|

시장보고서

상품코드

1708156

드립트레이 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Drip Trays Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

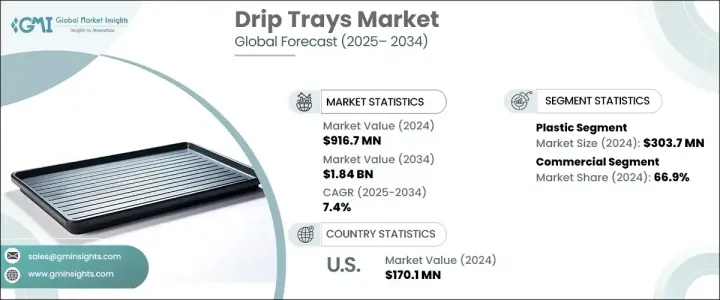

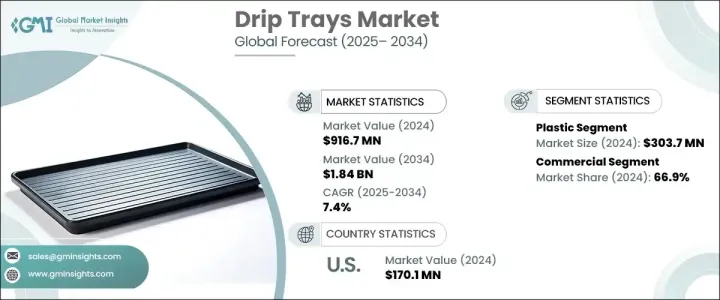

드립 트레이 세계 시장은 2024년에 9억 1,670만 달러에 달했고, 2025-2034년 연평균 7.4%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다.

이러한 시장 성장의 원동력은 드립 트레이의 내구성과 효율성을 높이고 상업 및 산업용으로 적합한 소재와 디자인의 지속적인 발전으로 인해 시장 확대가 이루어지고 있습니다. 친환경 솔루션으로의 전환은 시장 성장을 더욱 촉진하고 있으며, 제조업체들은 알루미늄 및 고밀도 폴리에틸렌(HDPE)과 같은 지속 가능한 고성능 소재에 초점을 맞추었습니다. 이러한 기술 혁신은 다양한 산업 분야의 요구를 충족하는 가볍고 부식에 강하며 수명이 긴 드립 트레이를 개발하는 데 기여하고 있습니다.

다양한 산업 분야에서 작업장 안전과 유출 방지에 대한 관심이 높아지면서 기업들은 첨단 드립 트레이 솔루션을 채택하고 있습니다. 특히 자동차, 식품 가공, 제조 등 엄격한 규제 준수가 요구되는 산업에서 맞춤형 특수 설계에 대한 수요가 증가하고 있습니다. 기업들은 환경적 위험을 최소화하고 업무 효율성을 높이기 위해 효율적이고 비용 효율적인 봉쇄 솔루션을 찾고 있습니다. 또한, 기술의 발전으로 드립 트레이에 자동 누출 감지 및 누출 방지 기능이 도입되어 기능성과 최종 사용자에 대한 호소력을 향상시키고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 9억 1,670만 달러 |

| 예상 금액 | 18억 4,000만 달러 |

| CAGR | 7.4% |

플라스틱 부문은 2024년 3억 3,700만 달러에 달했고, 시장에서의 강력한 입지를 강조하고 있습니다. 플라스틱 드립 트레이는 비용 효율성, 다용도성, 경량성으로 인해 널리 선호되고 있습니다. 이 소재 고유의 화학물질 및 열화에 대한 내성은 자동차, 제조, 식품 가공 및 기타 분야에 이상적인 선택이 되고 있습니다. 또한, 지속가능성에 대한 산업계의 관심이 높아지면서 재생 플라스틱 및 바이오플라스틱의 기술 혁신이 가속화되고 있으며, 환경 친화적인 솔루션의 가능성이 확대되고 있습니다. 규제에 대한 압력이 증가하고 기업들이 보다 친환경적인 대안을 찾는 가운데, 제조업체들은 지속가능성 목표에 부합하는 내구성이 뛰어나고 무해하며 재사용이 가능한 플라스틱 드립 트레이를 개발하기 위해 연구 개발에 투자하고 있습니다.

