|

시장보고서

상품코드

1755354

밀렛 시장 : 기회, 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Millets Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

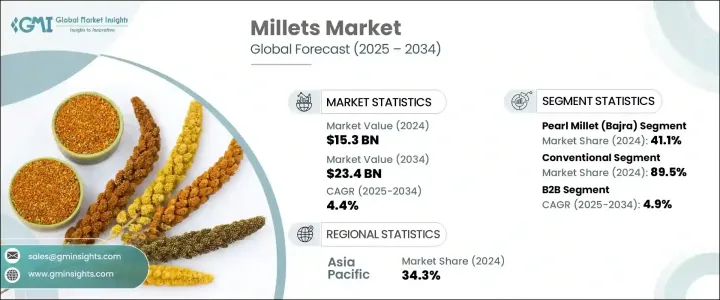

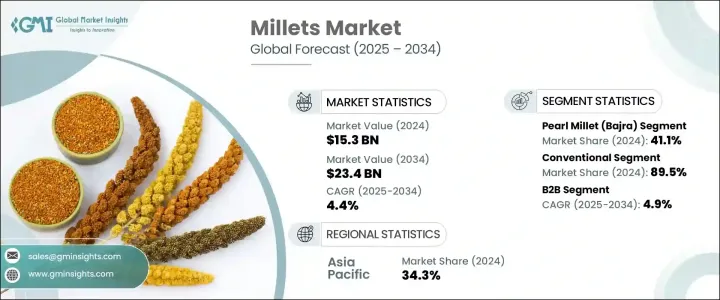

세계의 밀렛 시장은 2024년에는 153억 달러로 평가되었으며 2034년에는 234억 달러에 이를 것으로 추정되며, CAGR 4.4%로 성장할 전망입니다.

이러한 성장은 주로 섬유질과 단백질이 풍부한 건강에 좋은 글루텐이 함유되지 않은 식품에 대한 소비자의 관심이 높아진 데 기인합니다. 밀렛의 영양적 이점에 대한 인식이 높아짐에 따라 밀렛이 현대 식단에 포함되는 경우가 점점 더 많아지고 있습니다. 소비자들은 밀렛를 전통적인 소비 목적뿐 아니라 기능성 식품, 웰니스 다이어트, 지속 가능한 식품 실천의 일환으로 선택하고 있습니다. 최근 몇 년간 밀렛는 베이커리 제품, 스낵, 음료 등 다양한 신규 응용 분야에서 자리를 잡았으며, 건강 혜택뿐 아니라 향상된 텍스처와 맛을 제공한다는 점에서 주목받고 있습니다.

혹독한 기후 조건을 견딜 수 있는 능력 덕분에 물이 부족한 지역에서도 신뢰할 수 있는 식량 원천이 되어 식량 안보에 대한 중요성이 더욱 커지고 있습니다. 가공 및 제품 개발의 혁신은 전 세계적으로 밀렛 소비를 계속 촉진하고 있습니다. 식품 시스템 전반에 걸쳐 지속 가능성이 더욱 중요해짐에 따라 밀렛은 환경 친화적인 식단에 이상적인 기후 스마트 곡물로 인정받고 있습니다. 도시 시장에서 지속 가능한 식물성 식품에 대한 수요가 증가하면서 시장의 장기적인 성장 추세가 더욱 강화되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 153억 달러 |

| 예측 금액 | 234억 달러 |

| CAGR | 4.4% |

지원적인 정책 프레임워크와 제도적 인센티브가 이 시장을 계속해서 부추기고 있습니다. 밀렛을 홍보하기 위한 여러 가지 전 세계적 노력이 밀렛 기반 식품 산업에 대한 인식을 높이고 투자를 촉진하는 데 크게 기여했습니다. 정부와 농업 기관은 재정 지원 제공, 가치 사슬 인프라 구축, 밀렛 제품 개발을 위한 창업 지원 등을 통해 밀렛 재배를 장려하고 있습니다. 이러한 조치들은 농민을 지원하는 동시에 국내 및 국제 시장에서의 유통 효율성을 높이고 접근성을 확대하는 데 기여합니다.

2024년 기준 유형별 시장에서는 진주 밀렛이 41.1%의 점유율을 차지하며 시장 규모 $6.3억 달러를 기록했습니다. 각 밀렛 품종은 영양 성분과 다양한 식단에 대한 적합성에 따라 고유한 가치를 가지고 있습니다. 일부는 높은 단백질 또는 칼슘 함량으로 인기가 있는 반면, 다른 일부는 글루텐이 함유되지 않은 비건 식단에 사용될 수 있어 관심을 받고 있습니다. 전 세계적으로 클린 라벨 및 알레르기 유발 성분이 없는 식품에 대한 수요가 계속 증가함에 따라, 이러한 곡물은 여러 지역에서 강력한 성장 기회를 확보하고 있습니다.

