|

시장보고서

상품코드

1740977

증기 터빈 서비스 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Steam Turbine Service Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

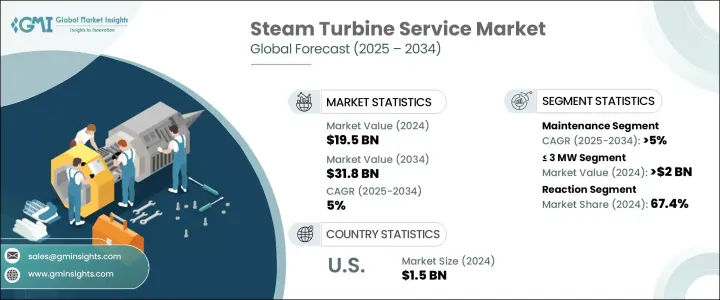

세계의 증기 터빈 서비스 시장 규모는 2024년에 195억 달러로 평가되었고, 화력발전 수요 증가, 업그레이드가 필요한 터빈 노후화, 운전 효율 최적화에 대한 주목 증가 등을 배경으로 2034년에는 318억 달러에 이를 것으로 예측되며, CAGR 5%로 성장할 전망입니다.

증기 터빈 서비스는 발전, 석유 및 가스, 산업 제조와 같은 산업 전반에서 터빈의 수명 주기와 성능을 향상시키기 위해 설계된 유지보수, 수리 및 점검(MRO) 활동을 포함합니다. 다운타임을 줄이고 에너지 생산량을 개선하는 것이 점점 더 중요해지면서 기업들은 최적의 터빈 기능을 보장하기 위해 예측 유지보수, 디지털 모니터링 및 고급 수리 솔루션에 점점 더 많은 투자를 하고 있습니다.

에너지 효율과 엄격한 배출 기준을 장려하는 정부 노력은 발전사와 산업 운영자가 증기 터빈의 정기적인 서비스에 투자하도록 더욱 장려하고 있습니다. 노후화된 석탄 및 가스 기반 발전소의 현대화와 열병합 발전(CHP) 프로젝트의 등장으로 종합 서비스 솔루션에 대한 수요가 증가하고 있습니다. 또한 서비스 제공업체는 최종 사용자의 진화하는 운영 요구 사항을 충족하기 위해 장기 서비스 계약(LTSA) 및 성과 기반 계약을 포함한 맞춤형 계약을 제공하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 195억 달러 |

| 예측 금액 | 318억 달러 |

| CAGR | 5% |

증기 터빈 서비스 시장은 주로 용량별로 구분되며, 정격 출력 100MW를 초과하는 터빈은 2024년 시장을 선도해 144억 달러를 창출했습니다. 대용량 터빈은 주로 운영 안정성과 고효율이 중요한 유틸리티 규모의 화력발전소, 원자력 시설, 산업용 열병합 발전소에서 주로 사용됩니다. 이러한 대용량 터빈의 서비스 수요는 운영 수명을 연장하고 변화하는 그리드 규정 및 효율성 규범을 준수하기 위해 주기적인 보수, 부품 교체 및 성능 업그레이드의 필요성으로 인해 증가하고 있습니다.

설계별로는 반응 증기 터빈 분야가 2024년 131억 달러의 평가액으로 서비스 시장을 독점했습니다. 고압 증기를 효율적으로 처리하는 것으로 잘 알려진 반응 터빈은 대규모 화력 및 원자력 발전에 널리 사용되고 있습니다. 반응 터빈의 복잡한 작동 환경은 비용이 많이 드는 고장을 방지하고 출력 수준을 유지하기 위해 잦은 검사, 정밀 수리 및 고급 진단 서비스가 필요합니다. 서비스 제공업체는 3D 스캐닝, 원격 모니터링, 적층 제조와 같은 기술을 활용하여 전 세계 리액션 터빈 차량에 더 빠르고 정밀한 유지보수 솔루션을 제공하는 사례가 늘고 있습니다.

서비스 유형별로는 2024년 수리 부문이 82억 달러로 가장 큰 시장 점유율을 차지했습니다. 많은 증기 터빈이 설계 수명에 도달하거나 초과함에 따라 블레이드 보수, 로터 용접, 케이싱 복원, 효율 개조를 포함한 수리 서비스에 대한 수요가 증가하고 있습니다. 적시에 수리하면 주요 고장을 예방할 뿐만 아니라 성능을 복원하고 연료 소비를 최적화하며 터빈 전체 교체와 관련된 자본 지출을 연기할 수 있습니다. 서비스 제공업체들은 가동 중단 시간을 최소화하고 고객 서비스를 개선하기 위해 모바일 서비스 유닛, 현장 수리, 디지털 트윈 기술을 통해 수리 역량을 확장하고 있습니다.

