|

시장보고서

상품코드

1750620

구급차 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Ambulance Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

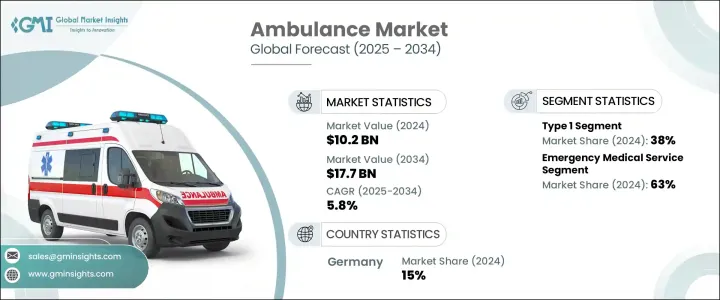

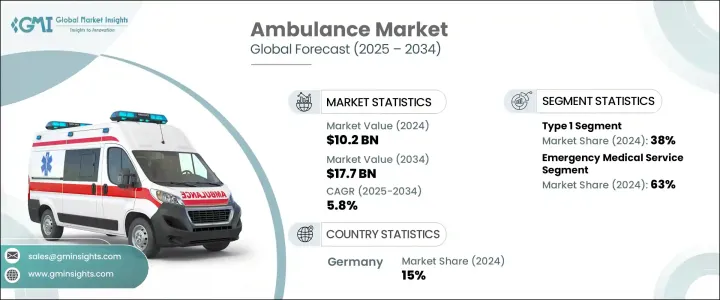

세계의 구급차 시장 규모는 2024년에는 102억 달러에 달하며, 헬스케어 지출의 증가와 응급의료 서비스(EMS)의 중요성 증가를 배경으로 CAGR 5.8%로 성장하며, 2034년에는 177억 달러에 달할 것으로 예측됩니다.

정부와 민간 부문은 구급대원 확충, 대응 시간 개선, 의료 기술 업그레이드에 많은 투자를 하고 있습니다. 이러한 투자는 구급차가 응급상황에 대처할 수 있는 장비를 보강하고 이송 중 환자 치료를 개선하는 데 도움이 되고 있습니다. 그 결과, 구급차에는 인공호흡기, 자동 체외식 제세동기, 자동심폐소생기, 자동제세동기 등 첨단 의료장비가 장착되어 이송 중 심각한 상황에 대처할 수 있게 되었습니다.

기도 관리와 인공호흡기에 대한 중요성이 부각되면서 구급차 시장의 성장을 더욱 촉진하고 있습니다. 인공호흡기는 호흡곤란 환자를 안정시키고 심정지나 심각한 외상 등 응급상황에서 효과적으로 산소를 공급하는 데 매우 중요합니다. 조절 가능한 압력 및 부피 조절과 같은 첨단 기능을 갖춘 이 장비는 구급대원들이 의료 시설로 이송하는 동안 중요한 치료를 제공하는 데 도움이 됩니다. 더 많은 의료 시스템이 고품질 EMS의 가치를 인식함에 따라 더 나은 장비와 전문 구급차에 대한 수요는 계속 증가하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024년 |

| 예측연도 | 2025-2034년 |

| 시작 금액 | 102억 달러 |

| 예측 금액 | 177억 달러 |

| CAGR | 5.8% |

2024년에는 유형 1 구급차가 시장을 주도하며 38%의 점유율을 차지할 것으로 예측됩니다. 이 차량은 일반적으로 트럭 섀시 위에 제작되며, 내구성이 뛰어난 플랫폼과 의료 장비 및 인력을 위한 추가 공간을 갖추고 있습니다. 유형 1 구급차에 대한 선호도가 높아진 것은 대형 사고나 자연재해 등 긴급 상황에 대응할 수 있고, 여러 명의 환자와 대형 장비를 운송할 수 있기 때문입니다.

응급의료 서비스 부문은 2024년 63%의 점유율을 차지할 것으로 예상되는데, 이는 의료 서비스 프로바이더가 중증 환자의 신속하고 안전한 이송을 우선시하고 있기 때문입니다. 원격의료 및 모바일 헬스 솔루션의 발전으로 구급대원들은 환자가 병원에 도착하기 전에 원격으로 의사와 상담하고 치료를 최적화할 수 있는 능력을 더욱 향상시킬 수 있게 되었습니다. 이러한 기술 혁신은 장거리 첨단 이송이 가능한 첨단 구급차에 대한 수요를 증가시킬 것으로 예측됩니다.

