|

시장보고서

상품코드

1721625

빌딩 자동화를 위한 에너지 수확 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Building Automation Energy Harvesting Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

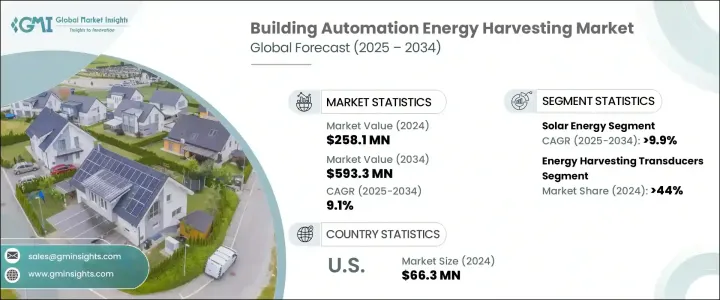

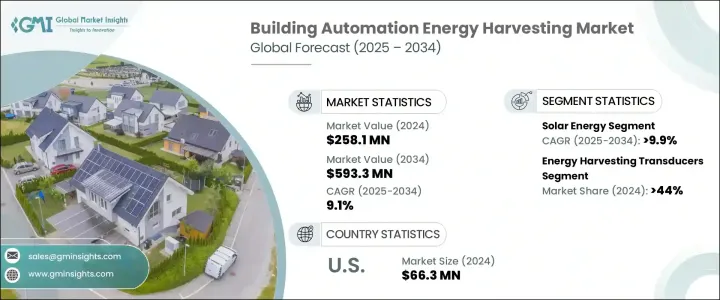

세계의 빌딩 자동화를 위한 에너지 수확 시장은 2024년 2억 5,810만 달러로 평가되었고, CAGR 9.1%로 성장할 전망이며, 2034년에는 5억 9,330만 달러에 이를 것으로 예측됩니다. 이 현저한 성장 궤도는 주택과 상업 환경 모두에서 지능형 에너지 시스템으로의 전환이 확산되고 있음을 반영하고 있습니다. 지속 가능성이 각 업계의 중심이 됨에 따라 빌딩 사업자, 시설 관리자, 개발자는, 운용 비용을 낮추면서 에너지 효율을 높이는 자동화 기술의 채용을 늘리고 있습니다. HVAC 시스템에서 조명, 고도의 시큐러티 네트워크에 이르기까지, 자동화는 최신의 빌딩 설계에 불가결한 것이 되고 있습니다. 이 변혁은 제로 에미션 구조의 세계 추진, 에너지 사용에 관한 정부의 엄격한 의무화, 기존 에너지원의 비용 상승에 의해 더욱 박차를 가하고 있습니다. 소비자도 기업도 마찬가지로, 환경 친화적인 주거 환경이나 직장 환경을 우선으로 하고 있어, 외부 에너지 그리드에 대한 의존을 최소한으로 억제하는 에너지 하베스팅 솔루션에 대한 왕성한 수요를 낳고 있습니다. 더불어 사물인터넷(IoT)과 AI 대응 플랫폼의 보급 확대로 자동화 기술의 원활한 통합이라는 새로운 기회가 생겨나 보다 스마트하고 응답성 높은 인프라로의 길이 열렸습니다.

에너지 효율이 세계적으로 중요한 관심사가 됨에 따라 조명, HVAC, 주방 기기, 보안 유닛 등의 자동화 시스템이 지속적으로 증가하고 있습니다. 빌딩은 기존의 에너지원에 대한 의존을 줄이고 전체적인 운용 관리를 개선하는 고도의 제어 시스템을 갖추고 있습니다. 배출량 삭감과 건물 효율 향상에 초점을 맞춘 규제의 틀이 건설업자나 부동산 소유자에게 스마트 기술의 채택을 재촉하고 있습니다. 에너지 하베스팅은 장기적으로 대폭적인 에너지 절약을 실현하면서 이러한 규제에 대한 컴플라이언스를 확보하기 위한 중요한 요소로 부상하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 2억 5,810만 달러 |

| 예측 금액 | 5억 9,330만 달러 |

| CAGR | 9.1% |

태양에너지는 지능형 건물로의 전환에 여전히 압도적인 힘을 가지고 있으며, 그 분야는 2034년까지 연평균 복합 성장률(CAGR) 9.9%를 보일 것으로 예측되고 있습니다. 기후에 대한 우려의 고조와 자급자족 전력 시스템에 대한 수요의 고조가 빌딩 분야에서의 태양광 발전의 채용을 가속화하고 있습니다. 솔라 기술은 빌딩 오토메이션 플랫폼과 쉽게 통합할 수 있으며 난방, 냉방, 조명 등의 중요한 기능에 청정 에너지를 공급합니다. 이를 통해 전기세가 절감될 뿐만 아니라 부동산 소유자와 개발업자에게 에너지 자립과 환경에 대한 책임이 강화됩니다.

