|

시장보고서

상품코드

1716597

전립선암 치료제 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Prostate Cancer Therapeutics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

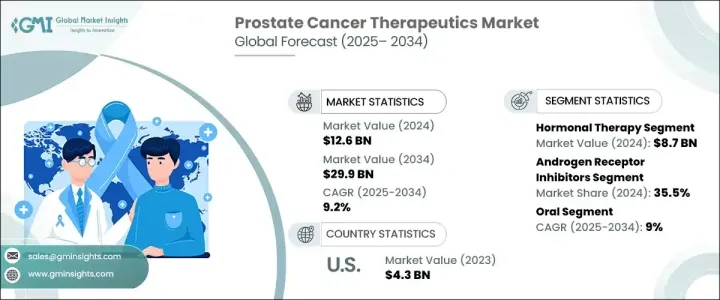

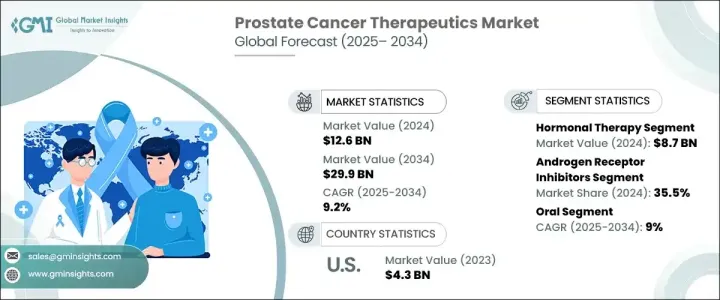

세계의 전립선암 치료제 시장은 2024년에 126억 달러를 창출했고 2025년부터 2034년에 걸쳐 CAGR 9.2%를 나타낼 것으로 예측되고 있습니다.

이 시장은 조기 진단과 효과적인 치료 옵션에 대한 의식이 높아짐에 따라 세계의 전립선암 유병률 증가를 주요 요인으로 큰 기세를 보이고 있습니다. 전립선암은 남성에게 가장 많은 암 중 하나이며 어시스템은 환자의 예후를 개선하기 위해 선진적인 치료제의 도입에 주력하고 있습니다.

또한 정밀의료 혁신과 유전체 검사, 바이오 마커 식별, AI 탑재 영상 진단 등의 고도 진단 도구의 통합이 전립선 암의 발견과 치료 계획에 혁명을 가져오고 있습니다. 도입하기 위한 연구 개발에 다액의 투자를 실시하고 있어, 병기가 진행된 환자에게 새로운 희망을 가져오고 있습니다. 또한, 병용 요법이나 면역 요법의 채용이 중시되게 된 것으로, 보다 안전하고 효율적인 치료법의 길이 열려, 치료의 전망이 크게 바뀌고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 126억 달러 |

| 예측 금액 | 299억 달러 |

| CAGR | 9.2% |

시장은 호르몬 요법, 화학 요법, 면역 요법, 표적 요법 및 기타 치료법을 포함한 다양한 치료 접근법에 따라 분류됩니다. 호르몬 요법은 안드로겐 호르몬 수준을 저하시키는 것으로, 질환의 진행을 억제하는 중요한 역할을 완수하기 위해, 전립선암 관리의 요로 계속되고 있습니다. 특히 테스토스테론은 전립선 암의 성장을 가속할 것으로 알려져 있습니다. 환자의 생존율 향상에 기여합니다. 진행 증례나 내성 증례에 의해 유효한 차세대 호르몬제의 채용이 증가하고 있는 것이, 세계 시장에서의 이 치료 부문의 우위성을 더욱 견고하게 하고 있습니다.

약물 등급별로 안드로겐 수용체 억제제(ARI)는 2024년 시장 점유율의 35.5%를 차지했습니다. 그리고 암세포가 안드로겐을 이용하여 증식하는 것을 저해합니다.

세계의 전립선암 치료제 시장은 2024년 북미가 39.2%의 점유율을 차지했습니다. 고수준의 공적·사적 투자, 제약회사와 연구기관의 공동 노력이, 이 지역 전체의 전립선암 치료의 기술 혁신을 계속적으로 추진하고 있습니다.

목차

제1장 조사 방법과 조사 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 전립선암의 유병률 증가

- 기술의 진보

- 의식의 고조와 스크리닝 프로그램

- 업계의 잠재적 위험 및 과제

- 고액의 치료비

- 치료에 따른 부작용

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 상환 시나리오

- 파이프라인 분석

- Porter's Five Forces 분석

- PESTEL 분석

- 향후 시장 동향

- 갭 분석

제4장 경쟁 구도

- 서론

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계·예측 : 치료별(2021-2034년)

- 주요 동향

- 호르몬 요법

- 화학 요법

- 면역 요법

- 표적 요법

- 기타 요법

제6장 시장 추계·예측 : 약제 클래스별(2021-2034년)

