|

시장보고서

상품코드

1740949

압연 또는 압출 알루미늄 로드, 바 및 와이어 시장 : 기회, 성장 요인, 산업 동향 분석 및 예측(2025-2034년)Rolled or Extruded Aluminum Rods, Bars, and Wires Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

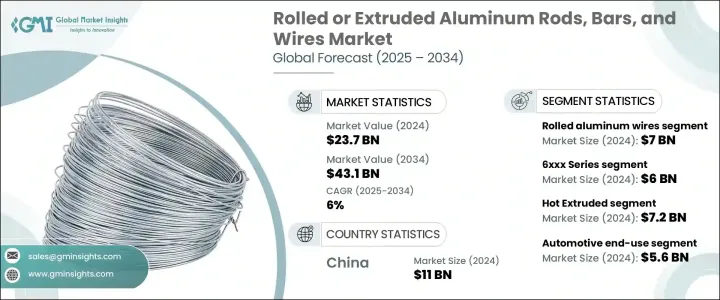

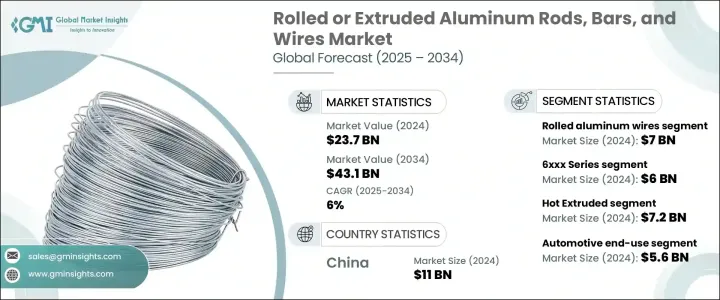

세계의 압연 또는 압출 알루미늄 로드, 바 및 와이어 시장은 2024년에 237억 달러로 평가되었으며, 산업용도의 급증과 고성장 분야 수요 증가로 2034년에는 431억 달러에 이를 것으로 추정되며, CAGR 6%로 성장할 전망입니다.

이러한 상승세는 알루미늄의 다용도성, 중량 대비 강도, 재활용성 덕분에 다양한 분야에서 알루미늄이 중요한 역할을 하고 있음을 반영합니다. 에너지 효율적인 제조에 대한 요구와 글로벌 산업화의 증가는 다양한 분야에서 알루미늄 제품의 사용을 촉진했습니다. 알루미늄과 같은 경량 소재는 내구성, 효율성, 에너지 소비 감소가 핵심 요건인 분야에서 특히 인기가 높습니다. 또한, 기술 발전으로 생산 공정이 간소화되면서 제조업체는 품질이나 비용 효율성을 저하시키지 않으면서도 증가하는 수요를 충족할 수 있는 역량을 갖추게 되었습니다. 알루미늄 로드, 바, 와이어 제조에 자동화 및 디지털 통합이 널리 보급되면서 생산 속도가 향상되고 자재 낭비가 최소화되고 있습니다. 이러한 혁신은 공급망 전반에서 물량 확장성과 품질 일관성을 모두 지원하는 데 필수적인 것으로 입증되고 있습니다.

2025년 기준, 이 시장은 257억 달러에서 10년 동안 견조한 성장세를 유지하며 성장할 것으로 예상됩니다. 이러한 성장의 가장 큰 요인 중 하나는 성능 향상과 운영 비용 절감을 가능하게 하는 경량 금속 부품에 대한 선호도가 높아지고 있다는 점입니다. 산업계에서는 알루미늄 제품이 제공하는 이점에 맞춰 지속가능성과 재활용성을 점점 더 우선시하고 있습니다. 과도한 무게를 추가하지 않으면서 내구성과 내식성을 갖춘 소재를 필요로 하는 부문의 구조적 변화로 인해 수요가 더욱 촉진되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 237억 달러 |

| 예측 금액 | 431억 달러 |

| CAGR | 6% |

보다 광범위한 시장에서 압연 알루미늄 라인 부문은 2024년 70억 달러로 평가되었으며, 2025년과 2034년 사이에 CAGR 5.8%를 보일 것으로 예측됩니다. 다양한 환경 조건에서 가단성과 일관된 성능으로 인해 다양한 용도에서 필수적인 역할을 합니다. 이러한 특성으로 인해 압연 알루미늄 와이어는 유연성과 내구성이 모두 필요한 산업용 용도에서 선호되는 선택입니다.

