|

시장보고서

상품코드

1721631

산업용 전기자동차 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Industrial Electric Vehicle Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

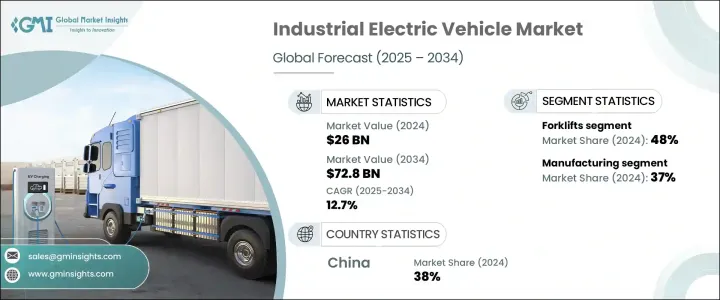

세계의 산업용 전기자동차 시장 규모는 2024년에 260억 달러로 평가되었고, CAGR 12.7%로 성장할 전망이며, 2034년에는 728억 달러에 이를 것으로 예측되고 있습니다. 이 기세는, 환경 의식의 고조, 규제 의무화, EV 친화적인 산업 서비스 센터 등의 서포트 인프라의 진화에 기인합니다. 이산화탄소 배출량 및 운전 비용 절감이 시급해짐에 따라 전기차는 기존 내연 엔진을 대체할 수 있는 실행 가능한 선택지로 자리매김하고 있습니다. 기업은 현재, 환경 목표에 따르기 위해서만이 아니라, 장기적인 비용 효율을 활용하기 위해서도, 물류 및 창고 업무의 전동화를 우선하고 있습니다. 산업 프로세스의 디지털화가 진행됨에 따라 조용하고 배기가스가 없으며, 자동화에 대응한 차량에 대한 수요가 세계 시장에서 가속화되고 있습니다. 배터리 기술의 진보 및 비용 저하로, 전기 자동차 채용의 케이스는 한층 더 강화되어, 기업은 성능이나 확장성을 해치지 않고 이행하기 쉬워지고 있습니다.

차량 유형 중에서 지게차가 2024년에 48%로 가장 큰 시장 점유율을 차지했으며, 2034년까지 13% 이상의 CAGR로 확대될 것으로 예측됩니다. 현대적인 창고 관리 및 제조 기준에 적합한 스마트하고 저배출 가스인 머티리얼 핸들링 솔루션의 필요성으로 인해 지게차의 용도는 업계 전체에서 급속히 확대되고 있습니다. 용도 측면에서는 제조 부문이 2024년 37%의 점유율로 시장을 선도하였으며, 예측 기간 동안 13% 이상의 CAGR로 성장할 것으로 예측됩니다. 이러한 성장은 청정 생산 의무화, 배출 규제 강화, 스마트 공장의 생태계와 원활하게 통합할 수 있는 에너지 효율이 높은 차량군에 대한 수요 증가로 형성되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 260억 달러 |

| 예측 금액 | 728억 달러 |

| CAGR | 12.7% |

추진력별로는 에너지 효율이 높고 총소유비용이 낮고 화석연료에 대한 의존도가 0인 배터리 전기자동차(BEV)가 계속 시장을 독점하고 있습니다. 이러한 차량은 조용한 운전과 최소한의 유지보수를 제공하여 실내 및 밀폐된 산업 환경에 이상적입니다. 또한 자동화도 용이하기 때문에 인더스트리 4.0 대응 업무에 점점 더 적합합니다. 정부의 인센티브 및 배출가스 관련 규제도 다양한 산업 영역에서 BEV를 선호하는 선택지로 삼고 있습니다.

