|

시장보고서

상품코드

1750596

바이오 센서 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Biosensors Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

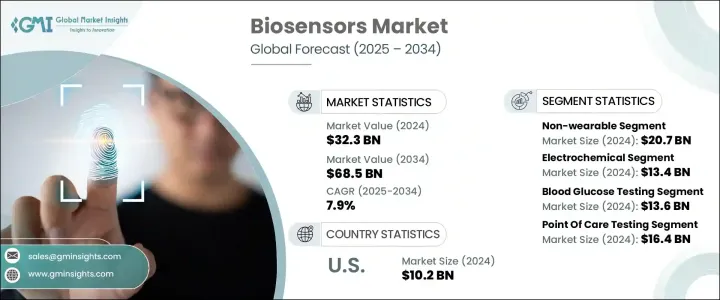

세계의 바이오 센서 시장 규모는 2024년에는 323억 달러로 평가되었고, 2034년에는 685억 달러에 이를 것으로 예측되며, CAGR 7.9%로 성장할 전망입니다.

이 장치는 높은 감도와 정밀도를 제공하여 다양한 질병의 조기 진단에 도움을 주는 바이오마커를 신속하게 탐지할 수 있습니다. 또한 바이오 센서의 약물 개발 및 생물의학 분야에서의 확대된 활용은 시장 성장을 더욱 촉진하고 있습니다. 휴대용 바이오 센서에 대한 수요 증가, 특히 아시아태평양 및 유럽 지역에서의 수요와 기술적 진보는 산업을 주도하는 주요 요인입니다.

바이오 센서 시장의 성장을 촉진하는 또 다른 주요 요인은 심각한 합병증을 예방하기 위해 지속적인 모니터링 및 관리가 필요한 당뇨병 및 심혈관 질환과 같은 만성 질환의 유병률 증가입니다. 예를 들어, 당뇨병을 관리하지 않고 방치하면 신부전, 뇌졸중, 하지 절단 등 심각한 건강 문제가 발생할 수 있습니다. 이로 인해 혈당 수치를 실시간으로 모니터링하여 환자가 필요할 때 즉시 조치를 취할 수 있는 기기의 수요가 증가하고 있습니다. 당뇨병 외에도 심혈관 질환의 발생률이 증가함에 따라 바이오 센서와 같은 고급 진단 도구를 통한 조기 발견과 지속적인 관리에 대한 수요가 증가하고 있습니다. 이러한 기술은 정확한 치료 계획을 수립하기 위해 시의적절한 데이터를 제공함으로써 환자 예후를 개선하는 데 기여하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 323억 달러 |

| 예측 금액 | 685억 달러 |

| CAGR | 7.9% |

2024년 비웨어러블 바이오 센서 시장은 207억 달러를 차지했습니다. 이 센서는 진단 기기에 통합되어 현장 진단 검사에 사용되며, 사용 편의성, 높은 정확도, 지속적인 사용자 상호작용 없이 즉시 결과를 제공할 수 있는 점으로 평가받고 있습니다. 의료 제공자들이 효율적이고 신속한 진단 도구를 추구함에 따라 이러한 비웨어러블 기기의 수요가 증가할 것으로 예상됩니다. 기술 혁신은 감도 향상, 소형화, 디지털 연결성 등을 통해 임상 환경에서의 효과성과 사용성을 높이고 있습니다.

전기화학적 바이오 센서 부문은 시장 점유율의 41.6%를 차지하며, 2024년 기준 134억 달러를 기록했습니다. 이 바이오 센서는 당뇨병 환자를 위한 혈당 측정기 등 의료 기기 및 심장 생체지표와 혈액 가스를 모니터링하는 시스템에 널리 사용됩니다. 심혈관 질환 및 당뇨병을 비롯한 만성 질환의 유병률이 증가함에 따라 필수 진단 기기로서 전기화학 센서의 수요가 촉진되고 있습니다.

