|

시장보고서

상품코드

1685157

자율주행 자동차 시장 : 기회, 성장 촉진요인, 산업 동향 분석(2025-2034년)Autonomous Cars Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

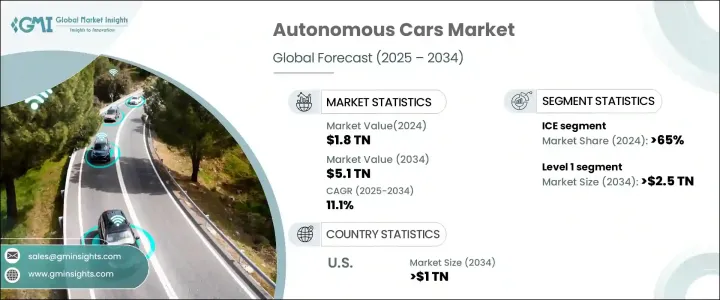

세계의 자율주행 자동차 시장은 2024년까지 1조8,000억 달러에 달했으며, 2034년까지 연평균 성장률(CAGR)은 11.1%를 나타낼 것으로 예측됩니다.

이러한 급증은 주로 차량의 자율성을 향상시키는 인공지능(AI)과 머신러닝의 획기적인 발전에 의해 주도되고 있습니다. 최근 LiDAR 및 카메라와 같은 센서 기술의 발전으로 차량이 주변 환경과 더욱 안정적으로 상호 작용할 수 있게 되면서 자율주행 자동차 도입에 대한 소비자의 신뢰가 높아졌습니다. 이러한 기술 발전은 차량의 기능을 혁신할 뿐만 아니라 실시간 의사결정을 개선하여 안전을 강화하고 경로 효율성을 최적화하고 있습니다. 커넥티드 및 자율주행 차량에 대한 수요가 증가함에 따라 이러한 기술은 증가하는 소비자의 관심과 기대를 충족하는 데 필수적인 요소가 되고 있습니다.

시장 확대에 기여하는 또 다른 요인은 교통 안전에 대한 강조가 증가하고 있다는 점입니다. 자율주행 자동차는 교통사고의 상당 부분을 차지하는 인적 오류를 줄이는 것을 목표로 합니다. 충돌 감지, 어댑티브 크루즈 컨트롤, 자동 제동과 같은 자동화된 안전 시스템의 구현은 안전을 강화하고 시장의 성장을 가속화합니다. 정부와 산업 기관은 우호적인 규제를 통해 이러한 시스템의 개발과 도입을 지원하며 시장 확대를 더욱 촉진하고 있습니다. 자율주행 기술이 계속 발전함에 따라 도로 안전과 효율성에 더욱 큰 영향을 미칠 것으로 예상됩니다..

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 1조 8,000억 달러 |

| 예측 금액 | 5조 1,000억 달러 |

| CAGR | 11.1% |

시장은 레벨 1, 레벨 2, 레벨 3, 레벨 4 등 자동화 수준에 따라 세분화됩니다. 2024년 기준, 레벨 1 자동화는 시장 점유율의 55% 이상을 차지하며 2034년까지 그 위치를 유지할 것으로 예상되며, 그 규모는 2조 5,000억 달러를 넘어설 것으로 전망됩니다. 이 레벨은 인프라를 크게 변경할 필요 없이 다양한 차량에 통합할 수 있는 범용성과 비용 효율성으로 인해 특히 매력적입니다. 차선 유지 보조 및 어댑티브 크루즈 컨트롤과 같은 기능은 운전자의 안전을 향상시킬 뿐만 아니라 자율주행 시스템을 완전히 받아들이기를 주저하는 소비자도 만족시킬 수 있습니다.