자연에 기반한 2024년에는 기존 밀렛이 89.5%의 점유율을 차지하며 우위를 차지할 것으로 예상되며, 예측 기간 동안 5.8%의 높은 CAGR로 성장할 것으로 예상됩니다. 이 부문은 저렴한 가격과 쉽게 구할 수 있는 특성으로 인해 계속해서 폭넓은 소비자층에 어필하고 있습니다. 그러나 유기농 밀렛 부문도 특히 화학 물질이 없는 친환경 식품을 찾는 소비자가 많은 도시 시장에서 관심이 증가하고 있습니다. 지속 가능한 농업을 촉진하는 정부 프로그램도 유기농 밀렛의 매력을 높이고 있습니다. 유기농 밀렛은 현재 시장 점유율이 낮지만, 깨끗한 영양에 대한 수요가 증가함에 따라 특히 고급 소매점과 건강에 민감한 인구층에서 보급률이 높아질 것으로 예상됩니다.

형태별로 구분하면, 통곡물이 2024년에 전체 시장 점유율의 39.7%를 차지하며, 풍부한 영양과 최소한의 가공으로 높은 관련성을 유지할 것으로 보입니다. 밀렛은 쿠키, 빵, 건강 스낵 등 글루텐이 함유되지 않은 제빵 제품에 다양한 용도로 사용될 수 있는 재료로 전 세계적으로 인기를 끌고 있습니다. 플레이크는 현대의 편리함을 중시하는 소비 패턴에 부합하여 아침 시리얼과 스낵바에 점점 더 많이 사용되고 있습니다. 식습관의 변화에 따라 밀렛을 사용한 즉석 조리 식품 및 즉석 섭취 식품에 대한 수요도 증가하고 있으며, 이는 제조업체들이 소매 매장에 다양한 제품군을 출시할 기회를 제공하고 있습니다.

B2B 부문은 2034년까지 연평균 4.9%의 성장률을 보이며 빠르게 확장되고 있습니다. 이러한 성장은 다양한 용도로 기능적이고 지속 가능한 원료로 밀렛을 통합하는 식품 제조업체, 기관 구매자 및 동물 사료 생산자의 수요 증가에 의해 촉진되고 있습니다. 밀렛이 포장 식품, 학교 급식 프로그램 및 개인 상표 건강 식품에 통합됨에 따라 대규모 조달 기회가 열리고 있습니다. 더 많은 산업이 밀렛의 건강 및 지속 가능성 이점을 활용함에 따라 B2B 부문은 강력한 모멘텀을 보일 것으로 예상됩니다.

지역별로는 아시아태평양 지역이 높은 생산량과 국내 소비 증가에 힘입어 2024년에 34.3%의 가장 큰 매출 점유율을 차지했습니다. 이 지역은 역사적인 재배 패턴과 건강에 대한 인식이 높아짐에 따라 밀렛의 거점으로 계속 남아 있습니다. 도시화, 소득 증가, 농업 지원 정책은 밀렛의 사용을 전통적인 식단뿐만 아니라 현대적인 식품 혁신 분야로 확대시키고 있습니다.

밀렛 시장 주요 기업들은 시장 점유율을 확대하고 브랜드 위치를 강화하기 위해 전략적 이니셔티브를 적극적으로 추진하고 있습니다. 선도 기업들은 소비자의 변화하는 선호도에 맞춰 밀렛 기반 즉석 식사, 스낵, 아침 시리얼, 글루텐 프리 베이커리 제품 등을 출시하며 제품 혁신에 투자하고 있습니다. 많은 기업들은 식품 기술 스타트업과 연구 기관과 협력해 영양 밀도가 높고 유통 기한을 연장하며 맛을 개선하면서도 곡물의 자연적 혜택을 유지하는 포뮬러를 개발하고 있습니다. 소매 체인과 전자상거래 플랫폼과의 전략적 파트너십도 일반화되고 있어 제품의 가시성과 소비자 접근성을 확대하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 업계의 잠재적 위험 및 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품별

- 장래 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)

(참고 : 무역 통계는 주요 국가에서만 제공됩니다)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경 측면

