|

시장보고서

상품코드

1698236

배터리 열관리 시스템 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Battery Thermal Management System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025-2034 |

||||||

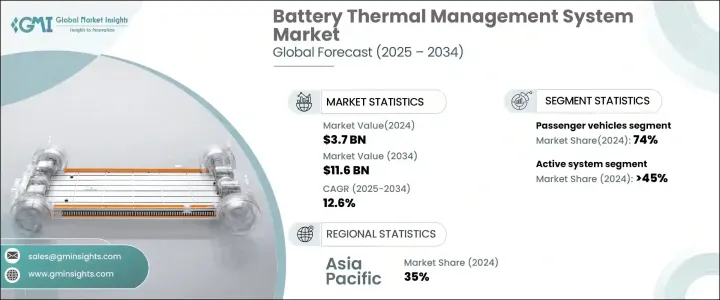

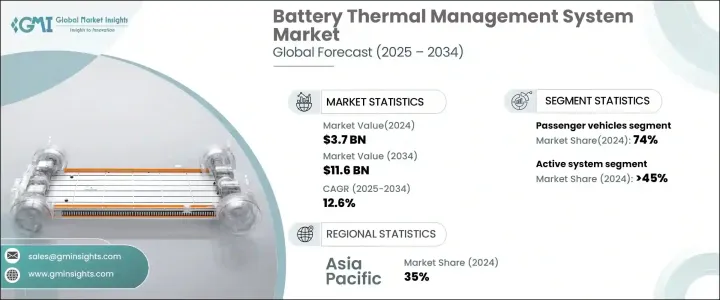

세계의 배터리 열관리 시스템 시장 규모는 37억 달러로 평가되었고, 전기자동차(EV) 생산 대수 증가 및 배터리 기술의 진보에 견인되어 2025-2034년 CAGR 12.6%로 확대될 것으로 예측되고 있습니다.

고성능 및 수명이 긴 배터리에 대한 수요가 계속 증가함에 따라 제조업체는 배터리의 효율, 안전성 및 수명을 보장하는 혁신적인 열관리 솔루션에 주력하고 있습니다.

EV로의 시프트가 기세를 늘리는 중, 배터리 열관리 시스템은 배터리 성능을 최적화하는데 있어 중요한 컴포넌트가 되고 있습니다. 이러한 시스템은 온도를 조정하고 과열을 방지하며 배터리 수명을 늘리고 에너지 효율, 충전 속도, 안전성과 같은 주요 우려 사항에 대처합니다. 배터리의 안전성에 관한 정부의 엄격한 규제 및 급속 충전 기술의 채택 증가가 시장의 성장을 더욱 촉진하고 있습니다. 게다가 EV 충전 인프라 확대 및 배터리 냉각 기술의 계속적인 연구 개발(R&D)은, 업계 기업에게 유리한 기회를 만들어 내고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 37억 달러 |

| 예측 금액 | 116억 달러 |

| CAGR | 12.6% |

시장은 액티브 시스템, 패시브 시스템, 하이브리드 시스템 등 열관리 시스템의 유형에 따라 구분됩니다. 2024년에는 주로 배터리 팩 내 온도를 효과적으로 조정하는 능력으로 인해 액티브 시스템 부문이 45%의 압도적인 시장 점유율을 차지했습니다. 액티브 시스템은 최적의 온도 조건을 유지하기 위해 액체 또는 공랭 기구를 사용하기 때문에 고성능 배터리에 적합합니다. 한편, 자연 냉각 방식에 의존하는 패시브 시스템은 배터리의 안전성 및 효율성을 높이는 데 있어 액티브 시스템을 보완하기 위해 2034년까지 CAGR 14%로 성장할 것으로 예측되고 있습니다. 또 액티브 냉각기구 및 패시브 냉각기구를 모두 통합한 하이브리드 시스템도 뛰어난 온도조절 기능을 갖춰 인기를 끌고 있습니다.

