|

시장보고서

상품코드

1740974

극저온 공기 분리 장치 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Cryogenic Air Separation Unit Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

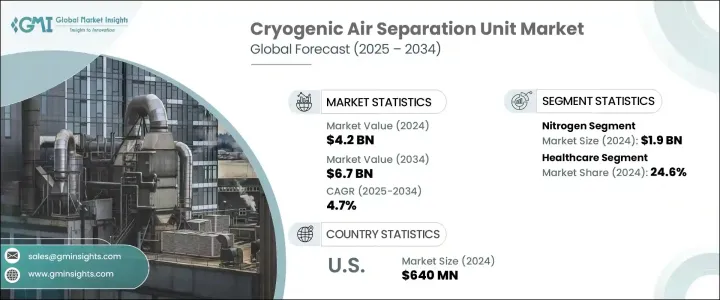

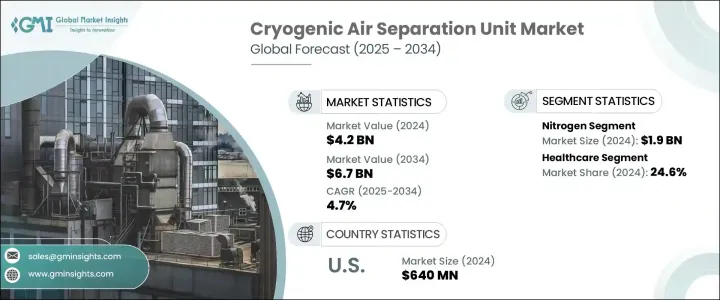

세계의 극저온 공기 분리 장치 시장은 2024년에는 42억 달러로 평가되었고 철강, 화학, 제조 등 다양한 분야에서 산소, 질소, 아르곤 등의 산업용 가스 수요 증가로 2034년에는 67억 달러에 달할 것으로 예측되며, CAGR 4.7%로 성장할 전망입니다.

특히 개발도상국을 중심으로 산업 활동이 확대되면서 이러한 가스에 대한 수요가 급증하여 공기 분리 기술에 대한 투자가 촉진되고 있습니다.

또한 코로나19 팬데믹은 전 세계 의료 시스템의 취약성, 특히 위기 상황에서 의료용 산소 부족 문제를 부각시켰습니다. 이러한 긴급 상황으로 인해 정부와 민간 의료 서비스 제공업체는 의료용 가스 인프라에 대한 투자 우선순위를 정했습니다. 그 결과 고순도 산소를 대규모로 생산할 수 있는 극저온 공기 분리 장치에 대한 수요가 급증했습니다. 병원과 응급 치료 시설은 산소 생산 능력을 업그레이드하기 시작했고, 이는 신규 설치와 개보수로 이어졌습니다. 이러한 추세는 즉각적인 위기 대응을 넘어, 특히 의료 접근성이 빠르게 확대되고 있는 신흥 시장에서 의료 회복력을 강화하기 위한 광범위한 노력의 일환으로 계속되고 있습니다. 이러한 변화는 또한 의료용 가스의 현지 생산을 장려하여 수입 의존도를 낮추고 지역 전반에 걸쳐 장기적인 공급 안정성을 보장했습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 42억 달러 |

| 예측 금액 | 67억 달러 |

| CAGR | 4.7% |

아르곤 부문은 정밀 산업 응용 분야에 필수적인 불활성 대기를 조성하는 데 필수적인 역할로 인해 2034년까지 14억 달러에 달할 것으로 예상됩니다. 제조 기술이 더욱 전문화됨에 따라 안정적이고 반응이 없는 환경에 대한 필요성이 더욱 커지고 있습니다. TIG 용접, 전자제품 제조, 레이저 절단, 특수 유리 및 태양광 패널 생산과 같은 공정에서 아르곤이 광범위하게 채택되고 있는 것은 아르곤의 중요성이 커지고 있음을 보여줍니다. 특히 태양광 기술의 확대와 같은 청정 에너지 전환은 고온 공정에서 재료를 오염으로부터 보호하는 데 필수적인 아르곤 수요의 주요 촉매제 역할을 하고 있습니다.

2024년 24.6%의 점유율을 차지할 의료 산업은 극저온 공기 분리 장치의 주요 최종 사용 부문으로 남아 있습니다. 병원, 진료소 및 장기 요양 센터는 현장에서 의료용 산소를 생성하기 위해 이러한 시스템에 점점 더 의존하고 있습니다. 인구 고령화와 만성 호흡기 질환이 전 세계적으로 의료 시스템에 더 큰 부담을 주면서 이러한 필요성은 더욱 절실해지고 있습니다. 이에 따라 의료 가스 인프라에 대한 투자가 증가하고 있으며, 특히 의료 접근성과 응급 상황 대비를 강화하고자 하는 지역에서 투자가 증가하고 있습니다.

