|

시장보고서

상품코드

1667064

군용 레이더 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Military Radar Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

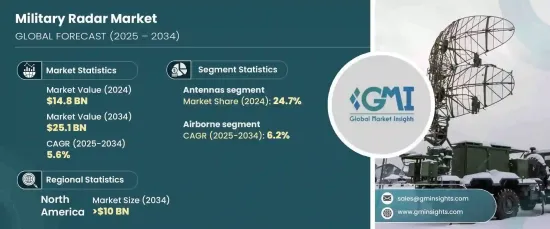

세계의 군용 레이더 시장은 강력한 성장을 이루고 있으며, 2024년에는 148억 달러에 이르렀고, 2025년부터 2034년에 걸쳐 CAGR 5.6%로 확대될 것으로 예측되고 있습니다.

이러한 급성장의 배경에는 각국이 안보 우려와 지정학적 긴장 증가에 대응하기 때문에 세계적으로 방위 예산이 확대되고 있습니다. 각국 정부는 국방 능력을 현대화하고, 국가 안보를 강화하고, 새로운 위협에 대응하기 위해 첨단 레이더 시스템에 대한 투자를 선호합니다. 위상 어레이 및 액티브 전자 스캔 어레이(AESA) 시스템을 포함한 차세대 레이더 기술의 채택이 확대되고 있는 것은 감지 정밀도, 추적 정밀도, 상황 인식의 향상에 중점을 두고 있음을 뒷받침하고 있습니다. 장거리 감지 및 신속한 위협 식별과 같은 향상된 기능으로 레이더 기술은 현대 군사 전략의 핵심으로 자리매김하고 있습니다. 또한, 방위 계약자와 정부 간의 협력이 기술 혁신에 박차를 가하고 진화하는 전투와 감시의 요구에 맞춘 최첨단 레이더 시스템의 개발을 뒷받침하고 있습니다.

시장은 안테나, 송신기, 수신기, 전력 증폭기, 안정화 시스템, 듀플렉서, 디지털 신호 프로세서, 그래픽 사용자 인터페이스 등을 포함한 구성 요소로 구분됩니다. 이 분야에서는 안테나가 주류이며 2024년 시장 점유율은 24.7%에 달했습니다. 레이더 기능에서 중요한 역할을 하는 안테나는 전기 신호를 전자파로 변환하고 그 반대의 변환을 수행하는 능력에서 유래합니다. 이 능력은 감지, 추적 및 조준에서 레이더의 성능을 결정하며 안테나는 탁월한 감지 거리, 정확성 및 해상도를 달성하는 데 필수적입니다. 경량 소재와 개선된 빔포밍 기술을 포함한 안테나 기술의 혁신은 효율성과 신뢰성을 더욱 높여 레이더 전반의 에코시스템에서 안테나의 중요성을 확고히 하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 148억 달러 |

| 예측 금액 | 251억 달러 |

| CAGR | 5.6% |

시장은 또한 플랫폼별로 지상 시스템, 해군 시스템, 공중 시스템, 우주 시스템으로 분류됩니다. 이 중 항공 분야는 가장 급성장하는 분야로 부상하고 있으며 예측 기간 중 CAGR은 6.2%로 예측되고 있습니다. 전투기, 정찰기, UAV에 탑재된 공중 레이더는 정찰 능력과 전투 능력 강화에 있어 매우 중요한 역할을 합니다. 이 시스템은 장거리 감지 및 추적이 뛰어나므로 군는 스텔스 항공기와 미사일 시스템과 같은 고급 위협에 대응할 수 있습니다. 위상 배열과 AESA 기술의 통합은 더 빠른 스캔 속도, 더 넓은 주파수 범위 및 더 높은 해상도를 제공함으로써 능력을 더욱 향상시켜 복잡한 전투 시나리오에서 작전 효율과 상황 인식을 크게 향상시킵니다.