차종별로는 배터리 열관리 시스템 시장은 승용차와 상용차로 분류됩니다. 2024년에는 EV 보급과 효율적인 배터리 냉각 솔루션 요구가 커지면서 승용차가 74%라는 큰 시장 점유율을 차지했습니다. 항속 거리의 연장 및 충전 시간의 단축을 선호하게 되어, 승용차에는 고도의 열관리 시스템이 불가결하게 되고 있습니다. 그러나 상용차는 더 빠른 성장률이 전망되고 있으며, 2034년까지 CAGR 13%로 성장이 예측되고 있습니다. 전기 트럭, 버스, 배달용 밴의 수요 증가 및 지속 가능한 운송을 추진하는 정부의 노력이 이 분야에서 열관리 솔루션의 채택을 뒷받침하고 있습니다.

아시아태평양은 배터리 열관리 시스템 시장의 주요 기업로 대두하고 있으며, 2024년에는 35%의 점유율을 차지했습니다. 중국이 이 지역을 선도하며 열관리 솔루션의 생산과 소비를 모두 견인하고 있습니다. 중국, 대만, 인도에는 확립된 공급망과 대형 배터리 제조업체가 존재해 시장 확대를 뒷받침하고 있습니다. EV의 급속한 보급은 도시화 및 정부의 지원 정책과 맞물려 이 지역의 배터리 열관리 시스템 수요를 더욱 가속화시키고 있습니다. 업계 각사는, 경쟁 정세에 있어서의 시장 포지션을 강화하기 위해, 기술적 진보, 전략적 파트너십, 제조 확대에 주력하고 있습니다.

목차

제1장 조사 방법 및 조사 범위

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 기본 추정 및 계산

- 기준 연도의 산출

- 시장추계의 주요 동향

- 예측 모델

- 1차 조사 및 검증

- 1차 정보

- 데이터 마이닝 소스

- 시장 범위 및 정의

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 원재료 제공업체

- 부품 제조업체

- 제조업체

- 기술 제공업체

- 최종 고객

- 공급자의 상황

- 이익률 분석

- 기술 혁신의 상황

- 특허 분석

- 주요 뉴스 및 이니셔티브

- 규제 상황

- 이용 사례

- 영향요인

- 성장 촉진요인

- 전기자동차(EV) 수요 증가

- 배터리 기술 진보

- 급속 충전소 보급 확대

- EV 인프라 투자 증가

- 업계의 잠재적 위험 및 과제

- 높은 초기 비용

- 통합의 복잡성

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추계 및 예측 : 제공 제품별(2021-2034년)

- 주요 동향

- 액티브 시스템

- 패시브 시스템

- 하이브리드 시스템

제6장 시장 추계 및 예측 : 배터리별(2021-2034년)

- 주요 동향

- 리튬 이온 배터리

- 니켈 수소 전지

- 납축전지

- 고체 배터리

제7장 시장 추계 및 예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV

- 소형 상용차

- 상용차(LCV)

- 대형 상용차(HCV)

제8장 시장 추계 및 예측 : 추진별(2021-2034년)

- 주요 동향

- 배터리 전기자동차(BEV)

- 플러그인 하이브리드 자동차(PHEV)

- 하이브리드 자동차(HEV)

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- UAE

- 남아프리카

- 사우디아라비아

제10장 기업 프로파일

- Aptiv PLC

- BASF

- Bosch

- Continental

- Dana Limited

- Gentherm

- Hanon Systems

- Hitachi

- Infineon

- Johnson Control

- MAHLE GmbH

- Marelli

- Modine

- Modine Manufacturing

- Sanden Corporation

- Schaeffler

- Valeo

- Vitesco Technologies

- VOSS Automotive

- ZF Friedrichshafen

The Global Battery Thermal Management System Market was valued at USD 3.7 billion and is projected to expand at a CAGR of 12.6% between 2025 and 2034, driven by the rising production of electric vehicles (EVs) and advancements in battery technologies. As the demand for high-performance and long-lasting batteries continues to rise, manufacturers are focusing on innovative thermal management solutions that ensure battery efficiency, safety, and longevity.

