|

시장보고서

상품코드

1871216

자동차용 48V 전기 정션 박스 및 전력 배전 센터 시장 : 기회, 성장 요인, 업계 동향 분석 예측(2025-2034년)Automotive 48-Volt Electronic Junction Box and Power Distribution Center Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

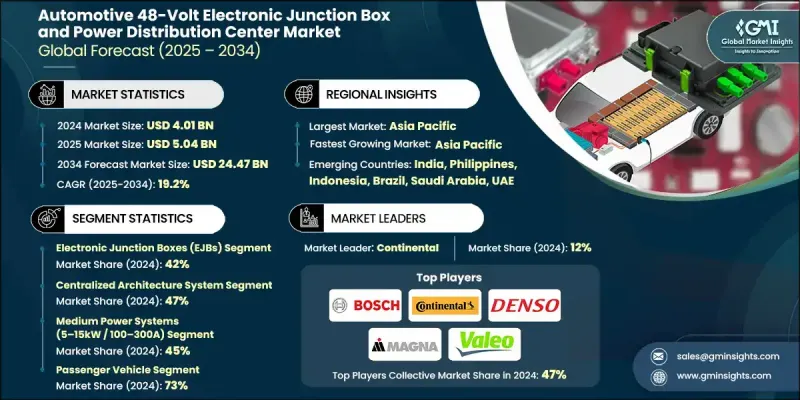

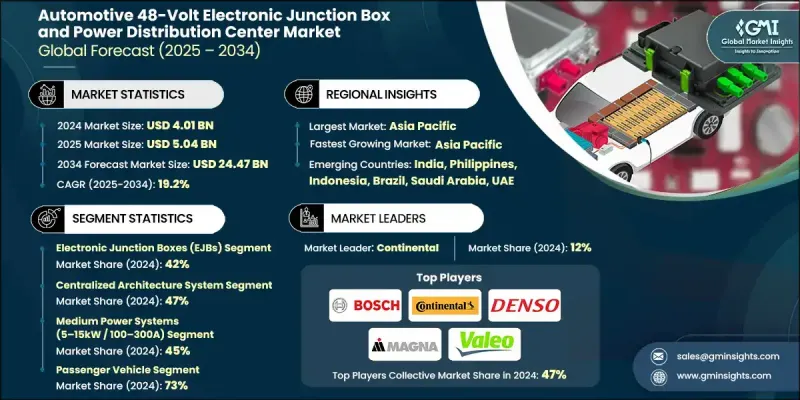

세계의 자동차용 48V 전기 정션 박스 및 전력 배전 센터 시장은 2024년 40억 1,000만 달러로 평가되었으며, 2034년까지 연평균 복합 성장률(CAGR) 19.2%로 성장하여 244억 7,000만 달러에 이를 것으로 예측됩니다.

자동차 제조업체가 차량의 전동화와 효율적인 전력 관리로 이행하는 움직임이 가속되는 가운데, 본 시장은 계속 확대되고 있습니다. 하이브리드 및 마일드 하이브리드 시스템의 인기가 높아짐에 따라 배출가스 최소화, 회생 브레이크에 의한 에너지 회수 최적화, 고출력 차량 부품 지원을 실현하는 48V 아키텍처에 대한 수요가 확대되고 있습니다. 첨단 전자 시스템과 구역별 차량 설계의 통합으로 실시간 모니터링, 고장 감지 및 적응형 에너지 제어가 가능한 지능형 전력 배전 모듈의 중요성이 더욱 높아지고 있습니다. 또한 사이버 보안 및 소프트웨어 정의 차량 기술도 이 시장에서 매우 중요 해지고 있습니다. 제조업체와 Tier 1 공급업체는 암호화된 데이터 통신, 보안 부팅 프로토콜, 지속적인 시스템 모니터링과 같은 고급 보안 메커니즘을 도입했습니다. 이러한 혁신 기술은 전자 부품을 무단 액세스로부터 보호하고 안정적인 펌웨어 업데이트를 보장하며 상호 연결된 시스템 전체에서 일관된 전력 흐름을 유지합니다. 정교한 소프트웨어 관리와 하드웨어 기반 안전 기능을 결합하여 자동차 제조업체는 전동화 차량 플랫폼 전반에 걸쳐 높은 성능, 신뢰성 및 엄격한 배출 가스 규제 및 안전 기준을 준수합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 40억 1,000만 달러 |

