|

시장보고서

상품코드

1773273

동물용 POC 진단 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Veterinary Point of Care Diagnostics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

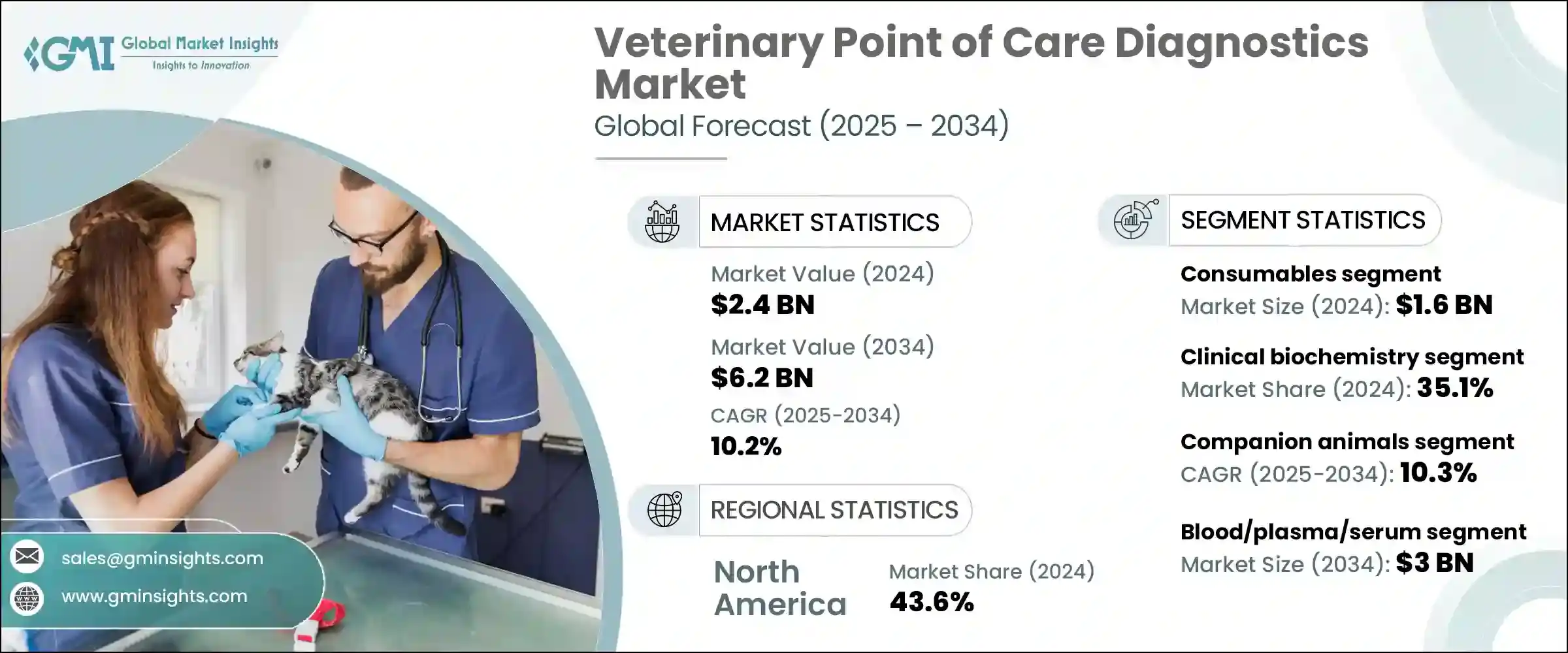

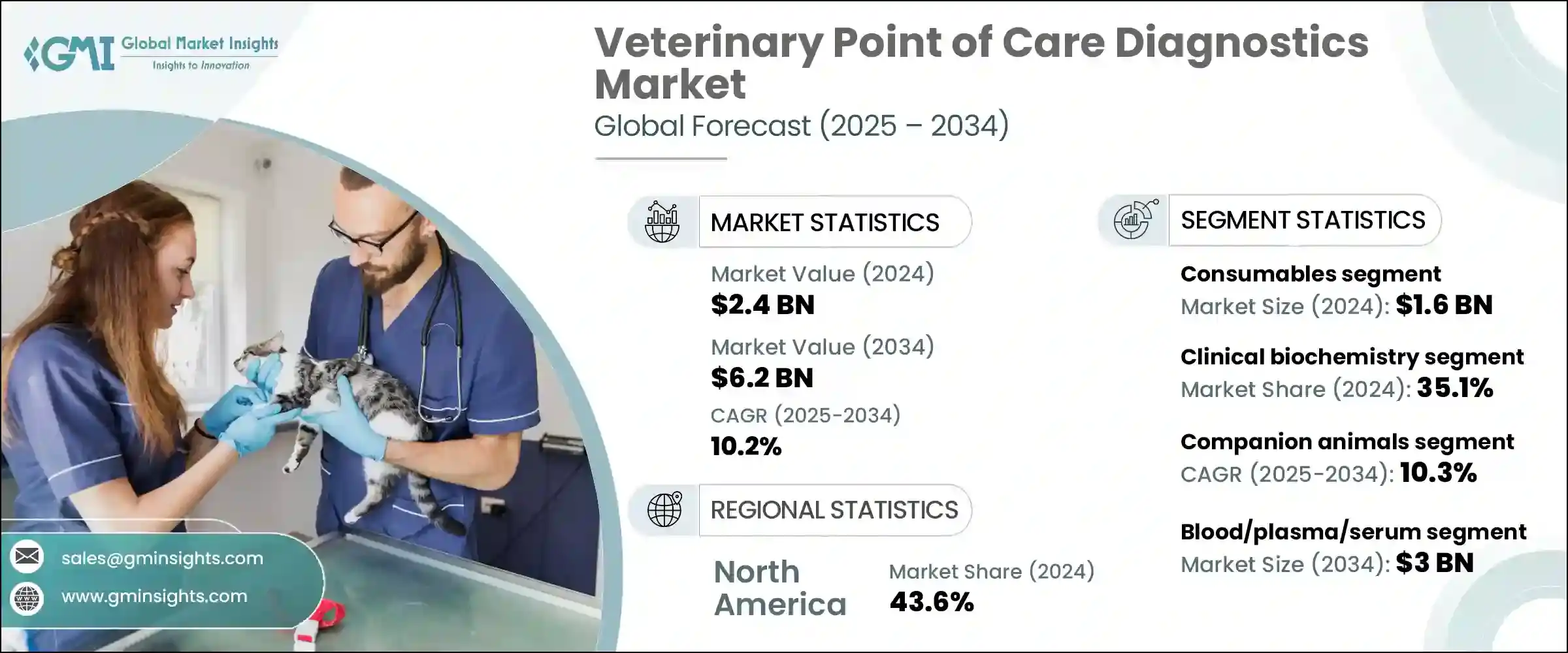

세계의 동물용 POC 진단 시장은 2024년에는 24억 달러로 평가되며, CAGR 10.2%로 성장하며, 2034년에는 62억 달러에 달할 것으로 추정되고 있습니다.

이러한 급격한 성장은 동물의 감염병 발생률 증가와 종을 넘어 감염되는 인수공통전염병에 대한 우려가 높아진 것을 반영합니다. 반려동물 사육과 가축 개체수가 증가함에 따라 신속한 현장 검사의 필요성이 증가하고 있습니다. 동물병원과 연구소는 정확도를 높이고 동물의 헬스케어를 간소화하는 AI 및 IoT 지원 플랫폼 덕분에 빠른 결과와 휴대성을 자랑하는 첨단 진단 툴을 도입하여 대응하고 있습니다.

수의학에 대한 접근성 향상과 반려동물 보험의 보급률 증가와 함께 이러한 추세는 현장 진료 검사에 대한 신뢰도를 높이고 시장 성장을 가속화하고 있습니다. 