|

시장보고서

상품코드

1892877

자동차 점화 플러그 시장 기회, 성장요인, 업계 동향 분석 및 예측(2026-2035년)Automotive Spark Plug Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2026 - 2035 |

||||||

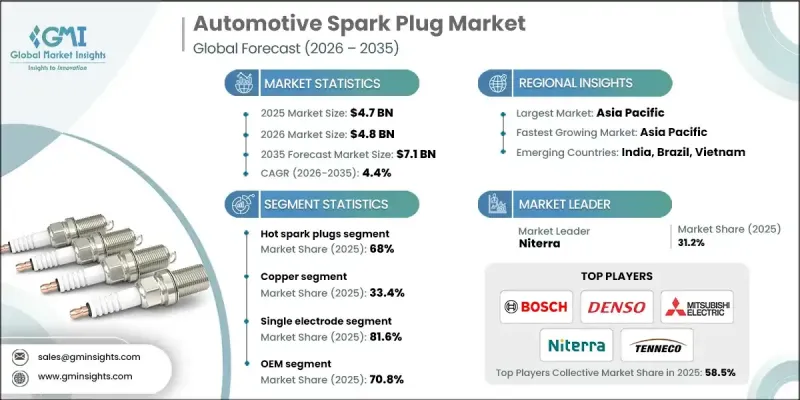

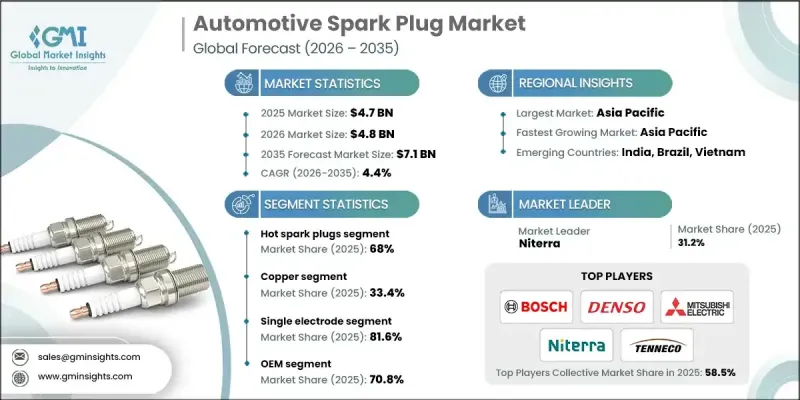

세계의 자동차 점화 플러그 시장은 2025년에 47억 달러로 평가되었고, 2035년까지 연평균 복합 성장률(CAGR) 4.4%로 성장하여 71억 달러에 이를 것으로 예측됩니다.

이러한 성장은 전 세계 신차 생산량의 꾸준한 증가와 가솔린 차량에 대한 소비자의 지속적인 선호에 의해 뒷받침되고 있습니다. 또한, 연비 효율을 향상시키기 위해 첨단 점화 플러그 기술의 채택 확대를 촉진하고 있으며, 효율을 극대화하도록 설계된 새로운 엔진 구조가 채택되고 있습니다. 제조업체들은 이리듐, 백금 등의 소재를 제품 라인 전체에 확대 적용하고 있으며, 이를 통해 보다 내구성이 높고 효율적인 점화 성능을 실현하고 있습니다. 현대의 연소 시스템은 연료 효율을 약 10% 향상시켰으며, 이는 고품질 점화 플러그 부품의 보급을 촉진하고 있습니다. 도심의 모빌리티 확대 추세에 따라 스파크 점화 시스템에 의존하는 소형 엔진에 대한 수요가 증가하고 있습니다. 애프터마켓도 계속해서 큰 기여를 하고 있으며, 특히 2024년 차량 평균 사용 연한이 12년을 넘어서면서 연간 교체 주기가 증가하고 있습니다. 고성능 금속의 지속적인 개선은 점화 플러그의 수명과 점화 신뢰성 향상에 지속적으로 기여하고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2025년 |

| 예측 연도 | 2026-2035년 |

| 개시 연도 시장 규모 | 47억 달러 |

| 예측 금액 | 71억 달러 |

| CAGR | 4.4% |

2025년 기준 고온 점화 플러그 부문은 68%의 점유율을 차지하고 있으며, 2026년부터 2035년까지 연평균 4.7%의 연평균 복합 성장률(CAGR)을 나타낼 전망입니다. 이 플러그는 넓은 온도 범위에서 안정적인 점화를 유지하기 때문에 기존 가솔린 엔진에 계속 선호되고 있습니다. 이 디자인은 효과적인 열 방출을 지원하며, 세계 주요 지역의 대도시 지역에서 흔히 발생하는 저속 주행 시 오염을 억제하는 데 도움이 됩니다.

