|

시장보고서

상품코드

1773314

자동차용 엔진커버 시장(2025-2034년) : 기회, 성장 촉진요인, 산업 동향 분석, 예측Automotive Engine Cover Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

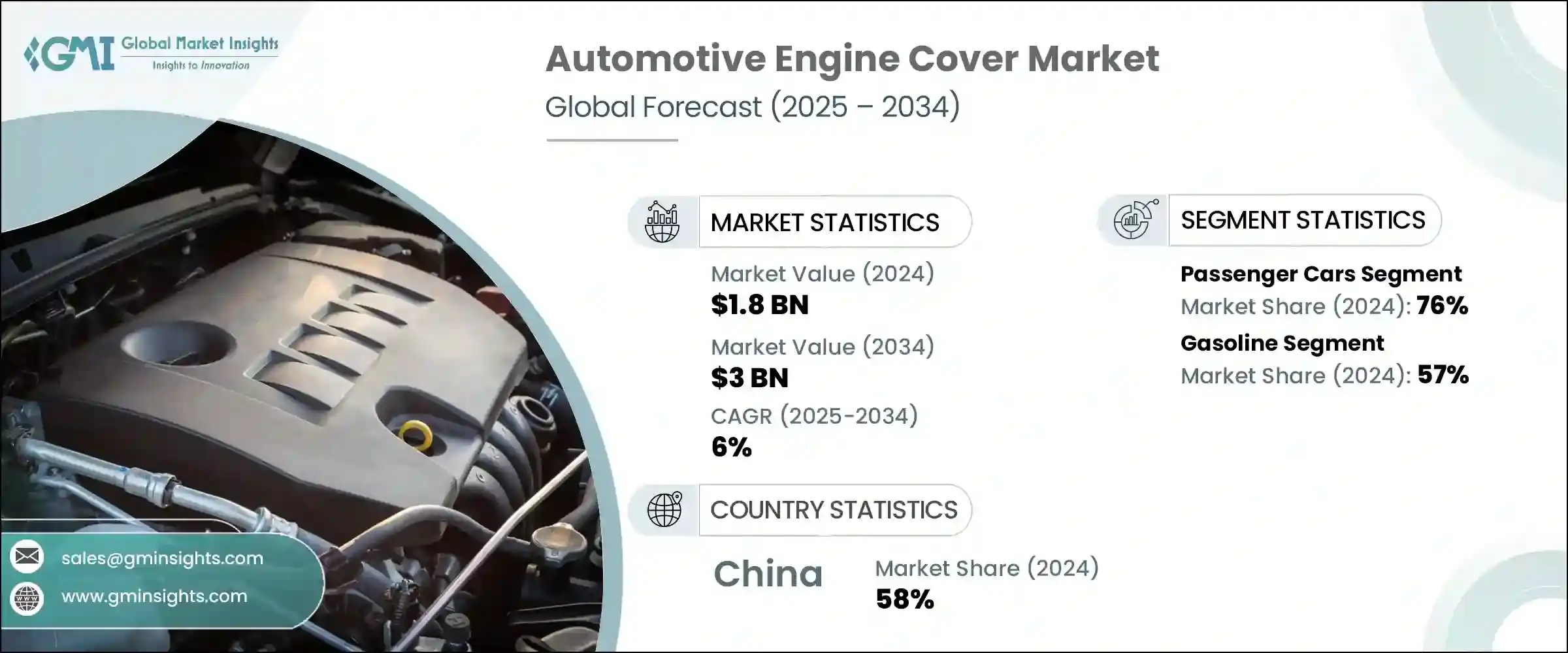

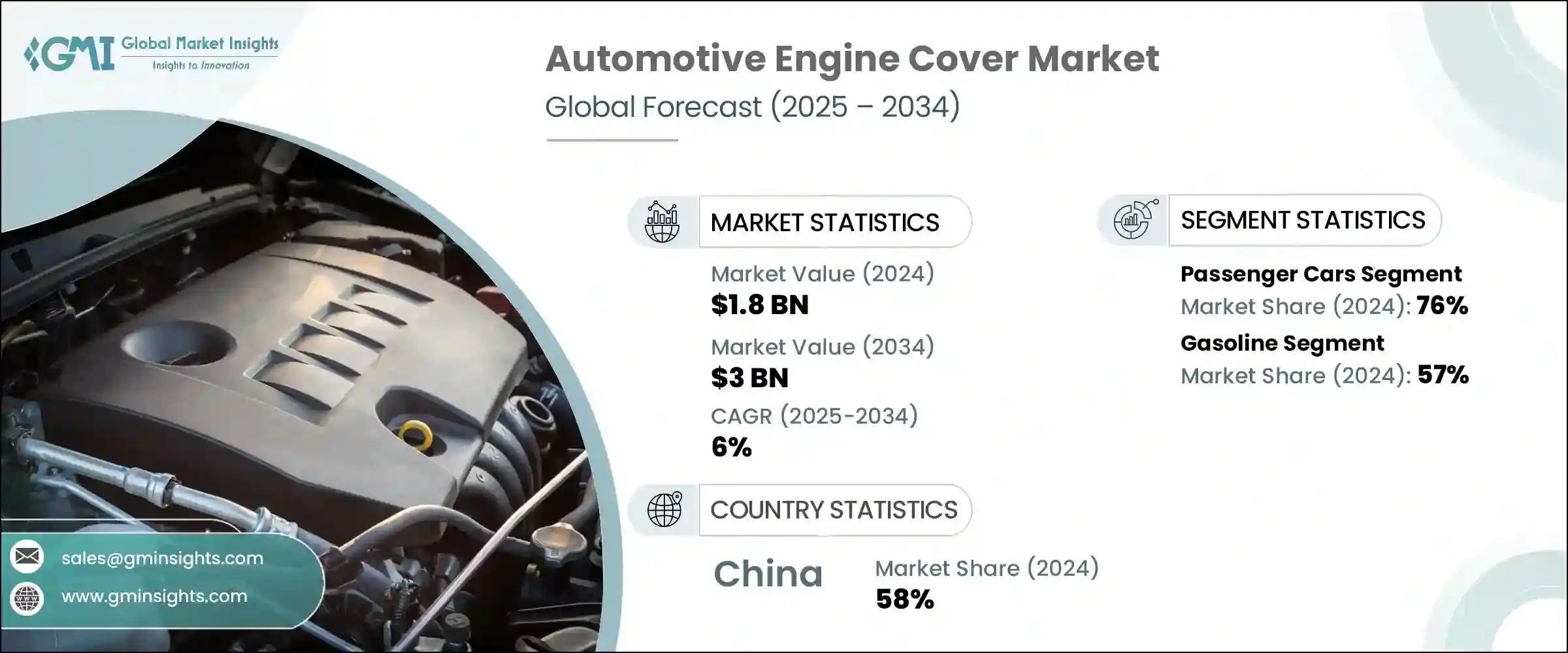

세계의 자동차용 엔진커버 시장 규모는 2024년에 18억 달러에 달하였고, CAGR 6%로 성장하여 2034년까지는 30억 달러에 이를 것으로 추정되고 있습니다.

이 성장의 원동력은 세계의 자동차 생산 대수 증가와 보다 경량이고 효율적인 자동차 부품에 대한 요구 상승으로 발생합니다. 자동차용 엔진커버는 전체적인 차량 디자인과 시각적인 조화를 실현하는 중요한 부품으로 변모하고 있습니다.

또한 복합재료 및 열가소성 플라스틱과 같은 첨단재료로의 전환으로 이 시장은 강력한 견인력을 보이고 있습니다. 기업들은 컴팩트한 자동차, 스포츠용 다목적 차량, 소형 트럭의 생산을 지원하기 위해 확장 가능한 모듈식 커버 설계를 채용하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024년 |

| 예측연도 | 2025-2034년 |

| 시작금액 | 18억 달러 |

| 예측금액 | 30억 달러 |

| CAGR | 6% |

승용차 부문은 2024년에 76%의 점유율을 차지하였으며, 2034년까지의 CAGR은 6.8%로 예측됩니다. 엔진커버를 세단, 해치백, 고급차에 적용하면서 제조업체는 성능과 차내 경험 모두를 향상시키고 있습니다. 경량의 열가소성 플라스틱이나 강화 복합재는 단열성과 고급스러운 미관을 제공하여 매끄럽고 공력 특성이 뛰어나며 브랜드에 어울리는 커버 제조에 사용되고 있습니다.

가솔린 자동차 부문은 2024년에 57%의 점유율로 시장을 선도했으며, 2034년까지의 CAGR은 7.1%로 예상됩니다. 엔진커버는 높은 연소열을 관리하고 엔진 노이즈를 줄이는 동시에 시각적 매력을 높이기 위해 설계되었습니다.

아시아태평양의 자동차용 엔진커버 시장은 58%의 점유율을 차지하였으며, 2024년에는 5억 5,310만 달러를 창출했습니다. 지역 내 기업들은 열가소성 플라스틱과 복합재 엔진커버의 대량생산에 주력하고 있습니다. 현지에서의 기술 혁신과 환경친화적인 기술을 장려하는 정부의 정책이 경량이며 배출가스를 삭감하는 부품 수요를 촉진하고 있습니다.