컴포넌트에서 에너지 수확 트랜스듀서는 2024년 시장 점유율의 44%를 차지했습니다. 이러한 장치는 무선 셀프 파워 센서 네트워크를 지원하여 배터리 교체 및 복잡한 배선의 필요성을 제거합니다. 조명, 온도 제어, 거주 감지, 보안 시스템에 응용함으로써 에너지 관리의 합리화와 지속 가능한 운영이 가능해집니다. 스마트 빌딩의 기반 요소로서 트랜스듀서는 최소한의 유지보수로 확장 가능한 에너지 제어를 제공하고 효율적인 빌딩 업그레이드를 지원합니다.

아시아태평양 빌딩 자동화를 위한 에너지 수확 시장은 급속한 도시화와 건설 활동 증가로 2024년에는 24%의 점유율을 차지했습니다. 이 지역의 나라들은, 진화하는 지속 가능성의 목표에 따르기 위해, 에너지 수집 자동화에 지탱된 그린 빌딩의 실천을 채용하고 있습니다. 정부 주도의 대처 및 스마트 부동산 솔루션에 대한 수요의 증대가 지역 시장의 확대를 더욱 가속화시키고 있습니다.

주요 기업은 ZF Friedrichshafen AG, Perpetua Power, Advanced Linear Devices, Inc., EnOcean GmbH, Texas Instruments Incorporated, Renesas Electronics Corporation, Cedrat Technologies, STMicroelectronics, Mide Technology Corp., Laird Connectivity, ABB, Honeywell, Kinergizer, Fujitsu, Mouser Electronics, and Powercast Corporation 등이 있습니다. 주요 기업은 트랜스듀서와 PMIC의 성능과 통합을 강화하기 위해 연구 개발에 많은 투자를 실시했습니다. 전략적 제휴는 세계적인 존재를 확대하는 데 도움이 됩니다. 또한 혁신 및 신축을 위해 맞춤화된 맞춤형 IoT 기반 솔루션이 인기를 끌고 자동화 기능을 강화하고 장기적인 시장 성장을 가속하고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 규제 상황

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 트럼프 정권의 관세가 무역 및 산업 전체에 미치는 영향

- 성장 가능성 분석

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 전략적 전망

- 혁신 및 지속가능성의 정세

제5장 시장 규모 및 예측 : 소스별(2021-2034년)

- 주요 동향

- 태양에너지

- 진동 및 운동 에너지

- 열에너지

- 무선 주파수(RF)

- 기타

제6장 시장 규모 및 예측 : 컴포넌트별(2021-2034년)

- 주요 동향

- 에너지 수확 트랜스듀서

- 전원 관리 집적 회로(PMIC)

- 기타

제7장 시장 규모 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 프랑스

- 영국

- 스페인

- 이탈리아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 라틴아메리카

- 브라질

- 아르헨티나

제8장 기업 프로파일

- ABB

- Advanced Linear Devices, Inc.

- Cedrat technologies

- EnOcean GmbH

- Fujitsu

- Honeywell

- Kinergizer

- Laird Connectivity

- Mide Technology Corp.

