|

시장보고서

상품코드

1750303

로봇 전투 차량 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Robotic Combat Vehicles Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

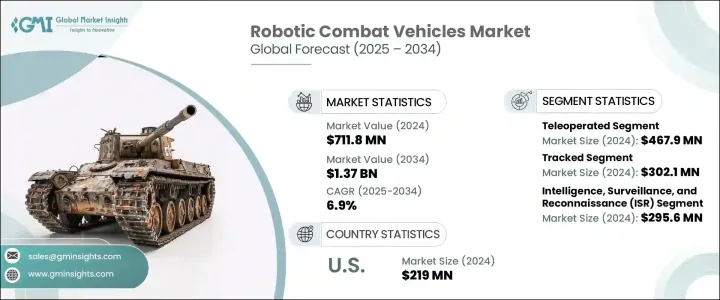

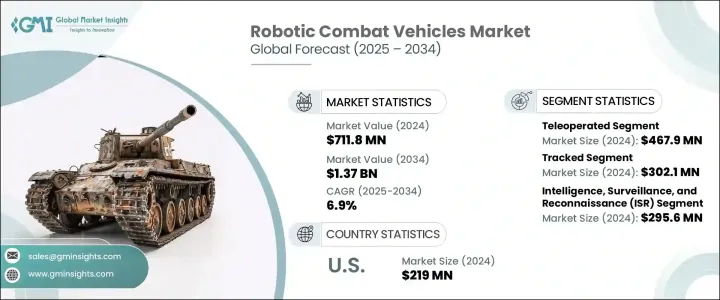

세계의 로봇 전투 차량 시장은 2024년 7억 1,180만 달러로 평가되었으며, 세계 방위 예산 증가와 인공지능(AI) 및 자율 기술의 진보로 CAGR 6.9%로 성장해 2034년까지 13억 7,000만 달러에 이를 것으로 추정됩니다.

각국이 국방지출을 늘리고 있는 가운데, 군사능력의 근대화와 병력의 유효성 강화에 주목이 모이고 있습니다.

인간의 개입을 최소한으로 억제하면서 리스크가 높은 환경에서의 임무를 가능하게 하는 것으로, 로봇 전투 차량은 전장을 재구축하고 있습니다. 감시, 수색 구조, 심지어 공격 작전 등, 종래는 인간의 병사가 실시하고 있던 작업을 실시할 수 있습니다. 이러한 고도의 무인 시스템에 대한 수요가 높아지고 있는 배경에는 현대 전쟁의 복잡화가 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 7억 1,180만 달러 |

| 예측 금액 | 13억 7,000만 달러 |

| CAGR | 6.9% |

시장은 동작 모드별로 자율형과 원격조작형으로 구분됩니다. 이러한 시스템은 군사 요원에게 높은 유연성을 제공하는 한편, 임무의 신뢰성과 윤리적 배려에 필수적인 인간의 제어를 유지합니다.

기동성별로 시장은 바퀴 부착형, 추적형, 하이브리드로 나뉘어져 있습니다. 상황에 최적입니다. 고급 무기나 센서 장치 등, 보다 무거운 적재물을 운반할 수 있기 때문에 직접 전투나 화력 지원의 역할에 있어서 수요가 더욱 높아지고 있습니다. 또한, 추적 차량은 안정성과 반동 흡수성이 높기 때문에 신속한 기동이나 실전 시나리오에 적합합니다.

미국 로봇 전투 차량(2024년) 시장 규모는 2억 1,900만 달러였습니다. 이는 지상 및 공중 작전을 위한 무인 시스템에 대한 군의 중점적인 노력 등 방위 프로그램이나 이니셔티브에 대한 정부의 많은 지출로 인한 것입니다. 또한, 육군 로봇 전투차 구상과 해군 무인 시스템 로드맵과 같은 프로그램은 이러한 기술에 대한 관심 증가에 기여하고 있습니다. 진화하는 위협과 더불어 군인의 위험을 완화할 필요성이 높아지고 있다는 것도 미국에서 RCV 수요를 더욱 높이고 있습니다.