- 지속가능한 관행

- 폐기물 삭감 전략

- 생산에 있어서의 에너지 효율

- 환경 친화적 인 노력

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 유형별(2021-2034년)

- 주요 동향

- 진주 밀렛(바쥬라)

- 손가락 밀렛(라기)

- 폭스테일 밀렛

- 프로소 밀렛

- 사탕수수(조와르)

- 헛간 밀렛

- 코도 기장

- 리틀 밀렛

- 기타

제6장 시장 추계 및 예측 : 성질별(2021-2034년)

- 주요 동향

- 유기농

- 기존

제7장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 식품

- 베이커리 제품

- 아침 시리얼 및 죽

- 스낵 및 짭짤한 제품

- 유아용 식품

- 전통 식품

- 기타

- 음료

- 알코올 음료

- 무알코올 음료

- 동물사료

- 가금류 사료

- 소 사료

- 기타

- 기능성 식품 및 영양보조식품

- 기타

제8장 시장 추계 및 예측 : 형태별(2021-2034년)

- 주요 동향

- 통곡물

- 밀가루

- 플레이크

- 조리용

- 즉석식

- 기타

제9장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- B2B

- 식품 제조업체

- 동물사료 산업

- HoReCa(호텔 및 레스토랑 및 카페)

- 기타

- B2C

- 슈퍼마켓 및 대형 슈퍼마켓

- 전문점

- 편의점

- 온라인 소매

- 기타

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제11장 기업 프로파일

- Nestle SA

- Archer Daniels Midland Company

- Cargill, Incorporated

- Bunge Limited

- Kellogg Company

- PepsiCo, Inc.(Quaker Oats)

- General Mills, Inc.

- Britannia Industries Ltd.

- ITC Limited

- Patanjali Ayurved Limited

- Organic India Pvt. Ltd.

- 24 Mantra Organic(Sresta Natural Bioproducts)

- Nature's Path Foods

- Bob's Red Mill Natural Foods

- Arrowhead Mills(Hain Celestial Group)

The Global Millets Market was valued at USD 15.3 billion in 2024 and is estimated to grow at a CAGR of 4.4% to reach USD 23.4 billion by 2034. This growth is largely driven by rising consumer interest in healthy, gluten-free foods rich in fiber and protein. With increasing awareness about the nutritional benefits of millets, their inclusion in modern diets is becoming more common. Consumers are turning to millets not just for traditional consumption but also for their role in functional foods, wellness diets, and sustainable food practices. In recent years, millets have found a place in a wide range of new applications, especially in baked goods, snacks, and beverages, where they offer not just health benefits but also improved texture and taste.

Their ability to withstand harsh climatic conditions also makes them a reliable food source in regions with limited water availability, reinforcing their importance for food security. Innovations in processing and product development continue to drive millet consumption globally. As sustainability becomes a stronger focus across food systems, millets are being recognized as climate-smart grains, ideal for environmentally-conscious diets. Growing demand in urban markets for sustainable and plant-based food products further supports the market's long-term trajectory.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $15.3 Billion |

| Forecast Value | $23.4 Billion |

| CAGR | 4.4% |

Supportive policy frameworks and institutional incentives continue to fuel this market. Several global efforts to promote millet have significantly contributed to building awareness and driving investment in millet-based food industries. Governments and agricultural bodies are encouraging millet cultivation by offering financial support, creating value-chain infrastructure, and fostering entrepreneurship in millet product development. Such measures not only support farmers but also help streamline distribution and widen accessibility for both domestic and international markets.

By type, pearl millet led the market in 2024, holding a share of 41.1%, which equates to a market size of USD 6.3 billion. Each millet variety holds unique value based on its nutrient profile and suitability for different diets. While some are favored for their high protein or calcium content, others are gaining interest for their use in gluten-free and vegan diets. As global demand continues to shift towards clean-label and allergen-friendly foods, these grains are securing strong growth opportunities across regions.

Based on nature, in 2024, conventional millets dominated with an 89.5% share and are expected to grow at a higher CAGR of 5.8% during the forecast period. This segment continues to appeal to a broader consumer base due to affordability and easy availability. However, the organic millet segment is also witnessing increased interest, especially in urban markets where consumers are seeking chemical-free and eco-friendly food options. Government programs that promote sustainable agriculture are also enhancing the appeal of organically produced millets. Although organic millets currently occupy a smaller share, rising demand for clean nutrition is expected to boost their penetration, particularly in premium retail spaces and health-conscious demographics.

