|

시장보고서

상품코드

1685213

전기 절연 재료 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Electrical Insulation Materials Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

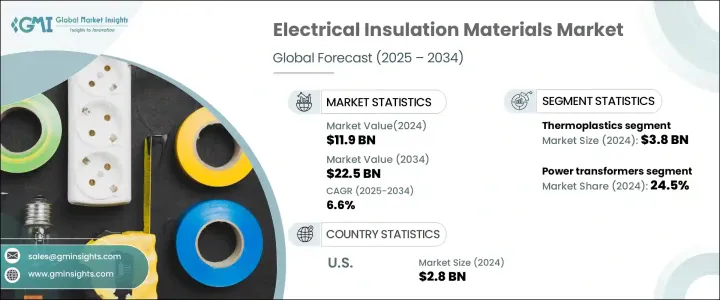

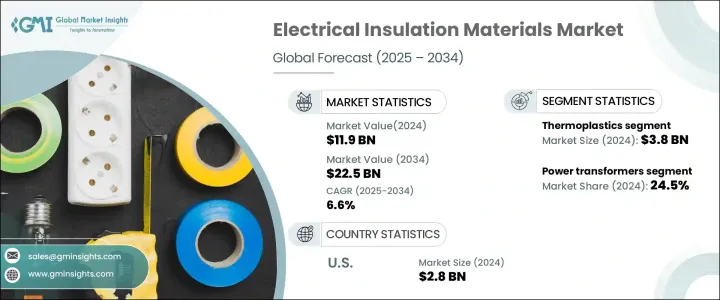

세계의 전기 절연 재료 시장은 2024년에 119억 달러로 평가되었고, 2025-2034년 CAGR 6.6%로 확대할 전망입니다.

이러한 성장의 원동력이 되고 있는 것은 다양한 산업에서 효율적이고 신뢰성이 높으며, 안전한 전기 시스템에 대한 수요가 증가하고 있다는 것입니다. 전기 절연 재료는 전기 부품 보호, 수명 확보, 상용 및 산업 용도에서 시스템 성능을 향상시키는 데 중요한 역할을 합니다.

산업이 발전함에 따라 보다 엄격한 규제 및 성능 기준을 충족하기 위해 혁신적이고 내구성이 뛰어나 지속 가능한 절연 솔루션에 대한 요구가 커지고 있습니다. 에너지 효율성 및 지속가능성의 중요성이 고조됨에 따라 재료 기술의 발전이 수요를 더욱 촉진하고 있습니다. 인프라, 특히 신재생 에너지와 현대화된 전력망의 지속적인 확대도 시장의 밝은 전망에 기여하고 있습니다. 친환경 솔루션으로의 전환이 진행됨에 따라 제조업체는 성능을 향상시킬 뿐만 아니라 친환경 제품을 제공하는 데 주력하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 119억 달러 |

| 예측 금액 | 225억 달러 |

| CAGR | 6.6% |

재료 유형별로 보면 열경화성 수지, 유리 섬유, 운모, 세라믹, 열가소성 수지, 셀룰로오스, 면 등이 있습니다. 2024년에는 열가소성 플라스틱 부문이 38억 달러를 창출했습니다. 열경화성 수지는 탁월한 내구성과 고온 내성으로 알려져 있으며, 까다로운 용도 분야에서 인기있는 선택입니다. 세라믹은 고전압 작동에 이상적인 우수한 유전 특성으로 높이 평가되며 유리 섬유는 강도 및 우수한 절연 능력을 제공합니다. 운모는 내열성과 전기 보호를 모두 제공하며 고전압 환경에서 선호되는 재료로 남아 있습니다. 또한, 셀룰로오스와 면은 내화성을 제공하는 친환경 소재로 부상하고 있으며, 전기 분야에서 지속가능하고 안전한 솔루션 증가 경향에 부합하고 있습니다.

전기 절연 재료의 용도는 광범위하며 전력 변압기, 배전 변압기, 전기 모터 및 발전기, 전선 및 케이블, 개폐 장치, 배터리, 회로 차단기 등의 산업에 서비스를 제공합니다. 전력 변압기는 2024년 시장 점유율의 24.5%를 차지했으며, 2034년까지 강력한 성장이 예상됩니다. 절연 재료는 배전 변압기 및 전기 모터의 성능과 효율을 최적화하는 데 매우 중요하며 발전, 송전, 산업 자동화와 같은 중요한 분야 전체에 대한 수요를 더욱 밀어 올리고 있습니다.

미국에서는 전기 절연 재료 시장이 2024년 28억 달러에 이르렀으며, 인프라에 많은 투자를 함으로써 상당한 성장이 예상됩니다. 과거의 송전망을 근대화하고 신재생 에너지에 대한 대처를 확대하는 것은 첨단 절연 재료의 채용을 촉진하고 있습니다. 지속가능성과 에너지 효율성이 뛰어난 솔루션에 중점을 둔 미국은 이 지역 시장의 기업으로서 예측 기간을 통해 지속적인 성장을 보장할 계획입니다.