북미는 세계의 군용 레이더 시장을 독점하고 2034년까지 100억 달러를 창출할 것으로 예상됩니다. 미국이 주도하는 이 리더십은 엄청난 국방 예산과 기술 진보에 대한 전략적 집중을 반영합니다. 이 지역은 감시, 조기 경계 및 전투 관리를 위한 최신 레이더 시스템에 대한 투자를 우선시합니다. AI 통합과 같은 신기술은 레이더 능력을 강화하고 첨단 군사 작전에 대한 적응성과 효능을 높이고 있습니다. 캐나다도 중요한 역할을 하고 있으며, 선진적인 레이더 개발과 방어 인프라 강화를 목적으로 한 국제 협력을 통해 공헌하고 있으며, 이 지역 시장 성장을 더욱 촉진하고 있습니다.

목차

제1장 조사 방법과 조사 범위

- 시장 범위와 정의

- 기본 추정과 계산

- 예측 계산

- 데이터 소스

- 1차 데이터

- 2차 데이터

- 유료 정보원

- 공적 정보원

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 방해

- 장래의 전망

- 제조업체

- 유통업체

- 공급자의 상황

- 이익률 분석

- 주요 뉴스

- 규제 상황

- 영향요인

- 성장 촉진요인

- 국방 예산 및 현대화 노력 증가

- 레이더 기술과 능력의 진보

- 고급 모니터링 시스템에 대한 수요 증가

- 향상된 위협 탐지 및 대응 요구 사항

- AI나 자율형 플랫폼과의 통합

- 업계의 잠재적 위험 및 과제

- 고급 레이더 시스템의 고비용

- 규제 및 수출규제의 제한

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추계·예측 : 구성 요소별(2021-2034년)

- 주요 동향

- 안테나

- 포물선 반사기 안테나

- 슬롯형 도파관 안테나

- 위상 배열 안테나

- 다중 입력-다중 출력 안테나

- 액티브 스캔 어레이 안테나

- 패시브 스캔 어레이 안테나

- 송신기

- 마이크로파 튜브 기반 송신기

- 무접점 전자 송신기

- 수신기

- 아날로그 수신기

- 디지털 수신기

- 전력 증폭기

- 이동파관 증폭기

- 고체 전력 증폭기

- 갈륨 비소

- 질화 갈륨

- 실리콘 카바이드

- 고체 전력 증폭기

- 이동파관 증폭기

- 듀플렉서

- 분기형 듀플렉서

- 밸런스형 듀플렉서

- 서큘레이터 듀플렉서

- 디지털 신호 프로세서

- 안정화 시스템

- 그래픽 사용자 인터페이스

- 기타

제6장 시장 추계·예측 : 파형별(2021-2034년)

- 주요 동향

- 주파수 변조 연속파

- 도플러

- 기존 도플러

- 펄스 도플러

제7장 시장 추계·예측 : 기술별(2021-2034년)

- 주요 동향

- 소프트웨어 정의 레이더

- 기존 레이더

- 퀀텀 레이더

제8장 시장 추계·예측 : 거리별(2021-2034년)

- 주요 동향

- 단거리(50kms 미만)

- 중거리(50-200kms)

- 장거리(200kms 초과)

제9장 시장 추계·예측 : 플랫폼별(2021-2034년)

- 주요 동향

- 지상 기반

- 고정 레이더

- 차량 기반 레이더

- 사람 휴대형 레이더

- 해군

- 선박 기반 레이더

- 해안 레이더

- USV 탑재 레이더

- 항공

- 유인 항공기 레이더

- UAV 탑재 레이더

- 항공 기반 레이더

- 우주

- 위성

- 우주선

제10장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 영공 모니터링 및 교통 관리

- 항공 및 미사일 방어

- 무기 유도

- 지상 감시 및 침입자 탐지

- 선박 교통 보안 및 감시

- 공중 매핑

- 네비게이션

- 지뢰 탐지 및 지하 매핑

- 지상군 보호 및 대응 매핑

- 기상 모니터링

- 지상 침투

- 해상 경비, 수색 및 구조

- 국경 보안

- 우주 상황 인식

- 기타

제11장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제12장 기업 프로파일

- Aselsan AS

- BAE Systems plc

- Boeing Company

- Cobham plc

- FLIR Systems, Inc.