단극 점화 플러그 부문은 2025년 81.6%의 점유율을 차지했습니다. 2024년 세계 승용차 생산량이 7,600만 대를 넘어설 것으로 예상되는 가운데, 대중용 승용차 및 이륜차의 주요 선택지로서의 지위를 유지하고 있습니다. 많은 보급형 및 중급 엔진은 여전히 단극 전극 시스템에 의존하고 있습니다. 이는 예측 가능한 동작과 낮은 유지보수 비용을 제공하기 위함입니다. 이는 노후화된 차량 기반이 큰 지역의 애프터마켓에서 특히 매력적인 선택이 될 수 있습니다.

중국 자동차 점화 플러그 시장은 2024년 46.8%의 점유율을 차지했으며, 2025년에는 8억 2,440만 달러 규모에 달할 것으로 예측됩니다. 성장세는 자동차 판매량 증가와 급속한 도시 확장과 연동되어 있으며, 승용차 생산량은 2,800만 대를 넘어 계속 증가하고 있습니다. 이로 인해 주요 도시와 지방 커뮤니티 모두에서 OEM 수요와 교체 주기가 가속화되고 있습니다. 이륜차 이동수단은 여전히 교통 구조의 큰 구성요소이며, 2024년에는 약 700만 대의 오토바이와 스쿠터가 생산될 것으로 예측됩니다. 대부분 구리 또는 백금 스파크 플러그에 의존하고 있으며, 앞으로도 지속적인 교체 수요가 꾸준히 증가할 것으로 예측됩니다.

자주 묻는 질문

목차

제1장 조사 방법

- 시장 범위와 정의

- 조사 설계

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역별/국가별

- 기본 추정치와 계산

- 기준연도 계산

- 시장 추정 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측 모델

- 조사의 전제조건과 제한 사항

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률 분석

- 비용 구조

- 각 단계별 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신 동향

- 현재 기술 동향

- 신기술

- 가격 동향

- OEM와 애프터마켓 가격차

- 지역별 가격변동

- 원재료 비용 영향

- 수출입 가격 분석

- 향후 가격 추이

- 생산 통계

- 생산 거점

- 소비 거점

- 수출입

- 비용 내역 분석

- 특허 및 지적재산 분석

- 전극 재료별 유효 특허

- 지역 목표 특허 분포

- 주요 특허 보유자

- 신기술 특허(스마트 플러그)

- 특허 만료 시기 타임라인(2024-2034)

- 지속가능성과 환경 측면

- 지속가능한 대처

- 폐기물 감축 전략

- 생산 에너지 효율

- 친환경 이니셔티브

- 탄소발자국에 관한 고려사항

- 투자 및 자금조달 분석

- 제조업체별 연구개발 투자 동향

- 대체연료 대응 투자

- 제조능력 확장

- 전략적 제휴 및 합병사업

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 인수합병(M&A)

- 제휴 및 협업

- 신제품 발매

- 사업 확대 계획과 자금조달

제5장 시장 추산 및 예측 : 제품별 2022 2035

- 주요 동향

- 고온 점화 플러그

- 콜드 점화 플러그

제6장 시장 추산 및 예측 : 재료별, 2022-2035

- 주요 동향

- 구리

- 플래티넘

- 이리듐

- 기타

제7장 시장 추산 및 예측 : 전극별, 2022-2035

- 주요 동향

- 단일 전극

- 트윈 전극

- 멀티 전극

- 표면 방전

제8장 시장 추산 및 예측 : 판매채널별, 2022-2035

- 주요 동향

- OEM

- 애프터마켓

제9장 시장 추산 및 예측 : 차량별, 2022-2035

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV

- 상용차

- 경자동차

- 중형 트럭

- 대형 차량

- 이륜차

- 오토바이

- 스쿠터

제10장 시장 추산 및 예측 : 지역별, 2022-2035

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 네덜란드

- 스웨덴

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 싱가포르

- 태국

- 인도네시아

- 베트남

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트(UAE)