예방 의료와 질병의 조기 발견을 우선시하는 보호자가 증가함에 따라 치료 결정을 신속하게 내리기 위해 진료 시점에 이용할 수 있는 신속한 진단에 의존하는 경향이 증가하고 있습니다. 이러한 수요 증가로 인해 동물병원 및 클리닉은 외부 검사실 검사에 뒤처지지 않고 정확한 실시간 결과를 제공하는 첨단 휴대용 진단 툴에 대한 투자를 늘리고 있습니다. 또한 이러한 툴이 제공하는 편리함과 신뢰성은 반려동물 보호자들에게 양질의 진료에 대한 인식을 강화하고, 반려동물 보호자들이 정기적인 수의사 검진 및 건강 모니터링에 더욱 적극적으로 참여하게 함으로써 수의 진단 분야 전반의 지속적인 성장을 가속하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024년 |

| 예측연도 | 2025-2034년 |

| 시작 금액 | 24억 달러 |

| 예측 금액 | 62억 달러 |

| CAGR | 10.2% |

동물용 POC 진단 시장의 소모품 부문은 2024년 16억 달러 시장을 창출했습니다. 소모품에는 카트리지, 시약, 시약, 검사 키트, 분석법 등이 포함되며, 각 현장 진료 절차에 필수적이며 빈번한 보충이 필요합니다. 이러한 지속적인 요구사항은 검사량이 증가함에 따라 안정적인 경상 매출을 지원하고 있습니다. 진료소와 병원이 확장됨에 따라 반려동물 보호자와 전문가들이 즉각적인 결과와 대기 시간 단축에 만족할 수 있는 휴대가 간편하고 사용하기 쉬운 소모품에 대한 수요가 증가하고 있습니다.