| 예측 금액 | 244억 7,000만 달러 |

| CAGR | 19.2% |

전기 정션 박스(EJB) 부문은 2024년 42%의 점유율을 차지했고 2034년까지 연평균 복합 성장률(CAGR) 18.2%를 보일 것으로 예측됩니다. EJB는 차세대 차량의 복잡한 전기 네트워크를 관리하는 데 필수적인 기능을 가지고 있기 때문에 시장을 선도하고 있습니다. 이들은 기존의 릴레이와 퓨즈 대신 다양한 전력 배전 기능을 소형 모듈에 통합합니다. 또한 EJB는 정밀한 부하 관리, 실시간 진단, 최적화된 에너지 사용을 가능하게 하며, 48V 하이브리드 및 마일드 하이브리드 자동차 아키텍처에서 필수적인 존재가 되고 있습니다.

중앙 집중식 아키텍처 시스템 부문은 2024년에 47%의 점유율을 차지했으며, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 17.9%를 보일 것으로 예측됩니다. 이 구성은 전력 제어와 배전를 집중화하여 차량 전기 시스템을 간소화하고 배선 복잡성을 줄이기 때문에 여전히 주류입니다. 중앙 집중식 설정은 운영 신뢰성 향상, 제조 간소화, 여러 전자 부품의 에너지 효율 향상을 실현합니다.

중국의 자동차용 48V 전기 정션 박스 및 전력 배전 센터 시장은 2024년 6억 8,530만 달러의 매출을 기록해 30%의 점유율을 차지했습니다. 중국 시장은 저배출 차량을 촉진하는 정부의 우대 조치, 하이브리드 기술의 보급 가속, 엄격한 환경 정책의 실시에 힘입어 급속히 진화하고 있습니다. 도시화의 진전과 에너지 효율이 우수한 차량에 대한 소비자 수요 증가도 48V 시스템의 도입을 촉진하고 있습니다. 이 시스템은 전기 부하를 효과적으로 관리하여 차량 성능 향상과 편안함 기능 향상을 지원합니다.

세계의 자동차용 48V 전기 정션 박스 및 배전 센터 시장에 있어서, 주요 기업은 Bosch, Aptiv, Continental, Denso, BYD Company, Eaton, Valeo, Magna International, Furukawa Electric, Eberspacher Automotive Electronics 등이 참가하고 있습니다. 자동차용 48V 전기 정션 박스 및 배전 센터 업계의 기업들은 경쟁력을 강화하기 위해 여러 전략적 노력을 추진하고 있습니다. 여기에는 제조 능력 확충, 주요 자동차 제조업체와의 장기적인 제휴 관계 구축, 경량화, 소프트웨어 구동형, 에너지 절약 시스템 개발을 위한 연구 개발에의 적극적인 투자가 포함됩니다. 많은 기업들이 유연한 차량 통합을 실현하는 모듈 설계에 주력함과 동시에 제품 시험 및 최적화를 위한 디지털 시뮬레이션 툴의 도입을 진행하고 있습니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역별/국가별

- 기본 추정치와 계산

- 기준연도 계산

- 시장 추정에서의 주요 동향

- 1차 조사 및 검증

- 1차 정보

- 예측 모델

- 조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 전기자동차 및 하이브리드차의 생산 급증

- 자동차용 전자기기의 진보

- 전기자동차 충전 인프라 확충

- 60 VDC 임계치 이하 규제 준수에서의 우위성

- 업계의 잠재적 위험 및 과제

- 48V 시스템의 높은 초기 비용

- 숙련노동력 부족

- 시장 기회

- 신흥 시장에서의 성장

- 스마트 전력 배전 시스템 개발

- 자율주행 기술과의 통합

- 협업 및 전략적 파트너십

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현재의 기술 동향

- 시스템 아키텍처 진화(12V에서 48V로의 전환)

