|

시장보고서

상품코드

1750412

예측 유전자 테스트 및 소비자 유전체학 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Predictive Genetic Testing and Consumer Genomics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

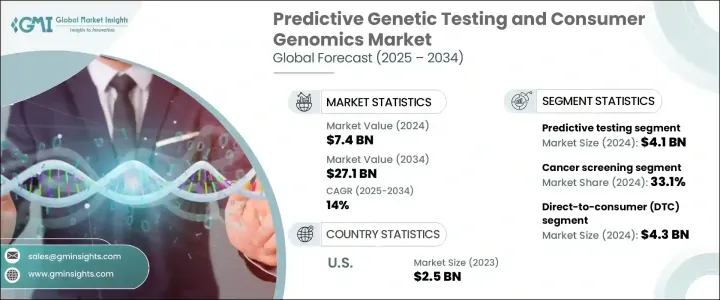

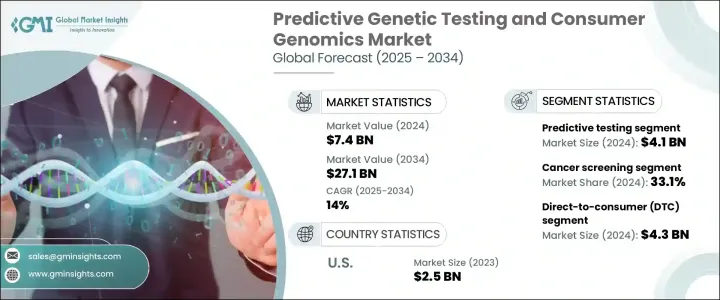

세계의 예측 유전자 테스트 및 소비자 유전체학 시장은 2024년에는 74억 달러로 평가되었고, 개별화 헬스케어에 대한 소비자의 관심이 높아지고, 유전자 테스트 기술의 진보, 예방적인 건강 전략으로의 이동이 요인이 되어 CAGR 14%를 나타내 2034년에는 271억 달러에 달할 것으로 추정됩니다.

소비자 직접(DTC) 유전자 테스트는 유전자 정보에 대한 액세스를 민주화하고 개인이 의료 종사자의 참여없이 자신의 가족, 라이프 스타일의 특징, 잠재적 건강 위험을 조사 할 수 있게 했습니다.

특히 차세대 시퀀싱(NGS)과 AI를 활용한 유전체 해석에 있어서의 기술적 비약적 진보는 테스트의 정확도를 극적으로 향상시키고, 비용을 낮추고, 소비자의 접근을 넓혔습니다. 파트너십에 의해 더욱 보완되어 유전체 데이터의 임상 케어에의 통합을 촉진하고 있습니다. 소비자 직접 판매형(DTC) 유전자 테스트의 이용 확대가 시장의 기세에 큰 영향을 주고 있어 건강 리스크에 대한 인사이트, 선조의 내역, 라이프 스타일에 관련하는 유전 형질에의 즉각 액세스를 개인에게 제공합니다. 지향적인 사람들 수요가 급증하는 가운데 이러한 서비스는 주류가 되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 74억 달러 |

| 예측 금액 | 271억 달러 |

| CAGR | 14% |

2024년 시장 규모는 41억 달러로 예측 테스트 분야가 시장을 선도했습니다. 암 스크리닝 용도는 큰 시장 점유율을 차지하고, 유전자 분석을 이용하여 다양한 암과 관련된 변이를 검출하고, 조기 진단과 대상을 좁힌 예방 대책을 촉진합니다.

DTC 분야는 2024년에 세계의 예측 유전자 테스트 및 소비자 유전체학 시장을 선도해 43억 달러에 달했고 2034년에는 145억 달러에 이를 것으로 예측되고 있습니다. 테스트는 개인이 집에 있으면서 자신의 조상, 라이프스타일의 특징, 잠재적인 건강 리스크를 조사할 수 있도록 하는 것입니다.

2024년 북미의 예측 유전자 테스트 및 소비자 유전체학 시장 점유율은 고급 건강 관리 인프라, 유전자 기술의 조기 도입, 맞춤형 의료 및 예방 의료로의 강한 문화적 변화가 견인해 42%에 달했습니다. 지역 소비자들은 인지도 향상, 교육 수준 향상, 디지털 건강에 대한 노력에 힘입어 일상적인 건강과 웰니스 프랙티스의 일환으로 유전체 테스트를 점점 받아들이게 되었습니다.