임상 생화학 분야는 대사, 장기 기능, 감염, 염증 평가에 중심적인 역할을 하며 2024년 35.1%의 점유율을 차지했습니다. 이 분야의 검사에는 간, 신장, 전해질, 포도당, 패혈증 바이오마커 패널이 포함됩니다. 동물병원과 검사실에서 널리 사용되는 것은 적시 진단과 치료, 특히 응급 상황이나 만성질환에 대한 적시 진단과 치료의 중요성을 지원합니다.

유럽 동물용 현장진단(POC) 시장 규모는 2024년 6억 580만 달러에 달하며, 향후에도 강력한 성장이 예상됩니다. 인수공통전염병 및 가축전염병에 대한 정부의 구상에 힘입어 신속한 동물 진단에 대한 인식이 높아지면서 도입이 가속화되고 있습니다. 마이크로플루이드, 면역 분석, 휴대용 분자 검사 등의 기술 혁신과 진단 기업 및 수의학 기관과의 제휴로 유럽 시장은 빠르게 발전하고 있습니다.

동물용 POC 진단 시장의 주요 기업에는 IDEXX Laboratories, GE Healthcare, Zoetis, Thermo Fisher Scientific, Mindray, BioMerieux, Antech, FUJIFILM SonoSite, Eurolyser Diagnostics, Randox Laboratories, Carestream Health, Esaote, NeuroLogica, Biotangents, Virbac, Woodley Equipment 등이 있습니다.. 진단 제공업체들은 제품 혁신, 파트너십 확대, 전략적 가격 책정을 통해 시장 입지를 강화하고 있습니다. 기업들은 테스트 감도, 휴대성, AI 및 클라우드 플랫폼과의 통합을 향상시키기 위해 R&D에 우선순위를 두고 있습니다. 동물 병원, 동물 보건 네트워크, 정부 기관과 제휴를 맺어 보급을 확대하고 표준 치료 프로토콜에 솔루션을 포함시킵니다. 소모품을 장비와 함께 번들로 제공하고 구독 또는 시약 보충 프로그램을 제공함으로써 반복적인 수익을 확보하는 동시에 임상의의 충성도를 유지합니다. 지역 확장과 현지 유통업체와의 협업을 통해 다양한 시장에 맞춤형 솔루션을 제공할 수 있습니다. 또한 경쟁력 있는 가격, 번들 서비스 계약, 보증 제도를 통해 제품을 차별화할 수 있습니다. 기술적 우수성과 고객 지원에 중점을 두어 빠르게 성장하는 결과 중심 부문에서 관련성을 유지하고 점유율을 확보할 수 있습니다.

