|

시장보고서

상품코드

1766303

세포주 개발 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Cell Line Development Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

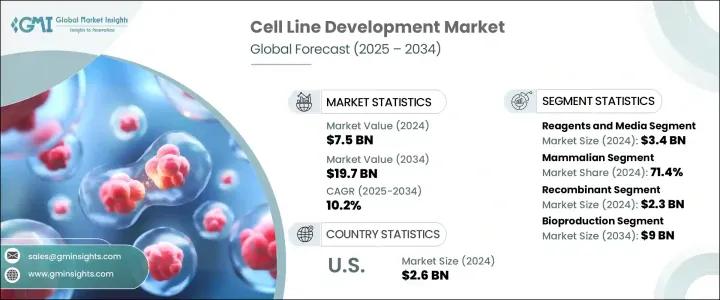

세계의 세포주 개발 시장 규모는 2024년 75억 달러로, CAGR 10.2%로 성장해, 2034년까지 197억 달러에 이를 것으로 추정됩니다.

특히 제약업계가 맞춤형 치료나 정밀의료로 시프트하는 가운데, 생물제제나 바이오시밀러에 대한 주목이 높아지고 있는 것이 시장 확대에 박차를 가하고 있습니다. 암, 감염증 등의 만성 질환 증가에 의해 생물학적 제제의 채용이 증가하고 있어 이러한 제제는 충분히 특성화된 세포주에 크게 의존하고 있습니다. 이 때문에 품질 관리된 생산 시스템의 필요성도 높아지고 있습니다.

중소규모의 생명공학 기업들은 오버헤드 비용을 줄이고 일정을 늘리기 위해 CDMO에 아웃소싱하는 것이 늘어나고 있으며, CDMO의 기술적 전문 지식, 확장 가능한 플랫폼, FDA와 같은 규제 당국에 대한 컴플라이언스의 혜택을 받고 있습니다. 세포주 스크리닝, 클론 선택, 프로세스 최적화, GMP 제조 등의 엔드 투 엔드 서비스에 CDMO를 활용할 수 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 75억 달러 |

| 예측 금액 | 197억 달러 |

| CAGR | 10.2% |

시약 및 배지 부문은 2024년 34억 달러를 만들어 냈습니다. 이 부문은 연구 개발 단계와 생산 단계 모두에서 세포의 증식과 유지에 중심적인 역할을 하기 때문에 계속 우위를 차지하고 있습니다. 무단백질 배지와 무혈청 배지에 대한 선호도 증가는 대규모 생산 환경에서의 확장성 향상, 오염 위험 감소, 일관성을 제공하며, 이 부문의 견인 역할이 되고 있습니다.

세포 유형별로 포유류 세포가 2024년에 71.4%를 차지했으며, 가장 높은 수익을 올렸습니다. 글리코실화, 확장성으로 인해 생물제제의 생산에 선호되고 있습니다.

미국의 세포주 개발 시장은 2024년에는 26억 달러로 평가되어 바이오파마의 고도의 인프라, 만성 질환의 높은 발생률, 최첨단 생물학적 치료의 강력한 채용이 그 원동력이 되고 있습니다. 미국의 각지의 연구기관이나 혁신 허브도 유전자 편집과 자동화 플랫폼의 기술적 진보를 가속시키고 있으며, 개발 사이클의 신속화와 효율화로 이어지고 있습니다.

세계의 세포주 개발 시장에서 사업을 전개하고 있는 주요 기업으로는 PromoCell, Novartis, Genscript Biotech, Sartorius, Thermo Fisher Scientific, ProBioGen, Cytiva(Danaher Corporation), ASIMOV, Advanced Instruments, Sigma Aldrich(Merck KGaA), EurofinsA Sciences, Fyonibio, Lonza Group 등이 있습니다. 세포주 개발 분야의 주요 기업은 자동 세포 스크리닝 플랫폼, 일회용 바이오 리액터, CRISPR 기반의 유전자 편집 등의 기술 혁신에 많은 투자를 실시했습니다. 서비스 제공의 강화와 생산 능력의 확대를 도모하고 있습니다. 또, 신규 기술을 통합하거나 지역적인 액세스를 획득하기 위한 인수도 일반적인 움직임이 되고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 업계에 미치는 영향요인

