|

시장보고서

상품코드

1684696

자동차용 배전 모듈 시장 기회, 성장 촉진 요인, 산업 동향 분석, 예측(2025-2034년)Automotive Power Distribution Modules Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

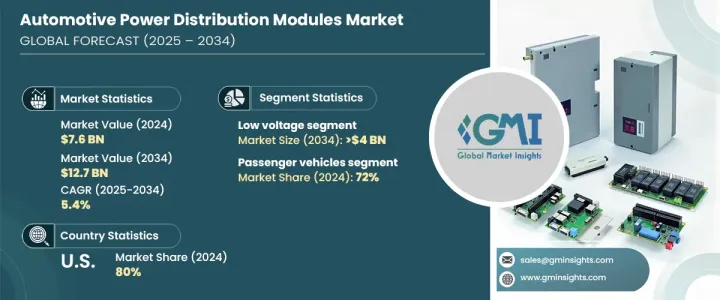

자동차용 배전 모듈 세계 시장은 2024년에 76억 달러에 이르렀고, 2025년부터 2034년에 걸쳐 CAGR 5.4%로 성장할 것으로 예측됩니다. 저연비로 친환경 자동차에 대한 수요가 높아지면서 배전 기술의 대폭적인 진보를 촉진하고 있습니다. 이러한 모듈은 다양한 차량 시스템 전체의 전력 소비를 관리하고 최적의 에너지 사용을 보장하며 낭비를 최소화하는 데 중요합니다. 자동차 제조업체들이 ADAS(첨단 운전 지원 시스템)부터 차세대 인포테인먼트 및 에어컨 제어에 이르기까지 더 많은 전자 부품을 지속적으로 통합하는 동안 효율적인 전력 관리의 필요성이 그 어느 때보다 높아지고 있습니다.

전기자동차와 하이브리드 자동차의 채용이 확대되고 있으며, 이러한 플랫폼에서는 전반적인 성능과 안전성을 높이기 위해 고도의 배전이 필요하기 때문에 수요가 더욱 높아지고 있습니다. 세계 각국 정부는 전기차(EV)의 보급을 촉진하기 위해 보다 엄격한 배출가스 규제를 실시하고 인센티브를 제공하고 있으며, 자동차 제조업체는 최첨단 에너지 효율이 우수한 솔루션에 대한 투자를 촉구하고 있습니다. 스마트 배전, 부하 분산 기능, 차량 탑재 진단 기능과의 통합과 같은 기술 혁신은 최신 자동차의 신뢰성과 효율을 높여줍니다. 게다가 소비자의 선호도가 지속가능한 운송 솔루션으로 변화하고 있다는 점도 시장 확대를 뒷받침하고 있으며, 업계 선두 기업들은 전력 흐름을 최적화하고, 에너지 손실을 줄이고, 확대하는 전동화 동향을 지원하는 차세대 모듈에 투자하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 76억 달러 |

| 예측 금액 | 127억 달러 |

| CAGR | 5.4% |

시장은 모듈 유형별로 저전압, 중전압, 고전압으로 구분됩니다. 2024년에는 저전압 모듈이 시장 점유율의 40%를 차지했고 2034년까지 40억 달러를 창출할 것으로 예상됩니다. 전기자동차와 하이브리드 자동차는 조명, 인포테인먼트, 에어컨 제어 등의 중요한 보조 기능에 전력을 공급하기 때문에 이러한 모듈의 사용이 증가하고 있으며, 이는 성장의 주요 요인이되었습니다. EV 시장이 급격히 증가함에 따라 이러한 시스템이 배터리 잔량을 소모하지 않고 안정적으로 작동할 수 있도록 효율적인 전력 관리 솔루션에 대한 필요성이 증가하고 있습니다. 제조업체 각 회사는 안전, 에너지 효율 및 에너지 절약을 향상시키기 위해 고급 배전 모듈을 통합하여 최신 차량 아키텍처의 핵심 구성 요소가 되었습니다. 첨단 스마트 시스템은 원활한 배전을 가능하게 하고, 과부하를 방지하고, 효율적인 에너지 이용을 보장하기 위해 더욱 보급을 촉진합니다.

차량 유형에 따라 시장은 승용차와 상용차로 분류됩니다. 2024년에는 승용차가 압도적이며 시장 점유율의 72%를 차지하고 있습니다. 전동 파워트레인과 ADAS를 포함한 차량용 전자 제품의 복잡성으로 인해 효율적인 배전 솔루션에 대한 수요가 증가하고 있습니다. 자동차 기술의 진화에 따라 자동차는 현재 안정적인 전력 공급이 필요한 여러 전자 부품에 의존하고 있습니다. 배전 모듈은 에너지 흐름을 조정하고 과부하를 방지하고 시스템 성능을 최적화하며 신뢰성을 높입니다. 자동차 제조업체는 기술 중심의 운전 경험에 대한 소비자의 기대 진화를 지원하기 위해 배전 시스템을 지속적으로 업그레이드하고 있으며, 안전성과 사용자 편의성을 모두 향상시키는 기능을 통합하고 있습니다. 스마트 차량 기술이 발전함에 따라 차세대 전력 관리 솔루션에 대한 수요가 급증할 것으로 예상됩니다.