2024년 시장 점유율은 상업 부문이 66.9%로 압도적이어서 다양한 산업에서 격리 솔루션에 대한 요구가 증가하고 있음을 강조합니다. 식품 가공, 자동차, 제조 분야의 기업들은 안전, 규정 준수 및 업무 효율성을 높이기 위해 드립 트레이를 채택하고 있습니다. 재료 과학과 제품 설계의 지속적인 발전으로 이러한 솔루션은 유출과 누출을 방지하는 데 더욱 효과적이며, 그 결과 작업장 내 위험과 환경적 책임을 감소시키고 있습니다. 기업이 안전과 비용 효율적인 유출 관리를 우선시함에 따라 상업용 부문이 드립 트레이 시장에서 지배적인 지위를 유지할 것으로 예측됩니다.

미국 드립 트레이 시장은 2024년 1억 7,010만 달러로 평가되었고, 업계 전반의 엄격한 환경 규제와 안전 프로토콜에 힘입어 성장하고 있습니다. 이 시장은 특정 산업 요구 사항에 맞는 맞춤형 드립 트레이의 채택이 증가함에 따라 꾸준한 성장세를 보이고 있습니다. 내식성 및 경량 옵션과 같은 재료 기술 혁신은 제품의 매력을 높여 수요를 견인하고 있습니다. 기업들은 규정 준수 기준을 충족하고 업무 효율성을 개선하기 위해 고품질의 내구성 있는 드립 트레이에 대한 투자를 늘리고 있으며, 미국은 드립 트레이 세계 시장 확대에 크게 기여하고 있습니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 미치는 요인.

- 이익률 분석

- 파괴적 변화

- 향후 전망

- 제조업체

- 유통업체

- 공급업체 상황

- 이익률 분석

- 주요 뉴스

- 규제 상황

- 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 잠재 성장력 분석

- 기술 개요

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략 전망 매트릭스

제5장 시장 추산 및 예측 : 재료 유형별, 2021년-2034년

- 주요 동향

- 플라스틱

- 금속

- 스테인리스

- 알루미늄

- 기타

- 유리섬유

- 기타(고무, 복합재 등)

제6장 시장 추산 및 예측 : 디자인별, 2021년-2034년

- 주요 동향

- Flat

- Grated

- Stackable

- 기타(Recessed 등)

제7장 시장 규모 추산·예측 : 사이즈별, 2021년-2034년

- 주요 동향

- 표준 사이즈

- 커스텀 사이즈

- 모듈러 시스템

제8장 시장 추산 및 예측 : 최종 용도별, 2021년-2034년

- 주요 동향

- 산업

- 공작기계

- 생산 설비

- 화학 플랜트

- 석유 및 가스

- 식품 가공

- 유틸리티

- 기타(전자부품 등)

- 상업

- 레스토랑 및 카페

- 호텔 및 호스피탈리티

- 소매점

- 오피스 빌딩

- 시설

- 병원

- 기타(정부 시설 등)

- 주택

제9장 시장 추산 및 예측 : 유통 채널별, 2021년-2034년

- 주요 동향

- 직접 판매

- 간접 판매

제10장 시장 추산 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 일본

- 인도

- 한국

- 호주

- 말레이시아

- 인도네시아

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카공화국

제11장 기업 개요

- Brewfitt

- DENIOS

- Drrader Manufacturing

- Eagle Manufacturing

- Haws

- Justrite

- MFG Tray

- Micro Matic

- New Pig

- Raffeiner GmbH

- Riverside Sheet Metal &Fabrications

- Short Run Pro

- SP Bel-Art

- Weber

- WirthCo Engineering

The Global Drip Trays Market reached USD 916.7 million in 2024 and is projected to grow at a CAGR of 7.4% between 2025 and 2034. This expansion is driven by continuous advancements in material and design, making drip trays more durable, efficient, and suited for commercial and industrial applications. The shift toward eco-friendly solutions is further fueling market growth, with manufacturers focusing on sustainable and high-performance materials such as aluminum and High-Density Polyethylene (HDPE). These innovations contribute to the development of lightweight, corrosion-resistant, and long-lasting drip trays that cater to diverse industry needs.