- 전력 배전 토폴로지와 설계 접근법

- DC-DC 컨버터 시스템과의 통합

- 신흥기술

- 지능형 전력 관리와 AI 통합

- 존 아키텍처 및 소프트웨어 정의 차량

- 첨단 반도체 기술(GaN, SiC)

- 현재의 기술 동향

- 가격 동향

- 지역별

- 차량별

- 생산 통계

- 생산 거점

- 소비 거점

- 수출과 수입

- 코스트 내역 분석

- 재료 비용

- 제조 비용

- 엔지니어링 및 개발 비용

- 특허 분석

- 특허 출원 동향과 활동 상황

- 주요 특허 보유 기업 및 기술 리더 기업

- 혁신의 핫스팟과 기술 클러스터

- 특허 절벽 분석 및 지적 재산권 만료 시기의 타임라인

- R&D 투자 패턴 및 포트폴리오 전략

- 장래 시장 동향과 파괴적 변화

- 시장 발전 시나리오(2025-2030년)

- 기술 혁신의 타임라인

- 신흥 비즈니스 모델과 가치 제안

- 시장 통합과 M&A 동향

- 규제의 진화와 정책의 영향

- 경쟁 구도의 변화

- 지속가능성과 환경면

- 지속가능한 실천

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 환경에 배려한 대처

- 탄소발자국에 관한 고려 사항

- 이용 사례

- 풀 48V 아키텍처 탑재의 프리미엄 승용차

- EPTO 통합형 상용 플릿 차량

- V2G 통합형 산업용 마이크로그리드

- 최상의 시나리오

- 업계 표준화에 의한 풀 48V 아키텍처의 채용 가속

- 와이드 밴드갭 반도체의 비용과 성능에 있어서의 획기적인 진전

- 규제의 가속과 세계한 조화

- 에코시스템 통합과 플랫폼 수렴

- 성장 계획 및 전략적 개발 프레임워크

- 시장 진출 전략적 틀

- 제품 포트폴리오 개발 전략

- 지역 확대 계획 프레임워크

- 리스크 관리 및 시나리오 계획

- 전략적 구현 로드맵

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- LATAM

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- Robert Bosch GmbH

- Continental AG

- Valeo

- Eaton Corporation plc

- Aptiv PLC

- Denso Corporation

- Magna International

- 경쟁력 포지션 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수합병

- 신제품 발매

- 사업 확대 계획과 자금 조달

- 벤더 선정 기준과 결정 요인

- 기술적 능력과 성능 사양

- 품질, 신뢰성, 안전 기준

- 비용 구조 및 총 소유 비용

- 제조 및 공급망 능력

- 혁신 및 기술 리더십

- 규제 준수 및 인증

- 서비스 및 지원 능력

- 파트너십 및 협업 가능성

- 지리적 존재 및 현지화

- 지속가능성 및 환경책임

제5장 시장 추계 및 예측 : 차량별, 2021-2034년

- 주요 동향

- 승용차

- 해치백 자동차

- 세단

- SUV

- 상용차

- 소형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

- 승용차

제6장 시장 추계 및 예측 : 제품별, 2021-2034년

- 주요 동향

- 전자 접속 박스(EJB)

- 인텔리전트 정션 박스(마이크로컨트롤러 탑재)

- 스마트 정션 박스(기본 로직 탑재)

- 표준 정션 박스(패시브 배전)

- 전력 배전 센터(PDC)