2024년 세계의 증기 터빈 서비스 시장은 화력발전소의 대규모 설비 기반과 견조한 산업활동에 힘입어 아시아태평양이 96억 달러를 벌어 세계를 선도했습니다. 중국, 인도, 일본, 한국 등의 국가는 급증하는 전력 수요와 지속 가능성 목표를 달성하기 위해 정부와 유틸리티가 기존 터빈 자산을 유지보수하고 업그레이드하는 데 막대한 투자를 하면서 이 지역의 성장을 주도하고 있습니다. 그리드 안정성, 석탄 화력 인프라의 현대화, 청정 석탄 기술에 대한 투자 증가는 이 지역 서비스 제공업체에게 수익성 높은 기회를 창출하고 있습니다. 또한 경쟁력 있는 현지화된 서비스를 제공하는 주요 OEM 및 제3자 서비스 제공업체의 존재는 아시아태평양 지역의 시장 지배력을 더욱 강화하고 있습니다.

지멘스에너지, 제너럴 일렉트릭(GE), 미쓰비시전기, 에토스에너지, 슬루자 리미티드 등의 주요 기업들은 전략적 서비스 제공, 디지털화를 위한 노력, 지역 서비스 센터 확대를 통해 시장에서의 지위를 강화하고 있습니다. AI 기반 예측 유지보수 플랫폼, 모듈식 수리 기술, 유연한 서비스 계약과 같은 혁신은 글로벌 증기 터빈 서비스 시장의 꾸준한 성장을 활용하고자 하는 기업에게 중추적인 역할을 하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 트럼프 정권의 관세 분석

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원자재)

- 주요 원자재의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원자재)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 규제 상황

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 전략적 전망

- 혁신과 지속가능성의 정세

제5장 시장 규모와 예측 : 용량별(2021-2034년)

- 주요 동향

- 3MW 미만

- 3-100MW 이상

- 100MW 이상

제6장 시장 규모와 예측 : 설계별(2021-2034년)

- 주요 동향

- 반응

- 임펄스

제7장 시장 규모와 예측 : 서비스 유형별(2021-2034년)

- 주요 동향

- 유지보수

- 수리

- 오버홀

- 기타

제8장 시장 규모와 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 산업

- 유틸리티

제9장 시장 규모와 예측 : 서비스 제공업체별(2021-2034년)

- 주요 동향

- OEM

- 비 OEM

제10장 시장 규모와 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 프랑스

- 러시아

- 독일

- 스페인

- 이탈리아

- 아시아태평양

- 중국

- 일본

- 한국

- 인도

- 호주

- 인도네시아

- 말레이시아

- 태국

- 중동 및 아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

- 이란

- 이집트

- 남아프리카

- 나이지리아

- 튀르키예

- 모로코

- 라틴아메리카

- 브라질

- 아르헨티나

- 칠레

제11장 기업 프로파일

- EthosEnergy

- Fincantieri

- Fortum

- GE Vernova

- Goltens

- Mechanical Dynamics & Analysis

- Metalock Engineering

- Mitsubishi Power

- Power Services Group

- ST Cotter Turbine Services

- Siemens Energy

- Soderqvist Engineering Sweden

- Steam Turbine Services

- Sulzer

- Toshiba America Energy Systems

- Trillium Flow Technologies

- Triveni Turbine

- WEG

The Global Steam Turbine Service Market was valued at USD 19.5 billion in 2024 and is estimated to grow at a CAGR of 5% to reach USD 31.8 billion by 2034, driven by the rising demand for thermal power generation, the aging turbine fleet requiring upgrades, and increased focus on optimizing operational efficiency. Steam turbine service encompasses maintenance, repair, and overhaul (MRO) activities designed to enhance the lifecycle and performance of turbines across industries such as power generation, oil and gas, and industrial manufacturing. With a growing emphasis on reducing downtime and improving energy output, companies are increasingly investing in predictive maintenance, digital monitoring, and advanced repair solutions to ensure optimal turbine functionality.

Government initiatives promoting energy efficiency and stricter emission standards are further encouraging power producers and industrial operators to invest in the regular servicing of their steam turbines. Modernization of aging coal- and gas-based plants, along with the emergence of combined heat and power (CHP) projects, is fueling the demand for comprehensive service solutions. Service providers are also offering customized contracts, including long-term service agreements (LTSA) and performance-based contracts, to meet the evolving operational requirements of end-users.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $19.5 Billion |

| Forecast Value | $31.8 Billion |

| CAGR | 5% |

The Steam Turbine Service Market is primarily segmented by capacity, with turbines rated >100 MW leading the market in 2024, generating USD 14.4 billion. Large-capacity turbines are predominantly used in utility-scale thermal power plants, nuclear facilities, and industrial cogeneration plants, where operational reliability and high efficiency are critical. The demand for servicing these high-capacity turbines is being propelled by the need for periodic refurbishment, parts replacement, and performance upgrades to extend operational life and maintain compliance with changing grid regulations and efficiency norms.