압연 알루미늄 로드 부문은 높은 정밀도와 기계적 강도가 필수적인 기계 및 운송 시스템과의 관련성 덕분에 강력한 경쟁 우위를 유지하고 있습니다. 이 부문은 특정 응용 분야에서 저가 대체재와의 적당한 경쟁에 직면해 있지만, 안정적인 원자재 가용성과 압연 공장 운영의 기술 발전으로 계속 혜택을 누리고 있습니다.

다양한 합금 등급 중 6xxx 시리즈 부문은 2024년 최대 규모로 부상하여 시장 매출으로 60억 달러에 기여합니다.

가공 방법 측면에서 열간 압출 부문은 2024년 72억 달러 규모를 차지했으며 2034년까지 6.5%의 연평균 성장률을 보일 것으로 예상됩니다. 이 방법은 균일한 치수의 고강도 부품을 생산할 수 있다는 점에서 선호됩니다. 또한 열간 압연 기술은 재료 유연성, 비용 효율성, 상대적으로 낮은 에너지 요구 사항으로 인해 대량 생산에 비용 효율적인 솔루션으로 각광받고 있습니다.

최종 용도의 관점에서 보면 2024년에는 자동차 부문에서만 56억 달러가 시장에 기여해 24%의 점유율을 획득했습니다. 이 부문은 2025년에서 2034년 사이에 5.7%의 연평균 성장률로 성장할 것으로 예상됩니다. 자동차 제조에서 연비와 지속가능성에 대한 요구가 증가함에 따라 프레임, 차체 패널 및 구조 보강재의 핵심 부품인 알루미늄과 같은 경량 및 고강도 소재에 대한 수요가 증가하고 있습니다.

지역별로는 중국이 2024년에 110억 달러로 평가되었으며, 시장을 선도해 2025년부터 2034년까지 연평균 성장률(CAGR) 5.9%로 확대될 것으로 예측됩니다. 세계 최고 알루미늄 생산국인 중국은 2024년에는 세계의 알루미늄 생산량의 절반 이상을 차지했으며, 생산량은 4,400만 톤에 달했습니다. 알루미늄 산업에서 중국의 강력한 입지는 탄탄한 제조 기반과 인프라 개발 및 에너지 전환 노력을 촉진하는 지원 정책 프레임워크에 의해 뒷받침되고 있습니다. 생산 및 소비 강국으로서의 중국의 역할은 첨단 제조 역량과 전략적 경제 계획에 힘입어 여전히 글로벌 알루미늄 시장의 핵심 동력으로 남아 있습니다.

이동식 콘크리트 배치 플랜트 산업의 몇몇 주요 업체들은 최근 몇 년 동안 시장 입지를 강화하고 혁신을 추진하기 위해 중요한 전략적 움직임을 보였습니다. 선도적인 기업들은 진화하는 규제 기준을 충족하는 에너지 효율적이고 친환경적인 첨단 배치 솔루션을 도입하기 위해 연구 개발에 적극적으로 투자하고 있습니다. 이러한 기업 중 다수는 제품 혁신과 함께 유통 역량을 개선하고 새로운 고객층에 접근하기 위한 인수합병 및 전략적 파트너십을 통해 글로벌 입지를 확장하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 혁신

- 장래의 전망

- 제조업자

- 리셀러

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원자재)

- 주요 원자재의 가격 변동

- 공급 체인 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원자재)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 무역 통계(HS코드)

