|

시장보고서

상품코드

1750421

커피 포드 시장 기회와 성장 촉진요인, 업계 동향 분석 및 예측(2025-2034년)Coffee Pods Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

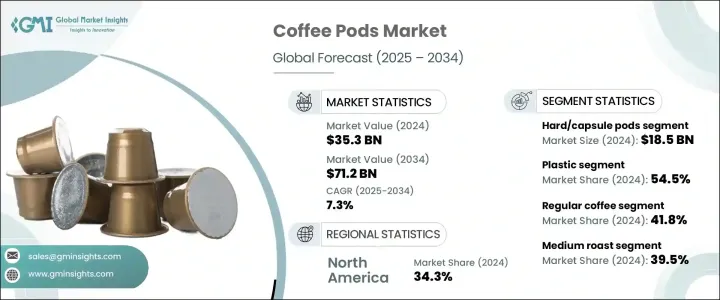

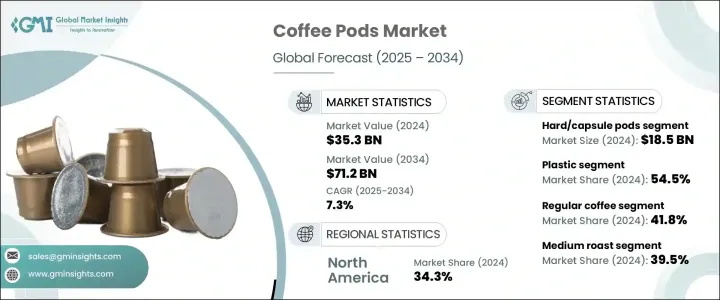

세계의 커피 포드 시장은 2024년에는 353억 달러로 평가되었으며, 2034년에는 CAGR 7.3%를 나타내 712억 달러에 이를 것으로 추정됩니다.

바쁜 일상생활이나 하이브리드인 직장 환경에 적응하는 사람이 늘어나는 가운데, 싱글서브 형식의 커피가 부엌이나 직장의 정평이 되고 있습니다. 이 때문에 가정에서 카페 스타일의 커피 체험을 요구하는 현대 소비자를 매료하고 있습니다.

또 다른 중요한 성장 요인은 현재 포드 형식으로 입수할 수 있는 다양한 향료, 유기농 블렌드, 스페셜티 옵션에 있으며, 다양한 커피 애음자 그룹을 매료시키고 있습니다. 북미와 유럽이 얼리 어답터였다면, 아시아 태평양과 라틴 아메리카 지역은 이제 프리미엄 포드 기반 커피 형식에 큰 관심을 보이고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 353억 달러 |

| 예측 금액 | 712억 달러 |

| CAGR | 7.3% |

2024년 제품 유형별 세계 시장은 하드 유형 또는 캡슐 유형의 커피 포드가 52.6%의 점유율을 차지했고 185억 달러의 매출을 계상했습니다. 대담한 에스프레소 스타일의 맥주를 선호하는 소비자에게 어필합니다. 레이버 프로파일, 로스팅 정도, 스페셜티 블렌드의 혁신의 급증이 이 카테고리를 확대해, 캐주얼인 식수로부터 커피통까지 폭넓은 층에 매력적인 존재로 계속하고 있습니다.

커피 포드 제조의 소재 선택은 제품의 매력과 지속가능성에 크게 영향을 미칩니다. 플라스틱 기반 포드 부문은 2024년 54.5%의 점유율을 차지했으며 2034년까지 7%의 연평균 성장률을 나타낼 것으로 예상됩니다. 그 인기는 내구성, 비용 효과, 신선도를 가두는 능력 등의 이점에 기인합니다. 이에 비해 기업은 소비자의 기대와 규제 요구를 모두 충족하기 위해 퇴비화 가능하고 완전히 재활용 가능한 대체 포드 등 환경 친화적인 소재의 개발을 강화하고 있습니다.

북미의 커피 포드 2024년 점유율은 34.3%에 달했는데, 경제적 요인이 소비자 행동에 변화를 가져왔고, 특히 가격에 민감한 구매층이 비용 절감 옵션으로 재사용 가능한 포드를 선택하게 되어 있습니다. 이와는 대조적으로, 유럽 시장은 더욱 안정적이며, 뿌리 깊은 커피의 전통과 추출 품질에 대한 정교한 평가가 프리미엄 포드의 견조한 판매를 견인하고 있습니다.

