|

시장보고서

상품코드

1741049

자동 주차 시스템 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Automated Parking System Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

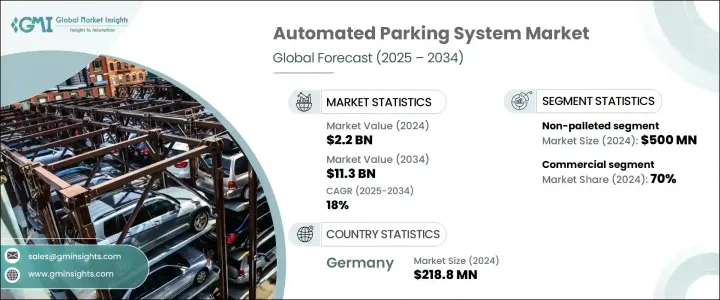

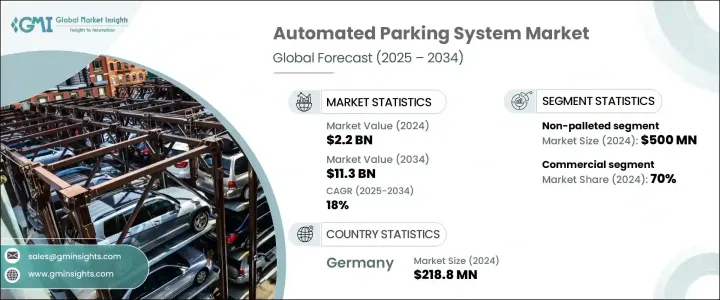

세계의 자동 주차 시스템 시장 규모는 2024년에는 22억 달러로 평가되었고, CAGR 18%로 성장할 전망이며, 2034년에는 113억 달러에 이를 것으로 예측됩니다.

이 산업은 급속한 도시화, 인구밀집 도시에서 주차장의 제한된 이용가능성, 스마트하고 공간절약적인 인프라에 대한 요구 증가 등을 배경으로 현저한 급성장을 이루고 있습니다. 자동차 대수 증가 및 부동산 축소에 따라 도시는 보다 효율적으로 공간을 관리할 필요가 있습니다. 자동 주차 시스템은 토지 이용을 최적화하고, 교통 흐름을 합리화하며, 이산화탄소 배출량을 삭감함으로써, 이러한 과제에 임하는 선진적인 솔루션으로서 대두되고 있습니다. 이러한 시스템은 사람의 개입을 줄이고 컴팩트하고 고효율적인 차량 보관 접근 방식을 제공합니다. 그 결과 주택과 상업 개발에서 병원과 교통 허브까지 폭넓은 도시 용도로 도입이 확대되고 있습니다.

자동 주차 시스템은 안전성을 높이고 공간 이용을 개선하고 환경에 미치는 영향을 최소화할 수 있기 때문에 인기를 끌고 있습니다. 고급 오토메이션 및 로봇 공학이 내장되어 있어 지능형 차량의 이동과 보관이 가능합니다. 다단 쌓기, 자동 차량 핸들링, 슬롯 관리 등의 기능을 통해 이러한 시스템은 시간 효율이 뛰어나고 환경 친화적입니다. 개발업자나 부동산 관리업자는, 운영 비용을 삭감해, 한정된 부지 면적에서 주차 용량을 늘려, 이용자에게 프리미엄의 경험을 제공하기 위해, 이러한 시스템을 채용하는 경우가 증가하고 있습니다. 지속 가능한 도시 인프라와 스마트 시티 구상에 대한 관심이 높아지는 가운데, 이러한 시스템은 보다 깨끗하고 효율적인 도시 모빌리티를 향한 세계의 대처에 부합하고 있기 때문에, 수요는 더욱 높아지고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 22억 달러 |

| 예측 금액 | 113억 달러 |

| CAGR | 18% |

플랫폼별로 볼 때 시장은 팔레트식과 비팔레트식으로 구분됩니다. 비팔레트 카테고리는 2024년 매출액이 약 5억 달러로 시장을 선도했습니다. 이 부문의 우위성은 공간 절약 설계 및 신속한 차량 회수 능력에 기인하고 있으며, 이들은 교통량이 많은 대도시권에서 특히 중요합니다. 팔레트식과 달리 비팔레트식은 지지대가 필요 없고 로봇공학과 컨베이어 시스템을 사용해 차량을 직접 이동시키기 때문에 기계적 셋업이 간소화되고 좁은 도시 지역 레이아웃에도 유연하게 설치할 수 있습니다. 높은 처리량 솔루션이 불가결한 상업 빌딩, 공항, 고층 주택 개발로 수요가 증가하고 있습니다.