- 주요 전력 배전 센터

- 보조 전력 배전 센터

- 특수용도용 PDC

- 통합형 전원 관리 유닛

제7장 시장 추계 및 예측 : 시스템 아키텍처별, 2021-2034년

- 주요 동향

- 중앙 집중식 아키텍처 시스템

- 분산형 아키텍처 시스템

- 하이브리드 아키텍처 시스템

제8장 시장 추계 및 예측 : 출력별, 2021-2034년

- 주요 동향

- 저전력 시스템(1-5kW/20-100A)

- 중출력 시스템(5-15kW/100-300A)

- 고출력 시스템(15-30kW/300-600A)

- 초고출력 시스템(30kW 초과/600A 초과)

제9장 시장 추계 및 예측 : 판매채널별, 2021-2034년

- 주요 동향

- OEM

- 애프터마켓

제10장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 싱가포르

- 인도네시아

- 필리핀

- 베트남

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카(MEA)

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- 세계 기업

- Aptiv

- Continental

- Eaton

- Leoni

- Littelfuse

- Bosch

- 지역 기업

- Delphi Technologies

- Sumitomo Electric Industries

- Valeo

- Yazaki

- 신흥기업

- Denso

- Furukawa Electric

- HELLA

- Hyundai Mobis

- Magna International

- Sensata Technologies

- Legal and Traditional Providers

- BYD Company

- Eberspacher Automotive Electronics

- Ficosa International

- IntegreL Solutions

- KOSTAL

- Lear

- Marelli

- Redler Technologies

- Samvardhana

- UAES(United Automotive Electronic Systems)

The Global Automotive 48-Volt Electronic Junction Box and Power Distribution Center Market was valued at USD 4.01 Billion in 2024 and is estimated to grow at a CAGR of 19.2% to reach USD 24.47 Billion by 2034.

This market is expanding as automakers increasingly transition toward vehicle electrification and efficient power management. The growing popularity of hybrid and mild-hybrid systems is fueling demand for 48V architectures that help minimize emissions, optimize energy recovery through regenerative braking, and support high-power vehicle components. The integration of advanced electronic systems and zonal vehicle designs has further elevated the importance of intelligent power distribution modules capable of real-time monitoring, fault detection, and adaptive energy control. Additionally, cybersecurity and software-defined vehicle technologies are becoming crucial in this market. Manufacturers and Tier-1 suppliers are introducing advanced security mechanisms such as encrypted data communication, secure boot protocols, and ongoing system surveillance. These innovations protect electronic components from unauthorized access, ensure stable firmware updates, and maintain consistent power flow across interconnected systems. By combining sophisticated software management with hardware-based safety features, automakers are ensuring high performance, reliability, and compliance with stringent emission and safety regulations across electrified vehicle platforms.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.01 Billion |

| Forecast Value | $24.47 Billion |

| CAGR | 19.2% |

The electronic junction boxes (EJBs) segment held a 42% share in 2024 and is projected to grow at a CAGR of 18.2% through 2034. EJBs dominate due to their essential function in managing complex electrical networks within next-generation vehicles. They integrate various power distribution functions into compact modules, replacing traditional relays and fuses. EJBs also enable precise load management, real-time diagnostics, and optimized energy usage, making them indispensable for 48V hybrid and mild-hybrid vehicle architectures.

The centralized architecture system segment held a 47% share in 2024 and is anticipated to grow at a CAGR of 17.9% from 2025 to 2034. This configuration remains dominant as it centralizes power control and distribution, streamlining vehicle electrical systems while reducing wiring complexity. Centralized setups also improve operational reliability, simplify manufacturing, and enhance energy efficiency across multiple electronic components.

China Automotive 48-Volt Electronic Junction Box and Power Distribution Center Market held a 30% share, generating USD 685.3 million in 2024. The market in China is evolving rapidly, supported by government incentives promoting low-emission vehicles, accelerating the adoption of hybrid technologies, and the enforcement of strict environmental policies. Growing urbanization and rising consumer demand for energy-efficient vehicles are also driving the deployment of 48V systems, which effectively manage electrical loads and support enhanced vehicle performance and comfort features.

