|

시장보고서

상품코드

1685141

단열 코팅 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Insulation Coatings Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

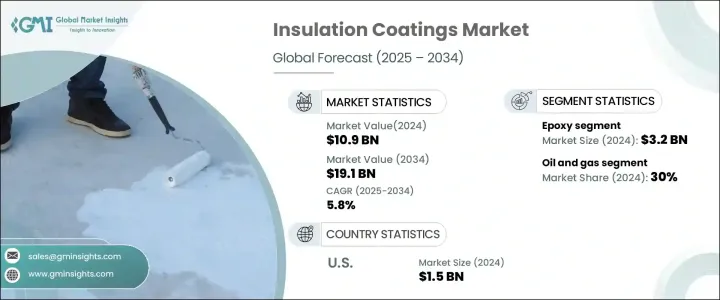

세계의 단열 코팅 시장은 2024년에 109억 달러에 이르렀으며, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 5.8%를 나타낼 것으로 예측됩니다.

에너지 효율적인 솔루션에 대한 수요 증가는 이 성장의 주요 원동력이 되고 있습니다. 세계 도시화가 진행됨에 따라 고급 건설 및 인프라 프로젝트의 요구가 급속히 증가하고 있습니다. 이는 단열 코팅 시장의 확대를 뒷받침하고 있습니다. 제조 공장, 발전소, 석유 정련소 등의 산업 부문에서는 에너지 효율 향상, 장비 보호, 운영 비용 절감 등을 목적으로 단열 코팅 채택이 증가하고 있습니다. 이러한 코팅은 에너지 소비와 지속가능성에 대한 환경 문제를 해결하면서 최상의 성능을 유지하는 데 매우 중요합니다. 산업계가 이산화탄소 배출 감소에 강한 압력에 직면하고 있는 동안, 단열 코팅은 운영과 환경의 목표를 달성하는 중요한 요소로 간주됩니다.

에너지 효율에 대한 관심 증가와 더불어, 환경에 미치는 영향에 대한 의식 증가와 지속가능성을 중시하는 규제의 강화도 세계 시장의 성장에 박차를 가하고 있습니다. 제조업체와 업계 관계자는 에너지 소비와 이에 따른 운영 비용을 줄이면서 장비 수명을 연장할 수 있는 단열 코팅의 비용 절감 가능성을 더욱 강력하게 인식하고 있습니다. 스마트 빌딩 솔루션, 에너지 효율적인 시스템, 녹색 건설 동향은 각 분야의 단열 코팅 채택을 더욱 강화하고 있습니다. 또한 기업이 에너지 가격 변동과 환경 규제 강화에 직면하고 있는 가운데, 단열 코팅은 에너지 절약과 환경 보호에 크게 기여하는 것으로 인정되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 109억 달러 |

| 예측 금액 | 191억 달러 |

| CAGR | 5.8% |

시장은 에폭시, 폴리우레탄, 아크릴, 이트리아 안정화 지르코니아, 기타 등 제품 유형별로 구분됩니다. 에폭시 기반의 단열 코팅 부문은 2024년 32억 달러로 평가되었습니다. 뛰어난 접착성, 내구성, 극단적인 온도에 대한 내성으로 알려진 에폭시 페인트는 다양한 산업 분야에서 높은 평가를 받고 있습니다. 부식, 습기, 환경 스트레스에 대한 견고한 보호를 제공할 수 있기 때문에 자동차, 선박, 건설 등의 분야에서 선호되고 있습니다. 에너지 효율을 높이고 기계 및 장비의 수명을 연장하는 실적이 있는 에폭시 수지 코팅은 유지 보수 비용을 줄이고 운영 성능을 향상시키는 데 필수적입니다.

최종 사용자 산업의 경우 단열 코팅 시장은 석유, 가스, 항공우주, 선박, 건축 및 건설, 자동차 등으로 나뉩니다. 석유 및 가스 분야는 30% 시장 점유율을 차지하고 있으며, 단열 코팅은 온도 제어, 내식성, 파이프라인 및 장비 보호에 중요한 역할을 합니다. 이 코팅은 열 손실을 최소화하고 에너지 효율을 높이고 가혹한 환경 조건으로부터 자산을 보호하는 데 도움이 됩니다. 안전성, 지속가능성, 업무 효율성에 대한 주목이 높아지는 가운데 고성능 단열 코팅에 대한 수요는 업계 전반에 걸쳐 꾸준히 증가하고 있습니다.

미국의 단열 코팅 시장은 2024년 15억 달러에 이르렀으며 앞으로 수년간 큰 성장이 예상됩니다. 이 급성장의 배경에는 건설, 제조, 석유 및 가스 등 다양한 산업에서 에너지 효율적인 솔루션에 대한 수요가 높아지고 있는 일이 있습니다. 보다 엄격한 에너지 효율 규제의 채택과 지속가능성에 대한 노력이 결합되어 첨단 단열 코팅의 보급으로 이어지고 있습니다.