목차

제1장 조사 방법과 범위

제2장 개요

제3장 업계 인사이트

- 에코시스템 분석

- 공급업체의 상황

- 각 단계에서의 부가가치

- 밸류체인에 영향을 미치는 요인

- 업계에 대한 영향요인

- 촉진요인

- POC(Point of Care) 진단의 수요 증가

- 동물 헬스케어비의 증가

- 동물 질병의 만연 증가

- 진단 기술의 진보

- 업계의 잠재적 리스크 & 과제

- POC 진단 기기와 소모품의 고비용

- 숙련 수의 전문가의 부족

- 시장 기회

- 애완동물 사육수의 증가와 애완동물의 인간화

- 수의학 교육과 훈련에서 POC(Point of Care)의 이용 증가

- 촉진요인

- 성장 가능성 분석

- 규제 상황

- 향후 시장 동향

- 테크놀러지의 상황

- 현재 기술 동향

- 신규 기술

- 국가별 수의사수, 2024년

- Porter의 산업 분석

- PESTEL 분석

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십과 협업

- 신제품 발매

- 확장 계획

제5장 시장 추산·예측 : 제품별, 2021-2034년

- 주요 동향

- 소모품

- 기구 및 기기

제6장 시장 추산·예측 : 테스트 유형별, 2021-2034년

- 주요 동향

- 임상 생화학

- 면역진단

- 분자진단

- 혈액학

- 요검사

- 기타 테스트 유형

제7장 시장 추산·예측 : 동물 유형별, 2021-2034년

- 주요 동향

- 반려동물

- 개

- 고양이

- 말

- 기타 애완동물

- 가축

- 소

- 돼지

- 가금

- 기타 가축

제8장 시장 추산·예측 : 샘플 유형별, 2021-2034년

- 주요 동향

- 혈액/혈장/혈청

- 뇨

- 분변

- 기타 샘플 유형

제9장 시장 추산·예측 : 용도별, 2021-2034년

- 주요 동향

- 감염증

- 비감염성 질환

- 유전성 및 선천성 질환

- 후천적인 건강 상태

- 기타 용도

제10장 시장 추산·예측 : 최종 용도별, 2021-2034년

- 주요 동향

- 동물병원 및 진료소

- 진단 실험실

- 홈케어 환경

- 기타 최종 용도

제11장 시장 추산·예측 : 지역별, 2021-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카공화국

- 사우디아라비아

- 아랍에미리트

제12장 기업 개요

- Antech

- BioMerieux

- Biotangents

- Carestream Health

- Esaote

- Eurolyser Diagnostica

- FUJIFILM SonoSite

- GE Healthcare

- IDEXX Laboratories

- Mindray

- NeuroLogica

- Randox Laboratories

- Thermo Fisher Scientific

- Virbac

- Woodley Equipment

- Zoetis

The Global Veterinary Point of Care Diagnostics Market was valued at USD 2.4 billion in 2024 and is estimated to grow at a CAGR of 10.2% to reach USD 6.2 billion by 2034. The surge reflects increasing rates of infectious diseases in animals and the growing concern over zoonotic illnesses crossing between species. As pet ownership and livestock populations expand, the need for rapid, on-site testing has intensified. Clinics and labs are responding by deploying advanced diagnostic tools that boast quick results and portability, thanks in part to AI and IoT-enabled platforms that enhance accuracy and streamline animal health management.

Together with better access to veterinary care and rising pet insurance adoption, these trends are fueling confidence in point-of-care testing and accelerating market growth. As more pet owners prioritize preventive care and early disease detection, they are increasingly relying on rapid diagnostics available at the point of care for faster treatment decisions. This growing demand is encouraging veterinary clinics and hospitals to invest in advanced, portable diagnostic tools that provide accurate, real-time results without the delays of external lab testing. Additionally, the convenience and reliability offered by these tools are reinforcing the perception of quality care, making pet owners more willing to engage in regular veterinary checkups and health monitoring, thereby propelling sustained growth across the entire veterinary diagnostics sector.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $2.4 Billion |

| Forecast Value | $6.2 Billion |

| CAGR | 10.2% |

The consumables segment from the veterinary point-of-care diagnostics market generated USD 1.6 billion in 2024. They include cartridges, reagents, test kits, and assays-essential for each point-of-care procedure and necessitating frequent replenishment. This continuous requirement supports reliable recurring revenue as testing volumes climb. As clinics and hospitals expand, demand for portable and easy-use consumables grows, enabling immediate results and reduced waiting times, which pet owners and professionals appreciate.

The clinical biochemistry segment held a 35.1% share in 2024, driven by its central role in evaluating metabolism, organ function, infection, and inflammation. Tests in this segment include panels for liver, kidney, electrolytes, glucose, and sepsis biomarkers. Widespread adoption in veterinary clinics and labs underscores their importance in timely diagnosis and treatment, especially critical in emergency and chronic conditions.

Europe Veterinary Point of Care Diagnostics Market reached USD 605.8 million in 2024 and is poised for strong future growth. Rising awareness around rapid animal diagnostics, backed by government initiatives targeting zoonotic and livestock diseases, is accelerating adoption. Enhanced by innovations in microfluidics, immunoassays, and portable molecular testing, along with collaborations between diagnostic firms and veterinary organizations, the European market is advancing rapidly.