미국의 바이오 센서 시장은 만성 질환, 특히 당뇨병 및 심장 관련 질환의 환자 수가 증가함에 따라 2024년에 102억 달러의 매출을 올렸습니다. 엄격한 규제 환경에도 불구하고 미국은 바이오 센서를 비롯한 혁신적인 의료 기술의 개발, 승인 및 상용화의 허브로 남아 있습니다. FDA와 같은 규제 기관은 새로운 바이오 센서 기술의 승인 절차를 가속화하는 데 점점 더 집중하고 있으며, 이는 의료 결과 개선에 대한 그들의 중요한 역할을 인식하고 있습니다.

시장에서의 위치를 강화하기 위해 기업들은 혁신과 파트너십에 집중하고 있습니다. 많은 기업들은 더 높은 감도와 정밀도를 갖춘 고급 바이오 센서 기술을 개발하기 위해 연구 개발(R&D)에 대규모 투자를 진행하고 있습니다. 의료 서비스 제공업체 및 연구 기관과의 협력은 혁신을 촉진하는 데 도움이 됩니다. 또한 일부 기업들은 질병별 바이오 센서 및 웨어러블 건강 모니터링 기기 등 다양한 의료 요구를 충족하기 위해 제품 포트폴리오를 확대하기 위해 노력하고 있습니다. Thermo Fisher Scientific, Masimo, Danaher 등 시장 선두 기업들은 이러한 전략을 채택하여 시장 입지를 강화하고 이처럼 빠르게 성장하는 산업에서 경쟁력을 유지하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 의료 분야에서의 바이오 센서 적용 확대

- 전 세계적인 당뇨병 유병률 증가

- 아시아태평양 및 유럽 지역에서의 휴대용 바이오 센서 수요 증가

- 기술의 진보의 가속

- 업계의 잠재적 위험 및 과제

- 엄격한 규제 환경

- 제품 개발의 높은 비용

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 트럼프 정권에 의한 관세에 대한 영향

- 무역에 미치는 영향

- 무역량의 혼란

- 국가별 대응

- 업계에 미치는 영향

- 공급측의 영향(제조 비용)

- 주요 원자재의 가격 변동

- 공급망 재구성

- 생산 비용에 미치는 영향

- 수요측의 영향(소비자의 비용)

- 최종 시장에의 가격 전달

- 시장 점유율 동향

- 소비자의 반응 패턴

- 공급측의 영향(제조 비용)

- 영향을 받는 주요 기업

- 전략적인 업계 대응

- 공급망 재구성

- 가격 설정 및 제품 전략

- 정책관여

- 전망과 향후 검토 사항

- 무역에 미치는 영향

- 기술적 상황

- 장래 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략 대시보드

제5장 시장 추계 및 예측 : 유형별(2021-2034년)

- 주요 동향

- 웨어러블

- 비웨어러블

제6장 시장 추계 및 예측 : 기술별(2021-2034년)

- 주요 동향

- 전기화학

- 광학

- 열

- 압전

- 기타 기술

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 혈당 검사

- 콜레스테롤 검사

- 혈액가스 분석

- 임신 검사

- 신약 개발

- 감염증 검사

- 기타 용도

제8장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 현장 검사

- 재택 케어 진단

- 연구실

- 기타 최종 사용자

제9장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 러시아

- 스위스

- 아시아태평양

- 중국

- 일본

- 인도

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

제10장 기업 프로파일

- Abbott Laboratories

- ARKRAY

- Bio-Rad Laboratories

- Biosensors International Group

- Dexcom

- Danaher

- F. Hoffmann-La Roche

- Masimo

- Nova Biomedical

- Platinum Equity Advisors

- PHC Holdings

- Pinnacle Technology

- Siemens Healthineers

- Thermo Fisher Scientific

- Trividia Health

The Global Biosensors Market was valued at USD 32.3 billion in 2024 and is estimated to grow at a CAGR of 7.9% to reach USD 68.5 billion by 2034, driven by increasing applications of biosensors across several sectors, particularly healthcare, where they play a crucial role in detecting biological signals. These devices offer high sensitivity and precision, allowing for the quick detection of biomarkers that aid in the early diagnosis of various diseases. Additionally, the expanding use of biosensors in drug discovery and biomedicine further supports the market's growth. The growing demand for portable biosensors, especially in regions like Asia Pacific and Europe, alongside technological advancements, is key factor propelling the industry.

