|

시장보고서

상품코드

1766361

자동차 음향 엔지니어링 서비스 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Automotive Acoustic Engineering Service Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

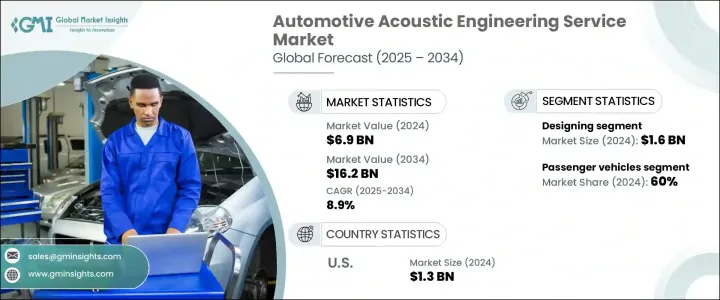

세계의 자동차 음향 엔지니어링 서비스 시장 규모는 2024년에는 69억 달러로 평가되었고, CAGR 8.9%로 성장할 전망이며, 2034년에는 162억 달러에 이를 것으로 예측됩니다.

수요의 급증은 보다 조용하고 편안한 운전 경험의 요구, 세계 소음 규제 강화, 전동 이동성으로의 산업 전반적인 전환이 크게 영향을 받고 있습니다. 자동차의 구조와 파워트레인이 변화하고, 특히 전기차 엔진 소음 감소 추세가 변화함에 따라 자동차 제조업체와 1차 협력업체들은 소음, 진동, 불쾌감(NVH) 개선에 다시 한번 집중하고 있습니다.

주요 기업은 가상 음향 테스트, 디지털 시뮬레이션, 음향 재료 최적화 등의 기술을 활용하여 비용과 개발 기간을 줄이면서 자동차의 청각 특성을 형성하고 있습니다. 시장은 특히 유럽과 아시아태평양에서 활황을 보이고 있으며, 제조업체 각사는 선진적인 소프트웨어 플랫폼과 시뮬레이션 환경을 도입하여 차종에 관계없이 NVH 성능을 관리하고 있습니다. 이러한 서비스는 규제 준수를 지원할 뿐만 아니라 경쟁이 치열해지는 자동차 상황에서 차별화를 지원합니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 69억 달러 |

| 예측 금액 | 162억 달러 |

| CAGR | 8.9% |

설계 단계 부문은 2024년에 16억 달러를 창출했습니다. 이 부문은 개발 초기 단계에서 음향 프로파일 형성에 중요한 역할을 합니다. 주요 활동으로는 단열 포장 재료 선정, 음향 패키지 구축, 3D 툴 및 AI 탑재 플랫폼을 통한 음향 환경 시뮬레이션 등이 있습니다. 디지털 트윈과 예측 음향 모델링의 대두로 OEM은 소형 EV부터 대형 SUV까지 차량 플랫폼 전체의 NVH 처리를 커스터마이징 할 수 있게 되어 비용 효율을 유지하면서 제품의 품질을 향상시킬 수 있습니다. 이러한 초기 단계의 서비스를 통해 제조사는 물리적인 시작을 시작하기 전에 음향 특성을 미세 조정할 수 있습니다.

2024년의 점유율은 승용차가 60%를 차지했으며, 차내의 쾌적성, 차음성, 세련된 음향 체험에 대한 소비자의 관심이 높아져, 계속 주류가 되고 있습니다. EV가 엔진 노이즈를 배제함에 따라 로드 노이즈와 공조 노이즈 등의 부차적인 소리가 눈에 띄게 되었습니다. 이러한 변화로 자동차 제조사들은 보다 조용하고 프리미엄한 차량 내 체험을 제공하기 위해 보다 뛰어난 방음재, 정밀한 튜닝, 고도의 시뮬레이션 소프트웨어에 대한 투자를 독려하고 있습니다. 또 자율주행 기능 및 커넥티드 인포테인먼트 시스템의 존재감이 높아짐에 따라 승용차의 사운드스케이프를 적절히 관리할 필요성도 커지고 있습니다.

미국의 자동차 음향 엔지니어링 서비스 시장은 2024년에 13억 달러를 창출했고, 2034년까지 연평균 복합 성장률(CAGR) 7.8%로 성장할 것으로 예측됩니다. 북미에서의 이 리더십은 강력한 자동차 제조 기반, 대규모 연구개발 투자, 선진 NVH 기술의 조기 도입에 기인하고 있습니다. 테슬라, 포드, 제너럴 모터스 등의 OEM들은 사용자 경험을 향상시키고 강화되는 소음 수준 규제를 충족시키기 위해 음향 설계 및 사운드 캘리브레이션에 주력하고 있습니다. 미시간주와 캘리포니아주 등의 지역 연구기관과 이노베이션 허브는 음향 시험과 제품 검증을 위한 견고한 에코시스템을 제공해 미국의 지역 우위성을 더욱 강화하고 있습니다.