로봇 전투 차량 시장의 주요 기업 몇사는 AI 주도의 기능을 통합하고 로봇 시스템의 견고성을 향상시킴으로써 적극적으로 제품 제공을 강화하고 있습니다. General Dynamics Land Systems, BAE Systems, Teledyne FLIR 등 주요 기업들은 이러한 차량의 기능성과 자율성 향상을 이끌고 있습니다. 또한 정찰, 감시, 물류 등 다양한 군사 요구에 대응하기 위해 제품 포트폴리오의 확대에도 주력하고 있습니다. 정부기관이나 방위 계약업체와의 협력관계도 장기계약을 확보하고 시장에서의 존재감을 높이기 위해 이들 기업이 이용하는 전략입니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향

- 주요 부품의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 업계에 미치는 영향요인

- 성장 촉진요인

- 증가하는 세계의 방위 예산

- AI와 자율 내비게이션의 진보

- 모듈식 전투 플랫폼 개발

- 고위험 지역의 무인 솔루션 수요

- 군사 근대화 프로그램 강화

- 업계의 잠재적 리스크 및 과제

- 고액의 개발 및 운용 비용

- 사이버 보안 취약성

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술의 상황

- 장래 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계 및 예측 : 동작 모드별, 2021-2034년

- 주요 동향

- 자율형

- 원격조작형

제6장 시장추계 및 예측 : 기동성별, 2021-2034년

- 주요 동향

- 바퀴 부착

- 추적형

- 하이브리드

제7장 시장 추계 및 예측 : 용도별, 2021-2034년

- 주요 동향

- 정보, 감시, 정찰(ISR)

- 직접 전투 및 화력 지원

- 전투 공학

- 의료 반송

- 기타

제8장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제9장 기업 프로파일

- BAE Systems

- Elbit Systems

- General Dynamics Land Systems

- HDT Global

- Israel Aerospace Industries

- Kratos Defense and Security Solutions

- Milrem Robotics

- Nexter Systems

- Oshkosh Defense

- Qinetiq

- Rheinmetall

- Teledyne FLIR

- Textron Systems

The Global Robotic Combat Vehicles Market was valued at USD 711.8 million in 2024 and is estimated to grow at a CAGR of 6.9% to reach USD 1.37 billion by 2034, driven by rising global defense budgets and advancements in artificial intelligence (AI) and autonomous technologies. As countries continue to increase their defense spending, there is a heightened focus on modernizing military capabilities and enhancing force effectiveness. RCVs are becoming increasingly integral to military strategies globally due to their ability to significantly reduce the risk to human personnel while enhancing operational capabilities.

By enabling missions in high-risk environments with minimal human intervention, robotic combat vehicles are reshaping the battlefield. Their use allows military forces to conduct complex operations more efficiently, from reconnaissance to direct combat, without exposing soldiers to unnecessary danger. These vehicles are equipped with advanced sensors, AI systems, and weaponry that enable them to perform tasks traditionally carried out by human soldiers, such as surveillance, search-and-rescue, and even offensive operations. The growing demand for these advanced unmanned systems is driven by the increasing complexity of modern warfare. Military operations today require more versatile and dynamic solutions, especially in situations where the terrain is challenging or the enemy is highly adaptive.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $711.8 Million |

| Forecast Value | $1.37 Billion |

| CAGR | 6.9% |

The market is segmented by the mode of operation into autonomous and teleoperated systems. The teleoperated RCVs segment generated USD 467.9 million in 2024, due to the demand for systems that require real-time control in complex environments, such as urban combat or dynamic combat zones. These systems offer military personnel greater flexibility while still retaining human control, which is vital for mission reliability and ethical considerations. As militaries transition toward fully autonomous systems, teleoperated RCVs serve as an important intermediary step in adapting to these technologies.

In terms of mobility, the market is divided into wheeled, tracked, and hybrid vehicles. The tracked RCV segment generated USD 302.1 million in 2024. These tracked vehicles offer superior mobility on rugged terrain, making them ideal for frontline operations and combat situations in difficult environments. Their ability to carry heavier payloads, including advanced weaponry and sensor equipment, further increases their demand in direct combat and fire support roles. Additionally, tracked vehicles provide greater stability and recoil absorption, making them well-suited for rapid maneuvers and live-fire scenarios.