- 주요 동향

- 안드로겐 수용체 억제제

- GnRH 수용체 길항제

- PARP 억제제

- 면역관문억제제

- 기타 약제 클래스별

제7장 시장 추계·예측 : 투여 경로별(2021-2034년)

- 주요 동향

- 경구제

- 주사제

제8장 시장 추계·예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 병원 약국

- 오프라인 매장

- 전자상거래

제9장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Astellas Pharma

- AstraZeneca

- Bayer

- Dendreon Pharmaceuticals

- Exelixis

- Ferring

- GlaxoSmithKline

- Ipsen Pharma

- Johnson &Johnson

- Novartis

- Pfizer

- Sanofi

- Sumitomo Pharma America

- Takeda Pharmaceutical

- Tolmar

The Global Prostate Cancer Therapeutics Market generated USD 12.6 billion in 2024 and is projected to expand at a CAGR of 9.2% from 2025 to 2034. The market is witnessing significant momentum, primarily driven by the growing prevalence of prostate cancer worldwide, coupled with increasing awareness around early diagnosis and effective treatment options. With prostate cancer ranking among the most common cancers in men, healthcare systems are focusing on adopting advanced therapeutics to improve patient outcomes. The aging male population, rising incidence rates, and a surge in patient awareness through government-led initiatives and cancer advocacy groups continue to foster market growth.

Moreover, innovations in precision medicine and the integration of advanced diagnostic tools like genomic testing, biomarker identification, and AI-powered imaging are revolutionizing prostate cancer detection and treatment planning. Pharmaceutical giants are heavily investing in research and development to introduce novel drugs and personalized therapies that can effectively target resistant forms of prostate cancer, offering renewed hope for patients with advanced disease stages. Additionally, the increased emphasis on combination therapies and the adoption of immunotherapies are transforming the therapeutic landscape, making way for safer and more efficient treatment modalities.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $12.6 Billion |

| Forecast Value | $29.9 Billion |

| CAGR | 9.2% |

The market is segmented based on different therapeutic approaches, including hormonal therapy, chemotherapy, immunotherapy, targeted therapy, and other treatment options. In 2024, hormonal therapy led the market, generating USD 8.7 billion in revenue. Hormonal therapy remains a cornerstone in prostate cancer management as it plays a crucial role in controlling the disease's progression by lowering androgen hormone levels. These hormones, especially testosterone, are known to fuel prostate cancer growth. By targeting and suppressing testosterone production, hormonal therapies significantly reduce tumor size and alleviate symptoms, which contributes to improved patient survival rates. The growing adoption of next-generation hormonal agents that are more effective in advanced and resistant cases has further cemented the dominance of this therapeutic segment in the global market.

Based on drug classes, androgen receptor inhibitors (ARIs) accounted for 35.5% of the market share in 2024. ARIs have emerged as a vital treatment option for patients with advanced prostate cancer, especially those who no longer respond to traditional androgen deprivation therapy (ADT). These inhibitors work by blocking the androgen receptor signaling pathway, thereby preventing cancer cells from utilizing androgens for growth. The increased use of ARIs in both early and late-stage prostate cancer treatment has shown improved clinical outcomes, making them indispensable in the current therapeutic arsenal. The introduction of new ARIs with enhanced efficacy and safety profiles is also expected to boost their adoption over the coming years.

North America dominated the global prostate cancer therapeutics market with a 39.2% share in 2024. The region's leadership position is largely attributed to its advanced healthcare infrastructure, cutting-edge cancer care centers, and strong focus on oncology research. High levels of public and private investments, along with collaborative efforts between pharmaceutical companies and research institutions, are continuously propelling innovation in prostate cancer treatment across the region.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of prostate cancer

- 3.2.1.2 Technological advancements

- 3.2.1.3 Rising awareness and screening programs

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of treatment

- 3.2.2.2 Side effects associated with treatment

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Reimbursement scenario

- 3.6 Pipeline analysis

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

- 3.9 Future market trends

- 3.10 Gap analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Therapy, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Hormonal therapy

- 5.3 Chemotherapy

- 5.4 Immunotherapy

- 5.5 Targeted therapy

- 5.6 Other therapies

Chapter 6 Market Estimates and Forecast, By Drug Class, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Androgen receptor inhibitors

- 6.3 GnRH receptor antagonists

- 6.4 PARP inhibitors

- 6.5 Immune checkpoint inhibitors

- 6.6 Other drug classes

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Oral

- 7.3 Injectable

Chapter 8 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospital pharmacy

- 8.3 Brick and mortar

- 8.4 E-commerce

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Astellas Pharma

- 10.2 AstraZeneca

- 10.3 Bayer

- 10.4 Dendreon Pharmaceuticals

- 10.5 Exelixis

- 10.6 Ferring

- 10.7 GlaxoSmithKline

- 10.8 Ipsen Pharma

- 10.9 Johnson & Johnson

- 10.10 Novartis

- 10.11 Pfizer

- 10.12 Sanofi

- 10.13 Sumitomo Pharma America

- 10.14 Takeda Pharmaceutical

- 10.15 Tolmar