목차

제1장 조사 방법 및 조사 범위

- 시장 범위 및 정의

- 기본 추정 및 계산

- 예측 계산

- 데이터 소스

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 파괴

- 장래 전망

- 제조업체

- 유통업체

- 공급자의 상황

- 이익률 분석

- 주요 뉴스

- 규제 상황

- 영향요인

- 성장 촉진요인

- 자동차 산업 수요 증가

- 항공우주 용도에서 채용 증가

- 화학가공 산업의 성장

- 업계의 잠재적 위험 및 과제

- 전기 절연 재료의 고비용

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 규모 및 예측 : 재료별(2021-2034년)

- 주요 동향

- 플루오로카본 엘라스토머(FKM)

- 전기 절연 재료(FFKM)

제6장 시장 규모 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 씰 및 개스킷

- O링

- 호스 및 튜브

- 기타

제7장 시장 규모 및 예측 : 최종 용도 산업별(2021-2034년)

- 주요 동향

- 자동차

- 항공우주

- 석유 및 가스

- 화학처리

제8장 시장 규모 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- 3M

- AGC(Asahi Glass)

- Chemours

- Daikin Industries

- DowDuPont

- DuPont(EI du Pont de Nemours and Company)

- Gujarat Fluorochemicals

- HaloPolymer

- Mitsui Chemicals

- Momentive Performance Materials

- Saint-Gobain Performance Plastics

- Shin-Etsu Chemical

- Solvay

- Wacker Chemie

- Zeon Corporation

The Global Electrical Insulation Materials Market reached USD 11.9 billion in 2024 and is set to expand at a CAGR of 6.6% from 2025 to 2034. This growth is driven by the increasing demand for efficient, reliable, and safe electrical systems across various industries. Electrical insulation materials play a critical role in protecting electrical components, ensuring longevity, and enhancing system performance in both commercial and industrial applications.

As industries evolve, there is a rising need for innovative, durable, and sustainable insulation solutions to meet stricter regulations and performance standards. Advancements in material technology, along with a growing emphasis on energy efficiency and sustainability, are further fueling demand. The continued expansion of infrastructure, particularly in renewable energy and modernized electrical grids, is also contributing to the positive market outlook. With the ongoing shift toward eco-friendly solutions, manufacturers are focusing on providing products that not only improve performance but are also environmentally responsible.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $11.9 Billion |

| Forecast Value | $22.5 Billion |

| CAGR | 6.6% |

Based on material type, the market segments include thermosets, fiberglass, mica, ceramics, thermoplastics, cellulose, cotton, and others. In 2024, the thermoplastics segment generated USD 3.8 billion. Thermosets are known for their exceptional durability and high-temperature resistance, making them a popular choice in demanding applications. Ceramics are highly valued for their superior dielectric properties, ideal for high-voltage operations, while fiberglass provides strength and excellent insulation capabilities. Mica remains a preferred material in high-voltage environments, providing both heat resistance and electrical protection. Additionally, cellulose and cotton are emerging as eco-friendly materials that offer fire resistance, aligning with the growing trend of sustainable and safe solutions in the electrical sector.

The applications of electrical insulation materials are wide-ranging, serving industries like power transformers, distribution transformers, electrical motors and generators, wires and cables, switchgear, batteries, and circuit breakers. Power transformers accounted for 24.5% of the market share in 2024, with strong growth expected through 2034. Insulation materials are crucial for optimizing the performance and efficiency of distribution transformers and electrical motors, further boosting demand across critical sectors such as power generation, transmission, and industrial automation.

In the U.S., the electrical insulation materials market reached USD 2.8 billion in 2024 and is expected to grow significantly due to substantial investments in infrastructure. Modernizing outdated electrical grids and expanding renewable energy initiatives are driving the adoption of advanced insulation materials. With a focus on sustainability and energy-efficient solutions, the U.S. is poised to remain a major player in the regional market, ensuring continued growth throughout the forecast period.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing demand in automotive industry

- 3.6.1.2 Rising adoption in aerospace applications

- 3.6.1.3 Growing chemical processing industries

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High cost of electrical insulation materials

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter’s analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Size and Forecast, By Material, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Fluorocarbon elastomers (FKM)

- 5.3 Perelectrical insulation materials (FFKM)

Chapter 6 Market Size and Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Seals and gaskets

- 6.3 O-rings

- 6.4 Hoses and tubings

- 6.5 Others

Chapter 7 Market Size and Forecast, By End Use Industries, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Automotive

- 7.3 Aerospace

- 7.4 Oil & gas

- 7.5 Chemical processing

Chapter 8 Market Size and Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 Australia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 3M

- 9.2 AGC (Asahi Glass)

- 9.3 Chemours

- 9.4 Daikin Industries

- 9.5 DowDuPont

- 9.6 DuPont (E. I. du Pont de Nemours and Company)

- 9.7 Gujarat Fluorochemicals

- 9.8 HaloPolymer

- 9.9 Mitsui Chemicals

- 9.10 Momentive Performance Materials

- 9.11 Saint-Gobain Performance Plastics

- 9.12 Shin-Etsu Chemical

- 9.13 Solvay

- 9.14 Wacker Chemie

- 9.15 Zeon Corporation