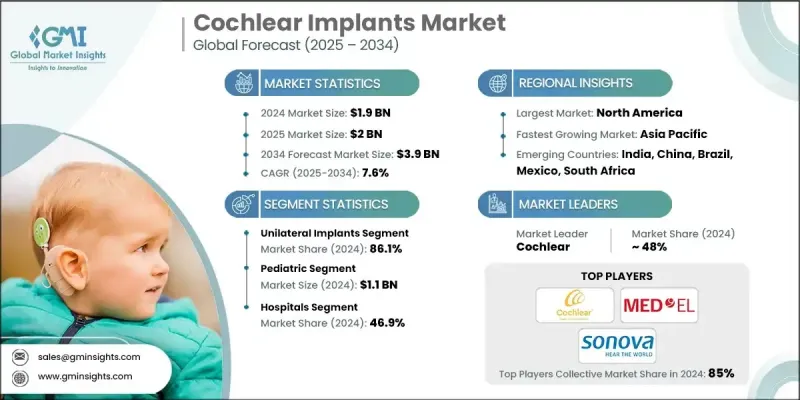

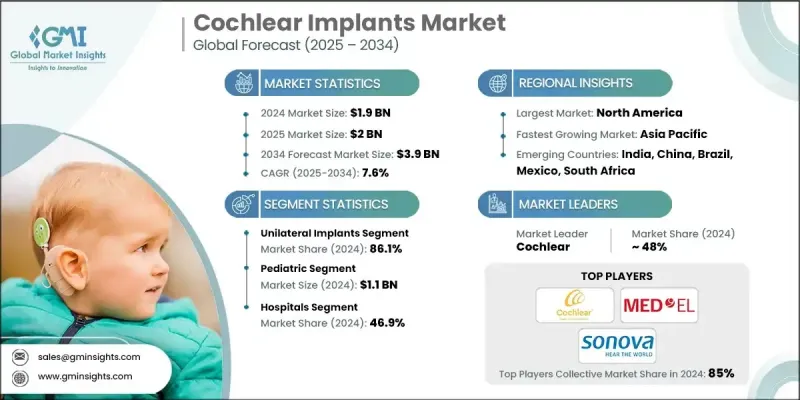

세계의 인공와우 시장은 2024년에 19억 달러로 평가되었고, 2034년까지 연평균 복합 성장률(CAGR) 7.6%로 성장하여 39억 달러에 이를 것으로 예측되고 있습니다.

시장 확대의 주요 요인으로는 청각 장애의 유병률 증가, 임플란트 기술의 혁신, 소아 및 노년층의 도입 증가, 광범위한 청력 검사 프로그램과 함께 높아진 인지도를 꼽을 수 있습니다. 인공와우는 손상된 내이 유모세포를 우회하여 직접 청신경을 자극하여 소리를 인지할 수 있도록 하는 첨단 전자기기입니다. 음신호를 수집, 처리, 전송하는 내부 구성요소와 외부 구성요소로 구성되어 있습니다. 소리를 증폭하는 보청기와 달리 인공와우는 소리를 전기 신호로 변환하여 청력을 부분적으로 회복시켜 줍니다. 학교와 병원의 인식개선 활동 확대와 조기 검진으로 적응증 환자를 조기에 발견할 수 있게 되었습니다. 또한, 청각학회, 의료진, 임플란트 제조업체 간의 협력을 통해 환자 교육이 강화되어 수술에 대한 수용성 향상으로 이어지고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 19억 달러 |

| 예측 금액 | 39억 달러 |

| CAGR | 7.6% |

일측성 임플란트 부문은 저렴한 비용, 수술의 편의성, 빠른 회복, 양측성 임플란트에 대한 임상의의 선호로 인해 2024년 86.1%의 점유율을 차지했습니다. 특히 개발도상국 시장에서는 비용적인 이점 때문에 환자나 의료진에게 일방적 임플란트가 더 쉽게 접근할 수 있는 선택이 되고 있습니다. 이러한 합리적인 가격대는 양측 임플란트 비용 부담 없이 청력 개선을 원하는 개인들의 채택을 촉진하고 있습니다.