미국의 극저온 공기 분리 장치 2024년 시장 규모는 6억 4,000만 달러에 이르렀습니다. 셰일가스 탐사 증가와 청정 수소 연료 솔루션에 대한 추진에 힘입어 북미의 산업 성장은 현지화된 고용량 ASU 설치에 대한 수요를 창출했습니다. 이러한 시설의 대부분은 운송보다 온사이트 가스 생산이 더 효율적인 외딴 지역이나 수요가 많은 지역에 있습니다. 또한 농업 및 제약 제조에서 질소 수요가 증가함에 따라 이 지역의 중요한 공급망을 지원하는 ASU의 역할이 강화되고 있습니다.

세계의 극저온 공기 분리 장치 시장의 주요 기업은 에어 리퀴드, 에어 프로덕츠 앤 케미컬스, 에어 워터, AMCS Corporation, CRYOTEC Anlagenbau GmbH, 에나플렉스, 바다풍 공기분리집단, 린데, 메사, 프락세아테크놀로지, 런치크라이오제닉스, 사천공기분리 플랜트 그룹, 대양닛산, 테크넥스, 유니버설 인더스트리얼 가스, 인데 가스 등이 있습니다. 이 기업들은 시장 입지와 기술 역량을 강화하기 위해 합병, 인수, 파트너십과 같은 전략적 이니셔티브에 집중하고 있습니다. 시장에서의 입지를 강화하기 위해 기업들은 몇 가지 주요 전략을 채택하고 있습니다. 첫째, 제품의 효율성과 환경적 지속 가능성을 높이기 위해 연구 개발에 투자하고 있습니다. 여기에는 탄소 발자국을 줄이기 위해 공기 분리 장치에 재생 에너지원을 통합하는 것이 포함됩니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 트럼프 정권의 관세 분석

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원자재)

- 주요 원자재의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원자재)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 무역에 미치는 영향

- 전망과 향후 검토 사항

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 전략적 대시보드

- 전략적 노력

- 기업의 시장 점유율

- 경쟁 벤치마킹

- 혁신과 지속가능성의 정세

제5장 시장 규모와 예측 : 가스별(2021-2034년)

- 주요 동향

- 질소

- 산소

- 아르곤

- 기타

제6장 시장 규모와 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 철강

- 석유 및 가스

- 의료

- 화학

- 기타

제7장 시장 규모와 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 남아프리카

- 라틴아메리카

- 브라질

- 아르헨티나

제8장 기업 프로파일

- Evoqua Water Technologies LLC

- Air Liquide

- Air Products and Chemicals, Inc.

- AIR WATER INC

- AMCS Corporation

- CRYOTEC Anlagenbau GmbH

- Enerflex Ltd.

- KaiFeng Air Separation Group Co, LTD.

- Linde plc

- Messer

- Praxair Technology, Inc.

- Ranch Cryogenics, Inc.

- Sichuan Air Separation Plant Group

- TAIYO NIPPON SANSO CORPORATION

- Technex

- Universal Industrial Gases, Inc.

- Yingde Gases

The Global Cryogenic Air Separation Unit Market was valued at USD 4.2 billion in 2024 and is estimated to grow at a CAGR of 4.7% to reach USD 6.7 billion by 2034, driven by the increasing demand for industrial gases such as oxygen, nitrogen, and argon across various sectors including steel, chemicals, and manufacturing. As industrial activities expand, particularly in developing nations, the need for these gases has surged, prompting investments in air separation technologies.

Additionally, the COVID-19 pandemic highlighted vulnerabilities in global healthcare systems, particularly the shortage of medical-grade oxygen during peak crisis periods. This urgency pushed governments and private healthcare providers to prioritize investments in medical gas infrastructure. As a result, demand surged for cryogenic air separation units capable of producing high-purity oxygen at scale. Hospitals and emergency care facilities began upgrading their oxygen generation capabilities, leading to new installations and retrofits. Beyond the immediate crisis response, this trend has continued as part of broader efforts to strengthen healthcare resilience, especially in emerging markets where healthcare access is expanding rapidly. The shift also encouraged local production of medical gases, reducing reliance on imports and ensuring long-term supply stability across regions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $4.2 Billion |

| Forecast Value | $6.7 Billion |

| CAGR | 4.7% |

The argon segment is projected to hit USD 1.4 billion by 2034, driven by its essential role in establishing inert atmospheres crucial for precision-driven industrial applications. As manufacturing technologies become more specialized, the need for stable, non-reactive environments has intensified. Argon's widespread adoption in processes such as TIG welding, electronics fabrication, laser cutting, and the production of specialty glass and solar panels underscores its growing relevance. The clean energy transition, particularly the expansion of solar technology, continues to be a major catalyst for argon demand, as the gas is indispensable in protecting materials from contamination during high-temperature procedures.