최종 사용자의 관점에서 볼 때 시장은 주택용과 상업용으로 나뉘어져 있습니다. 2024년에는 오피스 빌딩, 소매 센터, 병원, 호스피탈리티 시설에서의 채용이 견인해, 상업 부문이 70%의 시장 점유율을 차지했습니다. 이러한 환경에서는 자동 주차가 수용력을 강화하고 혼잡을 완화하며 혼잡한 환경에서 차량에 대한 신속한 접근을 제공하는 능력으로부터 많은 혜택을 받고 있습니다. 도시의 혼잡 및 토지 가격 급등으로 기업은 제한된 공간을 최대한 활용하는 수직 또는 지하 주차장 구조에 투자하게 되어 있습니다. 게다가 자동 주차장과 스마트 빌딩 기술이나 강화된 보안 시스템과의 통합은, 상업 개발자에게 있어서 매력적인 선택사항이 되고 있습니다.

시장은 유형별로 분류되어 있으며, 2024년에는 반자동 시스템이 대부분의 점유율을 차지했습니다. 반자동화 시스템의 매력은 비용 효율, 신속한 셋업, 사용 편의성에 있어 주택과 상업의 양 부문에서 다양한 용도에 적합합니다. 이러한 시스템은 완전 자동화와 수동 제어의 균형을 제공하며, 완전 자동화와 같은 고액의 선행 투자 없이 사용자 경험의 향상을 실현합니다. 유지보수의 필요성이 낮고 사용자 친화적인 특징이 널리 받아들여지는 요인이 되고 있습니다.

시스템 구조 중 무인 운송 차량(AGV) 부문은 2024년 세계 시장을 선도하여 최대 수익 공유를 창출했습니다. AGV 시스템은 적응성이 높고 복잡한 레이아웃을 정확하게 이동할 수 있어 혼잡한 도시 환경과 대규모 상업 프로젝트에 최적입니다. 기존 인프라에 매끄럽게 통합하면서 고도의 자동화 및 유연성을 구현하는 AGV의 역량으로 AGV는 현대 주차장 과제에 대한 바람직한 솔루션이 되고 있습니다. AGV는 처리량과 공간 이용을 극대화하는 것이 중요한 환경에 특히 적합합니다.

2024년 자동 주차 시스템 시장에서 하드웨어는 세계 수익의 최대 점유율을 차지했습니다. 이는 센서, 리프트, AGV, 컨베이어 시스템 등의 물리적인 구성 요소가 필수적이기 때문이며, 자동 주차의 핵심을 이루는 것입니다. 시스템이 고도화됨에 따라 내구성 있고 고성능인 하드웨어에 대한 수요는 특히 장기적인 신뢰성과 대량의 취급을 필요로 하는 프로젝트에서 계속 증가하고 있습니다.

지역별로는 독일이 2024년의 수익 2억 1,880만 달러로 유럽 시장을 리드했으며, 2034년까지의 CAGR은 16.9%로 예측되고 있습니다. 이 나라의 강력한 자동차 산업, 스마트 시티 프로젝트에 대한 투자, 선진적인 도시 인프라가, 이 분야에서의 리더쉽에 크게 공헌하고 있습니다. 게다가 전세계의 기업이 연구 개발, 전략적 파트너십, 최첨단의 제조 기술에 투자함으로써 존재감을 높이고 있습니다. 시장을 선도하는 기업들은 모듈식 시스템 설계, 에너지 효율, AI 및 IoT 기술 통합에 주력하며 사용자 경험과 환경 성능을 모두 높이고 있습니다. 이러한 혁신이, 차세대의 스마트하고 지속 가능한 주차장 솔루션의 무대를 정돈해 가고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 하드웨어 제공업체

- 소프트웨어 제공업체

- 서비스 제공업체

- 기술 공급자

- 최종 용도

- 이익률 분석

- 공급자의 상황

- 트럼프 정권의 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에 대한 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(원재료)

