|

시장보고서

상품코드

1708139

대형 자율주행차(HDAV) 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Heavy-Duty Autonomous Vehicle Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

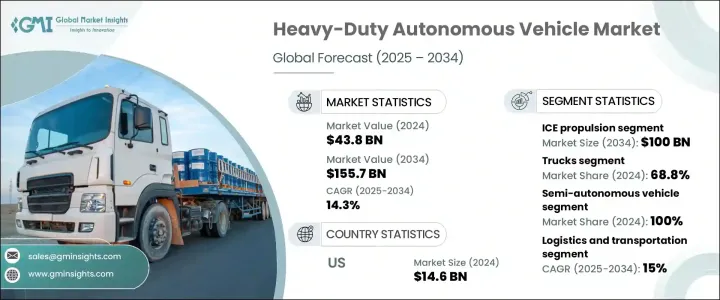

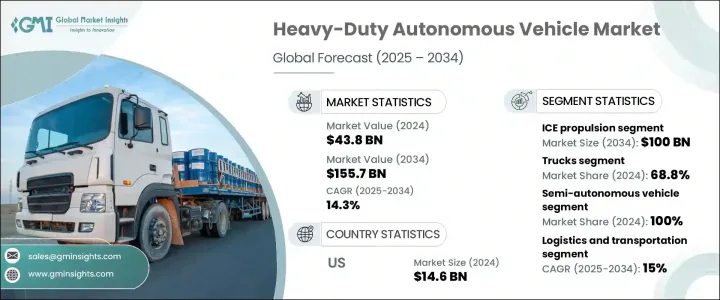

세계 대형 자율주행차(HDAV) 시장은 2024년 438억 달러에 달했고, 2025-2034년 연평균 복합 성장률(CAGR) 14.3%로 성장할 것으로 전망됩니다.

강화된 안전 기능에 대한 수요 증가와 자율주행 기술의 채택 증가가 이 분야의 큰 성장을 주도하고 있습니다. 자율주행 대형 차량은 최첨단 센서, 인공지능, 실시간 데이터 분석을 통합하여 도로를 효율적으로 탐색함으로써 교통수단에 혁명을 일으키고 있습니다. 이러한 첨단 시스템을 통해 차량은 주변 상황을 파악하고 즉각적인 판단을 내릴 수 있으며, 역동적인 교통 상황에 적응하여 사고 위험을 크게 줄일 수 있습니다. 이러한 자동화로의 전환은 교통 안전을 향상시킬 뿐만 아니라 인적 오류를 최소화하고, 인명 피해를 줄이며, 의료 및 재산 피해에 대한 비용을 크게 절감할 수 있습니다.

지속가능성과 운영 효율성에 대한 관심이 높아지면서 업계 전반에 걸쳐 중장비 자율 주행 차량 도입이 가속화되고 있습니다. 기업들은 노동력 부족을 해결하고, 장기적인 비용을 절감하고, 차량 관리를 최적화하기 위해 자동화를 활용하고 있으며, AI 기반 의사결정과 실시간 연결성의 발전으로 자율주행 트럭과 버스는 물류, 광업, 건설, 대중교통에 필수적인 존재가 되고 있습니다. 각국 정부는 자율 주행 차량의 테스트와 상용화를 촉진하는 규제와 정책을 도입하여 기존 교통망에 안전하고 원활하게 통합될 수 있도록 하고 있습니다. 또한, 5G 연결, 클라우드 기반 모니터링, 머신러닝 알고리즘의 급속한 발전은 업계를 발전시키고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 438억 달러 |

| 예상 금액 | 1,557억 달러 |

| CAGR | 14.3% |

이 시장은 내연기관차(ICE), 전기자동차, 하이브리드 자동차 등 추진력 유형에 따라 구분되며, 2024년에는 ICE가 60% 시장 점유율을 차지했고, 2034년에는 1,000억 달러에 달할 것으로 예측됩니다. 연료 보급 인프라로 인해 초기 단계의 연구개발에 여전히 선호되는 선택입니다. 전기자동차에 비해 주행거리가 길어 장거리 주행과 험난한 지형에 적합하며, 다양한 환경에서 폭넓은 테스트와 채택이 용이합니다.