세계의 예측 유전자 테스트 및 소비자 유전체 업계 주요 기업은 Abbott Laboratories, Agilent Technologies, ARUP Laboratories, BGI Genomics, Bio-Rad Laboratories, Danaher, EasyDNA, F. Hoffmann-La Roche, Illumina, Myriad Genetics, QIAGEN, Quest Diagnostics, Thermo Fisher Scientific, Variantyx 등이 있습니다. 예측 유전자 테스트 및 소비자 유전체학 시장의 기업은 시장에서의 존재감을 높이기 위해 다양한 전략을 채용하고 있습니다. 치료에 통합하기 위한 의료 서비스 제공업체와의 전략적 파트너십 형성, 접근성 향상을 위한 소비자에게 직접 서비스 확대 등이 포함되어 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 맞춤형 의료에의 의식의 고조

- 유전자 서열 분석에 있어서의 기술적 진보

- 조상과 건강에 대한 소비자의 관심 증가

- 업계의 잠재적 위험 및 과제

- 유전자 데이터에 관한 윤리와 프라이버시의 우려

- 테스트 기술의 고비용

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 트럼프 정권에 의한 관세에 대한 영향

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 수요측의 영향(판매가격)

- 향후 시장 동향

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계·예측 : 테스트 유형별(2021-2034년)

- 주요 동향

- 예측 테스트

- 유전적 감수성 테스트

- 예측 진단

- 인구 스크리닝

- 소비자 유전체학

- 웰빙 유전체학

- 뉴트리아 유전학

- 피부 및 신진대사 유전학

- 기타 웰니스 유전체학

제6장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 암 검진

- 심혈관 검진

- 근골격계 검진

- 당뇨병 검진 및 모니터링

- 파킨슨병/알츠하이머병 검진

- 기타 용도

제7장 시장 추계·예측 : 설정별(2021-2034년)

- 주요 동향

- 소비자 직접 판매(DTC)

- 병원 및 진료소

- 진단실험실

제8장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Abbott Laboratories

- Agilent Technologies

- ARUP Laboratories

- BGI Genomics

- Bio-Rad Laboratories

- Danaher

- EasyDNA

- F. Hoffmann-La Roche

- Illumina

- Myriad Genetics

- QIAGEN

- Quest Diagnostics

- Thermo Fisher Scientific

- Variantyx

The Global Predictive Genetic Testing and Consumer Genomics Market was valued at USD 7.4 billion in 2024 and is estimated to grow at a CAGR of 14% to reach USD 27.1 billion by 2034, attributed to heightened consumer interest in personalized healthcare, advancements in genetic testing technologies, and a shift towards proactive, preventative health strategies. Direct-to-consumer (DTC) genetic testing has democratized access to genetic information, allowing individuals to explore their ancestry, lifestyle traits, and potential health risks without healthcare provider involvement.

Technological breakthroughs, particularly in next-generation sequencing (NGS) and AI-powered genomic interpretation, have dramatically improved test precision and lowered costs, broadening consumer access. These advancements are further complemented by partnerships between genetic testing firms and healthcare providers, facilitating the integration of genomic data into clinical care. As the prevalence of chronic illnesses rises, and healthcare increasingly adopts predictive and precision medicine, North America is positioned to remain the global leader in this evolving landscape. The expanding use of direct-to-consumer (DTC) genetic tests has significantly influenced market momentum, offering individuals immediate access to health risk insights, ancestry breakdowns, and lifestyle-related genetic traits. With a surge in demand from a tech-savvy and health-conscious population, these offerings are becoming more mainstream. Additionally, strong governmental backing through initiatives and research funding from institutions like the NIH has created a robust foundation for the development and application of genomic tools.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.4 Billion |

| Forecast Value | $27.1 Billion |

| CAGR | 14% |

The predictive testing segment led the market in 2024, valued at USD 4.1 billion. These tests assess the likelihood of individuals developing specific diseases or conditions based on their genetic makeup, enabling early intervention and personalized healthcare strategies. The cancer screening application accounted for a significant market share, utilizing genetic analysis to detect mutations associated with various cancers, facilitating early diagnosis and targeted prevention measures.

