|

시장보고서

상품코드

1755208

용접 소모품 시장 : 기회, 촉진 요인, 업계 동향 분석, 예측(2025-2034년)Welding Consumables Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

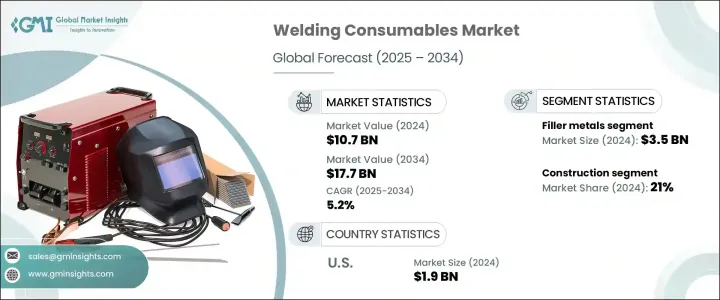

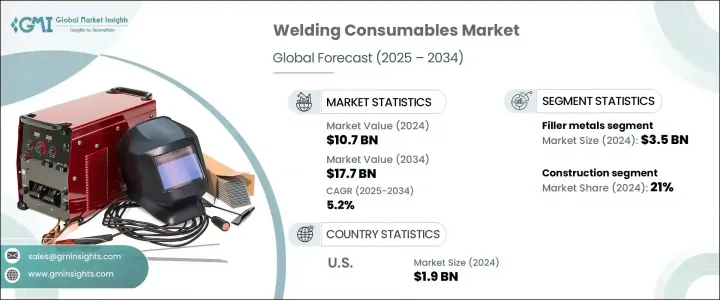

용접 소모품 세계 시장 규모는 2024년에 107억 달러로 평가되었고, CAGR 5.2%로 성장하여 2034년에는 177억 달러에 이를 것으로 예측되고 있습니다.

이 성장을 견인하고 있는 것은 산업용도에 있어서의 자동화나 로봇 도입 증가에 수반하는 인프라나 건설 프로젝트에 있어서의 용접 소모품 수요 증가입니다. 신흥 시장에서 자동차 부문의 확대도 시장 성장에 기여하고 있습니다.

이러한 지역의 산업 부문이 계속 번영함에 따라 용접의 필요성이 높아지고 시장에 새로운 기회가 탄생하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 107억 달러 |

| 예측 금액 | 177억 달러 |

| CAGR | 5.2% |

필러메탈의 2024년 시장 점유율은 35억 달러로 가장 컸으며, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 5.6%로 성장할 것으로 예측됩니다. 필러 메탈 수요는 파이프라인 부설, 중기계 생산, 해양 가공 등의 업계의 진화하는 요구에 대응하기 위해, 제조업체가 혁신적인 제품을 도입함에 따라 높아지고 있습니다.

건설 분야는 2024년에 21%의 점유율을 차지하며, 2025년부터 2034년까지 연평균 복합 성장률(CAGR) 5.9%로 성장할 것으로 예측됩니다. 대규모 건설 프로젝트와 금속 사용량 증가로 인해 용접은 건물과 인프라의 구조적 무결성을 보장하는 데 중요한 역할을 합니다. 이 분야에 있어서의 용접 소모품 수요는 건설 업계 전체의 성장과 밀접하게 연결되어 있어 용접은 조립식으로도 현장에서의 조립 작업에서도 중요한 역할을 하고 있습니다.

미국의 용접 소모품 시장은 77%의 점유율을 차지했으며, 2024년 시장 규모는 19억 달러였습니다. 협동 용접 로봇(코봇)은 인간의 용접공을 보조하기 위해 제조 시설에서 사용되는 것이 늘어나고 있으며, 용접 공정을 보다 효율적이고 정확한 것으로 하고 있습니다.

용접 소모품 세계 시장에서 사업을 전개하는 주요 기업은 링컨 일렉트릭, 파나소닉, ESAB, D&H Secheron, 미러 일렉트릭, 고베 제강소, 현대 웰딩, Ador Welding, Hobart Welding Products, Berkenhoff, EWM, Welding Alloy Welding, Nouveaux 등이 있습니다. 용접 소모품 시장에서의 지위를 강화하기 위해 각 회사는 기계적 및 화학적 특성을 강화한 새로운 필러 금속 개발 등 제품 제공에 있어서의 기술적 진보에 주력하고 있습니다. 또한 제조업체는 자동차 및 건설 분야에서 특히 높은 맞춤형 솔루션의 요구를 충족시키는 제품을 개발하기 위해 연구 개발에 많은 투자를 하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 밸류체인에 영향을 주는 요인