Prominent players active in the Global Automotive 48-Volt Electronic Junction Box and Power Distribution Center Market include Bosch, Aptiv, Continental, Denso, BYD Company, Eaton, Valeo, Magna International, Furukawa Electric, and Eberspacher Automotive Electronics. To strengthen their position, companies in the Automotive 48-Volt Electronic Junction Box and Power Distribution Center Industry are implementing a mix of strategic initiatives. These include expanding manufacturing capabilities, forming long-term collaborations with leading automakers, and investing heavily in R&D to develop lightweight, software-driven, and energy-efficient systems. Many firms are focusing on modular designs to support flexible vehicle integration and adopting digital simulation tools for product testing and optimization.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2021 - 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 System Architecture

- 2.2.4 Vehicle

- 2.2.5 Power Rating

- 2.2.6 Sales Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Surge in electric and hybrid vehicle production

- 3.2.1.2 Advancements in automotive electronics

- 3.2.1.3 Expansion of electric vehicle charging infrastructure

- 3.2.1.4 Regulatory compliance advantages below 60 VDC threshold.

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High initial cost of 48v systems

- 3.2.2.2 Lack of skilled workforce.

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in emerging markets

- 3.2.3.2 Development of smart power distribution systems

- 3.2.3.3 Integration with autonomous vehicle technologies

- 3.2.3.4 Collaborations and strategic partnerships

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.3.1 Application growth ranking

- 3.3.2 Product segment growth comparison

- 3.3.3 Market maturity vs growth potential assessment

- 3.3.4 Competitive intensity and growth correlation

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 System architecture evolution (12v to 48v migration)

- 3.7.1.2 Power distribution topologies and design approaches

- 3.7.1.3 Integration with DC-DC converter systems

- 3.7.2 Emerging technologies

- 3.7.2.1 Intelligent power management and AI integration

- 3.7.2.2 Zonal architecture and software-defined vehicles

- 3.7.2.3 Advanced semiconductor technologies (GaN, SiC)

- 3.7.1 Current technological trends

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By vehicle

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.10.1 Material costs

- 3.10.2 Manufacturing costs

- 3.10.3 Engineering and development costs

- 3.11 Patent analysis

- 3.11.1 Patent filing trends and activity

- 3.11.2 Key patent holders and technology leaders

- 3.11.3 Innovation hotspots and technology clusters

- 3.11.4 Patent cliff analysis and ip expiration timeline

- 3.11.5 R&d investment patterns and portfolio strategies

- 3.12 Future market trends and disruptions

- 3.12.1 Market evolution scenarios (2025-2030)

- 3.12.2 Technology disruption timeline

- 3.12.3 Emerging business models and value propositions

- 3.12.4 Market consolidation and M&A trends

- 3.12.5 Regulatory evolution and policy impact

- 3.12.6 Competitive landscape transformation

- 3.13 Sustainability and environmental aspects

- 3.13.1 Sustainable practices

- 3.13.2 Waste reduction strategies

- 3.13.3 Energy efficiency in production

- 3.13.4 Eco-friendly initiatives

- 3.13.5 Carbon footprint considerations

- 3.14 Use cases

- 3.14.1. Premium passenger vehicle with full 48 v architecture

- 3.14.2 Commercial fleet vehicle with epto integration

- 3.14.3. Industrial microgrid with V2 G integration

- 3.15 Best-case scenario

- 3.15.1. Accelerated full 48 v architecture adoption with industry standardization

- 3.15.2 Breakthrough in wide-bandgap semiconductor cost and performance

- 3.15.3 Regulatory acceleration and global harmonization

- 3.15.4 Ecosystem integration and platform convergence

- 3.16 Growth planning & strategic development framework

- 3.16.1 Market entry strategy framework

- 3.16.2 Product portfolio development strategy

- 3.16.3 Geographic expansion planning framework

- 3.16.4 Risk management and scenario planning

- 3.16.5 Strategic implementation roadmap

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive Analysis of Major Market Players

- 4.3.1. Robert Bosch GmbH

- 4.3.2. Continental AG

- 4.3.3. Valeo

- 4.3.4. Eaton Corporation plc

- 4.3.5. Aptiv PLC

- 4.3.6. Denso Corporation

- 4.3.7. Magna International

- 4.4 Competitive position matrix.