주요 기업은 Nestle SA, Tim Hortons, JAB, Keurig Dr Pepper Inc. Starbucks Corporation 등입니다. 시장 세분화를 강화하기 위해 시장 세분화 분야의 기업은 다양한 전략을 구사하고 있습니다. 머신의 호환성 강화, 지역의 미각에 맞춘 풍미의 다양화 등이 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 제조업체

- 유통업체

- 무역에 미치는 영향

- 무역량의 혼란

- 보복 조치

- 업계에 미치는 영향

- 공급측의 영향(원재료)

- 주요 원재료의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 공급측의 영향(원재료)

- 수요측의 영향(판매가격)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 공급자의 상황

- 이익률 분석

- 주요 뉴스와 대처

- 규제 상황

- 영향요인

- 성장 촉진요인

- 편리하고 고품질의 자가 양조에 대한 소비자 수요 증가

- 윤리적이고 고급스러운 커피에 대한 관심 증가

- 기술적 진보

- 업계의 잠재적 위험 및 과제

- 공급망의 혼란

- 경제 불확실성

- 시장 기회

- 성장 촉진요인

- 제품 개요

- 커피 포드의 제조 공정

- 커피의 가공 및 포장 기술

- 유통기한 보존 기술

- 맛 캡슐화 방법

- 규제 프레임워크과 기준

- 식품안전규제

- 포장 및 라벨 요구 사항

- 유기농 및 공정 무역 인증

- 일회용 제품에 관한 환경 규제

- 재활용 기준과 규정 준수

- 제조 공정 분석

- 커피의 로스팅과 분쇄

- 포드의 조립과 충전

- 씰링 및 포장 기술

- 품질 관리 프로세스

- 원재료 분석 및 조달 전략

- 가격 분석

- 지속가능성과 환경영향 평가

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 시장 점유율 분석

- 전략 틀

- 합병 및 인수

- 합작투자와 콜라보레이션

- 신제품 개발

- 확대 전략

- 경쟁 벤치마킹

- 벤더 상황

- 경쟁 포지셔닝 매트릭스

- 전략적 대시보드

- 브랜드 포지셔닝과 소비자 인식 분석

- 신규 참가자 시장 진출 전략

- 비공개 라벨 분석 및 전략

제5장 시장 추계·예측 : 제품 유형별(2021-2034년)

- 주요 동향

- 소프트 포드

- 종이 필터 포드

- 메쉬 필터 포드

- 기타 소프트 포드

- 하드/캡슐 포드

- 플라스틱 캡슐

- 알루미늄 캡슐

- 퇴비화 가능한 캡슐

- 기타 하드 포드

제6장 시장 추계·예측 : 재질별(2021-2034년)

- 주요 동향

- 플라스틱

- 일반 플라스틱

- 재활용 가능한 플라스틱

- 바이오플라스틱

- 알루미늄

- 종이 및 섬유

- 생분해성/퇴비화 가능한 소재

- 기타

제7장 시장 추계·예측 : 커피 유형별(2021-2034년)

- 주요 동향

- ㅇ리반 커피

- 아라비카

- 로부스터

- 블렌드

- 유기농 커피

- 향이 나는 커피

- 바닐라

- 카라멜

- 헤이즐넛

- 초콜릿

- 기타 맛

- 디카페인 커피

- 스페셜티 커피

- 싱글 오리진

- 마이크로 로트

- 기타 스페셜티 커피

- 공정 무역 커피

- 기타 커피의 유형

제8장 시장 추계·예측 : 로스팅 유형별(2021-2034년)

- 주요 동향

- 미디엄 로스트

- 미디엄 다크 로스트

- 다크 로스트

- 엑스트라 다크 로스트

제9장 시장 추계·예측 : 유통 채널별(2021-2034년)

- 주요 동향

- 슈퍼마켓 및 하이퍼마켓

- 전문점

- 편의점

- 온라인 소매

- 기업 웹사이트

- 전자상거래 플랫폼

- 구독 서비스

- 푸드서비스

- 소비자 직접 판매

- 기타

제10장 시장 추계·예측 : 기종 호환성별(2021-2034년)

- 주요 동향

- Nespresso

- Keurig

- Tassimo

- Senseo

- Dolce Gusto

- Lavazza

- Illy

- 멀티 호환 포드

- 기타

제11장 시장 추계·예측 : 가격대별(2021-2034년)

- 주요 동향

- 이코노미

- 미드레인지

- 프리미엄

- 슈퍼 프리미엄

제12장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제13장 기업 프로파일

- Nestle SA(Nespresso, Nescafe Dolce Gusto)

- Keurig Dr Pepper Inc.