- 튀르키예

제11장 기업 개요

- 세계 기업

- ACDelco

- Autolite

- Bosch

- DENSO

- MAHLE

- Mitsubishi Electric

- Niterra

- Tenneco

- Valeo

- 지역 제조업체

- BorgWarner

- Brisk Spark Plug Company

- E3 Spark Plugs

- Hella

- MAGNETI MARELLI PARTS &SERVICES

- MSD Performance

- Stitt Spark Plug Company

- Zhuzhou Torch Spark Plug

- 신규 기업/디스럽터

- Iskra Spark Plugs

- Nanjing Leidian

- Prenco Progress &Engineering Corporation

- Pulstar

- SMP Automotive

- Weichai Power

The Global Automotive Spark Plug Market was valued at USD 4.7 billion in 2025 and is estimated to grow at a CAGR of 4.4% to reach USD 7.1 billion by 2035.

Growth is supported by the steady rise in new vehicle production worldwide and continued consumer preference for gasoline-powered models. The shift toward better fuel economy is also driving higher adoption of advanced spark plug technologies, as newer engine architectures are built to maximize efficiency. Manufacturers are expanding the use of materials such as iridium and platinum throughout their portfolios, contributing to more durable and efficient ignition performance. Modern combustion systems now deliver around a 10 percent boost in fuel efficiency, which encourages broader use of premium spark plug components. Expanding urban mobility trends are creating more demand for compact engines that rely on spark-ignited systems. The aftermarket remains a strong contributor as well, particularly as the average age of vehicles surpassed 12 years in 2024, increasing annual replacement cycles. Ongoing improvements in high-performance metals also continue to enhance spark plug lifespan and ignition reliability.

Market Scope Start Year 2025 Forecast Year 2026-2035 Start Value $4.7 Billion Forecast Value $7.1 Billion CAGR 4.4% The hot spark plugs segment held a 68% share in 2025, and this category is expected to expand at a CAGR of 4.7% between 2026 and 2035. These plugs remain favored for conventional gasoline engines because they maintain dependable ignition across a wide temperature range. Their design supports effective heat dissipation, helping limit fouling during low-speed driving that is common in metropolitan settings across major global regions.

The single electrode spark plugs segment held 81.6% share in 2025. They remain the primary option for mass-market passenger cars and two-wheel vehicles, supported by more than 76 million units of global passenger car production in 2024. Most entry-level and mid-tier engines still depend on single electrode systems, which offer predictable operation and low maintenance costs. This makes them especially appealing for the aftermarket in regions with a large base of aging vehicles.

China Automotive Spark Plug Market held 46.8% share in 2024 and generated USD 824.4 million in 2025. Growth is tied to rising vehicle sales and rapid urban expansion, which continue to boost passenger car production beyond 28 million units. This accelerates OEM demand and replacement cycles in both major cities and smaller communities. Two-wheel mobility remains a large component of the transportation landscape, with around 7 million motorcycles and scooters produced in 2024, most of which relied on copper or platinum spark plugs, ensuring strong ongoing replacement needs.

Key companies participating in the Automotive Spark Plug Market include ACDelco, Autolite, Bosch, DENSO Corporation, Hyundai Mobis, MAHLE, Mitsubishi Electric, Niterra, Tenneco, and Valeo. Leading Automotive Spark Plug Market is strengthening its presence by expanding advanced material technologies, particularly through wider integration of iridium and platinum to improve durability and ignition precision. Many manufacturers are increasing R&D investments to support next-generation combustion systems and adapt to evolving engine designs. Companies are also focusing on broadening their global manufacturing footprints to reduce costs and improve supply reliability. Strategic collaborations with automakers remain essential for securing long-term OEM contracts, while an enhanced emphasis on aftermarket networks helps capture demand from aging vehicle fleets. In addition, several brands are modernizing their product portfolios with heat-range-optimized designs and cost-efficient options to reach both premium and mass-market customer segments.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis, 2022 - 2035

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Material

- 2.2.4 Electrode

- 2.2.5 Sales Channel

- 2.2.6 Vehicle

- 2.3 TAM Analysis, 2026-2035

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1.1 Growth drivers

- 3.2.1.2 Growth in gasoline powered vehicles

- 3.2.1.3 Shift toward high efficiency engines

- 3.2.1.4 Increasing aftermarket activity

- 3.2.1.5 Adoption of precious metal plugs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Increasing penetration of electric vehicles