차량 유형별로 중장비 자율주행차 시장은 트럭과 버스로 분류됩니다. 트럭은 2024년 68.8%로 압도적인 점유율을 차지했으며, 물류, 광업, 제조업 등의 산업에서 광범위하게 사용되고 있는 것이 그 요인으로 분석됩니다. 자율 주행 트럭은 휴식 없이 연속 운행이 가능하여 연료 소비를 최적화하고 배송을 신속하게 처리할 수 있습니다. 기업들이 효율성과 비용 절감을 우선시하는 가운데, 자율주행 트럭으로의 전환은 공급망 진화의 중요한 요소가 되고 있습니다. 기업들은 운송을 간소화하고, 생산성을 높이고, 노동력 부족을 완화하기 위해 자율주행 트럭 솔루션에 대한 투자를 늘리고 있습니다.

북미의 중장비 자율주행차 시장은 2024년 146억 달러 규모에 달했습니다. 정부 주도로 자율주행차 테스트와 대규모 배치를 지원하기 위한 규제 프레임워크가 적극적으로 형성되고 있습니다. 교통 안전과 교통 체증 완화에 대한 관심이 높아지면서 이 지역의 자율주행 대형 차량에 대한 수요가 증가하고 있습니다. 자율주행 기술이 계속 발전함에 따라 북미는 중요한 시장으로 부상하고 있으며, 업계 리더들은 운송 및 물류를 재정의하는 차세대 혁신에 투자하고 있습니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 원재료 제조업체

- 부품 제조업체

- 제조업체

- 기술 제공업체

- 유통 채널 분석

- 최종 용도

- 이익률 분석

- 공급업체 상황

- 기술 및 혁신 전망

- 특허 분석

- 규제 상황

- 비용 내역 분석

- 가격 동향

- 주요 뉴스와 이니셔티브

- 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추산 및 예측 : 차량별, 2021년-2034년

- 주요 동향

- 트럭

- 클래스 7

- 클래스 8

- 버스

제6장 시장 추산 및 예측 : 자율주행 레벨별, 2021년-2034년

- 주요 동향

- 반자율주행차

- 레벨 1

- 레벨 2

- 레벨 3

- 자율주행차

- 레벨 4

제7장 시장 추산 및 예측 : 추진별, 2021년-2034년

- 주요 동향

- ICE

- 전기자동차

- 하이브리드 자동차

제8장 시장 추산 및 예측 : 용도별, 2021년-2034년

- 주요 동향

- 물류 및 운송

- 광업

- 농업

- 건설

- 석유 및 가스

- 기타

제9장 시장 추산 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 프랑스

- 영국

- 스페인

- 이탈리아

- 러시아

- 북유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 뉴질랜드

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 남아프리카공화국

- 사우디아라비아

제10장 기업 개요

- 2getthere

- Aurora

- Baidu

- Caterpillar

- Daimler Truck

- Embark Trucks

- FAW

- General Motors

- Kodiak Robotics

- Navya ARMA

- New Flyer

- Oxa Autonomy

- PACCAR

- Schaeffler AG

- Torc Robotics

- TRATON

- TuSimple

- Volvo

- ZF Friedrichshafen

- Zoox

The Global Heavy-duty Autonomous Vehicle Market reached USD 43.8 billion in 2024 and is projected to expand at a CAGR of 14.3% between 2025 and 2034. The rising demand for enhanced safety features, coupled with the increasing adoption of self-driving technology, is driving substantial growth in this sector. Autonomous heavy-duty vehicles are revolutionizing transportation by integrating cutting-edge sensors, artificial intelligence, and real-time data analysis to navigate roads efficiently. These advanced systems allow vehicles to assess their surroundings, make instant decisions, and adapt to dynamic traffic conditions, significantly reducing accident risks. This shift toward automation not only enhances road safety but also minimizes human error, leading to fewer fatalities and injuries and substantial cost savings on healthcare and property damage.