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 무역에 미치는 영향

- 기술 및 혁신의 상황

- 특허 분석

- 규제 상황

- 비용 내역 분석

- 주요 뉴스 및 대처

- 영향요인

- 성장 촉진요인

- 북미와 유럽에서 자율주행차 증가

- 도시화의 급속한 진전

- 아시아태평양 및 중동의 스마트시티 프로젝트 상승

- 주차 시스템에서 기술의 진보

- 업계의 잠재적 위험 및 과제

- 높은 개발 비용

- 복잡한 유지보수 및 다운타임 위험

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추계 및 예측 : 유형별(2021-2034년)

- 주요 동향

- 완전 자동화

- 반자동

제6장 시장 추계 및 예측 : 구조별(2021-2034년)

- 주요 동향

- AGV 시스템

- 사일로 시스템

- 타워 시스템

- 레일 가이드 카트(RGC) 시스템

- 퍼즐 시스템

- 셔틀 시스템

제7장 시장 추계 및 예측 : 제공별(2021-2034년)

- 주요 동향

- 하드웨어

- 소프트웨어

- 서비스

제8장 시장 추계 및 예측 : 플랫폼별(2021-2034년)

- 주요 동향

- 팔레트

- 비팔레트

제9장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 주택용

- 상업용

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 프랑스

- 영국

- 스페인

- 이탈리아

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 남아프리카

- 사우디아라비아

제11장 기업 프로파일

- AutoMotion Parking

- City Lift Parking

- Dayang Parking

- EITO&GLOBAL

- Fata Automation

- IHI

- Klaus Multiparking

- Lodgie

- MHE Demag

- Park Assist

- Parkmatic

- ParkPlus

- Robotic Parking

- Serva Transport

- Skyline Parking

- Stolzer Parking

- TAPS

- Unitronics

- Westfalia Parking

- Wohr Parking

The Global Automated Parking System Market was valued at USD 2.2 billion in 2024 and is estimated to grow at a CAGR of 18% to reach USD 11.3 billion by 2034. The industry is experiencing a significant surge, driven by rapid urbanization, limited availability of parking in densely populated cities, and a growing need for smart, space-saving infrastructure. With rising vehicle numbers and shrinking real estate, cities are facing mounting pressure to manage space more efficiently. Automated parking systems are emerging as a forward-thinking solution that tackles these challenges by optimizing land usage, streamlining traffic flow, and reducing carbon emissions. These systems provide a compact, highly efficient approach to vehicle storage with reduced reliance on human intervention. As a result, their deployment is expanding across a wide range of urban applications-from residential and commercial developments to hospitals and transport hubs.

Automated parking systems are gaining popularity due to their ability to enhance safety, improve space utilization, and minimize environmental impact. They incorporate advanced automation and robotics, allowing for intelligent vehicle movement and storage. Features such as multi-level stacking, automated vehicle handling, and slot management make these systems both time-efficient and environmentally friendly. Developers and property managers are increasingly turning to these systems to reduce operational costs, increase parking capacity in a confined footprint, and offer a premium experience to users. The rising focus on sustainable urban infrastructure and smart city initiatives is further fueling demand, as these systems align with global efforts toward cleaner, more efficient urban mobility.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.2 Billion |

| Forecast Value | $11.3 Billion |

| CAGR | 18% |

In terms of platform, the market is segmented into palleted and non-palleted systems. The non-palleted category led the market with approximately USD 500 million in revenue in 2024. This segment's dominance is attributed to its space-saving design and quicker vehicle retrieval capabilities, which are especially important in high-traffic metropolitan areas. Unlike palleted systems, non-palleted ones eliminate the need for a supporting platform and use robotics and conveyor systems to move vehicles directly, simplifying the mechanical setup and allowing for flexible installation in tight urban layouts. Demand is growing in commercial buildings, airports, and high-rise residential developments where high-throughput solutions are essential.

From an end-user perspective, the market is split between residential and commercial applications. In 2024, the commercial segment held a substantial 70% market share, driven by adoption in office buildings, retail centers, hospitals, and hospitality venues. These settings benefit immensely from automated parking's ability to enhance capacity, reduce congestion, and provide quicker access to vehicles in busy environments. Urban congestion and the high cost of land are pushing businesses to invest in vertical or underground parking structures that make the most of limited space. Furthermore, the integration of automated parking with smart building technologies and enhanced security systems makes it an attractive option for commercial developers.