- JAB Holding Company(Jacobs Douwe Egberts)

- Luigi Lavazza SpA

- The JM Smucker Company

- Starbucks Corporation

- Kraft Heinz Company

- Dunkin' Brands Group, Inc.

- Illycaffe SpA

- Melitta Group

- Dualit Ltd.

- Gourmesso

- Ethical Coffee Company

- Caffe Vergnano SpA

- Peet's Coffee &Tea, Inc.

- Caribou Coffee Company

- Tchibo GmbH

- UCC Ueshima Coffee Co.Ltd.

- Strauss Group Ltd.

- Cameron's Coffee

- San Francisco Bay Coffee

- Cafe Bustelo(JM Smucker)

- Cafe Royal

- Luckin Coffee Inc.

- Trung Nguyen Group

- Tim Hortons Inc.(Restaurant Brands International)

- Segafredo Zanetti(Massimo Zanetti Beverage Group)

- Reily Foods Company(Community Coffee)

- Rogers Family Company

- Puroast Coffee Company

The Global Coffee Pods Market was valued at USD 35.3 billion in 2024 and is estimated to grow at a CAGR of 7.3% to reach USD 71.2 billion by 2034, driven by the increasing appeal of convenience-driven products, especially among busy consumers seeking fast, premium coffee without the effort. With more people adapting to hectic routines and hybrid work environments, single-serve coffee formats are becoming a staple in kitchens and workplaces. The convenience of sealed, pre-portioned pods with minimal cleanup continues to attract modern consumers looking for a cafe-style coffee experience at home. Urban households shift towards compact brewing solutions that save time while maintaining taste consistency.

Another important growth factor lies in the broad variety of flavors, organic blends, and specialty options now available in pod format, attracting a diverse group of coffee drinkers. Demand rises in non-traditional markets as coffee machines become more accessible across suburban and semi-urban areas. While North America and Europe have been early adopters, the Asia Pacific and Latin American regions are now showing robust interest in premium pod-based coffee formats. The growing consciousness around sustainability has added momentum to innovations in recyclable and biodegradable pod materials, reshaping product development and branding strategies in this competitive space.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $35.3 Billion |

| Forecast Value | $71.2 Billion |

| CAGR | 7.3% |

In 2024, hard or capsule coffee pods dominated the global market by product type, accounting for a 52.6% share and generating USD 18.5 billion in sales. This category appeals to consumers who prefer bold, espresso-style brews with consistent strength and flavor. The growing inclination toward gourmet experiences at home, combined with the rise in single-serve coffee machines tailored for compact kitchens and office spaces, has driven demand significantly. As more consumers seek convenience without sacrificing quality, the capsule pod segment continues flourishing. A surge in innovation across flavor profiles, roast intensities, and specialty blends expands this category, keeping it attractive to a broad audience ranging from casual drinkers to coffee connoisseurs.

The choice of material in coffee pod production significantly affects product appeal and sustainability performance. Plastic-based pods segment held a 54.5% share in 2024 and is expected to grow at a CAGR of 7% through 2034. Their popularity stems from benefits such as durability, cost-effectiveness, and the ability to lock in freshness. Yet, increasing environmental scrutiny has pressurized manufacturers to address the ecological footprint of non-biodegradable packaging. In response, companies are stepping up development of eco-friendly materials, including compostable and fully recyclable pod alternatives, to meet both consumer expectations and regulatory demands.

North America Coffee Pods Market held a 34.3% share in 2024. The economic factors influence a shift in consumer behavior, particularly among price-sensitive buyers now opting for reusable pods as a cost-saving alternative. Despite this shift, the region continues to maintain strong overall sales volumes. In contrast, European markets have remained more consistent, with robust sales of premium pods driven by deep-rooted coffee traditions and a refined appreciation for brewing quality. Higher per-capita consumption and the popularity of espresso-based drinks help sustain growth in this region.