- 이익률 분석

- 혁신

- 장래의 전망

- 제조업자

- 리셀러

- 공급자의 상황

- 주요 뉴스와 대처

- 규제 상황

- 가격 동향 분석

- 영향요인

- 성장 촉진요인

- 인프라와 건설 프로젝트의 급증

- 자동차 및 제조업의 성장

- 업계의 잠재적 위험 및 과제

- 원재료 가격 변동

- 지정학적 및 무역 장벽

- 성장 촉진요인

- 성장 가능성 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

제5장 시장 추정 및 예측 : 유형별, 2021년-2034년

- 주요 동향

- 전극

- 실드 메탈 아크 용접 전극

- 가스 메탈 아크 용접 전극

- 기타

- 플럭스

- 서브 머지 아크 용접 플럭스

- 산소 연료 용접 플럭스

- 기타(브레이징용 플럭스 등)

- 가스

- 실드 가스

- 보조가스

- 기타

- 필러 메탈

- 단선

- 플럭스가 들어있는 와이어

- 금속심선

- 용접봉

- 기타(특수 필러 금속 등)

- 기타

제6장 시장 추정 및 예측 : 재료별, 2021년-2034년

- 주요 동향

- 연강

- 스테인레스 스틸

- 알루미늄

- 니켈 합금

- 구리 합금

- 기타(코발트 합금 등)

제7장 시장 추정 및 예측 : 최종 이용 산업별, 2021년-2034년

- 주요 동향

- 건설

- 자동차

- 에너지

- 조선

- 항공우주

- 중공업

- 기타(방어 등)

제8장 시장 추정 및 예측 : 유통 채널별, 2021년-2034년

- 주요 동향

- 직접 판매

- 간접판매

제9장 시장 추정 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

제10장 기업 프로파일

- Ador Welding

- Berkenhoff

- D&H Secheron

- Diffusion Engineers

- ESAB

- EWM

- Hilco Welding

- Hobart Welding Products

- Hyundai Welding

- Kobe Steel

- Lincoln Electric

- Miller Electric

- Nouveaux

- Panasonic

- Welding Alloys

The Global Welding Consumables Market was valued at USD 10.7 billion in 2024 and is estimated to grow at a CAGR of 5.2% to reach USD 17.7 billion by 2034. This growth is driven by the increasing demand for welding consumables in infrastructure and construction projects with the rising adoption of automation and robotics in industrial applications. Additionally, the growing preference for eco-friendly welding materials and the expansion of the automotive sector in emerging markets are further contributing to market growth. In developing nations, urbanization and rising disposable incomes are expected to lead to significant investments in infrastructure, which in turn will fuel the demand for welding consumables.

As the industrial sector in these regions continues to thrive, the need for welding will grow, creating new opportunities in the market. Advances in welding technology, such as the development of stronger, more durable materials, are also supporting market growth. The automotive sector, particularly in both developed and emerging economies, is seeing a rise in the application of welding processes as manufacturers demand more custom-made products.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $10.7 Billion |

| Forecast Value | $17.7 Billion |

| CAGR | 5.2% |

Filler metals held the largest market share in 2024, generating USD 3.5 billion, and is expected to grow at a CAGR of 5.6% between 2025 and 2034. The demand for filler metals is rising as manufacturers introduce innovative products to meet the evolving needs of industries like pipeline installation, heavy machinery production, and offshore fabrication. These industries are increasingly turning to higher-strength materials to improve the durability and performance of their products.

The construction segment held a 21% share in 2024 and is expected to grow at a CAGR of 5.9% from 2025 to 2034. Welding is an essential process in construction, especially in the fabrication of structural metal frameworks. With large-scale construction projects and increasing metal usage, welding plays a critical role in ensuring the structural integrity of buildings and infrastructure. The demand for welding consumables in this sector is closely tied to the growth of the overall construction industry, with welding playing a significant role in both prefabricated and on-site assembly work.

United States Welding Consumables Market held a 77% share and was valued at USD 1.9 billion in 2024. The surge in infrastructure development, coupled with the adoption of robotics and automation in manufacturing, is propelling the growth of this market. In addition to robotics, collaborative welding robots (cobots) are increasingly being used in manufacturing facilities to assist human welders, making welding processes more efficient and precise. The demand for eco-friendly consumables and the automotive sector's expansion in emerging regions are also contributing to market growth in the U.S.