- 주요 수출국

- 주요 수입국

- 이익률 분석

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 자동차 산업에서 경량 소재에 대한 수요 증가

- 지속 가능한 인프라를 향한 정부의 대처

- 항공우주 및 방위 부문의 성장

- 소비자 가전 수요 확대

- 업계의 잠재적 위험 및 과제

- 원자재 가격 변동

- 알루미늄 생산의 환경 영향

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추계 및 예측 : 유형별(2021-2034년)

- 주요 동향

- 평판 롤 시트

- 압연 알루미늄 로드

- 압출 알루미늄 로드

- 알루미늄 로드

- 알루미늄 와이어

제6장 시장 추계 및 예측 : 합금 유형별(2021-2034년)

- 주요 동향

- 1xxx 시리즈

- 2xxx 시리즈

- 3xxx 시리즈

- 5xxx 시리즈

- 6xxx 시리즈

- 7xxx 시리즈

- 8xxx 시리즈

제7장 시장 추계 및 예측 : 가공 방법별(2021-2034년)

- 주요 동향

- 열간 압연

- 냉간 압연

- 열간 압출

- 냉간 압출

제8장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 자동차

- 항공우주

- 공사

- 전기 및 전자

- 기계

- 기타

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Hydro Aluminium

- Alcoa Corporation

- China Zhongwang Holdings Limited

- Rusal(UC Rusal)

- Chalco(Aluminum Corporation of China)

- Kaiser Aluminum Corporation

- Norsk Hydro ASA

- Constellium SE

- Novelis Inc.

- Bonnell Aluminum

- UACJ Corporation

- Southwire Company, LLC

- Jiangsu Dingsheng New Material

- Sapa Group(now part of Hydro)

- Vedanta Aluminium

The Global Rolled Or Extruded Aluminum Rods, Bars, And Wires Market was valued at USD 23.7 billion in 2024 and is estimated to grow at a CAGR of 6% to reach USD 43.1 billion by 2034, driven by a surge in industrial applications and increasing demand from high-growth sectors. This upward trajectory reflects the critical role aluminum plays across various sectors, thanks to its versatility, strength-to-weight ratio, and recyclability. The push for energy-efficient manufacturing, coupled with rising global industrialization, has propelled the use of aluminum products in diverse applications. Lightweight materials like aluminum are particularly sought after in applications where durability, efficiency, and reduced energy consumption are key requirements. Moreover, with technological advancements streamlining production processes, manufacturers are better equipped to meet the growing demand without compromising on quality or cost-efficiency. Automation and digital integration are becoming widespread in the manufacturing of aluminum rods, bars, and wires, which in turn enhances production speed and minimizes material waste. These innovations are proving vital in supporting both volume scalability and quality consistency across the supply chain.

As of 2025, the market is forecasted to grow from USD 25.7 billion, maintaining a healthy pace throughout the decade. One of the largest contributors to this expansion is the rising preference for lightweight metal components, which allow for improved performance and lower operational costs. Industries are increasingly prioritizing sustainability and recyclability, aligning perfectly with the benefits offered by aluminum products. Demand is further fueled by structural shifts in sectors that require materials offering durability and corrosion resistance without adding excessive weight.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $23.7 Billion |

| Forecast Value | $43.1 billion |

| CAGR | 6% |

Within the broader market, the rolled aluminum wires segment was valued at USD 7 billion in 2024 and is anticipated to grow at a CAGR of 5.8% between 2025 and 2034. This segment plays an integral role in various applications due to its malleability and consistent performance under different environmental conditions. These features make rolled aluminum wires a preferred choice in industrial applications that require both flexibility and durability.

The rolled aluminum rods segment maintains strong competitive positioning, largely due to its relevance in machinery and transportation systems where high precision and mechanical strength are essential. Despite facing moderate competition from lower-cost substitutes in specific applications, this segment continues to benefit from stable raw material availability and technological advancements in rolling mill operations.

Among the different alloy grades, the 6xxx Series segment emerged as the largest in 2024, contributing USD 6 billion in market value. With a projected CAGR of 6.7% from 2025 to 2034, this series is favored for its excellent corrosion resistance, strength, and versatility, making it suitable for structural and architectural uses.

