|

시장보고서

상품코드

1708214

의약품 콜드체인 포장 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Pharmaceutical Cold Chain Packaging Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

세계의 의약품 콜드체인 포장 시장은 2024년에 175억 달러를 창출하며, 2025-2034년에 15.1%의 CAGR로 성장할 것으로 예측됩니다.

이러한 성장은 주로 mRNA 기반 치료, 세포 치료, 유전자 치료 등 공급망 전반에 걸쳐 엄격한 온도 관리가 필요한 첨단 치료법의 채택이 증가하고 있기 때문입니다. 제약회사들이 이러한 혁신적인 치료제에 대한 수요 증가에 대응하기 위해 생산을 확대함에 따라 신뢰할 수 있는 콜드체인 포장 솔루션의 필요성이 더욱 중요해지고 있습니다. 콜드체인 포장은 제조 현장에서 최종사용자까지 운송하는 동안 생물제제 및 백신과 같은 온도에 민감한 의약품의 안전성, 안정성 및 유효성을 보장합니다.

또한 만성질환 증가와 맞춤형 의료 증가로 인해 복잡한 생물제제의 효능을 유지하기 위한 특수 포장 솔루션에 대한 필요성이 증가하고 있습니다. 보관 및 운송 중 온도에 민감한 의약품의 품질 및 규정 준수 유지에 대한 관심이 높아지면서 시장 확대에 더욱 기여하고 있습니다. 규제 당국의 감시가 강화되고 엄격한 유통 프로토콜을 준수해야 할 필요성이 증가함에 따라 제조업체들은 제품의 안전과 규정 준수를 보장하기 위해 첨단 콜드체인 포장 기술에 투자하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024년 |

| 예측연도 | 2025-2034년 |

| 시작 금액 | 175억 달러 |

| 예상 금액 | 716억 달러 |

| CAGR | 15.1% |

의약품 콜드체인 포장 시장은 재료별로 분류되며, 플라스틱, 금속, 종이가 주요 카테고리입니다. 플라스틱 부문은 2024년 135억 달러 규모 시장을 창출할 것으로 예측됩니다. 플라스틱의 장점은 운송 중 필요한 온도를 유지하는 데 필수적인 우수한 단열성에 기인합니다. 가볍고 비용 효율적이기 때문에 제품의 무결성을 유지하면서 운송 비용을 절감하고자 하는 제약회사에게 이상적인 선택이 될 수 있습니다. 내구성과 확장성으로 유명한 플라스틱 소재는 생물제제 및 기타 민감한 의약품을 안전하게 운송할 수 있는 실용적인 솔루션을 제공합니다. 생물제제에 대한 수요가 증가함에 따라 공급망 전체에 걸쳐 정확한 온도 제어를 유지할 수 있는 플라스틱 포장에 대한 수요가 증가하여 시장내 플라스틱 포장 부문의 입지가 강화될 것으로 예측됩니다.

시장은 물류 및 유통 센터, 바이오 제약 기업, 병원, 임상 연구 기관, 연구 기관, 기타 등 최종사용자별로 세분화됩니다. 바이오 제약회사는 2024년 63억 달러를 창출했으며, 이는 이 부문의 급속한 확장을 반영합니다. 유전자 치료와 mRNA 치료의 채택이 증가함에 따라 민감한 의약품의 안정성과 효능을 유지할 수 있는 특수 포장 솔루션에 대한 수요가 증가하고 있습니다. 엄격한 규제 지침은 유통 과정 전반에 걸쳐 안전 표준을 준수할 수 있는 첨단 콜드체인 포장 솔루션의 필요성을 촉진하는 데 중요한 역할을 하고 있습니다. 바이오 제약 기업이 생산 능력을 확대함에 따라 신뢰할 수 있는 고품질 콜드체인 포장에 대한 수요가 증가하면서 시장 상승세가 강화될 것으로 예측됩니다.