The DTC segment led the global predictive genetic testing and consumer genomics market in 2024, generating USD 4.3 billion and is projected to reach USD 14.5 billion by 2034, driven by offering consumers convenient access to genetic insights without the involvement of healthcare professionals. The growing demand for personalized health and wellness solutions is fueling the adoption of DTC testing services. These tests empower individuals to explore their ancestry, lifestyle traits, and potential health risks from the comfort of their homes. With user-friendly platforms and cost-effective kits, DTC companies are driving mainstream consumer engagement across both developed and emerging markets.

North America Predictive Genetic Testing and Consumer Genomics Market held 42% share in 2024 driven by a sophisticated healthcare infrastructure, early adoption of genetic technologies, and a strong cultural shift toward personalized and preventative medicine. Consumers in the region are increasingly embracing genomic testing as part of routine health and wellness practices, spurred by growing awareness, higher education levels, and digital health engagement.

Key players in the Global Predictive Genetic Testing and Consumer Genomics Industry include Abbott Laboratories, Agilent Technologies, ARUP Laboratories, BGI Genomics, Bio-Rad Laboratories, Danaher, EasyDNA, F. Hoffmann-La Roche, Illumina, Myriad Genetics, QIAGEN, Quest Diagnostics, Thermo Fisher Scientific, and Variantyx. Companies in the predictive genetic testing and consumer genomics market employ various strategies to strengthen their market presence. These include investing in research and development to enhance test accuracy and expand service offerings, forming strategic partnerships with healthcare providers to integrate genetic testing into clinical practices, and expanding direct-to-consumer services to increase accessibility. Additionally, companies are focusing on regulatory compliance to gain consumer trust and ensure the reliability of their tests.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising awareness about personalized medicine

- 3.2.1.2 Technological advancements in genetic sequencing

- 3.2.1.3 Growing consumer interest in ancestry and wellness

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Ethical and privacy concerns about genetic data

- 3.2.2.2 High cost of testing technologies

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Demand-side impact (selling price)

- 3.5.1.1 Price transmission to end markets

- 3.5.2 Key companies impacted

- 3.5.3 Strategic industry responses

- 3.5.3.1 Supply chain reconfiguration

- 3.5.3.2 Pricing and product strategies

- 3.5.3.3 Policy engagement

- 3.5.4 Outlook and future considerations

- 3.5.1 Demand-side impact (selling price)

- 3.6 Future market trends

- 3.7 Porter's analysis

- 3.8 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company matrix analysis

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Test Type, 2021-2034 ($ Mn)

- 5.1 Key trends

- 5.2 Predictive testing

- 5.2.1 Genetic susceptibility test

- 5.2.2 Predictive diagnostics

- 5.2.3 Population screening

- 5.3 Consumer genomics

- 5.4 Wellness genomics

- 5.4.1 Nutria genetics

- 5.4.2 Skin and metabolism genetics

- 5.4.3 Other wellness genomics

Chapter 6 Market Estimates and Forecast, By Application, 2021-2034 ($ Mn)

- 6.1 Key trends

- 6.2 Cancer screening

- 6.3 Cardiovascular screening

- 6.4 Musculoskeletal screening

- 6.5 Diabetic screening and monitoring

- 6.6 Parkinsons/Alzheimer disease screening

- 6.7 Other applications

Chapter 7 Market Estimates and Forecast, By Setting, 2021-2034 ($ Mn)

- 7.1 Key trends

- 7.2 Direct-to-consumer (DTC)

- 7.3 Hospitals and clinics

- 7.4 Diagnostic laboratories

Chapter 8 Market Estimates and Forecast, By Region, 2021-2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 MEA

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Abbott Laboratories

- 9.2 Agilent Technologies

- 9.3 ARUP Laboratories

- 9.4 BGI Genomics

- 9.5 Bio-Rad Laboratories

- 9.6 Danaher

- 9.7 EasyDNA

- 9.8 F. Hoffmann-La Roche

- 9.9 Illumina

- 9.10 Myriad Genetics

- 9.11 QIAGEN

- 9.12 Quest Diagnostics

- 9.13 Thermo Fisher Scientific

- 9.14 Variantyx