- 3.2.2.2 Rising raw material costs

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion of the global aftermarket

- 3.2.3.2 Development of advanced ignition systems

- 3.2.3.3 Growth in two-wheeler demand in emerging markets

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.1.1 Electrode material evolution (copper to ruthenium)

- 3.7.1.2 Fine wire technology development

- 3.7.1.3 Multi-electrode design innovations

- 3.7.1.4 Pre-chamber spark plug technology

- 3.7.1.5 IoT & smart diagnostics integration

- 3.7.1.6 Laser welding manufacturing advances

- 3.7.1.7 Heat range optimization technologies

- 3.7.1.8 Next-generation materials

- 3.7.2 Emerging technologies

- 3.7.1 Current technological trends

- 3.8 Price trends

- 3.8.1 OEM vs aftermarket price differential

- 3.8.2 Regional price variations

- 3.8.3 Raw material cost impact

- 3.8.4 Import/export price analysis

- 3.8.5 Future price trajectory

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent & intellectual property analysis

- 3.11.1 Active patents by electrode material

- 3.11.2 Geographic patent distribution

- 3.11.3 Key patent holders

- 3.11.4 Emerging technology patents (smart plugs)

- 3.11.5 Patent expiration timeline (2024-2034)

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

- 3.13 Investment & Funding Analysis

- 3.13.1 R&D investment trends by manufacturer

- 3.13.2 Alternative fuel adaptation investments

- 3.13.3 Manufacturing capacity expansion

- 3.13.4 Strategic partnerships & joint ventures

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2022 2035 (USD Mn, Units)

- 5.1 Key trends

- 5.2 Hot spark plug

- 5.3 Cold spark plug

Chapter 6 Market Estimates & Forecast, By Material, 2022 - 2035 (USD Mn, Units)

- 6.1 Key trends

- 6.2 Copper

- 6.3 Platinum

- 6.4 Iridium

- 6.5 Others

Chapter 7 Market Estimates & Forecast, By Electrode, 2022 - 2035 (USD Mn, Units)

- 7.1 Key trends

- 7.2 Single Electrode

- 7.3 Twin Electrode

- 7.4 Multi-Electrode

- 7.5 Surface Discharge

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2022 - 2035 (USD Mn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Vehicle, 2022 - 2035 (USD Mn, Units)

- 9.1 Key trends

- 9.2 Passenger car

- 9.2.1 Hatchback

- 9.2.2 Sedan

- 9.2.3 SUV

- 9.3 Commercial vehicle

- 9.3.1 Light duty

- 9.3.2 Medium duty

- 9.3.3 Heavy duty

- 9.4 Two-wheeler

- 9.4.1 Motorcycle

- 9.4.2 Scooter

Chapter 10 Market Estimates & Forecast, By Region, 2022 - 2035 (USD Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 US

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.3.8 Netherlands

- 10.3.9 Sweden

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Singapore

- 10.4.7 Thailand

- 10.4.8 Indonesia

- 10.4.9 Vietnam

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

- 10.6.4 Turkey

Chapter 11 Company Profiles

- 11.1 Global Players

- 11.1.1 ACDelco

- 11.1.2 Autolite

- 11.1.3 Bosch

- 11.1.4 DENSO

- 11.1.5 MAHLE

- 11.1.6 Mitsubishi Electric

- 11.1.7 Niterra

- 11.1.8 Tenneco

- 11.1.9 Valeo

- 11.2 Regional Players

- 11.2.1 BorgWarner

- 11.2.2 Brisk Spark Plug Company

- 11.2.3 E3 Spark Plugs

- 11.2.4 Hella

- 11.2.5 MAGNETI MARELLI PARTS & SERVICES

- 11.2.6 MSD Performance

- 11.2.7 Stitt Spark Plug Company

- 11.2.8 Zhuzhou Torch Spark Plug

- 11.3 Emerging Players / Disruptors

- 11.3.1 Iskra Spark Plugs

- 11.3.2 Nanjing Leidian

- 11.3.3 Prenco Progress & Engineering Corporation

- 11.3.4 Pulstar

- 11.3.5 SMP Automotive

- 11.3.6 Weichai Power