Top market players include Nestle SA, Tim Hortons, JAB, Keurig Dr Pepper Inc., and Starbucks Corporation. To enhance their market footprint, companies in the coffee pods segment are leveraging a mix of strategies. Key approaches include expanding product portfolios with plant-based and sustainable pod formats, enhancing machine compatibility, and diversifying flavor offerings to cater to regional palates. Strategic collaborations with appliance manufacturers help strengthen distribution networks, while direct-to-consumer channels and subscription models increase brand stickiness.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Methodology and Scope

- 1.2 Research methodology

- 1.3 Research scope & assumptions

- 1.4 List of data sources

- 1.5 Market estimation technique

- 1.6 Research limitations

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain

- 3.1.2 Profit margin analysis

- 3.1.3 Manufacturers

- 3.1.4 Distributors

- 3.1.5 Impact on trade

- 3.1.6 Trade volume disruptions

- 3.2 Retaliatory Measures

- 3.3 Impact on the Industry

- 3.3.1 Supply-Side impact (Raw Materials)

- 3.3.1.1 Price volatility in key materials

- 3.3.1.2 Supply chain restructuring

- 3.3.1.3 Production cost implications

- 3.3.1 Supply-Side impact (Raw Materials)

- 3.4 Demand-Side Impact (Selling Price)

- 3.4.1 Price transmission to end markets

- 3.4.2 Market share dynamics

- 3.4.3 Consumer response patterns

- 3.5 Key companies impacted

- 3.6 Strategic industry responses

- 3.6.1 Supply chain reconfiguration

- 3.6.2 Pricing and product strategies

- 3.6.3 Policy engagement

- 3.7 Outlook and future considerations

- 3.8 Supplier landscape

- 3.9 Profit margin analysis

- 3.10 Key news & initiatives

- 3.11 Regulatory landscape

- 3.12 Impact forces

- 3.12.1 Growth drivers

- 3.12.1.1 Rising consumer demand for convenient and high-quality home brewing

- 3.12.1.2 Growing interest in ethical and premium coffee options

- 3.12.1.3 Technological advancements

- 3.12.2 Industry pitfalls & challenges

- 3.12.2.1 Supply chain disruptions

- 3.12.2.2 Economic uncertainty

- 3.12.3 Market Opportunities

- 3.12.1 Growth drivers

- 3.13 Product Overview

- 3.13.1 Coffee pod manufacturing process

- 3.13.2 Coffee processing & packaging technologies

- 3.13.3 Shelf-life preservation techniques

- 3.13.4 Flavor encapsulation methods

- 3.14 Regulatory framework & standards

- 3.14.1 Food safety regulations

- 3.14.2 Packaging & labeling requirements

- 3.14.3 Organic & fair trade certifications

- 3.14.4 Environmental regulations for single-use products

- 3.14.5 Recyclability standards & compliance

- 3.15 Manufacturing process analysis

- 3.15.1 Coffee roasting & grinding

- 3.15.2 Pod assembly & filling

- 3.15.3 Sealing & packaging technologies

- 3.15.4 Quality control processes

- 3.16 Raw material analysis & procurement strategies

- 3.17 Pricing Analysis

- 3.18 Sustainability & environmental impact assessment

- 3.19 Growth potential analysis

- 3.20 Porter's analysis

- 3.21 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Market share analysis

- 4.3 Strategic framework

- 4.3.1 Mergers & acquisitions

- 4.3.2 Joint ventures & collaborations

- 4.3.3 New product developments

- 4.3.4 Expansion strategies

- 4.4 Competitive benchmarking

- 4.5 Vendor landscape

- 4.6 Competitive positioning matrix

- 4.7 Strategic dashboard

- 4.8 Brand positioning & consumer perception analysis

- 4.9 Market entry strategies for new players

- 4.10 Private label analysis & strategies

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Soft pods

- 5.2.1 Paper filter pods

- 5.2.2 Mesh filter pods

- 5.2.3 Other soft pods

- 5.3 Hard/Capsule pods

- 5.3.1 Plastic capsules

- 5.3.2 Aluminum capsules

- 5.3.3 Compostable capsules

- 5.3.4 Other hard pods

Chapter 6 Market Estimates and Forecast, By Material Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Plastic