- General Dynamics Corporation

- Hensoldt AG

- Honeywell International

- Israel Aerospace Industries

- L3Harris Technologies, Inc.

- Leonardo SPA

- Lockheed Martin Corporation

- Northrop Grumman Corporation

- Raytheon Technologies Corporation

- Rheinmetall AG

- Saab AB

- Thales Group

The Global Military Radar Market is poised for robust growth, reaching USD 14.8 billion in 2024 and projected to expand at a CAGR of 5.6% between 2025 and 2034. This surge is driven by escalating defense budgets worldwide as nations respond to mounting security concerns and geopolitical tensions. Governments are prioritizing investments in advanced radar systems to modernize their defense capabilities, enhance national security, and counter emerging threats. The growing adoption of next-generation radar technologies, including phased array and active electronically scanned array (AESA) systems, underscores the emphasis on improving detection accuracy, tracking precision, and situational awareness. Enhanced functionality, such as long-range detection and rapid threat identification, positions radar technology as a cornerstone of modern military strategies. In addition, collaborations between defense contractors and governments are spurring innovation, propelling the development of cutting-edge radar systems tailored to evolving combat and surveillance needs.

The market is segmented by components, including antennas, transmitters, receivers, power amplifiers, stabilization systems, duplexers, digital signal processors, graphical user interfaces, and others. Antennas dominate this segment, holding a 24.7% market share in 2024. Their critical role in radar functionality stems from their ability to convert electrical signals into electromagnetic waves and vice versa. This capability determines radar performance in detection, tracking, and targeting, making antennas essential for achieving superior range, accuracy, and resolution. Innovations in antenna technology, such as lightweight materials and improved beamforming techniques, are further enhancing their efficiency and reliability, cementing their importance in the overall radar ecosystem.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $14.8 Billion |

| Forecast Value | $25.1 Billion |

| CAGR | 5.6% |

The market is also categorized by platform into ground-based, naval, airborne, and space systems. Among these, the airborne segment is emerging as the fastest-growing category, projected to grow at a CAGR of 6.2% during the forecast period. Airborne radars deployed on fighter jets, surveillance aircraft, and UAVs play a pivotal role in enhancing reconnaissance and combat capabilities. These systems excel in long-range detection and tracking, enabling militaries to counter advanced threats, including stealth aircraft and missile systems. The integration of phased array and AESA technologies further elevates their capabilities by offering faster scanning speeds, wider frequency coverage, and higher resolution, which significantly improve operational efficiency and situational awareness in complex battle scenarios.

North America is set to dominate the global military radar market, expected to generate USD 10 billion by 2034. This leadership, spearheaded by the United States, reflects substantial defense budgets and a strategic focus on technological advancements. The region prioritizes investments in modern radar systems for surveillance, early warning, and combat management. Emerging technologies like AI integration are enhancing radar capabilities, making them more adaptive and effective for sophisticated military operations. Canada also plays a vital role, contributing through advanced radar development and international collaborations aimed at fortifying defense infrastructure, further driving regional market growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing defense budgets and modernization efforts

- 3.6.1.2 Advancements in radar technology and capabilities

- 3.6.1.3 Rising demand for advanced surveillance systems

- 3.6.1.4 Enhanced threat detection and countermeasure needs

- 3.6.1.5 Integration with AI and autonomous platforms

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High cost of advanced radar systems

- 3.6.2.2 Regulatory and export control restrictions

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021-2034 (USD Million)