지역별로 중국은 2024년 아시아태평양 산업용 전기자동차 시장을 선도하여 약 38%의 점유율을 획득하여 약 45억 달러의 수익을 올렸습니다. 이 나라의 강력한 산업 기반, 클린 에너지 이행에 대한 정부의 적극적인 지원, 고도의 EV 제조 능력이, 이 나라를 주요한 시장 기업으로서 평가하고 있습니다. 창고업의 급속한 자동화 및 적극적인 전철화 목표가 지속적으로 지역 수요를 견인하고 있으며, 스마트공장 인프라를 추진하는 이니셔티브로 더욱 강화되고 있습니다.

세계 시장의 주요 기업으로는 Hangcha Forklift, Hyundai Construction Equipment, Hyster-Yale Materials Handling, Jungheinrich AG, KION Group, Manitou, Komatsu, MITSUBISHI LOGISNEXT, Sany Electric, and Toyota가 포함됩니다. 이 회사는 모듈형 전기자동차 설계에 많은 투자를 하고 배터리 효율 연구 개발을 확대하며 실시간 진단을 위해 IoT 및 텔레매틱스를 통합하고 있습니다. 이 기업의 전략적 노력은 선진국과 신흥 경제 국가를 불문하고 시장 개척과 고객 지원을 강화하기 위해 현지 생산과 애프터 서비스 거점의 확대에도 관여하고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 원재료 공급자

- 컴포넌트 제공업체

- 제조업자

- 리셀러

- 최종 용도

- 트럼프 정권의 관세

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 생산 비용에 미치는 영향

- 이익률 분석

- 기술 및 혁신의 상황

- 특허 분석

- 주요 뉴스 및 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 전기자동차에 관한 정부의 대처 증가

- 배터리 구동 지게차 수요 증가

- 전기 기술의 진보

- 산업 차량 제조업 수요 증가

- 업계의 잠재적 위험 및 과제

- 산업용 전기자동차의 높은 초기 비용

- 배터리 제한 및 다운타임

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추계 및 예측 : 차량별(2021-2034년)

- 주요 동향

- 견인 트랙터

- 지게차

- 컨테이너 핸들러

- 통로 트럭

- 기타

제6장 시장 추계 및 예측 : 추진력별(2021-2034년)

- 주요 동향

- 배터리 전기자동차(BEV)

- 플러그인 하이브리드 전기자동차(PHEV)

- 하이브리드 전기자동차(HEV)

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 제조업

- 창고

- 화물 및 물류

- 기타

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

제9장 기업 프로파일

- Aisle Master

- Alke

- Anhui Heli

- Aprolis

- CLARK

- Crown Equipment

- Doosan Industrial Vehicle

- EP Equipment

- Hangcha Forklift

- Hyster-Yale Materials Handling

- Hyundai Construction Equipment

- Jungheinrich AG

- Kalmar Global

- KION Group

- Komatsu

- Manitou

- Mitsubishi Logisnext

- Motrec International

- Sany Electric

- Toyota Material Handling

The Global Industrial Electric Vehicle Market was valued at USD 26 billion in 2024 and is estimated to grow at a CAGR of 12.7% to reach USD 72.8 billion by 2034. This momentum stems from rising environmental awareness, regulatory mandates, and the evolution of support infrastructure such as EV-friendly industrial service centers. The growing urgency to reduce carbon emissions and operating costs has positioned electric vehicles as a viable alternative to traditional internal combustion engines. Businesses are now prioritizing electrification in logistics and warehouse operations not only to align with eco-goals but also to leverage long-term cost efficiencies. As industrial processes undergo digital transformation, the demand for quiet, emission-free, and automation-compatible vehicles is accelerating across global markets. Advancements in battery technologies and falling costs have further strengthened the case for electric adoption, making it easier for businesses to transition without compromising performance or scalability.