병원 부문은 2024년 46.9%의 점유율을 차지했으며, 2025년부터 2034년까지 17억 달러에 달할 것으로 예측됩니다. 고령화, 소음에 대한 장기간 노출, 선천성 질환으로 인한 감음성 난청 사례가 증가함에 따라 병원에서 치료를 받는 환자가 증가하고 있습니다. 병원은 이비인후과 및 청각학 서비스에 인공와우 수술을 통합함으로써 환자 치료와 수익원 강화라는 두 가지 이점을 얻고 있습니다.

북미 인공와우 시장은 2024년 41.2%의 점유율을 차지했습니다. 이 지역에서는 노화성, 선천성을 포함한 감음성 난청 유병률이 높아 조기 진단 및 중재 프로그램이 추진되고 있습니다. 이러한 노력은 인공와우에 대한 수요를 크게 증가시켜 시장의 꾸준한 성장을 견인하고 있습니다.

인공와우 시장의 주요 기업으로는 MED-EL, Cochlear, Sonova, Envoy Medical, Nurotron 등이 있습니다. 세계 시장에서 각 기업들은 시장 기반을 강화하기 위해 다양한 전략을 펼치고 있습니다. 각 업체들은 임플란트의 기능성과 편안함, 그리고 첨단 음성처리 기술과의 호환성을 높이기 위해 연구개발에 투자하고 있습니다. 의료진을 대상으로 한 대상별 캠페인과 교육 프로그램을 통해 소아 및 노인층에 대한 보급을 확대하고 있습니다. 병원 및 청각센터와의 제휴를 통해 수술에 대한 접근성과 환자의 신뢰를 높이고 있습니다. 개발도상국 시장으로의 지리적 확장은 미개척 수요를 포착하는 데 도움이 되며, 보험사 및 정부와의 전략적 제휴를 통해 가격 및 보급률을 높이고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 상환 시나리오

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- LAMEA

- 기술 동향

- 현재 기술 동향

- 신기술

- 세계

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 소비자 경로

- 가격 분석, 2024

- 소비자 통찰

- 정책 환경

- 리스크 관리 분석

- 연구개발

- 오퍼레이션즈

- 마케팅 및 판매

- 품질

- 지적재산권

- 규제

- 정보기술

- 기후

- 재무

- 향후 시장 동향

- 공급망 동향과 제조 분석

- 파이프라인 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 갭 분석

제4장 경쟁 구도

- 서론

- 기업 매트릭스 분석

- 기업의 시장 점유율 분석

- 세계

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카, 중동 및 아프리카

- 경쟁 포지셔닝 매트릭스

- 주요 시장 기업의 경쟁 분석

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추산·예측 : 제품별, 2021-2034

- 주요 동향

- 편측 임플란트

- 양측 임플란트

제6장 시장 추산·예측 : 환자 유형별, 2021-2034

- 주요 동향

- 성인

- 소아

제7장 시장 추산·예측 : 최종 용도별, 2021-2034

- 주요 동향

- 병원

- 이비인후과 클리닉

- 외래수술센터(ASC)

제8장 시장 추산·예측 : 지역별, 2021-2034

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 개요

- Cochlear

- Envoy Medical

- MED-EL

- Nurotron

- Sonova

The Global Cochlear Implants Market was valued at USD 1.9 billion in 2024 and is estimated to grow at a CAGR of 7.6% to reach USD 3.9 billion by 2034.

Market expansion is driven by the rising prevalence of hearing impairment, innovations in implant technology, increasing adoption among children and the elderly, and heightened awareness coupled with widespread hearing screening programs. Cochlear implants are advanced electronic devices designed to bypass damaged inner ear hair cells and directly stimulate the auditory nerve, enabling users to perceive sound. They consist of internal and external components that collect, process, and transmit sound signals. Unlike hearing aids that amplify sound, cochlear implants convert sound into electrical impulses to partially restore hearing. Growing awareness campaigns and early screening in schools and hospitals are helping identify candidates sooner, while collaborations among audiology associations, healthcare providers, and implant manufacturers have enhanced patient education, driving higher procedural acceptance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.9 Billion |

| Forecast Value | $3.9 Billion |

| CAGR | 7.6% |

The unilateral implants segment held 86.1% share in 2024 due to its lower cost, simpler surgery, quicker recovery, and preference among clinicians over bilateral implants. Unilateral implants remain more accessible to patients and healthcare providers because of their cost advantage, particularly in developing markets. This affordability encourages adoption among individuals seeking improved hearing without the expense of dual implantation.