When segmented by form, the whole grain accounted for 39.7% of the total market share in 2024, maintaining strong relevance due to its nutritional richness and minimal processing. Millet flour continues to gain popularity globally as a versatile ingredient in gluten-free bakery products, including cookies, breads, and health snacks. Flakes are increasingly favored for breakfast cereals and snack bars, reflecting the market's alignment with modern, convenience-driven consumption patterns. With evolving dietary habits, the demand for millet-based ready-to-cook and ready-to-eat offerings is also rising, providing manufacturers the opportunity to introduce diverse product lines across retail shelves.

The B2B segment is expanding rapidly, with a projected CAGR of 4.9% through 2034. This growth is driven by increased demand from food manufacturers, institutional buyers, and animal feed producers who are integrating millet as a functional and sustainable ingredient in a wide variety of applications. The integration of millets into packaged foods, school meal programs, and private-label health foods is opening up large-scale procurement opportunities. As more industries tap into the health and sustainability benefits of millets, the B2B segment is expected to witness strong momentum.

Regionally, Asia Pacific held the largest revenue share in 2024 at 34.3%, fueled by high production and rising domestic consumption. The region continues to be a stronghold for millets due to historical cultivation patterns and increasing health awareness. Urbanization, rising incomes, and supportive agriculture policies are boosting millet usage not only in traditional diets but also in contemporary food innovations.

Key players in the millets market are actively implementing strategic initiatives to expand their market footprint and strengthen brand positioning. Leading companies are investing in product innovation by launching millet-based ready-to-eat meals, snacks, breakfast cereals, and gluten-free bakery items to cater to evolving consumer preferences. Many are collaborating with food tech startups and research institutions to develop nutrient-dense formulations that enhance shelf life and taste while retaining the grains' natural benefits. Strategic partnerships with retail chains and e-commerce platforms are also becoming common, allowing broader product visibility and consumer reach.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 End use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code)

( Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Pearl millet (Bajra)

- 5.3 Finger millet (Ragi)

- 5.4 Foxtail millet

- 5.5 Proso millet

- 5.6 Sorghum (Jowar)

- 5.7 Barnyard millet

- 5.8 Kodo millet

- 5.9 Little millet

- 5.10 Others

Chapter 6 Market Estimates and Forecast, By Nature, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Organic

- 6.3 Conventional

Chapter 7 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Food

- 7.2.1 Bakery products

- 7.2.2 Breakfast cereals & porridges

- 7.2.3 Snacks & savory products

- 7.2.4 Infant food

- 7.2.5 Traditional foods

- 7.2.6 Others

- 7.3 Beverages

- 7.3.1 Alcoholic beverages

- 7.3.2 Non-alcoholic beverages

- 7.4 Animal feed

- 7.4.1 Poultry feed

- 7.4.2 Cattle feed

- 7.4.3 Others

- 7.5 Nutraceuticals & dietary supplements

- 7.6 Others

Chapter 8 Market Estimates and Forecast, By Form, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 Whole grain

- 8.3 Flour

- 8.4 Flakes

- 8.5 Ready-to-cook

- 8.6 Ready-to-eat

- 8.7 Others

Chapter 9 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 B2B

- 9.2.1 Food manufacturers

- 9.2.2 Animal feed industry

- 9.2.3 HoReCa (Hotels, Restaurants, Cafes)

- 9.2.4 Others

- 9.3 B2C

- 9.3.1 Supermarkets & Hypermarkets

- 9.3.2 Specialty stores

- 9.3.3 Convenience stores

- 9.3.4 Online retail

- 9.3.5 Others

Chapter 10 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Netherlands

- 10.3.7 Rest of Europe

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Rest of Asia Pacific

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.5.4 Rest of Latin America

- 10.6 Middle East and Africa

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

- 10.6.4 Rest of Middle East and Africa

Chapter 11 Company Profiles

- 11.1 Nestle S.A.

- 11.2 Archer Daniels Midland Company

- 11.3 Cargill, Incorporated

- 11.4 Bunge Limited

- 11.5 Kellogg Company

- 11.6 PepsiCo, Inc. (Quaker Oats)

- 11.7 General Mills, Inc.

- 11.8 Britannia Industries Ltd.

- 11.9 ITC Limited

- 11.10 Patanjali Ayurved Limited

- 11.11 Organic India Pvt. Ltd.

- 11.12 24 Mantra Organic (Sresta Natural Bioproducts)

- 11.13 Nature's Path Foods

- 11.14 Bob's Red Mill Natural Foods

- 11.15 Arrowhead Mills (Hain Celestial Group)