The market is also categorized by type, with semi-automated systems accounting for the majority share in 2024. Their appeal lies in cost efficiency, quick setup, and ease of use, making them suitable for diverse applications across both residential and commercial segments. These systems offer a balance between full automation and manual control, providing enhanced user experience without the high upfront investment of fully automated alternatives. Their low maintenance requirements and user-friendly features contribute to their widespread acceptance.

Among system structures, the Automated Guided Vehicle (AGV) segment led the global market in 2024, generating the largest revenue share. AGV systems are highly adaptable and can navigate complex layouts with precision, making them ideal for crowded urban settings and large commercial projects. Their ability to integrate seamlessly into existing infrastructure while delivering high levels of automation and flexibility has made them a preferred solution for modern parking challenges. AGVs are particularly well-suited for environments where maximizing throughput and space utilization is critical.

In terms of offerings, hardware dominated the automated parking system market in 2024, accounting for the largest share of global revenue. This is due to the essential nature of physical components such as sensors, lifts, AGVs, and conveyor systems, which form the core of any automated parking operation. As systems become more sophisticated, demand for durable, high-performance hardware continues to grow, especially in projects that require long-term reliability and high-volume handling.

Regionally, Germany led the European market with USD 218.8 million in revenue in 2024 and is forecasted to grow at a CAGR of 16.9% through 2034. The country's strong automotive industry, investment in smart city projects, and advanced urban infrastructure contribute significantly to its leadership in this sector. Additionally, companies across the globe are scaling their presence by investing in research and development, strategic partnerships, and cutting-edge manufacturing techniques. Market leaders are focusing on modular system designs, energy efficiency, and integration of AI and IoT technologies to enhance both user experience and environmental performance. These innovations are setting the stage for the next generation of smart, sustainable parking solutions.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates & calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimation

- 1.3 Forecast model

- 1.4 Primary research and validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market scope & definition

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.1.1 Hardware providers

- 3.1.1.2 Software providers

- 3.1.1.3 Service providers

- 3.1.1.4 Technology providers

- 3.1.1.5 End Use

- 3.1.2 Profit margin analysis

- 3.1.1 Supplier landscape

- 3.2 Impact of Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on industry

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.2.1.1 Price volatility in key materials

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact (raw materials)

- 3.2.3 Strategic industry responses

- 3.2.3.1 Supply chain reconfiguration

- 3.2.3.2 Pricing and product strategies

- 3.2.1 Impact on trade

- 3.3 Technology & innovation landscape

- 3.4 Patent analysis

- 3.5 Regulatory landscape

- 3.6 Cost breakdown analysis

- 3.7 Key news & initiatives

- 3.8 Impact forces

- 3.8.1 Growth drivers

- 3.8.1.1 Increasing autonomous vehicles in north america and europe

- 3.8.1.2 The rapid increase in urbanization

- 3.8.1.3 Rising smart city projects in asia pacific and middle east

- 3.8.1.4 Increasing technological advancements in parking systems

- 3.8.2 Industry pitfalls & challenges

- 3.8.2.1 High development cost

- 3.8.2.2 Complex maintenance and downtime risk

- 3.8.1 Growth drivers

- 3.9 Growth potential analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Fully automated

- 5.3 Semi-automated

Chapter 6 Market Estimates & Forecast, By Structure, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 AGV system

- 6.3 Silo system

- 6.4 Tower system

- 6.5 Rail Guided Cart (RGC) system

- 6.6 Puzzle system

- 6.7 Shuttle system

Chapter 7 Market Estimates & Forecast, By Offering, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Hardware

- 7.3 Software

- 7.4 Services

Chapter 8 Market Estimates & Forecast, By Platform, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 Palleted

- 8.3 Non-palleted

Chapter 9 Market Estimates & Forecast, By End Use, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 Residential

- 9.3 Commercial

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 France

- 10.3.3 UK

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 AutoMotion Parking

- 11.2 City Lift Parking

- 11.3 Dayang Parking

- 11.4 EITO&GLOBAL

- 11.5 Fata Automation

- 11.6 IHI

- 11.7 Klaus Multiparking

- 11.8 Lodgie

- 11.9 MHE Demag

- 11.10 Park Assist

- 11.11 Parkmatic

- 11.12 ParkPlus

- 11.13 Robotic Parking

- 11.14 Serva Transport

- 11.15 Skyline Parking

- 11.16 Stolzer Parking

- 11.17 TAPS

- 11.18 Unitronics

- 11.19 Westfalia Parking

- 11.20 Wohr Parking