The hospitals segment generated a 46.9% share in 2024 and is expected to reach USD 1.7 billion during 2025-2034. An increase in sensorineural hearing loss cases, driven by aging populations, prolonged exposure to noise, and congenital conditions, has resulted in more patients seeking treatment in hospitals. Hospitals benefit by integrating cochlear implant procedures into their ENT and audiology services, enhancing patient care and revenue streams.

North America Cochlear Implants Market held a 41.2% share in 2024. The region's population faces high rates of sensorineural hearing loss, including age-related and congenital cases, prompting early diagnosis and intervention programs. These initiatives have substantially boosted the demand for cochlear implants, driving steady market growth.

Key companies in the Cochlear Implants Market include MED-EL, Cochlear, Sonova, Envoy Medical, and Nurotron. Market players in the Global Cochlear Implants Market are employing several strategies to strengthen their market foothold. Companies are investing in research and development to enhance implant functionality, comfort, and compatibility with advanced sound processing technologies. They are expanding pediatric and geriatric adoption through targeted awareness campaigns and educational initiatives for healthcare professionals. Partnerships with hospitals and audiology centers improve procedural access and patient trust. Geographic expansion into developing markets helps capture untapped demand, while strategic collaborations with insurance providers and governments increase affordability and adoption rates.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Patient type trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increase in prevalence of hearing loss

- 3.2.1.2 Technological advancements

- 3.2.1.3 Rising awareness and early diagnosis

- 3.2.1.4 Facilitative government support and improving reimbursement scenario

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of cochlear implants

- 3.2.2.2 Lack of knowledge regarding hearing loss

- 3.2.3 Market opportunities

- 3.2.3.1 AI-driven sound processing & machine learning

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Reimbursement scenario

- 3.5 Regulatory landscape

- 3.5.1 North America

- 3.5.2 Europe

- 3.5.3 Asia Pacific

- 3.5.4 LAMEA

- 3.6 Technology landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Market size in terms of volume, 2021 - 2034 (Units)

- 3.7.1 Global

- 3.7.2 North America

- 3.7.3 Europe

- 3.7.4 Asia Pacific

- 3.7.5 Latin America

- 3.7.6 MEA

- 3.8 Consumer pathway

- 3.9 Pricing analysis, 2024

- 3.10 Consumer insights

- 3.11 Policy landscape

- 3.11.1 Risk management analysis

- 3.11.2 Research and development

- 3.11.3 Operations

- 3.11.4 Marketing and sales

- 3.11.5 Quality

- 3.11.6 Intellectual property rights

- 3.11.7 Regulatory

- 3.11.8 Information technology

- 3.11.9 Climate

- 3.11.10 Financial

- 3.12 Future market trends

- 3.13 Supply chain dynamics & manufacturing analysis

- 3.14 Pipeline analysis

- 3.15 Porter's analysis

- 3.16 PESTEL analysis

- 3.17 Gap analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Company market share analysis

- 4.3.1 Global

- 4.3.2 North America

- 4.3.3 Europe

- 4.3.4 Asia Pacific

- 4.3.5 LAMEA

- 4.4 Competitive positioning matrix

- 4.5 Competitive analysis of major market players

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Unilateral implants

- 5.3 Bilateral implants

Chapter 6 Market Estimates and Forecast, By Patient Type, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Adult

- 6.3 Pediatric

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 ENT clinics

- 7.4 Ambulatory surgical centers

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Cochlear

- 9.2 Envoy Medical

- 9.3 MED-EL

- 9.4 Nurotron

- 9.5 Sonova