북미 의약품 콜드체인 포장 시장은 2024년 34.4%의 점유율을 차지했습니다. 이 지역의 높은 시장 점유율은 보관 및 운송시 엄격한 온도 관리가 필요한 생물제제 및 세포치료제에 대한 수요가 증가하고 있으며, FDA를 비롯한 규제 당국은 의약품이 공급망 전반에 걸쳐 안전성, 유효성 및 규정 준수를 유지할 수 있도록 콜드체인 포장 솔루션의 채택을 촉진하는 엄격한 가이드라인을 제정하고 있습니다. 콜드체인 포장 솔루션의 채택을 촉진하는 엄격한 가이드라인을 시행하고 있습니다. 북미에서는 정밀의료에 대한 관심이 높아지고 생물제제 포트폴리오가 확대되면서 세계 의약품 콜드체인 포장 시장에서 북미가 우위를 점하고 있습니다.

목차

제1장 조사 방법과 조사 범위

제2장 개요

제3장 업계 인사이트

- 에코시스템 분석

- 업계에 대한 영향요인

- 촉진요인

- 생물제제와 특수 의약품에 대한 수요 증가

- mRNA 및 세포·유전자 치료의 확대

- 엄격한 규제 요건

- E-Commerce와 온라인 약국의 성장

- 제약 업계의 확대

- 업계의 잠재적 리스크 & 과제

- 콜드체인 인프라의 고비용

- 온도 이상과 제품 부패의 리스크

- 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술 상황

- 향후 시장 동향

- 갭 분석

- Porter의 산업 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추산·예측 : 소재별, 2021-2034년

- 주요 동향

- 플라스틱

- 폴리에틸렌(PE)

- 폴리프로필렌(PP)

- 폴리에틸렌 테레프탈레이트(PET)

- 폴리우레탄(PU)

- 기타

- 금속

- 종이

제6장 시장 추산·예측 : 유형별, 2021-2034년

- 주요 동향

- 액티브

- 패시브

제7장 시장 추산·예측 : 제품별, 2021-2034년

- 주요 동향

- 단열 박스

- 용기

- 보냉제

- 파렛트

- 기타

제8장 시장 추산·예측 : 최종 용도 산업별, 2021-2034년

- 주요 동향

- 바이오의약품 기업

- 임상 연구기관

- 병원

- 연구기관

- 물류·유통 기업

- 기타

제9장 시장 추산·예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 아랍에미리트

제10장 기업 개요

- Chill-Pak

- Cold Chain Technologies

- CoolPac

- Cryopak

- CSafe

- Envirotainer

- Haier Biomedical

- Insulated Products Corporation

- Intelsius

- Nordic Cold Chain Solutions

- Sealed Air

- Smurfit Kappa

- Sofrigam Group

- Sonoco ThermoSafe

- Tessol

- Va-Q-Tec Thermal Solutions

- Vericool

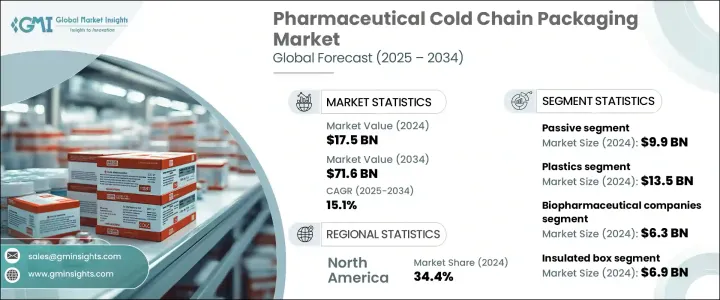

The Global Pharmaceutical Cold Chain Packaging Market generated USD 17.5 billion in 2024 and is projected to grow at a CAGR of 15.1% between 2025 and 2034. This growth is primarily driven by the increasing adoption of advanced therapies, such as mRNA-based treatments, cell therapies, and gene therapies, which require strict temperature control throughout the supply chain. As pharmaceutical companies ramp up production to meet the rising demand for these innovative treatments, the need for reliable cold chain packaging solutions becomes more critical. Cold chain packaging ensures the safety, stability, and efficacy of temperature-sensitive drugs, including biologics and vaccines, during transportation from manufacturing sites to end users.