세계의 자동차 음향 엔지니어링 서비스 시장을 형성하는 주요 기업으로는 Siemens, Gentex, Schaeffler Engineering, FEV Group, EDAG Engineering, Faurecia, Catalyst Acoustics, Continental, Autoneum 및 Bertrandt 등이 있습니다. 자동차 음향 엔지니어링 서비스 시장의 기업들은 디지털 시뮬레이션 플랫폼, AI 통합 음향 모델링, 실시간 NVH 분석에 대한 투자를 통해 시장에서의 존재감을 높이고 있습니다. 공동 개발을 위한 OEM과의 전략적 파트너십은 엔지니어링 기업이 EV나 하이브리드 플랫폼용으로 맞춤형 음향 솔루션을 공동 설계할 수 있습니다. 또한, 기업들은 스마트 센서 및 데이터베이스의 튜닝을 이용한 초기 단계의 설계 컨설팅이나 생산 후의 검증에도 서비스를 확대하고 있습니다. 세계의 혁신 센터를 통해서 연구 개발 능력을 강화해, 니치 기술 기업을 매수하는 것으로, 보다 신속한 제품 전개를 가능하게 하고 있습니다. 지속 가능하고 경량인 음향 소재를 중시함으로써 성능 기준을 충족시키면서 환경 규제에도 대응하고 있습니다. 시장 개척의 리더 기업은, 자동차 수요가 확대되는 신흥국 시장에도 서비스를 확대해, 현지화의 대처를 지원해, 장기적인 고객 관계를 구축하고 있습니다.

목차

제1장 조사 방법 및 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 차량 확장 기능에 대한 수요 증가

- 차량 소음에 관한 엄격한 정부 규제

- 고급차 판매 증가

- 음향 공학 기술의 진보

- 업계의 잠재적 위험 및 과제

- 높은 도입 비용

- 멀티 머티리얼 및 경량 설계의 복잡성

- 시장 기회

- EV 및 자율주행차 시장의 성장

- AI를 활용한 NVH 분석 도입

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술 및 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 제품별

- 생산 통계

- 생산 거점

- 소비 거점

- 수출 및 수입

- 비용 내역 분석

- 특허 분석

- 지속가능성 및 환경 측면

- 지속가능한 관행

- 폐기물 삭감 전략

- 생산에서 에너지 효율

- 환경 친화적인 노력

- 카본 풋 프린트의 고려

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카 항공

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획 및 자금조달

제5장 시장 추계 및 예측 : 공정별(2021-2034년)

- 주요 동향

- 설계

- 개발

- 테스트

제6장 시장 추계 및 예측 : 제공별(2021-2034년)

- 주요 동향

- 피지컬

- 가상

제7장 시장 추계 및 예측 : 솔루션별(2021-2034년)

- 주요 동향

- 교정

- 진동

- 시뮬레이션

- 기타

제8장 시장 추계 및 예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- 세단

- 해치백

- SUV

- 상용차

- 소형 상용차(LCV)

- 중형 상용차(MCV)

- 대형 상용차(HCV)

제9장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 인테리어

- 바디 및 구조

- 파워트레인

- 드라이브 트레인

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제11장 기업 프로파일

- Adler Pelzer

- Autoneum

- AVL List

- Bertrandt

- Catalyst Acoustics

- Continental

- DESIGNA

- EDAG Engineering

- Faurecia SA

- FEV Group

- Gentex

- HEAD

- Horiba

- IAV GmbH

- Roechling

- Schaeffler

- Siemens

- Spectris

- STS Group

- Vibroacoustic

The Global Automotive Acoustic Engineering Service Market was valued at USD 6.9 billion in 2024 and is estimated to grow at a CAGR of 8.9% to reach USD 16.2 billion by 2034. The surge in demand is largely influenced by the need for quieter and more comfortable driving experiences, stricter global noise regulations, and the industry-wide transition toward electric mobility. As the structure and powertrains of vehicles change, particularly with the reduced engine noise in EVs, automakers and Tier 1 suppliers are placing renewed focus on noise, vibration, and harshness (NVH) refinement.

Leading companies are leveraging technologies such as virtual acoustic testing, digital simulation, and sound material optimization to shape the auditory signature of vehicles while cutting costs and development time. The market is particularly dynamic in Europe and Asia-Pacific, where manufacturers are deploying advanced software platforms and simulation environments to manage NVH performance across vehicle types. These services not only help meet regulatory compliance but also support differentiation in an increasingly competitive automotive landscape.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $6.9 Billion |

| Forecast Value | $16.2 Billion |

| CAGR | 8.9% |

The design phase segment generated USD 1.6 billion in 2024. This segment plays a critical role in shaping acoustic profiles from the earliest phases of development. Key activities include selecting sound-insulating materials, building sound packages, and simulating acoustic environments using 3D tools and AI-powered platforms. The rise of digital twins and predictive acoustic modeling allows OEMs to customize NVH treatments across vehicle platforms-from compact EVs to large SUVs-improving product quality while maintaining cost efficiency. These early-stage services enable manufacturers to fine-tune sound characteristics before physical prototyping begins.

