|

시장보고서

상품코드

1684782

스티어링 휠 스위치 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Steering Wheel Switches Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

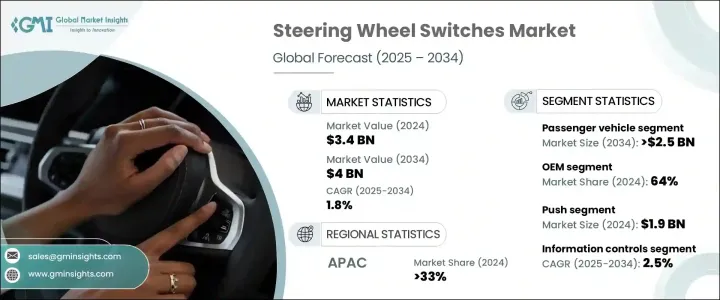

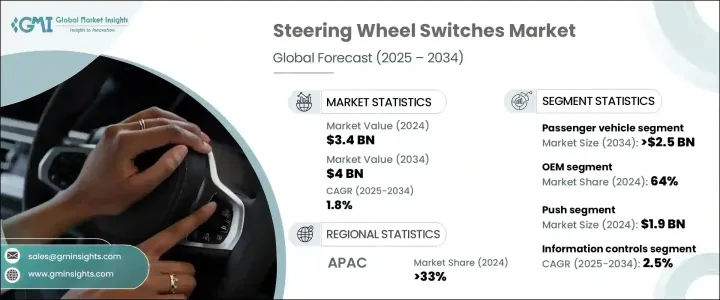

세계의 스티어링 휠 스위치 시장은 2024년 34억 달러로 평가되었고 2025년부터 2034년까지 연평균 복합 성장률(CAGR)은 1.8%를 나타낼 것으로 예측됩니다.

교통안전은 여전히 세계의 큰 관심사이며, 특히 선진지역에서는 자동차사고가 큰 사상자를 내고 있습니다. 소비자 의식의 높이는 규제의 영향과 높은 구매력과 함께 최신 안전 기술에 대한 수요가 증가하고 있습니다. 자동차 제조업체 각사는 자동차에 선진적인 운전 지원 기능을 탑재하는 경향을 강화하고 있으며, 안전성과 시장 확대를 모두 강화하고 있습니다. 운전자 보호를 중시하게 됨으로써, 스티어링 휠 일렉트로닉스의 채용에 박차가 걸려, 주의 산만을 줄이고, 전체적인 운전 효율을 향상시키고 있습니다. 다기능 스티어링 휠 컨트롤은 사용자 편의성을 높이는 동시에 업계 동향, 특히 전기자동차의 급속한 보급에 맞추어 인기를 끌고 있습니다. 원활한 자동차 제어 시스템으로의 전환은 시장 전망을 더욱 강화하고 있습니다.

승용차는 2024년에 60% 이상 시장 점유율을 차지했으며, 2034년에는 25억 달러 이상에 달할 것으로 예상됩니다. 세단, 해치백, SUV가 스티어링 휠 스위치 수요에 크게 기여하고 있습니다. 드라이버가 신경 쓰지 않고 인포테인먼트, 크루즈 컨트롤 및 통신 시스템을 관리할 수 있는 내장 컨트롤을 통해 제조업체는 보다 직관적이고 사용자 친화적인 인터페이스 통합에 주력하고 있습니다. 특히 도시 지역에서는 일상적으로 사용되는 자동차에 대한 수요가 높아지고 있으며, 스티어링 휠 탑재 스위치에 대한 요구가 더욱 높아지고 있습니다. 자동차 제조업체가 운전자의 편의성과 효율성을 우선시하는 동안 올인원 제어 솔루션은 최신 승용차의 중요한 구성 요소가 되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 34억 달러 |

| 예측 금액 | 40억 달러 |

| CAGR | 1.8% |

시장은 OEM과 애프터마켓 판매 채널로 나뉘어 2024년 점유율은 OEM이 64%를 차지했습니다. 스티어링 휠 스위치는 주로 OEM 제조업체에서 공급됩니다. 이러한 스위치가 최근 대부분의 자동차에 표준으로 장착되기 때문에 자동차 제조업체는 수요 증가에 대응하기 위해 생산 사이클을 확대하고 있습니다. 자동차 조립 라인은 효율적인 조달을 위해 공급업체에 의존하며 제조업체는 생산을 간소화하기 위해 자동화에 투자합니다. 특히 고성장 시장에서 신차에 대한 요구가 증가함에 따라 OEM 스티어링 스위치 수요가 증가하고 있습니다.