Among vehicle types, forklifts held the largest market share at 48% in 2024 and are expected to expand at a CAGR of over 13% through 2034. Their application across industries is growing rapidly, driven by the need for smart, low-emission material handling solutions that align with modern warehousing and manufacturing standards. On the application front, the manufacturing segment led the market with a 37% share in 2024 and is projected to grow at over 13% CAGR through the forecast period. This growth is being shaped by cleaner production mandates, tighter emissions regulations, and the growing demand for energy-efficient vehicle fleets that can seamlessly integrate with smart factory ecosystems.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $26 Billion |

| Forecast Value | $72.8 Billion |

| CAGR | 12.7% |

By propulsion, Battery Electric Vehicles (BEVs) continue to dominate the market, supported by their high energy efficiency, lower total cost of ownership, and zero dependence on fossil fuels. These vehicles offer quiet operation and minimal maintenance and are ideal for indoor and enclosed industrial environments. They are also easier to automate, making them increasingly suitable for Industry 4.0-enabled operations. Government incentives and emission-related regulations are also making BEVs the preferred option across various industrial domains.

Regionally, China led the Asia Pacific industrial electric vehicle market in 2024, capturing around 38% share and generating nearly USD 4.5 billion in revenue. The country's strong industrial base, proactive government support for clean energy transitions, and advanced EV manufacturing capabilities have positioned it as a key market player. Rapid automation in warehousing and aggressive electrification goals continue to drive regional demand, further strengthened by initiatives that promote smart factory infrastructure.

Key players in the global market include Hangcha Forklift, Hyundai Construction Equipment, Hyster-Yale Materials Handling, Jungheinrich AG, KION Group, Manitou, Komatsu, MITSUBISHI LOGISNEXT, Sany Electric, and Toyota. These companies are heavily investing in modular electric vehicle designs, expanding R&D in battery efficiency, and integrating IoT and telematics for real-time diagnostics. Their strategic efforts also involve expanding local production and aftersales service hubs to enhance market reach and customer support across both developed and emerging economies.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material providers

- 3.2.2 Component providers

- 3.2.3 Manufacturers

- 3.2.4 Distributors

- 3.2.5 End use

- 3.3 Trump administration tariffs

- 3.3.1 Supply-side impact (Raw Materials)

- 3.3.2 Price volatility in key materials

- 3.3.3 Production cost implications

- 3.4 Profit margin analysis

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rise in government initiatives for electric vehicles

- 3.9.1.2 Increasing demand for battery-operated forklift

- 3.9.1.3 Technology advancement in electric technology

- 3.9.1.4 Increasing demand for industrial vehicle form manufacturing industry

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High initial costs of industrial electric vehicles

- 3.9.2.2 Battery limitations and downtime

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter’s analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Tow tractors

- 5.3 Forklifts

- 5.4 Container handlers

- 5.5 Aisle trucks

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Battery Electric Vehicles (BEV)

- 6.3 Plug-in Hybrid Electric Vehicles (PHEV)

- 6.4 Hybrid Electric Vehicles (HEV)

Chapter 7 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 Manufacturing

- 7.3 Warehousing

- 7.4 Freight & logistics

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 UK

- 8.3.2 Germany

- 8.3.3 France

- 8.3.4 Italy

- 8.3.5 Spain

- 8.3.6 Russia

- 8.3.7 Nordics

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 South Korea

- 8.4.5 ANZ

- 8.4.6 Southeast Asia

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 UAE

- 8.6.2 Saudi Arabia

- 8.6.3 South Africa

Chapter 9 Company Profiles

- 9.1 Aisle Master

- 9.2 Alke

- 9.3 Anhui Heli

- 9.4 Aprolis

- 9.5 CLARK

- 9.6 Crown Equipment

- 9.7 Doosan Industrial Vehicle

- 9.8 EP Equipment

- 9.9 Hangcha Forklift

- 9.10 Hyster-Yale Materials Handling

- 9.11 Hyundai Construction Equipment

- 9.12 Jungheinrich AG

- 9.13 Kalmar Global

- 9.14 KION Group

- 9.15 Komatsu

- 9.16 Manitou

- 9.17 Mitsubishi Logisnext

- 9.18 Motrec International

- 9.19 Sany Electric

- 9.20 Toyota Material Handling