- 6.2.1 Conventional plastic

- 6.2.2 Recyclable plastic

- 6.2.3 Bioplastic

- 6.3 Aluminum

- 6.4 Paper & fiber

- 6.5 Biodegradable/Compostable materials

- 6.6 Others

Chapter 7 Market Estimates and Forecast, By Coffee Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Regular coffee

- 7.2.1 Arabica

- 7.2.2 Robusta

- 7.2.3 Blends

- 7.3 Organic coffee

- 7.4 Flavored coffee

- 7.4.1 Vanilla

- 7.4.2 Caramel

- 7.4.3 Hazelnut

- 7.4.4 Chocolate

- 7.4.5 Other Flavors

- 7.5 Decaffeinated coffee

- 7.6 Specialty coffee

- 7.6.1 Single Origin

- 7.6.2 Micro-Lot

- 7.6.3 Other specialty coffee

- 7.7 Fair trade coffee

- 7.8 Other coffee types

Chapter 8 Market Estimates and Forecast, By Roast Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Medium roast

- 8.3 Medium-dark roast

- 8.4 Dark roast

- 8.5 Extra dark roast

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 – 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 Supermarkets & Hypermarkets

- 9.3 Specialty stores

- 9.4 Convenience stores

- 9.5 Online retail

- 9.5.1 Company websites

- 9.5.2 E-commerce platforms

- 9.5.3 Subscription services

- 9.6 Foodservice

- 9.7 Direct-to-consumer

- 9.8 Others

Chapter 10 Market Estimates and Forecast, By Machine Compatibility, 2021 - 2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 Nespresso

- 10.3 Keurig

- 10.4 Tassimo

- 10.5 Senseo

- 10.6 Dolce Gusto

- 10.7 Lavazza

- 10.8 Illy

- 10.9 Multi-compatible pods

- 10.10 Others

Chapter 11 Market Estimates and Forecast, By Price Range, 2021 - 2034 (USD Billion) (Kilo Tons)

- 11.1 Key trends

- 11.2 Economy

- 11.3 Mid-Range

- 11.4 Premium

- 11.5 Super-Premium

Chapter 12 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 12.1 Key trends

- 12.2 North America

- 12.2.1 U.S.

- 12.2.2 Canada

- 12.3 Europe

- 12.3.1 Germany

- 12.3.2 UK

- 12.3.3 France

- 12.3.4 Spain

- 12.3.5 Italy

- 12.3.6 Netherlands

- 12.4 Asia Pacific

- 12.4.1 China

- 12.4.2 India

- 12.4.3 Japan

- 12.4.4 Australia

- 12.4.5 South Korea

- 12.5 Latin America

- 12.5.1 Brazil

- 12.5.2 Mexico

- 12.5.3 Argentina

- 12.6 Middle East and Africa

- 12.6.1 Saudi Arabia

- 12.6.2 South Africa

- 12.6.3 UAE

Chapter 13 Company Profiles

- 13.1 Nestle S.A. (Nespresso, Nescafe Dolce Gusto)

- 13.2 Keurig Dr Pepper Inc.

- 13.3 JAB Holding Company (Jacobs Douwe Egberts)

- 13.4 Luigi Lavazza S.p.A.

- 13.5 The J.M. Smucker Company

- 13.6 Starbucks Corporation

- 13.7 Kraft Heinz Company

- 13.8 Dunkin' Brands Group, Inc.

- 13.9 Illycaffe S.p.A.

- 13.10 Melitta Group

- 13.11 Dualit Ltd.

- 13.12 Gourmesso

- 13.13 Ethical Coffee Company

- 13.14 Caffe Vergnano S.p.A.

- 13.15 Peet's Coffee & Tea, Inc.

- 13.16 Caribou Coffee Company

- 13.17 Tchibo GmbH

- 13.18 UCC Ueshima Coffee Co., Ltd.

- 13.19 Strauss Group Ltd.

- 13.20 Cameron's Coffee

- 13.21 San Francisco Bay Coffee

- 13.22 Cafe Bustelo (J.M. Smucker)

- 13.23 Cafe Royal

- 13.24 Luckin Coffee Inc.

- 13.25 Trung Nguyen Group

- 13.26 Tim Hortons Inc. (Restaurant Brands International)

- 13.27 Segafredo Zanetti (Massimo Zanetti Beverage Group)

- 13.28 Reily Foods Company (Community Coffee)

- 13.29 Rogers Family Company

- 13.30 Puroast Coffee Company