|

시장보고서

상품코드

1721431

전기 모터 경적 : 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Electric Motor Horn Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

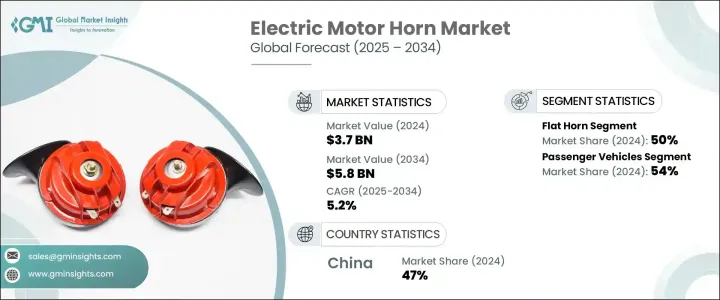

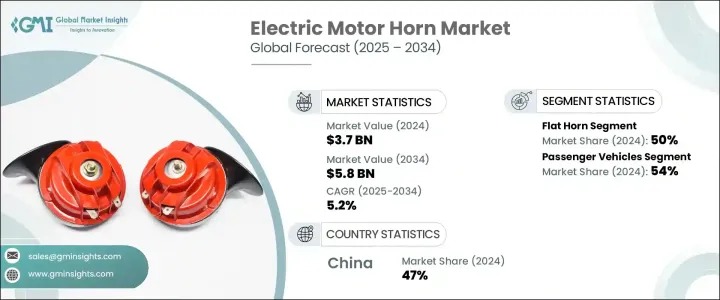

세계의 전기 모터 경적 시장 규모는 2024년 37억 달러로 평가되었고, 2034년에는 58억 달러에 이를 것으로 추정되며, CAGR 5.2%로 성장할 전망입니다. 이러한 꾸준한 성장은 전기 모터 경적에 대한 수요가 급증한 전기자동차(EV)의 채택이 증가함에 따라 촉진되고 있습니다. 기존 내연기관(ICE) 차량에 비해 조용하게 작동하는 전기차는 안전 기준을 충족하기 위해 효율적이고 소음이 적은 경고 시스템이 필요합니다. 따라서 보행자 및 도로 안전을 위해 청각적 경고 시스템이 중요해졌습니다. 전기차 보급이 증가함에 따라 소음 공해 및 소음 배출 기준에 대한 규제가 강화되면서 제조업체는 효과적일 뿐만 아니라 정부 규정을 준수하는 경적을 혁신하고 생산해야 하는 과제를 안고 있습니다.

신흥 경제국들이 더 엄격한 도로 안전법을 시행함에 따라 글로벌 시장은 변화를 목격하고 있습니다. 이러한 추세로 인해 전기차 전용으로 설계된 규제된 저데시벨 전기 경적에 대한 수요가 증가하고 있습니다. 제조업체는 안전과 환경 요건을 모두 충족하는 전기 및 하이브리드 차량에 적합한 에너지 효율적이고 컴팩트한 경적 시스템을 개발해야 한다는 압박에 시달리고 있습니다. 지속 가능성에 대한 관심이 높아지면서 최적의 소음 수준을 유지하면서 전력 소비를 줄이는 것이 업계의 주요 과제이자 혁신 분야가 되었습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 37억 달러 |

| 예측 금액 | 58억 달러 |

| CAGR | 5.2% |

2024년 플랫형 전기 모터 경적 부문은 시장 점유율의 50%를 차지했습니다. 이 경적은 컴팩트하고 공간 절약형 디자인, 견고함, 비용 효율성으로 선호되어 오토바이, 승용차, 경상용차에 선호됩니다. 다목적성과 통합 용이성 덕분에 OEM(주문자 상표 부착 생산업체)과 애프터마켓 공급업체 모두에서 지속적인 시장 지배력을 확보하고 있습니다.

승용차 부문은 2024년 시장에서 54%의 점유율을 차지했으며 2025년부터 2034년까지 5%의 연평균 성장률(CAGR)로 꾸준히 성장할 것으로 예상됩니다. 이러한 성장은 인도와 중국과 같은 신흥 시장에서 승용차의 인기가 높아짐에 따라 주도되고 있습니다. 이들 지역의 도시화, 가처분 소득 및 차량 소유 증가는 안정적이고 합리적인 가격의 안전 기능에 대한 수요를 촉진합니다. 승용차의 전기 모터 경적 수요는 상용차 및 이륜차의 수요를 계속 능가하며 가장 큰 소비 부문으로서의 입지를 굳히고 있습니다./p>

중국의 전기 모터 경적 시장은 2024년 7억 5,600만 달러로 전 세계 시장 점유율의 47%를 차지할 것으로 예상됩니다. 이러한 우위는 높은 자동차 생산량, 광범위한 전기차 보급, 정부의 도로 안전 의무화 등에 기인합니다. 비용에 민감한 소비자들이 내구성이 뛰어난 고급 경적 시스템에 대한 현지 수요를 주도하고 있습니다. 또한 차량 소유율이 증가하면서 애프터마켓 성장에 박차를 가하고 있으며, 지능형 저소음 경적 솔루션이 수요를 더욱 높이고 있습니다.