연료 유형도 시장에서 중요한 역할을 하고 있으며, 내연기관(ICE), 전기 및 하이브리드 엔진이 주요 부문을 구성하고 있습니다. 2024년에는 내연기관 차량이 시장의 65% 이상을 차지할 것으로 예상됩니다. 상대적으로 저렴한 비용과 함께 ICE 차량의 광범위한 사용은 시장에서 지속적인 지배력을 보장합니다. ICE 차량은 기존 연료 인프라와 호환이 가능하여 실용성이 뛰어나고 소비자들에게 매력적으로 다가갈 수 있습니다.

지역적으로 미국은 2024년 북미 시장에서 90% 이상의 점유율을 차지하며 시장을 주도하고 있으며, 2034년에는 1조 달러를 넘어설 것으로 예상됩니다. 미국은 강력한 기술 인프라와 AI, 머신러닝, 센서 기술에 대한 막대한 투자 덕분에 자율주행 자동차 기술의 허브 역할을 하고 있습니다. 또한 미국은 자율주행 차량의 테스트와 배포를 촉진하는 지원적인 규제 프레임워크의 혜택을 누리고 있습니다. 전기 및 자율주행 차량에 대한 강력한 수요와 지원 인프라의 빠른 발전은 향후 몇 년 동안 시장 성장을 더욱 촉진할 것으로 예상됩니다.

목차

제1장 조사 방법과 조사 범위

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 기본 추정과 계산

- 기준연도의 산출

- 시장추계의 주요 동향

- 예측 모델

- 1차 조사와 검증

- 1차 정보

- 데이터 마이닝 소스

- 시장 정의

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 부품 공급자

- 자율주행 자동차 제조업체

- 기술 공급자

- 유통업체

- 최종 사용자

- 이익률 분석

- 가격 동향

- 비용 내역

- 기술과 혁신의 전망

- 주요 뉴스와 대처

- 특허 분석

- 규제 상황

- 영향요인

- 성장 촉진요인

- 친환경 교통수단의 채택 증가

- 자율주행 자동차의 신흥기업의 성장

- 북미에서 자율주행 기술 채택 증가

- 자율주행 기술에 대한 정부 지원 규정

- 업계의 잠재적 위험 및 과제

- 기술 발전 증가

- 자율주행 자동차에 대한 높은 초기 투자

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추계 및 예측 : 자동화 수준별(2021-2034년)

- 주요 동향

- 레벨 1

- 레벨 2

- 레벨 3

- 레벨 4

제6장 시장 추계 및 예측 : 연료 유형별(2021-2034년)

- 주요 동향

- ICE

- 전기자동차

- 하이브리드

제7장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 개인

- 공유 모빌리티

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 스페인

- 이탈리아

- 러시아

- 북유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 뉴질랜드

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- UAE

- 남아프리카

- 사우디아라비아

제9장 기업 프로파일

- Aptiv

- Aurora Innovation

- Baidu Apollo

- BMW Group

- Ford Motors

- General Motors

- Honda Motor

- 현대자동

- Mercedes-Benz

- Mobileye

- NIO

- Nissan Motor

- Rivian Automotive

- Stellantis NV

- Tesla

- Toyota Motor

- Volkswagen Group

- Volvo Cars

- Waymo

- Zoox

The Global Autonomous Cars Market reached USD 1.8 trillion by 2024 and is anticipated to grow at a CAGR of 11.1% through 2034. This surge is primarily driven by breakthroughs in artificial intelligence (AI) and machine learning, which are enhancing vehicle autonomy. Recent advancements in sensor technologies, such as LiDAR and cameras, have enabled vehicles to interact with their surroundings more reliably, leading to increased consumer confidence in adopting autonomous vehicles. These technological improvements are not only transforming vehicle capabilities but also improving real-time decision-making, which bolsters safety and optimizes routing efficiency. As the demand for connected and autonomous vehicles rises, these technologies are becoming essential to meet the growing consumer interest and expectations.