Passenger vehicles represented a 60% share in 2024, continuing to dominate due to heightened consumer focus on cabin comfort, noise isolation, and refined acoustic experiences. With EVs eliminating engine noise, secondary sounds like road and HVAC noise have become more noticeable. This shift is prompting carmakers to invest in better soundproofing materials, precision tuning, and advanced simulation software to deliver a quieter, more premium in-vehicle experience. The expanding presence of autonomous features and connected infotainment systems also increases the need for well-managed soundscapes in passenger vehicles.

U.S. Automotive Acoustic Engineering Service Market generated USD 1.3 billion in 2024 and is forecasted to grow at a CAGR of 7.8% through 2034. This leadership in North America stems from a strong automotive manufacturing base, significant R&D investment, and early adoption of advanced NVH technologies. OEMs like Tesla, Ford Motor Company, and General Motors are increasing their focus on acoustic design and sound calibration to enhance user experience and meet tightening noise-level regulations. Research institutions and innovation hubs across regions such as Michigan and California provide a robust ecosystem for acoustic testing and product validation, further reinforcing the U.S.'s regional dominance.

Key players shaping the Global Automotive Acoustic Engineering Service Market include Siemens, Gentex, Schaeffler Engineering, FEV Group, EDAG Engineering, Faurecia, Catalyst Acoustics, Continental, Autoneum, and Bertrandt. Companies in the automotive acoustic engineering service market are enhancing their market presence through investment in digital simulation platforms, AI-integrated acoustic modeling, and real-time NVH analytics. Strategic partnerships with OEMs for collaborative development are helping engineering firms co-design tailored acoustic solutions for EVs and hybrid platforms. Firms are also expanding service offerings into early-phase design consultation and post-production validation using smart sensors and data-based tuning. Enhancing R&D capabilities through global innovation centers and acquiring niche tech firms are enabling faster product rollout. Emphasis on sustainable and lightweight acoustic materials aligns with environmental regulations while meeting performance standards. Market leaders are also extending services to developing markets with growing automotive demand, supporting localization efforts, and building long-term client relationships.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Process

- 2.2.3 Offering

- 2.2.4 Solution

- 2.2.5 Vehicle

- 2.2.6 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for enhanced features in vehicle

- 3.2.1.2 Stringent government regulations on vehicle noise

- 3.2.1.3 Rise in sales of premium vehicles

- 3.2.1.4 Advancements in acoustic engineering technology

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High implementation costs

- 3.2.2.2 Complexity in multi-material and lightweight designs

- 3.2.3 Market opportunities

- 3.2.3.1 Growth of EV and autonomous vehicle markets

- 3.2.3.2 Adoption of AI-driven NVH analytics

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Process, 2021 - 2034 ($Mn)

- 5.1 Key trends

- 5.2 Designing

- 5.3 Development

- 5.4 Testing

Chapter 6 Market Estimates & Forecast, By Offering, 2021 - 2034 ($Mn)

- 6.1 Key trends

- 6.2 Physical

- 6.3 Virtual

Chapter 7 Market Estimates & Forecast, By Solution, 2021 - 2034 ($Mn)

- 7.1 Key trends

- 7.2 Calibration

- 7.3 Vibration

- 7.4 Simulation

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn)

- 8.1 Key trends

- 8.2 Passenger cars

- 8.2.1 Sedans

- 8.2.2 Hatchbacks

- 8.2.3 SUV

- 8.3 Commercial vehicles

- 8.3.1 Light Commercial Vehicles (LCV)

- 8.3.2 Medium Commercial Vehicles (MCV)

- 8.3.3 Heavy Commercial Vehicles (HCV)

Chapter 9 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn)

- 9.1 Key trends

- 9.2 Interior

- 9.3 Body & structure

- 9.4 Powertrain

- 9.5 Drivetrain

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 Saudi Arabia

- 10.6.2 South Africa

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Adler Pelzer

- 11.2 Autoneum

- 11.3 AVL List

- 11.4 Bertrandt

- 11.5 Catalyst Acoustics

- 11.6 Continental

- 11.7 DESIGNA

- 11.8 EDAG Engineering

- 11.9 Faurecia SA

- 11.10 FEV Group

- 11.11 Gentex

- 11.12 HEAD

- 11.13 Horiba

- 11.14 IAV GmbH

- 11.15 Roechling

- 11.16 Schaeffler

- 11.17 Siemens

- 11.18 Spectris

- 11.19 STS Group

- 11.20 Vibroacoustic