- 4.5 Strategic outlook matrix

- 4.6 Key developments.

- 4.6.1 mergers & acquisitions

- 4.6.2 New product launches

- 4.6.3 Expansion plans and funding

- 4.7 Vendor selection criteria & decision factors

- 4.7.1 Technical capabilities & performance specifications

- 4.7.2 Quality, reliability & safety standards

- 4.7.3 Cost structure & total cost of ownership

- 4.7.4 Manufacturing & supply chain capabilities

- 4.7.5 Innovation & technology leadership

- 4.7.6 Regulatory compliance & certification

- 4.7.7 Service & support capabilities

- 4.7.8 Partnership & collaboration potential

- 4.7.9 Geographic presence & localization

- 4.7.10 Sustainability & environmental responsibility

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021-2034 ($Bn, Units)

- 5.1 Key trends

- 5.1.1 Passenger cars

- 5.1.1.1 Hatchbacks

- 5.1.1.2 Sedans

- 5.1.1.3 SUVs

- 5.1.2 Commercial vehicles

- 5.1.2.1 Light commercial vehicles (LCVs)

- 5.1.2.2 Medium commercial vehicles (MCVs)

- 5.1.2.3 Heavy commercial vehicles (HCVs)

- 5.1.1 Passenger cars

Chapter 6 Market Estimates & Forecast, By Product, 2021-2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Electronic Junction Boxes (EJBs)

- 6.2.1 Intelligent Junction Boxes (with microcontrollers)

- 6.2.2 Smart Junction Boxes (with basic logic)

- 6.2.3 Standard Junction Boxes (passive distribution)

- 6.3 Power Distribution Centers (PDCs)

- 6.3.1 Main Power Distribution Centers

- 6.3.2 Auxiliary Power Distribution Centers

- 6.3.3 Specialized Application PDCs

- 6.4 Integrated Power Management Units

Chapter 7 Market Estimates & Forecast, By System Architecture, 2021-2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Centralized architecture system

- 7.3 Distributed architecture system

- 7.4 Hybrid architecture system

Chapter 8 Market Estimates & Forecast, By Power Rating, 2021-2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Low Power Systems (1-5kW / 20-100A)

- 8.3 Medium Power Systems (5-15kW / 100-300A)

- 8.4 High Power Systems (15-30kW / 300-600A)

- 8.5 Ultra-High-Power Systems (>30kW / >600A)

Chapter 9 Market Estimates & Forecast, By Sales Channel, 2021-2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 OEMs

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Indonesia

- 10.4.8 Philippines

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 Aptiv

- 11.1.2 Continental

- 11.1.3 Eaton

- 11.1.4 Leoni

- 11.1.5 Littelfuse

- 11.1.6 Bosch

- 11.2 Regional Players

- 11.2.1 Delphi Technologies

- 11.2.2 Sumitomo Electric Industries

- 11.2.3 Valeo

- 11.2.4 Yazaki

- 11.3 Emerging Players

- 11.3.1 Denso

- 11.3.2 Furukawa Electric

- 11.3.3 HELLA

- 11.3.4 Hyundai Mobis

- 11.3.5 Magna International

- 11.3.6 Sensata Technologies

- 11.4 Legal and Traditional Providers

- 11.4.1 BYD Company

- 11.4.2 Eberspacher Automotive Electronics

- 11.4.3 Ficosa International

- 11.4.4 IntegreL Solutions

- 11.4.5 KOSTAL

- 11.4.6 Lear

- 11.4.7 Marelli

- 11.4.8 Redler Technologies

- 11.4.9 Samvardhana

- 11.4.10 UAES (United Automotive Electronic Systems)