By design, the reaction steam turbine segment dominated the service market in 2024 with a valuation of USD 13.1 billion. Reaction turbines, known for their efficiency at handling high-pressure steam conditions, are widely deployed in large-scale thermal and nuclear power generation. The complex operating environments of reaction turbines necessitate frequent inspections, precision repairs, and advanced diagnostic services to prevent costly failures and sustain output levels. Service providers are increasingly leveraging technologies such as 3D scanning, remote monitoring, and additive manufacturing to deliver faster and more precise maintenance solutions for reaction turbine fleets globally.

In terms of service type, the repair segment held the largest market share in 2024, accounting for USD 8.2 billion. As many steam turbines are reaching or surpassing their design lifespans, demand for repair services - including blade refurbishment, rotor welding, casing restoration, and efficiency retrofits - is rising. Timely repairs not only prevent major breakdowns but also restore performance, optimize fuel consumption, and defer the capital expenditure associated with complete turbine replacements. Service providers are expanding their repair capabilities with mobile service units, in-situ repairs, and digital twin technologies to minimize downtime and improve customer service.

Asia Pacific led the global Steam Turbine Service Market in 2024, generating USD 9.6 billion, supported by its large installed base of thermal power plants and robust industrial activity. Countries like China, India, Japan, and South Korea are driving regional growth, as governments and utilities invest heavily in maintaining and upgrading existing turbine assets to meet surging electricity demand and sustainability goals. The push for grid stability, modernization of coal-fired power infrastructure, and rising investments in clean coal technologies are creating lucrative opportunities for service providers across the region. Additionally, the presence of major OEMs and third-party service providers offering competitive, localized services further strengthens Asia Pacific's dominance in the market.

Leading companies such as Siemens Energy, General Electric (GE), Mitsubishi Power, EthosEnergy, and Sulzer Ltd. are reinforcing their market position through strategic service offerings, digitalization initiatives, and regional service center expansions. These players are increasingly focused on providing comprehensive service portfolios - encompassing field services, condition monitoring, upgrade solutions, and remote diagnostics - to cater to the evolving needs of utilities and industrial clients. Innovations such as AI-powered predictive maintenance platforms, modular repair techniques, and flexible service agreements are becoming pivotal for companies seeking to capitalize on the steady growth of the global Steam Turbine Service Market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.2 Market estimates & forecast parameters

- 1.3 Forecast calculation

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid

- 1.4.2.2 Public

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs analysis

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Regulatory landscape

- 3.4 Industry impact forces

- 3.4.1 Growth drivers

- 3.4.2 Industry pitfalls & challenges

- 3.5 Growth potential analysis

- 3.6 Porter's analysis

- 3.6.1 Bargaining power of suppliers

- 3.6.2 Bargaining power of buyers

- 3.6.3 Threat of new entrants

- 3.6.4 Threat of substitutes

- 3.7 PESTEL analysis

Chapter 4 Competitive Landscape, 2025

- 4.1 Introduction

- 4.2 Strategic outlook

- 4.3 Innovation & sustainability landscape

Chapter 5 Market Size and Forecast, By Capacity, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 ≤ 3 MW

- 5.3 > 3 MW - 100 MW

- 5.4 > 100 MW

Chapter 6 Market Size and Forecast, By Design, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Reaction

- 6.3 Impulse

Chapter 7 Market Size and Forecast, By Service, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Maintenance

- 7.3 Repair

- 7.4 Overhaul

- 7.5 Others

Chapter 8 Market Size and Forecast, By End Use, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 Industrial

- 8.3 Utility

Chapter 9 Market Size and Forecast, By Service Provider, 2021 - 2034 (USD Million)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Non-OEM

Chapter 10 Market Size and Forecast, By Region, 2021 - 2034 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.2.3 Mexico

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 France

- 10.3.3 Russia

- 10.3.4 Germany

- 10.3.5 Spain

- 10.3.6 Italy

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 South Korea

- 10.4.4 India

- 10.4.5 Australia

- 10.4.6 Indonesia

- 10.4.7 Malaysia

- 10.4.8 Thailand

- 10.5 Middle East & Africa

- 10.5.1 Saudi Arabia

- 10.5.2 UAE

- 10.5.3 Iran

- 10.5.4 Egypt

- 10.5.5 South Africa

- 10.5.6 Nigeria

- 10.5.7 Turkey

- 10.5.8 Morocco

- 10.6 Latin America

- 10.6.1 Brazil

- 10.6.2 Argentina

- 10.6.3 Chile

Chapter 11 Company Profiles

- 11.1 EthosEnergy

- 11.2 Fincantieri

- 11.3 Fortum

- 11.4 GE Vernova

- 11.5 Goltens

- 11.6 Mechanical Dynamics & Analysis

- 11.7 Metalock Engineering

- 11.8 Mitsubishi Power

- 11.9 Power Services Group

- 11.10 S.T. Cotter Turbine Services

- 11.11 Siemens Energy

- 11.12 Soderqvist Engineering Sweden

- 11.13 Steam Turbine Services

- 11.14 Sulzer

- 11.15 Toshiba America Energy Systems

- 11.16 Trillium Flow Technologies

- 11.17 Triveni Turbine

- 11.18 WEG