In terms of processing methods, the hot extruded segment accounted for USD 7.2 billion in 2024 and is expected to grow at a CAGR of 6.5% through 2034. This method is preferred for its ability to produce high-strength components with uniform dimensions. The hot rolling technique is also gaining traction due to its material flexibility, cost efficiency, and relatively low energy requirements, making it a cost-effective solution for mass production.

From an end-use perspective, the automotive sector alone contributed USD 5.6 billion to the market in 2024, capturing a 24% share. This segment is forecasted to expand at a CAGR of 5.7% between 2025 and 2034. The growing push for fuel efficiency and sustainability in vehicle manufacturing is steering demand toward lightweight and high-strength materials, such as aluminum, which serve as key components in frames, body panels, and structural reinforcements.

Geographically, China led the market with a valuation of USD 11 billion in 2024 and is expected to expand at a CAGR of 5.9% from 2025 to 2034. As the top global producer of aluminum, China accounted for over half of global aluminum output in 2024, with production reaching 44 million tons. Its strong foothold in the aluminum industry is underpinned by a robust manufacturing base and supportive policy frameworks that promote infrastructure development and energy transition efforts. China's role as a production and consumption powerhouse remains a key driver for the global aluminum market, backed by advanced manufacturing capabilities and strategic economic planning.

Several key players in the mobile concrete batch plant industry have made significant strategic moves in recent years to strengthen their market presence and drive innovation. Leading companies are actively investing in research and development to introduce advanced, energy-efficient, and eco-friendly batching solutions that meet evolving regulatory standards. Alongside product innovation, many of these firms have expanded their global footprint through mergers, acquisitions, and strategic partnerships aimed at improving distribution capabilities and accessing new customer segments.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufacturers

- 3.1.6 Distributors

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Trade statistics (HS code)

- 3.3.1 Major exporting countries

- 3.3.2 Major importing countries

- 3.4 Profit margin analysis

- 3.5 Key news & initiatives

- 3.6 Regulatory landscape

- 3.7 Impact forces

- 3.7.1 Growth drivers

- 3.7.1.1 Rising demand for lightweight materials in automotive industry

- 3.7.1.2 Government initiatives for sustainable infrastructure

- 3.7.1.3 Growth in aerospace and defense sector

- 3.7.1.4 Expanding demand in consumer electronics

- 3.7.2 Industry pitfalls & challenges

- 3.7.2.1 Fluctuating raw material prices

- 3.7.2.2 Environmental impact of aluminum production

- 3.7.1 Growth drivers

- 3.8 Growth potential analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.1.1 Flat rolled sheets

- 5.1.2 Rolled aluminum rods

- 5.1.3 Extruded aluminum rods

- 5.1.4 Aluminum bars

- 5.1.5 Aluminum wires

Chapter 6 Market Estimates & Forecast, By Alloy Type, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 1xxx series

- 6.3 2xxx series

- 6.4 3xxx series

- 6.5 5xxx series

- 6.6 6xxx series

- 6.7 7xxx series

- 6.8 8xxx series

Chapter 7 Market Estimates & Forecast, By Processing Method, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Hot rolled

- 7.3 Cold rolled

- 7.4 Hot extruded

- 7.5 Cold extruded

Chapter 8 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Automotive

- 8.3 Aerospace

- 8.4 Construction

- 8.5 Electrical & electronics

- 8.6 Machinery

- 8.7 Others

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Hydro Aluminium

- 10.2 Alcoa Corporation

- 10.3 China Zhongwang Holdings Limited

- 10.4 Rusal (UC Rusal)

- 10.5 Chalco (Aluminum Corporation of China)

- 10.6 Kaiser Aluminum Corporation

- 10.7 Norsk Hydro ASA

- 10.8 Constellium SE

- 10.9 Novelis Inc.

- 10.10 Bonnell Aluminum

- 10.11 UACJ Corporation

- 10.12 Southwire Company, LLC

- 10.13 Jiangsu Dingsheng New Material

- 10.14 Sapa Group (now part of Hydro)

- 10.15 Vedanta Aluminium