목차

제1장 조사 방법과 조사 범위

- 시장 범위와 정의

- 기본 추정과 계산

- 예측 계산

- 데이터 소스

- 1차 데이터

- 2차 자료

- 유료 소스

- 공적 소스

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 파괴적 혁신

- 향후 전망

- 제조업체

- 유통업체

- 공급업체 상황

- 이익률 분석

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 에너지 효율이 높은 솔루션에 대한 수요 증가

- 산업 및 인프라 부문의 성장

- 환경 지속성에 대한 관심 증가

- 업계의 잠재적 위험 및 과제

- 단열 코팅의 높은 초기 비용

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 규모와 예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 아크릴

- 에폭시

- 폴리우레탄

- 이트리아 안정화 지르코니아

- 기타

제6장 시장 규모와 예측 : 최종 용도 산업별(2021-2034년)

- 주요 동향

- 석유 및 가스

- 항공우주

- 자동차

- 선박

- 건축 및 건설

- 기타

제7장 시장 규모와 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제8장 기업 프로파일

- 3M

- AkzoNobel

- BASF SE

- Hempel A/S

- PPG Industries

- Sherwin-Williams

- The Dow Chemical Company

The Global Insulation Coatings Market reached USD 10.9 billion in 2024 and is projected to grow at a CAGR of 5.8% from 2025 to 2034. The increasing demand for energy-efficient solutions is a primary driver of this growth. As the world continues to urbanize, the need for advanced construction and infrastructure projects is rising rapidly. This is driving the expansion of the insulation coatings market. Industrial sectors such as manufacturing plants, power stations, and oil refineries are increasingly adopting insulation coatings to enhance energy efficiency, protect equipment, and reduce operational costs. These coatings are crucial for maintaining peak performance while addressing environmental concerns related to energy consumption and sustainability. As industries continue to face mounting pressure to reduce their carbon footprints, insulation coatings are being seen as a key element in achieving both operational and environmental goals.

In addition to the growing focus on energy efficiency, global market growth is also spurred by rising awareness of environmental impacts and the increasing regulatory emphasis on sustainability. Manufacturers and industrial players are now more aware of the cost-saving potential of insulation coatings, which help extend the lifespan of equipment while reducing energy consumption and associated operational costs. The trend toward smart building solutions, energy-efficient systems, and green construction further supports the adoption of these coatings across sectors. Moreover, as businesses continue to face fluctuating energy prices and stricter environmental regulations, insulation coatings are being recognized for their significant contribution to energy conservation and environmental protection.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.9 Billion |

| Forecast Value | $19.1 Billion |

| CAGR | 5.8% |

The market is segmented by product types, including epoxy, polyurethane, acrylic, yttria-stabilized zirconia, and others. The epoxy-based insulation coatings segment was valued at USD 3.2 billion in 2024. Known for their excellent adhesion, durability, and resistance to extreme temperatures, epoxy coatings are highly regarded in a variety of industrial applications. Their ability to provide robust protection against corrosion, moisture, and environmental stress makes them a preferred choice in sectors like automotive, marine, and construction. With a proven track record in enhancing energy efficiency and extending the lifespan of machinery and equipment, epoxy coatings are integral to reducing maintenance costs and improving operational performance.

When it comes to end-user industries, the insulation coatings market is divided into oil and gas, aerospace, marine, building and construction, automotive, and others. The oil and gas sector holds a 30% market share, with insulation coatings playing a vital role in offering temperature control, corrosion resistance, and safeguarding pipelines and equipment. These coatings help minimize heat loss, increase energy efficiency, and protect assets from harsh environmental conditions. With an increasing focus on safety, sustainability, and operational efficiency, demand for high-performance insulation coatings is rising steadily across this industry.

In the U.S., the insulation coatings market reached USD 1.5 billion in 2024, with significant growth anticipated in the coming years. This surge is driven by the growing demand for energy-efficient solutions across various industries, such as construction, manufacturing, and oil and gas. The adoption of stricter energy efficiency regulations, combined with sustainability initiatives, has led to the widespread use of advanced insulation coatings.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Rising demand for energy-efficient solutions

- 3.6.1.2 Growth in industrial and infrastructure sectors

- 3.6.1.3 Increasing focus on environmental sustainability

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High initial costs of insulation coatings

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Size and Forecast, By Product Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Acrylic

- 5.3 Epoxy

- 5.4 Polyurethane

- 5.5 Yttria stabilized zirconia

- 5.6 Others

Chapter 6 Market Size and Forecast, By End Use Industry, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Oil and gas

- 6.3 Aerospace

- 6.4 Automotive

- 6.5 Marine

- 6.6 Building and construction

- 6.7 Others

Chapter 7 Market Size and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 UK

- 7.3.2 Germany

- 7.3.3 France

- 7.3.4 Italy

- 7.3.5 Spain

- 7.3.6 Russia

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Latin America

- 7.5.1 Brazil

- 7.5.2 Mexico

- 7.6 MEA

- 7.6.1 South Africa

- 7.6.2 Saudi Arabia

- 7.6.3 UAE

Chapter 8 Company Profiles

- 8.1 3M

- 8.2 AkzoNobel

- 8.3 BASF SE

- 8.4 Hempel A/S

- 8.5 PPG Industries

- 8.6 Sherwin-Williams

- 8.7 The Dow Chemical Company