Key players operating in the Global Welding Consumables Market include Lincoln Electric, Panasonic, ESAB, D&H Secheron, Miller Electric, Kobe Steel, Hyundai Welding, Ador Welding, Hobart Welding Products, Berkenhoff, EWM, Welding Alloys, Diffusion Engineers, Hilco Welding, and Nouveaux. To strengthen their position in the welding consumables market, companies are focusing on technological advancements in their product offerings, such as the development of new filler metals with enhanced mechanical and chemical properties. They are also emphasizing eco-friendly solutions to cater to the growing demand for sustainable practices in manufacturing. Additionally, manufacturers are investing heavily in R&D to develop products that meet the increasing need for customized solutions, especially in the automotive and construction sectors. Expanding their presence in emerging markets and focusing on automation and robotics are also key strategies, enabling companies to improve production efficiency while reducing labor costs.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Research design

- 1.1.1 Research approach

- 1.1.2 Data collection methods

- 1.2 Base estimates and calculations

- 1.2.1 Base year calculation

- 1.2.2 Key trends for market estimates

- 1.3 Forecast model

- 1.4 Primary research & validation

- 1.4.1 Primary sources

- 1.4.2 Data mining sources

- 1.5 Market definitions

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 - 2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Factor affecting the value chain.

- 3.1.2 Profit margin analysis.

- 3.1.3 Disruptions

- 3.1.4 Future outlook

- 3.1.5 Manufactures

- 3.1.6 Distributors

- 3.2 Supplier landscape

- 3.3 Key news & initiatives

- 3.4 Regulatory landscape

- 3.5 Pricing trend analysis

- 3.6 Impact forces

- 3.6.1 Growth drivers

- 3.6.1.1 Surge in infrastructure and construction projects

- 3.6.1.2 Growth in automotive and manufacturing sectors

- 3.6.2 Industry pitfalls & challenges

- 3.6.2.1 Fluctuating raw material prices

- 3.6.2.2 Geopolitical and trade barriers

- 3.6.1 Growth drivers

- 3.7 Growth potential analysis

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Competitive positioning matrix

- 4.4 Strategic outlook matrix

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 ($Billion, Million Units)

- 5.1 Key trends

- 5.2 Electrodes

- 5.2.1 Shielded metal arc welding electrodes

- 5.2.2 Gas metal arc welding electrodes

- 5.2.3 Others

- 5.3 Fluxes

- 5.3.1 Submerged arc welding flux

- 5.3.2 Oxy-fuel welding flux

- 5.3.3 Others (brazing flux etc.)

- 5.4 Gases

- 5.4.1 Shielding Gases

- 5.4.2 Backing Gases

- 5.4.3 Others

- 5.5 Filler metals

- 5.5.1 Solid wire

- 5.5.2 flux-cored wire

- 5.5.3 Metal cored wire

- 5.5.4 Welding rods

- 5.5.5 Others (specialty filler metals etc.)

- 5.6 Others

Chapter 6 Market Estimates & Forecast, By Material Type, 2021 - 2034 ($Billion, Million Units)

- 6.1 Key trends

- 6.2 Mild steel

- 6.3 Stainless steel

- 6.4 Aluminum

- 6.5 Nickel alloys

- 6.6 Copper alloys

- 6.7 Others (cobalt alloys etc.)

Chapter 7 Market Estimates & Forecast, By End Use Industry, 2021 - 2034 ($Billion, Million Units)

- 7.1 Key trends

- 7.2 Construction

- 7.3 Automobile

- 7.4 Energy

- 7.5 Shipbuilding

- 7.6 Aerospace

- 7.7 Heavy engineering

- 7.8 Others (defense etc.)

Chapter 8 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Billion, Million Units)

- 8.1 Key trends

- 8.2 Direct sales

- 8.3 Indirect sales

Chapter 9 Market Estimates & Forecast, By Region, 2021 - 2034 ($Billion, Million Units)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 UK

- 9.3.2 Germany

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Russia

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 South Korea

- 9.4.5 Australia

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.6 MEA

- 9.6.1 UAE

- 9.6.2 Saudi Arabia

- 9.6.3 South Africa

Chapter 10 Company Profiles

- 10.1 Ador Welding

- 10.2 Berkenhoff

- 10.3 D&H Secheron

- 10.4 Diffusion Engineers

- 10.5 ESAB

- 10.6 EWM

- 10.7 Hilco Welding

- 10.8 Hobart Welding Products

- 10.9 Hyundai Welding

- 10.10 Kobe Steel

- 10.11 Lincoln Electric

- 10.12 Miller Electric

- 10.13 Nouveaux

- 10.14 Panasonic

- 10.15 Welding Alloys