제품 부문에는 푸시 스위치와 See-saw 스위치가 있으며, 푸시 버튼 스위치 부문은 2024년에 19억 달러를 생산했습니다. 푸시 버튼은 인포테인먼트, 오디오, 크루즈 컨트롤 및 통신 기능에 널리 사용되며 직관적인 사용자 경험을 제공합니다. 내구성과 비용 효율성이 뛰어나 자동차 제조업체가 선호하며 저렴한 가격을 유지하면서 다기능 용도을 지원합니다. 첨단 전자 제품의 통합과 함께 차내 제어 시스템의 간소화로의 변화가 이 분야의 성장을 이어가고 있습니다.

인포테인먼트 컨트롤은 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 2.5% 이상을 나타낼 것으로 예상됩니다. 커넥티드 차량 기술의 채용이 증가하고 있어, 스티어링 휠 일체형의 인포테인먼트 기능에 대한 수요가 높아지고 있어, 보다 안전하고 편리한 인터랙션이 확보되고 있습니다. 네비게이션, 음성 명령 및 기타 기능에 대한 핸즈프리 액세스는 운전자의 안전과 사용자 경험을 모두 향상시키기 때문에 인포테인먼트 컨트롤은 최신 자동차에서 매우 중요한 요소가 되었습니다.

아시아태평양은 2024년 세계 시장을 선도하여 총 점유율의 33% 이상을 차지했습니다. 호조로운 자동차 생산과 스티어링 휠 컨트롤 수요 증가로 이 지역은 계속 시장 확대를 견인하고 있습니다.

목차

제1장 조사 방법과 조사 범위

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 기본 추정과 계산

- 기준연도의 산출

- 시장추계의 주요 동향

- 예측 모델

- 1차 조사와 검증

- 1차 소스

- 데이터 마이닝 소스

- 시장 범위와 정의

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 공급자의 상황

- 원재료 공급자

- 부품 공급자

- 제조업체

- 기술 제공업체

- 유통업체

- 최종 사용자

- 이익률 분석

- 공급자의 상황

- 기술과 혁신의 전망

- 특허 분석

- 규제 상황

- 가격 동향

- 영향요인

- 성장 촉진요인

- 세계의 자동차 판매 성장

- 교통안전에 대한 의식의 고조

- 자동차 부품 산업의 상승

- 자동차 제조 부문의 꾸준한 개발

- 자동차 일렉트로닉스와 어댑티브 크루즈 컨트롤 기술의 진보

- 업계의 잠재적 리스크 및 과제

- 자동차용 터치스크린 디스플레이의 도입 증가

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추계·예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV차

- 상용차

- 소형 상용차(LCV)

- 대형 상용차(HCV)

제6장 시장 추계·예측 : 판매 채널별(2021-2034년)

- 주요 동향

- OEM

- 애프터마켓

제7장 시장 추계·예측 : 제품별(2021-2034년)

- 주요 동향

- 푸시

- See-saw

제8장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 인포테인먼트 컨트롤

- 오디오 컨트롤

- 크루즈 컨트롤

- 전화 컨트롤

- 기타

제9장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- UAE

- 남아프리카

- 사우디아라비아

제10장 기업 프로파일

- ALPS

- Changjiang Automobile Electronic System

- COBO

- Continental

- Delphi

- Denso

- Dongguan

- Hyundai Motor

- Johnson Electric Holdings

- Kia Corporation

- Leopold Kostal

- LS Automotive Technologies

- Marquardt Group

- Nissan Motor

- Panasonic Corporation

- Preh

- TOKAI RIKA

- Toyota Motor

- Valeo

- ZF Friedrichshafen

The Global Steering Wheel Switches Market was valued at USD 3.4 billion in 2024 and is projected to grow at a CAGR of 1.8% between 2025 and 2034. Road safety remains a major concern worldwide, particularly in developed regions where vehicle accidents result in significant casualties. High consumer awareness, combined with regulatory influences and advanced purchasing power, has led to a growing demand for modern safety technologies. Automakers are increasingly integrating advanced driver-assist features into vehicles, enhancing both safety and market expansion. The rising emphasis on driver protection is fueling the adoption of steering wheel electronics, reducing distractions, and improving overall driving efficiency. Multi-functional steering wheel controls are gaining popularity as they enhance user convenience while aligning with industry trends, particularly the rapid acceptance of electric vehicles. The shift towards seamless in-car control systems further strengthens the market outlook.