- 성장 촉진요인

- 세계 백신 생산 증가

- 세계 암의 이환율이 증가

- 세포주 개발에 있어서의 기술 혁신

- 성장하는 생명 공학 산업

- 업계의 잠재적 위험 및 과제

- 복잡한 규제 상황

- 줄기세포 연구와 관련된 과제

- 시장 기회

- 맞춤형 의료 및 재생 요법에서의 새로운 응용

- 세포주 최적화에서의 인공지능 도입

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 미래 시장 동향

- CHO 세포주의 새로운 치료 응용

- 기술의 상황

- 현재의 기술 동향

- 신흥기술

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 제품 및 서비스별, 2021-2034년

- 주요 동향

- 시약과 배지

- 장치

- 인큐베이터

- 원심분리기

- 바이오리액터

- 보관 설비

- 현미경

- 일렉트로포레이터

- 형광 활성화 세포 선별

- 기타 기기

- 액세서리와 소모품

- 서비스

제6장 시장 추계 및 예측 : 소스별, 2021-2034년

- 주요 동향

- 포유류

- 중국햄스터 난소(CHO)

- 인간 태아 신장(HEK)

- 아기 햄스터 신장(BHK)

- 쥐 골수종

- 기타 포유류 유래

- 비포유류

- 곤충

- 양서류

제7장 시장 추계 및 예측 : 세포주별, 2021-2034년

- 주요 동향

- 재조합

- 하이브리도마

- 상용 세포주

- 1차 세포주

제8장 시장 추계 및 예측 : 용도별, 2021-2034년

- 주요 동향

- 바이오 프로덕션

- 창약

- 독성시험

- 조직공학

- 조사

제9장 시장 추계 및 예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 제약 및 생명 공학 기업

- 학술연구기관

- 계약연구기관(CRO)

제10장 시장 추계 및 예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- Advanced Instruments

- Aragen Life Sciences

- ASIMOV

- Cytiva(Danaher Corporation)

- Eurofins Scientific

- Fyonibio

- Genscript Biotech

- Lonza Group

- Novartis

- ProBioGen

- PromoCell

- Sartorius

- Sigma Aldrich(Merck KGaA)

- Thermo Fisher Scientific

- WuXi AppTec

The Global Cell Line Development Market was valued at USD 7.5 billion in 2024 and is estimated to grow at a CAGR of 10.2% to reach USD 19.7 billion by 2034. Market expansion is being fueled by a growing focus on biologics and biosimilars, particularly as the pharmaceutical industry shifts toward personalized therapies and precision medicine. The surge in demand for monoclonal antibodies, vaccines, and recombinant proteins has placed a strong emphasis on the development of highly stable and productive cell lines. The increase in chronic illnesses-such as autoimmune diseases, cancer, and infectious disorders-has led to the rising adoption of biologics, which depend heavily on well-characterized cell lines. This has also elevated the need for quality-controlled production systems. Contract development and manufacturing organizations (CDMOs) have contributed significantly to market momentum.

Small and mid-sized biotech firms are increasingly outsourcing their cell line development to CDMOs to reduce overhead costs and accelerate timelines, benefiting from their technical expertise, scalable platforms, and regulatory compliance with agencies like the FDA. This trend allows companies to focus on core competencies such as research and innovation while leveraging CDMOs for end-to-end services including cell line screening, clone selection, process optimization, and GMP manufacturing. These partnerships also offer access to advanced technologies, streamlined workflows, and proven quality assurance frameworks, enabling faster entry into clinical trials and reducing risks associated with internal capacity limitations.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $7.5 Billion |

| Forecast Value | $19.7 Billion |

| CAGR | 10.2% |

The reagents and media segment generated USD 3.4 billion in 2024. This segment continues to dominate due to its central role in cell growth and maintenance across both R&D and production stages. With a notable increase in the use of mammalian cells for biologics manufacturing, the demand for high-efficiency reagents and cell culture media has surged. A growing preference for protein-free and serum-free media is helping the segment gain traction, offering improved scalability, reduced risk of contamination, and consistency in large-scale production environments. Such media types are essential for regulatory approval and efficiency in biologics manufacturing, which demands stringent process control.

In terms of cell type, mammalian cells segment generated the highest revenue in 2024, accounting for 71.4%. Their dominance is linked to their superior ability to express human-compatible therapeutic proteins with accurate post-translational modifications. Widely used cell lines such as CHO and HEK-293 are favored in biologics production due to their robust protein folding, glycosylation, and scalability. Technological progress in gene editing tools, such as CRISPR-Cas9, combined with automation and high-throughput systems, continues to enhance the speed and stability of mammalian cell line development, further reinforcing their leadership in the market.