U.S. Robotic Combat Vehicles Market was valued at USD 219 million in 2024 due to substantial government spending on defense programs and initiatives, such as the military's focus on unmanned systems for ground and aerial operations. Furthermore, programs like the Army's Robotic Combat Vehicle initiative and the Navy's unmanned systems roadmap contribute to the growing interest in these technologies. The increasing need to reduce risks to military personnel, coupled with evolving threats, further fuels demand for RCVs in the U.S.

Several key players in the Robotic Combat Vehicles Market are actively enhancing their offerings by integrating AI-driven capabilities and improving the robustness of their robotic systems. Companies like General Dynamics Land Systems, BAE Systems, and Teledyne FLIR are leading the way in advancing the functionality and autonomy of these vehicles. They are also focusing on expanding their product portfolios to cater to diverse military needs, such as reconnaissance, surveillance, and logistics. Collaborations with government agencies and defense contractors are another strategy used by these players to secure long-term contracts and reinforce their market presence.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Trump administration tariffs

- 3.2.1 Impact on trade

- 3.2.1.1 Trade volume disruptions

- 3.2.1.2 Retaliatory measures

- 3.2.2 Impact on the industry

- 3.2.2.1 Supply-side impact

- 3.2.2.1.1 Price volatility in key components

- 3.2.2.1.2 Supply chain restructuring

- 3.2.2.1.3 Production cost implications

- 3.2.2.2 Demand-side impact (selling price)

- 3.2.2.2.1 Price transmission to end markets

- 3.2.2.2.2 Market share dynamics

- 3.2.2.2.3 Consumer response patterns

- 3.2.2.1 Supply-side impact

- 3.2.3 Key companies impacted

- 3.2.4 Strategic industry responses

- 3.2.4.1 Supply chain reconfiguration

- 3.2.4.2 Pricing and product strategies

- 3.2.4.3 Policy engagement

- 3.2.5 Outlook and future considerations

- 3.2.1 Impact on trade

- 3.3 Industry impact forces

- 3.3.1 Growth drivers

- 3.3.1.1 Rising global defense budgets

- 3.3.1.2 Advancements in ai and autonomous navigation

- 3.3.1.3 Development of modular combat platforms

- 3.3.1.4 Demand for unmanned solutions in high-risk zones

- 3.3.1.5 Increasing military modernization programs

- 3.3.2 Industry pitfalls and challenges

- 3.3.2.1 High development and operational costs

- 3.3.2.2 Cybersecurity vulnerabilities

- 3.3.1 Growth drivers

- 3.4 Growth potential analysis

- 3.5 Regulatory landscape

- 3.6 Technology landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Mode of Operation, 2021 – 2034 (USD Million & Thousand Units)

- 5.1 Key trends

- 5.2 Autonomous

- 5.3 Teleoperated

Chapter 6 Market Estimates and Forecast, By Mobility, 2021 – 2034 (USD Million & Thousand Units)

- 6.1 Key trends

- 6.2 Wheeled

- 6.3 Tracked

- 6.4 Hybrid

Chapter 7 Market Estimates and Forecast, By Application, 2021 – 2034 (USD Million & Thousand Units)

- 7.1 Key trends

- 7.2 Intelligence, surveillance, and reconnaissance (ISR)

- 7.3 Direct Combat & Fire Support

- 7.4 Combat Engineering

- 7.5 Medical Evacuation

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Region, 2021 – 2034 (USD Million & Thousand Units)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 BAE Systems

- 9.2 Elbit Systems

- 9.3 General Dynamics Land Systems

- 9.4 HDT Global

- 9.5 Israel Aerospace Industries

- 9.6 Kratos Defense and Security Solutions

- 9.7 Milrem Robotics

- 9.8 Nexter Systems

- 9.9 Oshkosh Defense

- 9.10 Qinetiq

- 9.11 Rheinmetall

- 9.12 Teledyne FLIR

- 9.13 Textron Systems