세계의 전기 모터 경적 시장의 주요 업체로는 HELLA, Panasonic, Johnson Electric, Denso, UNO Minda, MITSUBA, Imasen Electric Industrial, Robert Bosch, Nidec 및 FIAMM Technologies 등이 있습니다. 기업들은 경쟁력을 유지하기 위해 국제 규정을 준수하는 맞춤형 소음 수준을 갖춘 소형 저에너지 경적을 만들기 위해 연구 개발에 투자하고 있습니다. 전기차 제조업체와의 전략적 파트너십, 고성장 신흥 시장으로의 사업 확장, 차량 전자장치와 통합된 스마트 경적 시스템 개발은 성장을 위한 핵심 전략입니다. 또한 제조업체들은 가격 전략을 최적화하고 애프터마켓 유통 채널을 통해 증가하는 교체 부품 수요를 충족하기 위해 현지 생산 역량을 강화하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 원자재 공급자

- 부품 제조업체

- 전기 모터 경적 제조업체

- OEM(주문자 상표 부착 생산) 및 1차 공급 업체

- 애프터마켓의 유통업체 및 소매업체

- 트럼프 정권 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 경적란

- 보복 조치

- 업계에 미치는 영향

- 주요 원자재의 가격 변동

- 공급 체인 재구성

- 최종 시장에의 가격 전달

- 주요 원자재의 가격 변동

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 무역에 미치는 영향

- 이익률 분석

- 기술과 혁신의 상황

- 특허 분석

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 세계의 자동차 생산 증가

- 전 세계 정부의 차량 안전 표준을 의무화

- 전기자동차(EV) 수요 증가

- 전기 모터 경적의 기술적 발전

- 업계의 잠재적 위험 및 과제

- 엄격한 소음 공해 규제

- ADAS 및 자율 주행 차량의 채택 증가

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추계 및 예측 : 제품별(2021-2034년)

- 주요 동향

- 플랫형 경적

- 나선형 경적

- 트럼펫

제6장 시장 추계 및 예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV

- 이륜차

- 상용차

- 소형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

제7장 시장 추계 및 예측 : 음압별(2021-2034년)

- 주요 동향

- 110dB 미만

- 110-118dB

- 118 초과

제8장 시장추계 및 예측 : 판매채널별(2021-2034년)

- 주요 동향

- OEM

- 애프터마켓

제9장 시장추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

제10장 기업 프로파일

- Chief Enterprises

- CHINT Automotive

- Denso

- FIAMM Technologies

- Grote Industries

- HELLA

- Imasen Electric Industrial

- Jindong Electronic Technology

- Johnson Electric

- MARUKO KEIHOKI

- MITSUBA

- Miyamoto Electric Horn

- Nidec

- Oriental Motor

- Panasonic

- Robert Bosch

- Roots Industries India Limited

- SEGER Horns

- UNO Minda

- Wolo Manufacturing

The Global Electric Motor Horn Market was valued at USD 3.7 billion in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 5.8 billion by 2034. This steady growth is fueled by the increasing adoption of Electric Vehicles (EVs), which have generated a surge in demand for electric motor horns. EVs, which operate quietly compared to traditional internal combustion engine (ICE) vehicles, require efficient, low-noise warning systems to meet safety standards. As a result, audible alert systems have become critical for pedestrian and road safety. Alongside the growing adoption of EVs, rising regulations on noise pollution and sound emission standards are pushing manufacturers to innovate and produce horns that are not only effective but also compliant with government mandates.

