|

시장보고서

상품코드

1667152

태양열 지역 난방 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Solar District Heating Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

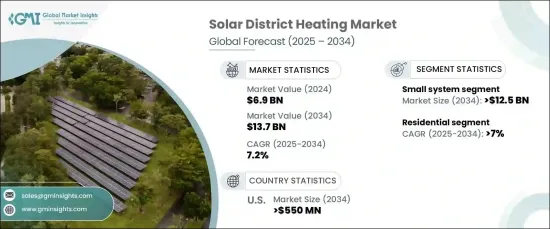

세계의 태양열 지역 난방 시장은 2024년 69억 달러에 달했으며, 2025년부터 2034년까지 CAGR 7.2%로 견조한 성장이 전망되고 있습니다.

이 시장 성장은 태양열 난방 시스템의 채용을 촉진하는 강력한 정책적 인센티브와 규제조치에 힘입어 재생가능 에너지로의 전환이 진행되고 있는 것이 배경에 있습니다. 세계 각국의 정부는 보다 엄격한 에너지 효율 기준을 도입하고 신재생에너지 도입에 인센티브를 주고 있으며, 태양열 지역 난방 솔루션에 역동적인 환경을 조성하고 있습니다. 또한 고성능 집열기와 강화된 축열 시스템의 개발 등 태양열 기술의 발전으로 태양열 지역 난방의 효율과 비용 효율성이 향상되고 있습니다. 이러한 기술 혁신은 시스템 성능을 향상시킬 뿐만 아니라 폭넓은 소비자의 이용을 확대하고 시장 도입을 더욱 가속시킬 것으로 보입니다.

태양열 지역 난방 시장의 성장은 태양열 솔루션의 끊임없는 진화로 인한 것입니다. 에너지 효율은 산업계, 정부, 소비자 모두에게 가장 큰 관심사입니다. 현재 사용 가능한 태양열 지역 난방 시스템은 이전보다 비용 효율적이며 이산화탄소 배출량을 줄이려는 소비자와 기업에게 점점 매력적인 선택이되고 있습니다. 세계가 야심찬 기후 변화 목표 달성에 가까워지면서 이러한 시스템은 기존 온실가스 배출의 주요 원인이었던 난방부문의 탈탄소화에 중요한 역할을 하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024년 |

| 예측연도 | 2025-2034년 |

| 시작금액 | 69억 달러 |

| 예측 금액 | 137억 달러 |

| CAGR | 7.2% |

2034년까지 소형 시스템 분야는 125억 달러를 창출할 것으로 예상됩니다. 이 분야는 지역 난방(DH) 시스템의 채용이 증가하고 있는 주택 및 상업개발 수요 증가로부터 혜택을 받을 것으로 보입니다. 이러한 작고 효율적인 시스템은 가정, 중소기업 및 중규모 산업의 난방 요구를 충족하도록 설계되었습니다. 보다 엄격한 온실가스 배출규제가 시행되고, 열과 전력을 위해 재생가능에너지를 이용하는 소비자가 늘어나면서 이 분야는 시장 확대에 크게 공헌하게 됩니다.

주택용 태양열 지역 난방시장도 대폭적인 성장이 예상되고 있으며, 2034년까지의 CAGR은 7%로 예측되고 있습니다. 환경 친화적인 건축 솔루션에 대한 수요 증가와 내부 열 부하 증가는 이 성장의 주요 촉진요인입니다. 소비자는 지속 가능한 난방 방법을 점점 더 요구하고 있으며, 태양열 지역 난방 시스템은 자연스럽게 적합합니다. 또한 온도 제어 기술 혁신, 기존 인프라와의 원활한 통합, 높은 운영 기준 준수는 시장 성장을 더욱 강화할 것입니다. 게다가 에너지 효율적인 인프라에 대한 대규모 투자와 단독주택이나 집합주택으로의 난방 네트워크의 확대가 지속적인 보급을 뒷받침할 것으로 보입니다.

미국의 태양열 지역 난방 시장은 2034년까지 5억 5,000만 달러를 창출할 것으로 예상됩니다. 지속가능하고 에너지 효율적인 난방 솔루션에 대한 소비자 수요 증가와 온실가스 배출량 감소에 초점을 맞춘 정부의 이니셔티브가 시장 궤도를 형성하고 있습니다. 태양열 수집기 기술과 열에너지 저장 시스템의 발전으로 주택, 상업 및 산업 분야의 열 공급이 더욱 강화됩니다. 주 수준의 인센티브와 신재생에너지 인프라에 대한 투자 증가는 태양열 지역 난방 시스템의 채택에 박차를 가하고 미국 시장의 대폭적인 성장을 가속할 것으로 예상됩니다.