- Mouser Electronics

- Perpetua Power

- Powercast Corporation

- Renesas Electronics Corporation

- STMicroelectronics

- Texas Instruments Incorporated

- ZF Friedrichshafen AG

The Global Building Automation Energy Harvesting Market was valued at USD 258.1 million in 2024 and is estimated to grow at a CAGR of 9.1% to reach USD 593.3 million by 2034. This remarkable growth trajectory reflects a widespread shift toward intelligent energy systems across both residential and commercial environments. As sustainability takes center stage across industries, building operators, facility managers, and developers are increasingly adopting automation technologies that drive energy efficiency while lowering operational costs. From HVAC systems to lighting and advanced security networks, automation is becoming integral to modern building design. This transformation is further fueled by the global push for zero-emission structures, stringent government mandates on energy usage, and the rising costs of conventional energy sources. Consumers and businesses alike are prioritizing eco-friendly living and working environments, creating robust demand for energy harvesting solutions that minimize reliance on external energy grids. In addition, the growing penetration of the Internet of Things (IoT) and AI-enabled platforms has unlocked new opportunities for seamless integration of automation technologies, paving the way for smarter, more responsive infrastructure.

As energy efficiency becomes a critical global concern, automated systems for lighting, HVAC, kitchen appliances, and security units continue to gain ground. Buildings are equipped with advanced control systems that reduce dependence on traditional energy sources and improve overall operational management. Regulatory frameworks focused on reducing emissions and increasing building efficiency are prompting builders and property owners to embrace smart technologies. Energy harvesting is emerging as a key component in ensuring compliance with these regulations while delivering significant long-term energy savings.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $258.1 million |

| Forecast Value | $593.3 million |

| CAGR | 9.1% |

Solar energy remains a dominant force in the transition toward intelligent buildings, with its segment projected to grow at a CAGR of 9.9% through 2034. Growing climate concerns and the rising demand for self-sufficient power systems are accelerating solar adoption in the building sector. Solar technologies integrate easily with building automation platforms, providing clean energy to power critical functions such as heating, cooling, and lighting. This not only reduces electricity bills but also enhances energy independence and environmental responsibility for property owners and developers.

In terms of components, energy-harvesting transducers accounted for 44% of the market share in 2024. These devices support wireless and self-powered sensor networks, eliminating the need for battery changes or complex wiring. Their application in lighting, temperature control, occupancy sensing, and security systems ensures streamlined energy management and sustainable operations. As a foundational element of smart building infrastructure, transducers offer scalable energy control with minimal maintenance, supporting efficient building upgrades.

The Asia Pacific Building Automation Energy Harvesting Market held a 24% share in 2024, driven by rapid urbanization and increasing construction activity. Nations across the region are adopting green building practices supported by energy-harvesting automation to align with evolving sustainability goals. Government-led initiatives and rising demand for smart real estate solutions are further accelerating regional market expansion.

Key players include ZF Friedrichshafen AG, Perpetua Power, Advanced Linear Devices, Inc., EnOcean GmbH, Texas Instruments Incorporated, Renesas Electronics Corporation, Cedrat Technologies, STMicroelectronics, Mide Technology Corp., Laird Connectivity, ABB, Honeywell, Kinergizer, Fujitsu, Mouser Electronics, and Powercast Corporation. Leading companies are investing heavily in R&D to enhance transducer and PMIC performance and integration. Strategic alliances with automation developers, infrastructure projects, and public programs are helping broaden their global presence. Additionally, custom IoT-based solutions tailored for retrofitting and new builds are gaining traction, enhancing automation capabilities and driving long-term market growth.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Regulatory landscape

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.2 Industry pitfalls & challenges

- 3.4 Impact of Trump administration tariffs on trade & overall industry

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Source, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Solar energy

- 5.3 Vibration & kinetic energy

- 5.4 Thermal energy

- 5.5 Radio Frequency (RF)

- 5.6 Others

Chapter 6 Market Size and Forecast, By Component, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Energy harvesting transducer

- 6.3 Power Management Integrated Circuits (PMIC)

- 6.4 Others

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 France

- 7.3.3 UK

- 7.3.4 Spain

- 7.3.5 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 Australia

- 7.4.5 South Korea

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 South Africa

- 7.5.3 UAE

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 ABB

- 8.2 Advanced Linear Devices, Inc.

- 8.3 Cedrat technologies

- 8.4 EnOcean GmbH

- 8.5 Fujitsu

- 8.6 Honeywell

- 8.7 Kinergizer

- 8.8 Laird Connectivity

- 8.9 Mide Technology Corp.

- 8.10 Mouser Electronics

- 8.11 Perpetua Power

- 8.12 Powercast Corporation

- 8.13 Renesas Electronics Corporation

- 8.14 STMicroelectronics

- 8.15 Texas Instruments Incorporated

- 8.16 ZF Friedrichshafen AG