독일의 구급차 시장 점유율은 2024년 15%로, 환경 유지에 대한 규제 당국의 강력한 지원과 전기 구급차 채택 확대가 그 요인으로 작용하고 있습니다. 독일은 이산화탄소 배출량을 줄이기 위해 적극적인 노력을 기울이고 있으며, 전기 구급차의 인기가 높아지고 있습니다. 유럽 전역의 환경 규제가 강화되는 가운데, 독일은 엄격한 배기가스 기준을 충족하고 깨끗한 공기에 기여하기 위해 구급차를 포함한 전기자동차를 채택하고 있습니다. 이러한 움직임은 국가의 지속가능성에 대한 광범위한 노력과 일치하며, 친환경 응급의료 서비스(EMS)로의 전환을 선도하는 국가로 자리매김하고 있습니다.

세계 구급차 시장의 주요 기업에는 Braun Industries, NAFFCO, yota, Demers Ambulances, Crestline Ambulance 등이 있습니다. 시장 점유율을 확대하기 위해 기업은 지속가능성 목표를 달성하고 운영 비용을 절감하기 위해 전기 구급차에 투자하고 있습니다. 각 업체들은 실시간 원격의료 및 첨단 모니터링 시스템과 같은 첨단 기술을 차량에 통합하고 있습니다. 서비스 제공 및 차량 관리를 개선하기 위해 의료 서비스 프로바이더 및 정부 기관과의 협력은 기업의 경쟁력을 강화하는 데 도움이 되고 있습니다. 또한 헬스케어 인프라가 빠르게 발전하고 있는 시장으로 진출함으로써 기업은 새로운 수입원을 개발할 수 있게 되었습니다.

목차

제1장 조사 방법과 범위

제2장 개요

제3장 산업 인사이트

- 에코시스템 분석

- 공급업체의 상황

- 원료 공급업체

- 기술 프로바이더

- 제조업체

- 판매 대리점

- 최종 용도

- 이익률 분석

- 트럼프 정권 관세에 대한 영향

- 무역에 대한 영향

- 무역량 혼란

- 타국에 의한 보복 조치

- 산업에 대한 영향

- 주요 원료의 가격 변동

- 공급망 재구축

- 생산비용에 대한 영향

- 영향을 받는 주요 기업

- 전략적 산업 대응

- 공급망 재구성

- 가격결정과 제품 전략

- 전망과 향후 검토 사항

- 무역에 대한 영향

- 기술과 혁신의 상황

- 특허 분석

- 주요 뉴스와 구상

- 규제 상황

- 영향요인

- 촉진요인

- 만성질환과 외상의 증가

- 헬스케어비의 증가

- 구급차 기술의 진보

- 전 세계에서 헬스케어 부문에 대한 투자가 증가

- 산업의 잠재적 리스크·과제

- 높은 운영·유지보수 비용

- 교통 정체와 응답 시간의 지연

- 촉진요인

- 성장 가능성 분석

- Porter의 산업 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추정·예측 : 차량별, 2021-2034년

- 주요 동향

- 유형 1

- 유형 2

- 유형 3

- 중형

제6장 시장 추정·예측 : 용도별, 2021-2034년

- 주요 동향

- 응급의료 서비스

- 소방 구급차

- 기타

제7장 시장 추정·예측 : 유통 채널별, 2021-2034년

- 주요 동향

- OEM

- 애프터마켓

제8장 시장 추정·예측 : 연료별, 2021-2034년

- 주요 동향

- 디젤

- 가솔린

- 전기자동차

제9장 시장 추정·예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주·뉴질랜드

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트

- 사우디아라비아

- 남아프리카공화국

제10장 기업 개요

- Auto Ribeiro

- BAUS AT

- Bollanti

- Braun Industries

- Crestline Ambulance

- Demers Ambulances

- Excellence

- Frazer Ltd

- JCBL Group

- Life Line Emergency Vehicles

- Medicop

- Medix Specialty Vehicles

- Miller Coach Company

- NAFFCO

- O& H Vehicle Technology

- Osage Ambulances

- Profile Vehicles Oy

- REV Group

- Toyota

- WAS

The Global Ambulance Market was valued at USD 10.2 billion in 2024 and is estimated to grow at a CAGR of 5.8% to reach USD 17.7 billion by 2034, driven by the increased healthcare spending and the rising importance of emergency medical services (EMS). Government and private sectors are investing significantly in expanding ambulance fleets, improving response times, and upgrading medical technology. These investments help ensure that ambulances are better equipped to handle emergencies, improving patient care during transport. As a result, ambulances are increasingly equipped with advanced medical equipment, such as ventilators, automated CPR devices, and advanced defibrillators, to manage critical conditions during transit.

The growing emphasis on airway management and ventilators further supports the ambulance market's growth. Ventilators are crucial in stabilizing patients with respiratory distress, ensuring oxygen is delivered effectively during emergencies such as cardiac arrest or severe trauma. With advanced features like adjustable pressure and volume control, these devices help paramedics provide critical care while en route to medical facilities. As more healthcare systems recognize the value of high-quality EMS, demand for better-equipped and specialized ambulances continues to rise.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.2 Billion |

| Forecast Value | $17.7 Billion |

| CAGR | 5.8% |

In 2024, Type 1 ambulances led the market, accounting for 38% share. These vehicles, typically built on a truck chassis, provide a durable platform and additional space for medical equipment and personnel. The growing preference for Type 1 ambulances is driven by their ability to handle emergencies, including large-scale accidents or natural disasters, and their capacity to transport multiple patients or larger equipment.