The global market is witnessing a shift as emerging economies enforce stricter road safety laws. This trend is driving the demand for regulated, low-decibel electric horns designed specifically for EVs. Manufacturers are under increasing pressure to develop energy-efficient, compact horn systems suitable for electric and hybrid vehicles, which meet both safety and environmental requirements. With a rising focus on sustainability, reducing power consumption while maintaining optimal sound levels has become a key challenge and innovation area for the industry.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.7 Billion |

| Forecast Value | $5.8 Billion |

| CAGR | 5.2% |

In 2024, the flat-type electric motor horns segment accounted for 50% of the market share. These horns are favored for their compact, space-saving design, robustness, and cost-efficiency, making them the preferred choice for motorcycles, passenger cars, and light commercial vehicles. Their versatility and ease of integration ensure their continued dominance in the market, both among original equipment manufacturers (OEMs) and aftermarket suppliers.

The passenger vehicle segment held a 54% share of the market in 2024 and is expected to grow steadily at a 5% CAGR between 2025 and 2034. This growth is driven by the increasing popularity of passenger cars in emerging markets such as India and China. Rising urbanization, disposable income, and vehicle ownership in these regions fuel the demand for reliable and affordable safety features. The demand for electric motor horns in passenger vehicles continues to surpass that of commercial vehicles and two-wheelers, solidifying its position as the largest consumer segment.

China electric motor horn market generated USD 756 million in 2024, accounting for 47% of the global market share. This dominance is attributed to high automotive production volumes, widespread EV adoption, and government-backed road safety mandates. Cost-sensitive consumers are driving the local demand for durable, advanced horn systems. Additionally, the increasing vehicle ownership rate is spurring aftermarket growth, with intelligent low-noise horn solutions further boosting demand.

Key players in the Global Electric Motor Horn Market include HELLA, Panasonic, Johnson Electric, Denso, UNO Minda, MITSUBA, Imasen Electric Industrial, Robert Bosch, Nidec, and FIAMM Technologies. To maintain a competitive edge, companies are investing in research and development to create compact, low-energy horns with customizable sound levels that adhere to international regulations. Strategic partnerships with EV automakers, expanding operations into high-growth emerging markets, and the development of smart horn systems integrated with vehicle electronics are key strategies for growth. Manufacturers are also enhancing local production capacities to optimize pricing strategies and meet the increasing demand for replacement parts through aftermarket distribution channels.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Component manufacturers

- 3.2.3 Electric motor horn manufacturers

- 3.2.4 Original equipment manufacturers (OEMs) and tier 1 suppliers

- 3.2.5 Aftermarket distributors and retailers

- 3.3 Impact of Trump administration tariffs

- 3.3.1 Impact on trade

- 3.3.1.1 Trade volume disruptions

- 3.3.1.2 Retaliatory measures

- 3.3.2 Impact on the Industry

- 3.3.2.1 Price volatility in key materials

- 3.3.2.1.1 Supply chain restructuring

- 3.3.2.1.2 Price transmission to end markets

- 3.3.2.1 Price volatility in key materials

- 3.3.3 Strategic industry responses

- 3.3.3.1 Supply chain reconfiguration

- 3.3.3.2 Pricing and product strategies

- 3.3.1 Impact on trade

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 The rise in global automobile production

- 3.9.1.2 Governments worldwide are mandating vehicle safety standards

- 3.9.1.3 Growing demand for electric vehicles (EVs)

- 3.9.1.4 Technological advancements in electric motor horns

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 Stringent noise pollution regulations

- 3.9.2.2 Increasing adoption of ADAS & autonomous vehicles

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Flat type horn

- 5.3 Spiral type horn

- 5.4 Trumpet

Chapter 6 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Passenger vehicles

- 6.2.1 Hatchback

- 6.2.2 Sedan

- 6.2.3 SUV

- 6.3 Two-Wheelers

- 6.4 Commercial vehicles

- 6.4.1 Light Commercial Vehicles (LCV)

- 6.4.2 Medium Commercial Vehicle (MCV)

- 6.4.3 Heavy Commercial Vehicles (HCV)

Chapter 7 Market Estimates & Forecast, By Sound Pressure, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Up to 110 dB

- 7.3 110 dB to 118 dB

- 7.4 Greater than 118 dB

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Chief Enterprises

- 10.2 CHINT Automotive

- 10.3 Denso

- 10.4 FIAMM Technologies

- 10.5 Grote Industries

- 10.6 HELLA

- 10.7 Imasen Electric Industrial

- 10.8 Jindong Electronic Technology

- 10.9 Johnson Electric

- 10.10 MARUKO KEIHOKI

- 10.11 MITSUBA

- 10.12 Miyamoto Electric Horn

- 10.13 Nidec

- 10.14 Oriental Motor

- 10.15 Panasonic

- 10.16 Robert Bosch

- 10.17 Roots Industries India Limited

- 10.18 SEGER Horns

- 10.19 UNO Minda

- 10.20 Wolo Manufacturing