Additionally, the rise in chronic diseases and the growing trend of personalized medicine have heightened the need for specialized packaging solutions to maintain the potency of complex biologics. The growing focus on maintaining the quality and compliance of temperature-sensitive pharmaceutical products during storage and transit further contributes to the market's expansion. Increased regulatory scrutiny and the need to adhere to strict distribution protocols push manufacturers to invest in advanced cold chain packaging technologies, ensuring product safety and compliance.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $17.5 Billion |

| Forecast Value | $71.6 Billion |

| CAGR | 15.1% |

The pharmaceutical cold chain packaging market is segmented by material, with plastic, metal, and paper being the primary categories. The plastic segment generated USD 13.5 billion in 2024. Plastic's dominance can be attributed to its superior thermal insulation properties, which are essential for maintaining the required temperatures during transit. Its lightweight nature and cost-effectiveness make it an ideal choice for pharmaceutical companies aiming to reduce shipping costs while preserving product integrity. Plastic materials, known for their durability and scalability, provide a practical solution for ensuring the safe transportation of biologics and other sensitive drugs. As the demand for biologics increases, the need for plastic packaging that can maintain precise temperature control throughout the supply chain is expected to grow, strengthening the segment's position in the market.

The market is further categorized by end users, including logistics and distribution centers, biopharmaceutical companies, hospitals, clinical research organizations, research institutes, and others. Biopharmaceutical companies generated USD 6.3 billion in 2024, reflecting the rapid expansion of this segment. The growing adoption of gene and mRNA therapies has fueled the demand for specialized packaging solutions capable of preserving the stability and efficacy of sensitive pharmaceuticals. Strict regulatory guidelines play a crucial role in driving the need for advanced cold chain packaging solutions that ensure compliance with safety standards throughout the distribution process. As biopharmaceutical companies expand their production capabilities, the demand for reliable and high-quality cold chain packaging is expected to rise, reinforcing the market's upward trajectory.

North America's pharmaceutical cold chain packaging market held a 34.4% share in 2024. The region's strong market presence is largely attributed to the growing demand for biologics and cell therapies, which require stringent temperature management during storage and transportation. Regulatory authorities, including the FDA, enforce strict guidelines that drive the adoption of cold chain packaging solutions, ensuring that pharmaceutical products maintain their safety, efficacy, and compliance throughout the supply chain. The increasing emphasis on precision medicine and the expanding portfolio of biologics in North America contribute to the region's stronghold in the global pharmaceutical cold chain packaging market.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising demand for biologics & specialty drugs

- 3.2.1.2 Expansion of mRNA & cell/gene therapies

- 3.2.1.3 Stringent regulatory requirement

- 3.2.1.4 Growth of e-commerce and online pharmacies

- 3.2.1.5 Expansion of the pharmaceutical industry

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High costs of cold chain infrastructure

- 3.2.2.2 Risk of temperature excursions & product spoilage

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Technology landscape

- 3.6 Future market trends

- 3.7 Gap analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Material, 2021 - 2034 (USD Billion & Kilo Tons)

- 5.1 Key trends

- 5.2 Plastics

- 5.2.1 Polyethylene (PE)

- 5.2.2 Polypropylene (PP)

- 5.2.3 Polyethylene Terephthalate (PET)

- 5.2.4 Polyurethane (PU)

- 5.2.5 Others

- 5.3 Metal

- 5.4 Paper

Chapter 6 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Billion & Kilo Tons)

- 6.1 Key trends

- 6.2 Active

- 6.3 Passive

Chapter 7 Market Estimates and Forecast, By Product, 2021 - 2034 (USD Billion & Kilo Tons)

- 7.1 Key trends

- 7.2 Insulated box

- 7.3 Containers

- 7.4 Coolants

- 7.5 Pallets

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By End Use Industry, 2021 - 2034 (USD Billion & Kilo Tons)

- 8.1 Key trends

- 8.2 Biopharmaceutical companies

- 8.3 Clinical research organizations

- 8.4 Hospitals

- 8.5 Research institutes

- 8.6 Logistics and distribution companies

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion & Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Chill-Pak

- 10.2 Cold Chain Technologies

- 10.3 CoolPac

- 10.4 Cryopak

- 10.5 CSafe

- 10.6 Envirotainer

- 10.7 Haier Biomedical

- 10.8 Insulated Products Corporation

- 10.9 Intelsius

- 10.10 Nordic Cold Chain Solutions

- 10.11 Sealed Air

- 10.12 Smurfit Kappa

- 10.13 Sofrigam Group

- 10.14 Sonoco ThermoSafe

- 10.15 Tessol

- 10.16 Va-Q-Tec Thermal Solutions

- 10.17 Vericool