The growing emphasis on sustainability and operational efficiency is further accelerating the adoption of heavy-duty autonomous vehicles across industries. Companies are leveraging automation to address labor shortages, reduce long-term expenses, and optimize fleet management. With advancements in AI-driven decision-making and real-time connectivity, autonomous trucks and buses are becoming integral to logistics, mining, construction, and public transportation. Governments worldwide are introducing regulations and policies to facilitate autonomous vehicle testing and commercial deployment, ensuring safe and seamless integration into existing transportation networks. Additionally, rapid developments in 5G connectivity, cloud-based monitoring, and machine learning algorithms are propelling the industry forward.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $43.8 Billion |

| Forecast Value | $155.7 Billion |

| CAGR | 14.3% |

The market is segmented based on propulsion types, including internal combustion engine (ICE), electric, and hybrid vehicles. In 2024, the ICE segment dominated with a 60% market share and is expected to generate USD 100 billion by 2034. ICE-powered autonomous vehicles remain the preferred choice for early-stage research and development due to their affordability and well-established refueling infrastructure. Their extended range compared to electric alternatives makes them more suitable for long-distance operations and challenging terrains, facilitating broader testing and adoption across diverse environments.

By vehicle type, the heavy-duty autonomous vehicle market is categorized into trucks and buses. Trucks held a dominant share of 68.8% in 2024, driven by their widespread use in industries such as logistics, mining, and manufacturing. Autonomous trucks offer continuous operation without breaks, optimizing fuel consumption and expediting deliveries. As businesses prioritize efficiency and cost reduction, the shift toward self-driving trucks is becoming a critical component of supply chain evolution. Companies are increasingly investing in autonomous trucking solutions to streamline transportation, enhance productivity, and mitigate workforce shortages.

North America heavy-duty autonomous vehicle market generated USD 14.6 billion in 2024. Government initiatives are actively shaping regulatory frameworks to support autonomous vehicle testing and large-scale deployment. The growing focus on road safety and congestion reduction is propelling demand for self-driving heavy-duty vehicles in this region. As autonomous technology continues to evolve, North America is emerging as a key market, with industry leaders investing in next-generation innovations to redefine transportation and logistics.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Raw material providers

- 3.1.1.2 Component providers

- 3.1.1.3 Manufacturers

- 3.1.1.4 Technology providers

- 3.1.1.5 Distribution channel analysis

- 3.1.1.6 End Use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Technology & innovation landscape

- 3.3 Patent analysis

- 3.4 Regulatory landscape

- 3.5 Cost breakdown analysis

- 3.6 Price trend

- 3.7 Key news & initiatives

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Rising demand for automation in mining and construction

- 3.8.1.2 Advancements in ai and sensor technologies

- 3.8.1.3 Regulatory push for safer and sustainable transport

- 3.8.1.4 Growing government investment in infrastructure development

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High initial investment costs

- 3.8.2.2 Regulatory and safety concerns

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Trucks

- 5.2.1 Class 7

- 5.2.2 Class 8

- 5.3 Buses

Chapter 6 Market Estimates & Forecast, By Level of Autonomy, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Semi-autonomous vehicle

- 6.2.1 Level 1

- 6.2.2 Level 2

- 6.2.3 Level 3

- 6.3 Autonomous vehicle

- 6.3.1 Level 4

Chapter 7 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 ICE

- 7.3 Electric vehicle

- 7.4 Hybrid vehicle

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Logistics and transportation

- 8.3 Mining

- 8.4 Agriculture

- 8.5 Construction

- 8.6 Oil & gas

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 France

- 9.3.3 U.K.

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 South Africa

- 9.6.3 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 2getthere

- 10.2 Aurora

- 10.3 Baidu

- 10.4 Caterpillar

- 10.5 Daimler Truck

- 10.6 Embark Trucks

- 10.7 FAW

- 10.8 General Motors

- 10.9 Kodiak Robotics

- 10.10 Navya ARMA

- 10.11 New Flyer

- 10.12 Oxa Autonomy

- 10.13 PACCAR

- 10.14 Schaeffler AG

- 10.15 Torc Robotics

- 10.16 TRATON

- 10.17 TuSimple

- 10.18 Volvo

- 10.19 ZF Friedrichshafen

- 10.20 Zoox