Key companies in the Veterinary Point of Care Diagnostics Market include IDEXX Laboratories, GE Healthcare, Zoetis, Thermo Fisher Scientific, Mindray, BioMerieux, Antech, FUJIFILM SonoSite, Eurolyser Diagnostics, Randox Laboratories, Carestream Health, Esaote, NeuroLogica, Biotangents, Virbac, Woodley Equipment. Diagnostic providers are strengthening their market foothold through product innovation, expanding partnerships, and strategic pricing. Companies prioritize R&D to enhance test sensitivity, portability, and integration with AI and cloud platforms. They forge alliances with veterinary clinics, animal health networks, and government agencies to expand distribution and embed solutions in standard care protocols. Bundling consumables with equipment and offering subscription or reagent-replenishment programs secures recurring revenues while maintaining clinician loyalty. Regional expansions and collaborations with local distributors enable customized solutions for diverse markets. Additionally, competitive pricing, bundled service contracts, and warranty schemes help differentiate offerings. A dual emphasis on technological excellence and customer support allows players to maintain relevance and capture share in a rapidly growing, outcome-driven sector.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definitions

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Test type

- 2.2.4 Animal type

- 2.2.5 Sample type

- 2.2.6 Application

- 2.2.7 End use

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Value addition at each stage

- 3.1.3 Factors affecting the value chain

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing demand for point of care diagnostics

- 3.2.1.2 Increasing animal healthcare expenditures

- 3.2.1.3 Rising prevalence of animal diseases

- 3.2.1.4 Advancements in diagnostics technology

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of POC diagnostic devices and consumables

- 3.2.2.2 Shortage of skilled veterinary professionals

- 3.2.3 Market opportunities

- 3.2.3.1 Rising companion animal ownership and pet humanization

- 3.2.3.2 Growing use of point of care in veterinary education and training

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Future market trends

- 3.6 Technology landscape

- 3.6.1 Current technological trends

- 3.6.2 Emerging technologies

- 3.7 Number of veterinarians, by country, 2024

- 3.8 Porter's analysis

- 3.9 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Merger and acquisition

- 4.6.2 Partnership and collaboration

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 – 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Consumables

- 5.3 Instruments and devices

Chapter 6 Market Estimates and Forecast, By Test Type, 2021 – 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Clinical biochemistry

- 6.3 Immunodiagnostics

- 6.4 Molecular diagnostics

- 6.5 Hematology

- 6.6 Urinalysis

- 6.7 Other test types

Chapter 7 Market Estimates and Forecast, By Animal Type, 2021 – 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Companion animals

- 7.2.1 Dogs

- 7.2.2 Cats

- 7.2.3 Horses

- 7.2.4 Other companion animals

- 7.3 Livestock animals

- 7.3.1 Cattle

- 7.3.2 Swine

- 7.3.3 Poultry

- 7.3.4 Other livestock animals

Chapter 8 Market Estimates and Forecast, By Sample Type, 2021 – 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Blood/plasma/serum

- 8.3 Urine

- 8.4 Fecal

- 8.5 Other sample types

Chapter 9 Market Estimates and Forecast, By Application, 2021 – 2034 ($ Mn)

- 9.1 Key trends

- 9.2 Infectious diseases

- 9.3 Non-infectious conditions

- 9.4 Hereditary and congenital conditions

- 9.5 Acquired health conditions

- 9.6 Other applications

Chapter 10 Market Estimates and Forecast, By End Use, 2021 – 2034 ($ Mn)

- 10.1 Key trends

- 10.2 Veterinary hospitals and clinics

- 10.3 Diagnostic labs

- 10.4 Home care settings

- 10.5 Other end use

Chapter 11 Market Estimates and Forecast, By Region, 2021 – 2034 ($ Mn)

- 11.1 Key trends

- 11.2 North America

- 11.2.1 U.S.

- 11.2.2 Canada

- 11.3 Europe

- 11.3.1 Germany

- 11.3.2 UK

- 11.3.3 France

- 11.3.4 Spain

- 11.3.5 Italy

- 11.3.6 Netherlands

- 11.4 Asia Pacific

- 11.4.1 China

- 11.4.2 Japan

- 11.4.3 India

- 11.4.4 Australia

- 11.4.5 South Korea

- 11.5 Latin America

- 11.5.1 Brazil

- 11.5.2 Mexico

- 11.5.3 Argentina

- 11.6 Middle East and Africa

- 11.6.1 South Africa

- 11.6.2 Saudi Arabia

- 11.6.3 UAE

Chapter 12 Company Profiles

- 12.1 Antech

- 12.2 BioMerieux

- 12.3 Biotangents

- 12.4 Carestream Health

- 12.5 Esaote

- 12.6 Eurolyser Diagnostica

- 12.7 FUJIFILM SonoSite

- 12.8 GE Healthcare

- 12.9 IDEXX Laboratories

- 12.10 Mindray

- 12.11 NeuroLogica

- 12.12 Randox Laboratories

- 12.13 Thermo Fisher Scientific

- 12.14 Virbac

- 12.15 Woodley Equipment

- 12.16 Zoetis