미국의 자동차용 배전 모듈 시장은 2024년 세계 점유율의 80%를 차지합니다. 이 나라에서는 정부의 인센티브와 엄격한 배기가스 규제에 힘입어 자동차의 전동화를 적극적으로 추진하고 있으며, 시장 성장을 가속화하고 있습니다. EV 산업의 확대로 배터리 시스템, 모터 및 기타 중요한 구성 요소 간의 전기 흐름을 최적화하는 고급 전원 관리 솔루션에 대한 필요성이 커지고 있습니다. 배전 모듈은 효율적인 에너지 분배를 가능하게 하고 전기자동차의 안전하고 효율적인 운전을 보장합니다. 제조업체가 지속 가능한 솔루션과 최첨단 기술을 우선시하는 동안 최적화된 배전에 대한 수요는 계속 증가하고 있으며, 미국은 이 진화하는 업계에서 지배적인 선수로서 확고한 지위를 구축하고 있습니다.

목차

제1장 조사 방법과 조사 범위

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 기본 추정과 계산

- 기준연도의 산출

- 시장추계의 주요 동향

- 예측 모델

- 1차 조사와 검증

- 1차 정보

- 데이터 마이닝 소스

- 시장 범위와 정의

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 원재료 제공업체

- 부품 제조업체

- 제조업체

- 기술 제공업체

- 최종 고객

- 공급자의 상황

- 이익률 분석

- 기술 혁신의 상황

- 특허 분석

- 주요 뉴스 및 이니셔티브

- 규제 상황

- 가격 분석

- 영향요인

- 성장 촉진요인

- 자동차 일렉트로닉스의 진보

- 저연비차에 대한 소비자의 기호의 고조

- 스마트 배전 솔루션의 채용

- 전기자동차 인프라 확대

- 업계의 잠재적 위험 및 과제

- 첨단 모듈의 고비용

- 설계와 통합의 복잡성

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추정 및 예측 : 컴포넌트별, 2021년-2034년

- 주요 동향

- 파워 모듈

- 퓨즈와 회로 차단기

- 커넥터 및 단자

- 릴레이

- 전압 조정기

- 기타

제6장 시장 추정 및 예측 : 모듈별, 2021년-2034년

- 주요 동향

- 저전압

- 중전압

- 고전압

제7장 시장 추정 및 예측 : 차량별, 2021년-2034년

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV차

- 상용차

- 소형 상용차(LCV)

- 대형 상용차(HCV)

제8장 시장 추정 및 예측 : 용도별, 2021년-2034년

- 주요 동향

- 조명 시스템

- 인포테인먼트 시스템

- HVAC 시스템

- 안전 및 운전 지원 시스템

- 배터리 관리 시스템

- 기타

제9장 시장 추정 및 예측 : 판매 채널별, 2021년-2034년

- 주요 동향

- OEM

- 애프터마켓

제10장 시장 추정 및 예측 : 지역별, 2021년-2034년

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- UAE

- 남아프리카

- 사우디아라비아

제11장 기업 프로파일

- Aptiv

- Bosch

- Continental

- Delphi(BorgWarner)

- Denso

- Eaton

- Hitachi

- Infineon

- Lear Corporation

- Mitsubishi

- NXP Semiconductors

- ON Semiconductor

- Panasonic

- Sensata

- STMicroelectronics

- TE Connectivity

- Texas Instruments

- Valeo

- ZF Friedrichshafen

The Global Automotive Power Distribution Modules Market reached USD 7.6 billion in 2024 and is projected to grow at a CAGR of 5.4% between 2025 and 2034. Rising demand for fuel-efficient and eco-friendly vehicles is driving significant advancements in power distribution technology. These modules are critical in managing power consumption across various vehicle systems, ensuring optimal energy use and minimizing waste. As automakers continue to integrate more electronic components, from advanced driver-assistance systems (ADAS) to next-generation infotainment and climate control, the need for efficient power management has become more pressing than ever.