Another key factor driving the growth of the biosensors market is the increasing prevalence of chronic conditions, such as diabetes and cardiovascular diseases, which require continuous monitoring and management to avoid serious complications. For example, diabetes, if left unmanaged, can lead to severe health issues like kidney failure, stroke, or lower limb amputations. This has led to a growing demand for devices that can offer real-time monitoring of blood glucose levels, allowing patients to take immediate action when necessary. In addition to diabetes, cardiovascular diseases are also on the rise, creating an increasing need for early detection and ongoing management through advanced diagnostic tools like biosensors. These technologies are helping improve patient outcomes by providing timely data that allows for more precise treatment plans.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $32.3 Billion |

| Forecast Value | $68.5 Billion |

| CAGR | 7.9% |

The non-wearable biosensor segment accounted for USD 20.7 billion in 2024. These sensors, integrated into diagnostic devices used for point-of-care testing, are valued for their ease of use, high accuracy, and ability to provide immediate results without continuous user interaction. As healthcare providers seek efficient and timely diagnostic tools, the demand for these non-wearable devices is expected to rise. Technological innovations such as improved sensitivity, miniaturization, and digital connectivity enhance their effectiveness and usability in clinical settings.

The electrochemical biosensor segment holds a substantial share of the market, representing 41.6% share, which was USD 13.4 billion in 2024. These biosensors are widely used in medical devices such as glucose meters for diabetic patients and in systems that monitor cardiac biomarkers and blood gases. The increasing prevalence of chronic conditions, including cardiovascular diseases and diabetes, drives the demand for electrochemical sensors as essential diagnostic tools.

United States Biosensors Market generated USD 10.2 billion in 2024, driven by the rising number of chronic disease cases, especially diabetes and heart-related conditions. Despite a strict regulatory environment, the U.S. remains a hub for the development, approval, and commercialization of innovative medical technologies, including biosensors. Regulatory bodies like the FDA are increasingly focused on accelerating the approval process for new biosensor technologies, recognizing their critical role in improving healthcare outcomes.

To strengthen their position in the market, companies are focusing on innovation and partnerships. Many firms invest heavily in R&D to develop more advanced biosensor technologies with greater sensitivity and precision. Collaborations with healthcare providers and research institutions help in driving innovation. Furthermore, some companies are working to expand their product portfolios to cater to various medical needs, such as disease-specific biosensors and wearable health monitoring devices. Market leaders, such as Thermo Fisher Scientific, Masimo, and Danaher, are adopting these strategies to enhance their market presence and remain competitive in this rapidly growing industry.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing application of biosensors in medical field

- 3.2.1.2 Rising prevalence of diabetes globally

- 3.2.1.3 High demand for portable biosensors in Asia Pacific and Europe

- 3.2.1.4 Increasing technological advancements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory scenario

- 3.2.2.2 High cost of product development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Country-wise response

- 3.5.2 Impact on the industry

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (Cost to consumers)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technological landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 5 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Wearable

- 5.3 Non-wearable

Chapter 6 Market Estimates and Forecast, By Technology, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Electrochemical

- 6.3 Optical

- 6.4 Thermal

- 6.5 Piezoelectric

- 6.6 Other technologies

Chapter 7 Market Estimates and Forecast, By Applications, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Blood glucose testing

- 7.3 Cholesterol testing

- 7.4 Blood gas analysis

- 7.5 Pregnancy testing

- 7.6 Drug discovery

- 7.7 Infectious disease testing

- 7.8 Other applications

Chapter 8 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Point of care testing