The healthcare industry, accounting for a 24.6% share in 2024, remains a major end-use segment for cryogenic air separation units. Hospitals, clinics, and long-term care centers increasingly depend on these systems to generate medical-grade oxygen onsite. This need is becoming more pressing as aging populations and chronic respiratory conditions place greater strain on healthcare systems worldwide. In response, investments in medical gas infrastructure have grown, particularly in regions seeking to enhance healthcare access and emergency readiness.

U.S. Cryogenic Air Separation Unit Market reached USD 640 million in 2024. Industrial growth in North America, supported by increased exploration of shale gas and a push for cleaner hydrogen fuel solutions, has created demand for localized, high-capacity ASU installations. Many of these facilities are in remote or high-demand zones where on-site gas generation is more efficient than transportation. Additionally, rising nitrogen demand in agriculture and pharmaceutical manufacturing reinforces the role of ASUs in supporting critical supply chains across the region.

Key players in the Global Cryogenic Air Separation Unit Market include Air Liquide, Air Products and Chemicals, Inc., AIR WATER INC, AMCS Corporation, CRYOTEC Anlagenbau GmbH, Enerflex Ltd., KaiFeng Air Separation Group Co., LTD, Linde plc, Messer, Praxair Technology, Inc., Ranch Cryogenics, Inc., Sichuan Air Separation Plant Group, TAIYO NIPPON SANSO CORPORATION, Technex, Universal Industrial Gases, Inc., and Yingde Gases. These companies focus on strategic initiatives such as mergers, acquisitions, and partnerships to enhance their market presence and technological capabilities. To strengthen their presence in the market, companies are adopting several key strategies. Firstly, they are investing in research and development to enhance the efficiency and environmental sustainability of their products. This includes integrating renewable energy sources into air separation units to reduce carbon footprints.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market definition

- 1.2 Base estimates & calculations

- 1.3 Forecast calculation

- 1.4 Data source

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.1 Impact on trade

- 3.3 Outlook and future considerations

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive landscape, 2024

- 4.1 Introduction

- 4.2 Strategic dashboard

- 4.3 Strategic initiative

- 4.4 Company market share

- 4.5 Competitive benchmarking

- 4.6 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Gas, 2021 - 2034 (USD Billion)

- 5.1 Key trends

- 5.2 Nitrogen

- 5.3 Oxygen

- 5.4 Argon

- 5.5 Others

Chapter 6 Market Size and Forecast, By End Use, 2021 - 2034 (USD Billion)

- 6.1 Key trends

- 6.2 Iron & steel

- 6.3 Oil & gas

- 6.4 Healthcare

- 6.5 Chemicals

- 6.6 Others

Chapter 7 Market Size and Forecast, By Region, 2021 - 2034 (USD Billion)

- 7.1 Key trends

- 7.2 North America

- 7.2.1 U.S.

- 7.2.2 Canada

- 7.2.3 Mexico

- 7.3 Europe

- 7.3.1 Germany

- 7.3.2 UK

- 7.3.3 France

- 7.3.4 Spain

- 7.3.5 Italy

- 7.4 Asia Pacific

- 7.4.1 China

- 7.4.2 India

- 7.4.3 Japan

- 7.4.4 South Korea

- 7.4.5 Australia

- 7.5 Middle East & Africa

- 7.5.1 Saudi Arabia

- 7.5.2 UAE

- 7.5.3 South Africa

- 7.6 Latin America

- 7.6.1 Brazil

- 7.6.2 Argentina

Chapter 8 Company Profiles

- 8.1 Evoqua Water Technologies LLC

- 8.2 Air Liquide

- 8.3 Air Products and Chemicals, Inc.

- 8.4 AIR WATER INC

- 8.5 AMCS Corporation

- 8.6 CRYOTEC Anlagenbau GmbH

- 8.7 Enerflex Ltd.

- 8.8 KaiFeng Air Separation Group Co., LTD.

- 8.9 Linde plc

- 8.10 Messer

- 8.11 Praxair Technology, Inc.

- 8.12 Ranch Cryogenics, Inc.

- 8.13 Sichuan Air Separation Plant Group

- 8.14 TAIYO NIPPON SANSO CORPORATION

- 8.15 Technex

- 8.16 Universal Industrial Gases, Inc.

- 8.17 Yingde Gases