With the shift towards EVs gaining momentum, battery thermal management systems have become a critical component in optimizing battery performance. These systems regulate temperature, prevent overheating, and enhance battery lifespan, addressing key concerns such as energy efficiency, charging speed, and safety. Stringent government regulations on battery safety and the increasing adoption of fast-charging technology are further fueling market growth. Additionally, the expansion of EV charging infrastructure and continuous research and development (R&D) in battery cooling technologies are creating lucrative opportunities for industry players.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.7 Billion |

| Forecast Value | $11.6 Billion |

| CAGR | 12.6% |

The market is segmented by the type of thermal management system, including active, passive, and hybrid systems. In 2024, the active system segment held a dominant 45% market share, primarily due to its ability to regulate temperature effectively within the battery pack. Active systems use liquid or air cooling mechanisms to maintain optimal thermal conditions, making them a preferred choice for high-performance batteries. Meanwhile, passive systems, which rely on natural cooling methods, are projected to grow at a CAGR of 14% through 2034 as they complement active systems in enhancing battery safety and efficiency. Hybrid systems, which integrate both active and passive cooling mechanisms, are also gaining traction due to their ability to provide superior temperature regulation.

By vehicle type, the battery thermal management system market is categorized into passenger vehicles and commercial vehicles. In 2024, passenger vehicles accounted for a substantial 74% market share, driven by the increasing adoption of EVs and the need for efficient battery cooling solutions. The growing preference for longer driving ranges and faster charging times has made advanced thermal management systems indispensable for passenger vehicles. However, commercial vehicles are expected to witness a faster growth rate, with a projected CAGR of 13% through 2034. The rising demand for electric trucks, buses, and delivery vans, along with government initiatives promoting sustainable transportation, is propelling the adoption of thermal management solutions in this segment.

Asia Pacific emerged as a key player in the battery thermal management system market, holding a 35% share in 2024. China leads the region, driving both production and consumption of thermal management solutions. The presence of well-established supply chains and major battery manufacturers in China, Taiwan, and India is boosting market expansion. The rapid increase in EV adoption, coupled with urbanization and supportive government policies, is further accelerating demand for battery thermal management systems in the region. Industry players are focusing on technological advancements, strategic partnerships, and manufacturing expansion to strengthen their market position in the competitive landscape.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Raw material providers

- 3.1.2 Component providers

- 3.1.3 Manufacturers

- 3.1.4 Technology providers

- 3.1.5 End customers

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Technology & innovation landscape

- 3.5 Patent analysis

- 3.6 Key news & initiatives

- 3.7 Regulatory landscape

- 3.8 Use cases

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rising demand for electric vehicles (EVs)

- 3.9.1.2 Advancements in battery technology

- 3.9.1.3 Increasing adoption of fast-charging stations

- 3.9.1.4 Growing investment in EV infrastructure

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High initial costs

- 3.9.2.2 Complexity in integration

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Offering, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Active system

- 5.3 Passive system

- 5.4 Hybrid system

Chapter 6 Market Estimates & Forecast, By Battery, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Lithium-ion battery

- 6.3 Nickel-Metal Hydride (NiMH) battery

- 6.4 Lead-acid battery

- 6.5 Solid-state battery

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Passenger vehicles

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial vehicles Light

- 7.3.1 Commercial Vehicles (LCV)

- 7.3.2 Heavy Commercial Vehicles (HCV)

Chapter 8 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Battery Electric Vehicles (BEVs)

- 8.3 Plug-in Hybrid Electric Vehicles (PHEVs)

- 8.4 Hybrid Electric Vehicles (HEVs)

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Aptiv PLC

- 10.2 BASF

- 10.3 Bosch

- 10.4 Continental

- 10.5 Dana Limited

- 10.6 Gentherm

- 10.7 Hanon Systems

- 10.8 Hitachi

- 10.9 Infineon

- 10.10 Johnson Control

- 10.11 MAHLE GmbH

- 10.12 Marelli

- 10.13 Modine

- 10.14 Modine Manufacturing

- 10.15 Sanden Corporation

- 10.16 Schaeffler

- 10.17 Valeo

- 10.18 Vitesco Technologies

- 10.19 VOSS Automotive

- 10.20 ZF Friedrichshafen