- 8.3 Home healthcare diagnostics

- 8.4 Research laboratories

- 8.5 Other end users

Chapter 9 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Switzerland

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

Chapter 10 Company Profiles

- 10.1 Abbott Laboratories

- 10.2 ARKRAY

- 10.3 Bio-Rad Laboratories

- 10.4 Biosensors International Group

- 10.5 Dexcom

- 10.6 Danaher

- 10.7 F. Hoffmann-La Roche

- 10.8 Masimo

- 10.9 Nova Biomedical

- 10.10 Platinum Equity Advisors

- 10.11 PHC Holdings

- 10.12 Pinnacle Technology

- 10.13 Siemens Healthineers

- 10.14 Thermo Fisher Scientific

- 10.15 Trividia Health

Table of Contents

Chapter 11 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Base estimates and calculations

- 1.3.1 Base year calculation

- 1.3.2 Key trends for market estimation

- 1.4 Forecast model

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.5.2 Data mining sources

Chapter 12 Executive Summary

- 2.1 Industry 360° synopsis

Chapter 13 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing application of biosensors in medical field

- 3.2.1.2 Rising prevalence of diabetes globally

- 3.2.1.3 High demand for portable biosensors in Asia Pacific and Europe

- 3.2.1.4 Increasing technological advancements

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory scenario

- 3.2.2.2 High cost of product development

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Trump administration tariffs

- 3.5.1 Impact on trade

- 3.5.1.1 Trade volume disruptions

- 3.5.1.2 Country-wise response

- 3.5.2 Impact on the industry

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.2.1.1 Price volatility in key materials

- 3.5.2.1.2 Supply chain restructuring

- 3.5.2.1.3 Production cost implications

- 3.5.2.2 Demand-side impact (Cost to consumers)

- 3.5.2.2.1 Price transmission to end markets

- 3.5.2.2.2 Market share dynamics

- 3.5.2.2.3 Consumer response patterns

- 3.5.2.1 Supply-side impact (Cost of manufacturing)

- 3.5.3 Key companies impacted

- 3.5.4 Strategic industry responses

- 3.5.4.1 Supply chain reconfiguration

- 3.5.4.2 Pricing and product strategies

- 3.5.4.3 Policy engagement

- 3.5.5 Outlook and future considerations

- 3.5.1 Impact on trade

- 3.6 Technological landscape

- 3.7 Future market trends

- 3.8 Gap analysis

- 3.9 Porter's analysis

- 3.10 PESTEL analysis

Chapter 14 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Strategy dashboard

Chapter 15 Market Estimates and Forecast, By Type, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Wearable

- 5.3 Non-wearable

Chapter 16 Market Estimates and Forecast, By Technology, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Electrochemical

- 6.3 Optical

- 6.4 Thermal

- 6.5 Piezoelectric

- 6.6 Other technologies

Chapter 17 Market Estimates and Forecast, By Applications, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Blood glucose testing

- 7.3 Cholesterol testing

- 7.4 Blood gas analysis

- 7.5 Pregnancy testing

- 7.6 Drug discovery

- 7.7 Infectious disease testing

- 7.8 Other applications

Chapter 18 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Point of care testing

- 8.3 Home healthcare diagnostics

- 8.4 Research laboratories

- 8.5 Other end users

Chapter 19 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Russia

- 9.3.7 Switzerland

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 Japan

- 9.4.3 India

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 Middle East and Africa

- 9.6.1 South Africa

- 9.6.2 Saudi Arabia

Chapter 20 Company Profiles

- 10.1 Abbott Laboratories

- 10.2 ARKRAY

- 10.3 Bio-Rad Laboratories

- 10.4 Biosensors International Group

- 10.5 Dexcom

- 10.6 Danaher

- 10.7 F. Hoffmann-La Roche

- 10.8 Masimo

- 10.9 Nova Biomedical

- 10.10 Platinum Equity Advisors

- 10.11 PHC Holdings

- 10.12 Pinnacle Technology

- 10.13 Siemens Healthineers

- 10.14 Thermo Fisher Scientific

- 10.15 Trividia Health