The EMS segment held a 63% share in 2024, driven by healthcare providers prioritizing rapid, reliable transport of critically ill patients. Advances in telemedicine and mobile health solutions have further improved EMS capabilities, enabling paramedics to consult with doctors remotely and optimize care before patients arrive at the hospital. These innovations are expected to increase the demand for more advanced ambulances capable of longer-distance, high-level care during transport.

Germany Ambulance Market held a 15% share in 2024, fueled by strong regulatory support for environmental sustainability and the growing adoption of electric ambulances. The country is taking proactive steps to reduce its carbon footprint, making electric ambulances an increasingly popular choice. As environmental regulations tighten across Europe, Germany has embraced electric vehicles, including ambulances, to meet stringent emission standards and contribute to cleaner air. This move aligns with the nation's broader commitment to sustainability and has positioned it as a leader in the transition toward eco-friendly emergency medical services (EMS).

Key players in the Global Ambulance Market include Braun Industries, NAFFCO, Toyota, Demers Ambulances, and Crestline Ambulance. To expand their market footprint, companies are investing in electric ambulances to meet sustainability goals and reduce operational costs. They integrate cutting-edge technologies like real-time telemedicine and advanced monitoring systems into their vehicles. Collaborations with healthcare providers and government agencies to improve service delivery and fleet management are helping companies enhance their competitive advantage. Additionally, expanding into emerging markets where healthcare infrastructure is rapidly developing has allowed companies to tap into new revenue streams.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Supplier landscape

- 3.2.1 Raw material suppliers

- 3.2.2 Technology providers

- 3.2.3 Manufacturers

- 3.2.4 Distributors

- 3.2.5 End use

- 3.3 Profit margin analysis

- 3.4 Trump administration tariffs

- 3.4.1 Impact on trade

- 3.4.1.1 Trade volume disruptions

- 3.4.1.2 Retaliatory measures by other countries

- 3.4.2 Impact on the industry

- 3.4.2.1 Price Volatility in key materials

- 3.4.2.2 Supply chain restructuring

- 3.4.2.3 Production cost implications

- 3.4.3 Key companies impacted

- 3.4.4 Strategic industry responses

- 3.4.4.1 Supply chain reconfiguration

- 3.4.4.2 Pricing and product strategies

- 3.4.5 Outlook and future considerations

- 3.4.1 Impact on trade

- 3.5 Technology & innovation landscape

- 3.6 Patent analysis

- 3.7 Key news & initiatives

- 3.8 Regulatory landscape

- 3.9 Impact forces

- 3.9.1 Growth drivers

- 3.9.1.1 Rise in chronic diseases and trauma cases

- 3.9.1.2 Rising healthcare expenditure

- 3.9.1.3 Advancements in ambulance technology

- 3.9.1.4 Growing investments in the healthcare sector across the globe

- 3.9.2 Industry pitfalls & challenges

- 3.9.2.1 High operational and maintenance cost

- 3.9.2.2 Traffic congestion and delayed response times

- 3.9.1 Growth drivers

- 3.10 Growth potential analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Bn, Units)

- 5.1 Key trends

- 5.2 Type 1

- 5.3 Type 2

- 5.4 Type 3

- 5.5 Medium-duty

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 ($Bn, Units)

- 6.1 Key trends

- 6.2 Emergency medical service

- 6.3 Fire ambulances

- 6.4 Others

Chapter 7 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Bn, Units)

- 7.1 Key trends

- 7.2 OEM

- 7.3 Aftermarket

Chapter 8 Market Estimates & Forecast, By Fuel, 2021 - 2034 ($Bn, Units)

- 8.1 Key trends

- 8.2 Diesel

- 8.3 Gasoline

- 8.4 Electric vehicles

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Bn, Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.3.7 Nordics

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 ANZ

- 9.4.6 Southeast Asia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Auto Ribeiro

- 10.2 BAUS AT

- 10.3 Bollanti

- 10.4 Braun Industries

- 10.5 Crestline Ambulance

- 10.6 Demers Ambulances

- 10.7 Excellence

- 10.8 Frazer Ltd

- 10.9 JCBL Group

- 10.10 Life Line Emergency Vehicles

- 10.11 Medicop

- 10.12 Medix Specialty Vehicles

- 10.13 Miller Coach Company

- 10.14 NAFFCO

- 10.15 O&H Vehicle Technology

- 10.16 Osage Ambulances

- 10.17 Profile Vehicles Oy

- 10.18 REV Group

- 10.19 Toyota

- 10.20 WAS