목차

제1장 조사 방법과 조사 범위

- 시장 범위와 정의

- 시장 추계 및 예측 파라미터

- 예측 계산

- 데이터 소스

- 1차

- 2차

- 유료

- 공적

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 규제 상황

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크 및 과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 전략적 전망

- 혁신과 지속가능성의 전망

제5장 시장 규모와 예측 : 시스템별, 2021-2034년

- 주요 동향

- 소형 시스템

- 대형 시스템

제6장 시장 규모와 예측 : 용도별, 2021-2034년

- 주요 동향

- 주택용

- 상업용

- 산업용

제7장 시장 규모와 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 폴란드

- 러시아

- 스웨덴

- 핀란드

- 이탈리아

- 덴마크

- 영국

- 오스트리아

- 프랑스

- 아시아태평양

- 중국

- 일본

- 한국

제8장 기업 프로파일

- Aalborg CSP

- Fortum

- Goteborg Energy

- Kelag Energy

- Keppel DHCS

- Korea District Heating

- Logstor

- NRG Energy

- Ramboll Group

- RWE

- Savosolar

- Shinryo

- Statkraft

- STEAG

- Vattenfall

The Global Solar District Heating Market is projected to reach USD 6.9 billion in 2024 and is set to grow at a robust CAGR of 7.2% from 2025 to 2034. This market growth is driven by an increasing shift towards renewable energy, supported by strong policy incentives and regulatory measures that promote the adoption of solar heating systems. Governments worldwide are implementing stricter energy-efficiency standards and incentivizing renewable energy adoption, creating a dynamic environment for solar district heating solutions. In addition, advancements in solar thermal technology-such as the development of high-performance collectors and enhanced thermal storage systems-are making solar district heating more efficient and cost-effective. These innovations will not only improve system performance but also expand access to a broader range of consumers, further accelerating market adoption.

The growth of the solar district heating market can also be attributed to the continuous evolution of solar thermal solutions. Energy efficiency is a primary concern for industries, governments, and consumers alike. The solar district heating systems now available are more cost-effective than ever, making them an increasingly attractive option for consumers and businesses looking to reduce their carbon footprint. As the world moves closer to meeting ambitious climate goals, these systems play a key role in decarbonizing the heating sector, which has traditionally been a significant contributor to greenhouse gas emissions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.9 Billion |

| Forecast Value | $13.7 Billion |

| CAGR | 7.2% |

By 2034, the small system segment is expected to generate USD 12.5 billion. This segment will benefit from the growing demand for residential and commercial developments, which are increasingly adopting district heating (DH) systems. These small, efficient systems are designed to meet the heating needs of households, small businesses, and medium-sized industries. As stricter greenhouse gas emission regulations come into effect and a growing number of consumers turn to renewable energy for heat and power, this segment will contribute significantly to market expansion.

The residential solar district heating market is also poised for substantial growth, with a projected CAGR of 7% through 2034. Rising demand for eco-friendly building solutions and increasing internal heat loads are key drivers of this growth. Consumers are increasingly seeking sustainable heating options, and solar district heating systems are a natural fit. Moreover, technological innovations in temperature control, seamless integration with existing infrastructure, and adherence to higher operational standards will further bolster market growth. In addition, substantial investments in energy-efficient infrastructure and the expansion of heating networks to single-family homes and apartment complexes will fuel continued adoption.

The U.S. solar district heating market is expected to generate USD 550 million by 2034. Growing consumer demand for sustainable and energy-efficient heating solutions, along with government initiatives focused on reducing greenhouse gas emissions, will shape the market's trajectory. Advancements in solar collector technologies and thermal energy storage systems will further enhance heat delivery across residential, commercial, and industrial sectors. State-level incentives and increasing investments in renewable energy infrastructure are expected to spur the adoption of solar district heating systems, driving significant growth in the U.S. market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Growth potential analysis

- 3.5 Porter's analysis

- 3.5.1 Bargaining power of suppliers

- 3.5.2 Bargaining power of buyers

- 3.5.3 Threat of new entrants

- 3.5.4 Threat of substitutes

- 3.6 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By System, 2021 – 2034 (PJ & USD Million)

- 5.1 Key trends

- 5.2 Small systems

- 5.3 Large systems

Chapter 6 Market Size and Forecast, By Application, 2021 – 2034 (PJ & USD Million)

- 6.1 Key trends

- 6.2 Residential

- 6.3 Commercial

- 6.4 Industrial

Chapter 7 Market Size and Forecast, By Region, 2021 – 2034 (PJ & USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 Poland

- 7.3.3 Russia

- 7.3.4 Sweden

- 7.3.5 Finland

- 7.3.6 Italy

- 7.3.7 Denmark

- 7.3.8 UK

- 7.3.9 Austria

- 7.3.10 France

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 Japan

- 7.4.3 South Korea

Chapter 8 Company Profiles

- 8.1 Aalborg CSP

- 8.2 Fortum

- 8.3 Goteborg Energy

- 8.4 Kelag Energy

- 8.5 Keppel DHCS

- 8.6 Korea District Heating

- 8.7 Logstor

- 8.8 NRG Energy

- 8.9 Ramboll Group

- 8.10 RWE

- 8.11 Savosolar

- 8.12 Shinryo

- 8.13 Statkraft

- 8.14 STEAG

- 8.15 Vattenfall