Passenger vehicles held a market share of over 60% in 2024 and are expected to surpass USD 2.5 billion by 2034. Sedans, hatchbacks, and SUVs contribute significantly to the demand for steering wheel switches, as these vehicles continue to dominate global sales. With built-in controls allowing drivers to manage infotainment, cruise control, and communication systems without distractions, manufacturers are focusing on integrating more intuitive and user-friendly interfaces. The increasing demand for daily-use vehicles, especially in urban areas, is further driving the need for steering wheel-mounted switches. As automakers prioritize driver convenience and efficiency, all-in-one control solutions are becoming a key component in modern passenger cars.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.4 billion |

| Forecast Value | $4 billion |

| CAGR | 1.8% |

The market is divided into OEM and aftermarket sales channels, with the OEM segment holding a 64% share in 2024. Steering wheel switches are predominantly supplied by original equipment manufacturers, which ensures seamless integration into vehicles during production. As these switches become standard across most modern cars, automakers are expanding production cycles to meet rising demand. Automotive assembly lines rely on suppliers for efficient sourcing, with manufacturers investing in automation to streamline production. The increasing need for new vehicles, especially in high-growth markets, is boosting demand for OEM steering wheel switches.

The product segment includes push and see-saw switches, with the push button segment generating USD 1.9 billion in 2024. Push buttons are widely used for infotainment, audio, cruise control, and communication functions, providing an intuitive user experience. Their durability and cost-effectiveness make them a preferred choice for automakers, supporting multi-functional applications while maintaining affordability. The shift towards simplified in-car control systems, combined with the integration of advanced electronics, continues to drive segment growth.

Infotainment controls are expected to grow at a CAGR of over 2.5% from 2025 to 2034. The rising adoption of connected vehicle technologies has increased the demand for steering wheel-integrated infotainment features, ensuring safer and more convenient interactions. Hands-free access to navigation, voice commands, and other functions enhances both driver safety and user experience, making infotainment controls a crucial component in modern vehicles.

The Asia Pacific region led the global market in 2024, accounting for over 33% of the total share. With strong automotive production and increasing demand for steering wheel controls, the region continues to drive market expansion.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material suppliers

- 3.1.1.2 Component suppliers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Technology providers

- 3.1.1.5 Distributors

- 3.1.1.6 End users

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Technology & innovation landscape

- 3.3 Patent analysis

- 3.4 Regulatory landscape

- 3.5 Price trend

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Growing sales of vehicles across the globe

- 3.6.1.2 Increased awareness about road safety

- 3.6.1.3 Emergence of automotive parts & components industry

- 3.6.1.4 Steadily developing automotive manufacturing sector

- 3.6.1.5 Advancements in automotive electronics & adaptive cruise control technology

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Increasing implementation of automotive touchscreen displays

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Passenger vehicles

- 5.2.1 Hatchback

- 5.2.2 Sedan

- 5.2.3 SUVs

- 5.3 Commercial vehicles

- 5.3.1 Light commercial vehicles (LCVs)

- 5.3.2 Heavy commercial vehicles (HCVs)

Chapter 6 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 OEM

- 6.3 Aftermarket

Chapter 7 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Push

- 7.3 See-saw

Chapter 8 Market Estimates & Forecast, By application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Infotainment control

- 8.3 Audio controls

- 8.4 Cruise control

- 8.5 Phone control

- 8.6 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 ALPS

- 10.2 Changjiang Automobile Electronic System

- 10.3 COBO

- 10.4 Continental

- 10.5 Delphi

- 10.6 Denso

- 10.7 Dongguan

- 10.8 Hyundai Motor

- 10.9 Johnson Electric Holdings

- 10.10 Kia Corporation

- 10.11 Leopold Kostal

- 10.12 LS Automotive Technologies

- 10.13 Marquardt Group

- 10.14 Nissan Motor

- 10.15 Panasonic Corporation

- 10.16 Preh

- 10.17 TOKAI RIKA

- 10.18 Toyota Motor

- 10.19 Valeo

- 10.20 ZF Friedrichshafen