Another factor contributing to market expansion is the growing emphasis on traffic safety. Autonomous vehicles aim to reduce human error, which is responsible for a significant number of road accidents. The implementation of automated safety systems such as collision detection, adaptive cruise control, and automatic braking enhances safety and accelerates the market's growth. Governments and industry bodies are supporting the development and deployment of these systems through favorable regulations, further fueling market expansion. As autonomous technologies continue to evolve, they are expected to make an even greater impact on road safety and efficiency.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Trillion |

| Forecast Value | $5.1 Trillion |

| CAGR | 11.1% |

The market is segmented by levels of automation, including Level 1, Level 2, Level 3, and Level 4. As of 2024, Level 1 automation commands over 55% of the market share, a position it is expected to maintain through 2034, with projections to exceed USD 2.5 trillion. This level is particularly attractive due to its versatility and cost-effectiveness, as it can be incorporated into a wide range of vehicles without requiring major infrastructure changes. Features such as lane-keeping assistance and adaptive cruise control not only improve driver safety but also cater to consumers who are hesitant to fully embrace autonomous systems.

Fuel type also plays a significant role in the market, with internal combustion engines (ICE), electric, and hybrid engines making up the major segments. In 2024, ICE vehicles accounted for more than 65% of the market. The widespread use of ICE vehicles, coupled with their relatively lower cost, ensures their continued dominance in the market. ICE vehicles are compatible with existing fuel infrastructure, which enhances their practicality and appeal to consumers.

Geographically, the United States leads the North American market, holding more than 90% of the regional share in 2024, with projections to surpass USD 1 trillion by 2034. The U.S. is a hub for autonomous car technology, thanks to its robust technological infrastructure and significant investments in AI, machine learning, and sensor technologies. Additionally, the U.S. benefits from a supportive regulatory framework that facilitates testing and deployment of autonomous vehicles. The strong demand for electric and self-driving vehicles, coupled with the rapid development of supporting infrastructure, is expected to further drive market growth in the coming years.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Component suppliers

- 3.2.2 Autonomous car manufacturers

- 3.2.3 Technology providers

- 3.2.4 Distributors

- 3.2.5 End users

- 3.3 Profit margin analysis

- 3.4 Price trend

- 3.5 Cost breakdown

- 3.6 Technology & innovation landscape

- 3.7 Key news & initiatives

- 3.8 Patent analysis

- 3.9 Regulatory landscape

- 3.10 Impact forces

- 3.10.1 Growth drivers

- 3.10.1.1 Rising adoption of eco-friendly transportation

- 3.10.1.2 Growing autonomous car startups

- 3.10.1.3 Increasing adoption of self-driving technologies in North America

- 3.10.1.4 Supportive government regulations for autonomous driving technology

- 3.10.2 Industry pitfalls & challenges

- 3.10.2.1 Increasing technological advancements

- 3.10.2.2 High initial investments in autonomous cars

- 3.10.1 Growth drivers

- 3.11 Growth potential analysis

- 3.12 Porter’s analysis

- 3.13 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Autonomy, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Level 1

- 5.3 Level 2

- 5.4 Level 3

- 5.5 Level 4

Chapter 6 Market Estimates & Forecast, By Fuel, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 ICE

- 6.3 Electric

- 6.4 Hybrid

Chapter 7 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Personal

- 7.3 Shared mobility

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Russia

- 8.3.7 Nordics

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 ANZ

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 South Africa

- 8.6.3 Saudi Arabia

Chapter 9 Company Profiles

- 9.1 Aptiv

- 9.2 Aurora Innovation

- 9.3 Baidu Apollo

- 9.4 BMW Group

- 9.5 Ford Motor

- 9.6 General Motors

- 9.7 Honda Motor

- 9.8 Hyundai Motor

- 9.9 Mercedes-Benz

- 9.10 Mobileye

- 9.11 NIO

- 9.12 Nissan Motor

- 9.13 Rivian Automotive

- 9.14 Stellantis N.V.

- 9.15 Tesla

- 9.16 Toyota Motor

- 9.17 Volkswagen Group

- 9.18 Volvo Cars

- 9.19 Waymo

- 9.20 Zoox