A rising emphasis on workplace safety and spill containment across multiple industries is pushing businesses to adopt advanced drip tray solutions. The demand for customized and specialized designs is increasing, particularly in industries that require stringent regulatory compliance, such as automotive, food processing, and manufacturing. Companies are seeking efficient and cost-effective containment solutions to minimize environmental risks and enhance operational efficiency. Furthermore, technological advancements have introduced automated leak detection and spill prevention features in drip trays, improving their functionality and appeal to end users.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $916.7 million |

| Forecast Value | $1.84 billion |

| CAGR | 7.4% |

The plastic segment generated USD 303.7 million in 2024, highlighting its strong presence in the market. Plastic drip trays are widely preferred due to their cost-effectiveness, versatility, and lightweight nature, which enhances mobility and adaptability in different settings. The material's inherent resistance to chemicals and degradation makes it an ideal choice for sectors such as automotive, manufacturing, and food processing. Additionally, the industry's growing focus on sustainability has spurred innovations in recycled plastics and bioplastics, expanding opportunities for environmentally conscious solutions. As regulatory pressures mount and businesses seek greener alternatives, manufacturers are investing in research and development to create durable, non-toxic, and reusable plastic drip trays that align with sustainability goals.

The commercial sector held a commanding 66.9% market share in 2024, emphasizing the increasing need for containment solutions across various industries. Businesses in the food processing, automotive, and manufacturing sectors are adopting drip trays to enhance safety, regulatory compliance, and operational efficiency. The ongoing advancements in material science and product design are making these solutions more effective in preventing spills and leaks, thus reducing workplace hazards and environmental liabilities. As companies prioritize safety and cost-effective spill management, the commercial sector is expected to remain a dominant force in the drip trays market.

The U.S. drip trays market was valued at USD 170.1 million in 2024, supported by stringent environmental regulations and safety protocols across industries. The market is experiencing steady growth due to the rising adoption of customized drip trays tailored to specific industry requirements. Innovations in material technology, such as corrosion-resistant and lightweight options, are enhancing product appeal and driving demand. Companies are increasingly investing in high-quality, durable drip trays to meet compliance standards and improve operational efficiencies, making the U.S. a key contributor to the global drip trays market expansion.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations.

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain.

- 3.1.2 Profit margin analysis.

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Profit margin analysis

- 3.4 Key news & initiatives

- 3.5 Regulatory landscape

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Increasing awareness of workplace safety and environmental regulations

- 3.6.1.2 Rising demand from industries such as automotive and manufacturing

- 3.6.1.3 Innovation in materials and eco-friendly designs

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 High competition among market players

- 3.6.2.2 Fluctuating raw material prices

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Technology overview

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Material Type, 2021-2034 (USD Million) (Thousand Units)

- 5.1 Key trends

- 5.2 Plastic

- 5.3 Metal

- 5.3.1 Stainless steel

- 5.3.2 Aluminum

- 5.3.3 Others

- 5.4 Fiberglass

- 5.5 Others (Rubber, Composite, etc.)

Chapter 6 Market Estimates & Forecast, By Design, 2021-2034 (USD Million) (Thousand Units)

- 6.1 Key trends

- 6.2 Flat

- 6.3 Grated

- 6.4 Stackable

- 6.5 Others (Recessed, etc.)

Chapter 7 Market Estimates & Forecast, By Size, 2021-2034 (USD Million) (Thousand Units)

- 7.1 Key trends

- 7.2 Standard sizes

- 7.3 Custom sizes

- 7.4 Modular systems

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Million) (Thousand Units)

- 8.1 Key trends

- 8.2 Industrial

- 8.2.1 Machine tools

- 8.2.2 Production equipment

- 8.2.3 Chemical plants

- 8.2.4 Oil & gas

- 8.2.5 Food processing

- 8.2.6 Utilities

- 8.2.7 Others (Electronic component, etc.)

- 8.3 Commercial

- 8.3.1 Restaurants & cafes

- 8.3.2 Hotels & hospitality

- 8.3.3 Retail stores

- 8.3.4 Office buildings

- 8.3.5 Institutional

- 8.3.6 Hospitals

- 8.3.7 Others (Government facilities, etc.)

- 8.4 Residential

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021-2034 (USD Million) (Thousand Units)

- 9.1 Key trends

- 9.2 Direct sales

- 9.3 Indirect sales

Chapter 10 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Thousand Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Malaysia

- 10.4.7 Indonesia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Brewfitt

- 11.2 DENIOS

- 11.3 Drrader Manufacturing

- 11.4 Eagle Manufacturing

- 11.5 Haws

- 11.6 Justrite

- 11.7 MFG Tray

- 11.8 Micro Matic

- 11.9 New Pig

- 11.10 Raffeiner GmbH

- 11.11 Riverside Sheet Metal & Fabrications

- 11.12 Short Run Pro

- 11.13 SP Bel-Art

- 11.14 Weber

- 11.15 WirthCo Engineering