The growing adoption of electric and hybrid vehicles is further fueling demand, as these platforms require sophisticated power distribution to enhance overall performance and safety. Governments worldwide are implementing stricter emissions regulations and providing incentives to boost electric vehicle (EV) adoption, pushing automakers to invest in cutting-edge energy-efficient solutions. Technological innovations such as smart power distribution, load-balancing capabilities, and integration with onboard diagnostics are enhancing the reliability and efficiency of modern vehicles. Moreover, shifting consumer preferences toward sustainable transportation solutions reinforces the market's expansion, with industry leaders investing in next-generation modules to optimize power flow, reduce energy loss, and support growing electrification trends.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.6 Billion |

| Forecast Value | $12.7 Billion |

| CAGR | 5.4% |

The market is segmented by module type into low voltage, medium voltage, and high voltage. In 2024, low voltage modules accounted for 40% of the market share and are expected to generate USD 4 billion by 2034. The increasing use of these modules in electric and hybrid vehicles is a major driver of growth, as they power essential auxiliary functions such as lighting, infotainment, and climate control. With the EV market expanding rapidly, the need for efficient power management solutions has intensified to ensure these systems operate reliably without draining battery reserves. Manufacturers are integrating advanced power distribution modules to improve safety, energy efficiency, and conservation, making them a key component in modern vehicle architecture. Advanced smart systems allow seamless distribution of electricity, preventing overload and ensuring efficient energy use, further driving adoption.

Based on vehicle type, the market is categorized into passenger and commercial vehicles. Passenger vehicles dominated in 2024, holding 72% of the market share. The increasing complexity of in-vehicle electronics, including electric powertrains and ADAS, has heightened the demand for efficient power distribution solutions. As automotive technology evolves, vehicles now rely on multiple electronic components that require stable power delivery. Power distribution modules regulate energy flow, preventing overloads, optimizing system performance, and enhancing reliability. Automakers are continuously upgrading distribution systems to support evolving consumer expectations for technology-driven driving experiences, integrating features that enhance both safety and user convenience. As smart vehicle technology continues to advance, the demand for next-generation power management solutions is expected to surge.

The US automotive power distribution modules market accounted for 80% of the global share in 2024. The country's aggressive push toward vehicle electrification, supported by government incentives and stringent emissions regulations, is accelerating market growth. The expanding EV industry has intensified the need for advanced power management solutions that optimize electrical flow between battery systems, motors, and other critical components. Power distribution modules enable efficient energy allocation, ensuring electric vehicles operate safely and efficiently. As manufacturers prioritize sustainable solutions and cutting-edge technology, the demand for optimized power distribution continues to rise, solidifying the US as a dominant player in this evolving industry.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material providers

- 3.1.2 Component providers

- 3.1.3 Manufacturers

- 3.1.4 Technology providers

- 3.1.5 End customers

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Price analysis

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Advancements in automotive electronics

- 3.9.1.2 growing consumer preference for fuel-efficient vehicles

- 3.9.1.3 Adoption of smart power distribution solutions

- 3.9.1.4 Expansion of electric vehicle infrastructure

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High cost of advanced modules

- 3.9.2.2 Complexity in design and integration

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Component, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Power modules

- 5.3 Fuses and circuit breakers

- 5.4 Connectors and terminals

- 5.5 Relays

- 5.6 Voltage regulators

- 5.7 Others

Chapter 6 Market Estimates & Forecast, By Module, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Low voltage

- 6.3 Medium voltage

- 6.4 High voltage

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger vehicles

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUVs

- 7.3 Commercial vehicles

- 7.3.1 Light Commercial Vehicles (LCVs)

- 7.3.2 Heavy Commercial Vehicles (HCVs)

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Lighting systems

- 8.3 Infotainment systems

- 8.4 HVAC systems

- 8.5 Safety and driver assistance systems

- 8.6 Battery management systems

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 North America

- 10.1.1 U.S.

- 10.1.2 Canada

- 10.2 Europe

- 10.2.1 UK

- 10.2.2 Germany

- 10.2.3 France

- 10.2.4 Italy

- 10.2.5 Spain

- 10.2.6 Russia

- 10.2.7 Nordics

- 10.3 Asia Pacific

- 10.3.1 China

- 10.3.2 India

- 10.3.3 Japan

- 10.3.4 Australia

- 10.3.5 South Korea

- 10.3.6 Southeast Asia

- 10.4 Latin America

- 10.4.1 Brazil

- 10.4.2 Mexico

- 10.4.3 Argentina

- 10.5 MEA

- 10.5.1 UAE

- 10.5.2 South Africa

- 10.5.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Aptiv

- 11.2 Bosch

- 11.3 Continental

- 11.4 Delphi (BorgWarner)

- 11.5 Denso

- 11.6 Eaton

- 11.7 Hitachi

- 11.8 Infineon

- 11.9 Lear Corporation

- 11.10 Mitsubishi

- 11.11 NXP Semiconductors

- 11.12 ON Semiconductor

- 11.13 Panasonic

- 11.14 Sensata

- 11.15 STMicroelectronics

- 11.16 TE Connectivity

- 11.17 Texas Instruments

- 11.18 Valeo

- 11.19 ZF Friedrichshafen