- 5.1 Key trends

- 5.2 Antennas

- 5.2.1 Parabolic reflector antennas

- 5.2.2 Slotted waveguide antennas

- 5.2.3 Phased array antennas

- 5.2.4 Multiple Input-Multiple output antennas

- 5.2.5 Active scanned array antennas

- 5.2.6 Passive scanned array antennas

- 5.3 Transmitters

- 5.3.1 Microwave Tube-Based Transmitters

- 5.3.2 Solid-State electronic transmitters

- 5.4 Receivers

- 5.4.1 Analog receivers

- 5.4.2 Digital receivers

- 5.5 Power amplifiers

- 5.5.1 Traveling wave tube amplifiers

- 5.5.1.1 Solid-State power amplifiers

- 5.5.1.1.1 Gallium arsenide

- 5.5.1.1.2 Gallium nitride

- 5.5.1.1.3 Silicon carbide

- 5.5.1.1 Solid-State power amplifiers

- 5.5.1 Traveling wave tube amplifiers

- 5.6 Duplexers

- 5.6.1 Branch-Type duplexers

- 5.6.2 Balanced-Type duplexers

- 5.6.3 Circulator duplexers

- 5.7 Digital signal processors

- 5.8 Stabilization systems

- 5.9 Graphical user interfaces

- 5.10 Others

Chapter 6 Market Estimates & Forecast, By Waveform, 2021-2034 (USD Million)

- 6.1 Key trends

- 6.2 Frequency-Modulated continuous wave

- 6.3 Doppler

- 6.3.1 Conventional doppler

- 6.3.2 Pulse-Doppler

Chapter 7 Market Estimates & Forecast, By Technology, 2021-2034 (USD Million)

- 7.1 Key trends

- 7.2 Software-Defined radars

- 7.3 Conventional radars

- 7.4 Quantum radars

Chapter 8 Market Estimates & Forecast, By Range, 2021-2034 (USD Million)

- 8.1 Key trends

- 8.2 Short (<50 Kms)

- 8.3 Medium (50-200 Kms)

- 8.4 Long (>200 Kms)

Chapter 9 Market Estimates & Forecast, By Platform, 2021-2034 (USD Million)

- 9.1 Key trends

- 9.2 Ground-Based

- 9.2.1 Fixed radars

- 9.2.2 Vehicle-Based radars

- 9.2.3 Man-Portable radars

- 9.3 Naval

- 9.3.1 Vessel-Based radars

- 9.3.2 Coastal radars

- 9.3.3 USV-Mounted radars

- 9.4 Airborne

- 9.4.1 Manned aircraft radars

- 9.4.2 UAV-Mounted radars

- 9.4.3 Aerostats-Based radar

- 9.5 Space

- 9.5.1 Satellites

- 9.5.2 Spacecraft

Chapter 10 Market Estimates & Forecast, By Application, 2021-2034 (USD Million)

- 10.1 Key trends

- 10.2 Airspace Monitoring & Traffic management

- 10.3 Air & Missile defense

- 10.4 Weapon guidance

- 10.5 Ground Surveillance & Intruder Detection

- 10.6 Vessel Traffic Security & Surveillance

- 10.7 Airborne mapping

- 10.8 Navigation

- 10.9 Mine Detection & Underground mapping

- 10.10 Ground Force Protection & Counter-Mapping

- 10.11 Weather monitoring

- 10.12 Ground penetration

- 10.13 Maritime Patrolling, Search, & Rescue

- 10.14 Border security

- 10.15 Space situational awareness

- 10.16 Others

Chapter 11 Market Estimates & Forecast, By Region, 2021-2034 (USD Million)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 UK

- 11.3.2 Germany

- 11.3.3 France

- 11.3.4 Italy

- 11.3.5 Spain

- 11.3.6 Russia

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 India

- 11.4.3 Japan

- 11.4.4 South Korea

- 11.4.5 Australia

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.6 MEA

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Aselsan A.S.

- 12.2 BAE Systems plc

- 12.3 Boeing Company

- 12.4 Cobham plc

- 12.5 FLIR Systems, Inc.

- 12.6 General Dynamics Corporation

- 12.7 Hensoldt AG

- 12.8 Honeywell International

- 12.9 Israel Aerospace Industries

- 12.10 L3Harris Technologies, Inc.

- 12.11 Leonardo S.P.A.

- 12.12 Lockheed Martin Corporation

- 12.13 Northrop Grumman Corporation

- 12.14 Raytheon Technologies Corporation

- 12.15 Rheinmetall AG

- 12.16 Saab AB

- 12.17 Thales Group