United States Cell Line Development Market was valued at USD 2.6 billion in 2024, driven by a combination of advanced biopharma infrastructure, high rates of chronic disease, and strong adoption of cutting-edge biologic therapies. The country's well-established pharmaceutical ecosystem, which includes top-tier biotech firms and extensive R&D investment, plays a pivotal role in expanding the market. Research institutions and innovation hubs across the US are also accelerating technological advancements in gene editing and automated platforms, leading to faster and more efficient development cycles. Government and private sector funding are also propelling innovation, further supporting the country's leadership in the field.

Key companies operating in the Global Cell Line Development Market include PromoCell, Novartis, Genscript Biotech, Sartorius, Thermo Fisher Scientific, ProBioGen, Cytiva (Danaher Corporation), ASIMOV, Advanced Instruments, Sigma Aldrich (Merck KGaA), Eurofins Scientific, WuXi AppTec, Aragen Life Sciences, Fyonibio, and Lonza Group. Top-tier players in the cell line development space are heavily investing in technological innovations like automated cell screening platforms, single-use bioreactors, and CRISPR-based genome editing. Many companies are forming strategic alliances with biotech firms and CDMOs to enhance service offerings and expand production capabilities. Acquisitions are also a popular move to integrate novel technologies or gain regional access. Firms are focusing on R&D to develop serum-free and chemically defined media, helping improve regulatory compliance and scalability.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Products & services

- 2.2.3 Source

- 2.2.4 Cell line

- 2.2.5 Application

- 2.2.6 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing vaccine production worldwide

- 3.2.1.2 Increasing prevalence of cancer across the globe

- 3.2.1.3 Technological innovations in cell line development

- 3.2.1.4 Growing biotechnology industry

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Complex regulatory landscape

- 3.2.2.2 Challenges related to stem cell research

- 3.2.3 Market opportunities

- 3.2.3.1 Emerging applications in personalized medicine and regenerative therapies

- 3.2.3.2 Adoption of artificial intelligence in cell line optimization

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Future market trends

- 3.6 Emerging therapeutic applications of CHO cell lines

- 3.7 Technology landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Products & Services, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Reagents and media

- 5.3 Equipment

- 5.3.1 Incubator

- 5.3.2 Centrifuges

- 5.3.3 Bioreactors

- 5.3.4 Storage equipment

- 5.3.5 Microscopes

- 5.3.6 Electroporators

- 5.3.7 Fluorescence-activated cell sorting

- 5.3.8 Other equipment

- 5.4 Accessories and consumables

- 5.5 Services

Chapter 6 Market Estimates and Forecast, By Source, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Mammalian

- 6.2.1 Chinese Hamster Ovary (CHO)

- 6.2.2 Human Embryonic Kidney (HEK)

- 6.2.3 Baby Hamster Kidney (BHK)

- 6.2.4 Murine myeloma

- 6.2.5 Other mammalian sources

- 6.3 Non-mammalian

- 6.3.1 Insects

- 6.3.2 Amphibians

Chapter 7 Market Estimates and Forecast, By Cell Line, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Recombinant

- 7.3 Hybridomas

- 7.4 Continuous cell lines

- 7.5 Primary cell lines

Chapter 8 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Bioproduction

- 8.3 Drug discovery

- 8.4 Toxicity testing

- 8.5 Tissue engineering

- 8.6 Research

Chapter 9 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Pharmaceutical and biotechnology companies

- 9.3 Academic and research institutes

- 9.4 Contract research organizations (CROs)

Chapter 10 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Netherlands

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 Japan

- 10.4.3 India

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.6 Middle East and Africa

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Advanced Instruments

- 11.2 Aragen Life Sciences

- 11.3 ASIMOV

- 11.4 Cytiva (Danaher Corporation)

- 11.5 Eurofins Scientific

- 11.6 Fyonibio

- 11.7 Genscript Biotech

- 11.8 Lonza Group

- 11.9 Novartis

- 11.10 ProBioGen

- 11.11 PromoCell

- 11.12 Sartorius

- 11.13 Sigma Aldrich (Merck KGaA)

- 11.14 Thermo Fisher Scientific

- 11.15 WuXi AppTec