이 업계에서 사업을 전개하는 주요 기업은 Rochling Group, Denso Corporation, MAHLE GmbH, Woco Industrietechnik, Montaplast, Toyota Boshoku Corporation, Aisin Corporation, Valeo SA, ElringKlinger, Continental 등이 있습니다. 시장의 각 회사는 선진적인 제조기술을 활용하여 세계적인 연비규제를 충족하는 경량 내구성 엔진커버를 제공합니다. 또한 부품 제조사는 자동차 제조사와의 협업을 통해 제품 개발과 진화하는 플랫폼의 요구를 충족시킬 수 있습니다. 그리고 다양한 차종에 대응하기 위해 모듈형 설계와 스케일러블 설계의 채용이 진행되고 있어 금형 비용을 최소화하고 생산 사이클을 가속화하고 있습니다.

목차

제1장 조사방법

- 시장의 범위와 정의

- 조사 디자인

- 조사 접근

- 데이터 수집방법

- 데이터 마이닝 소스

- 세계

- 지역/국가

- 기본 추정과 계산

- 기준연도 계산

- 시장 예측의 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측모델

- 조사의 전제와 한계

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 공급자의 상황

- 이익률 분석

- 비용구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 세계 자동차 생산 증가

- 경량 부품 수요 증가

- 내연기관(ICE)차의 성장

- 컴포넌트 통합에 주력하는 OEM

- 업계의 잠재적 리스크 및 과제

- 통합 파워트레인에 의한 설계의 복잡성

- 원재료비의 변동

- 시장 기회

- 프리미엄차 및 고급차 판매의 성장

- 지속 가능하고 재활용 가능한 소재 채용 증가

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 제품별

- 생산통계

- 생산거점

- 소비거점

- 수출과 수입

- 코스트 내역 분석

- 특허 분석

- 지속 가능성과 환경 측면

- 지속 가능한 관행

- 폐기물 감축 전략

- 생산에서의 에너지 효율

- 환경친화적인 노력

- 탄소발자국의 고려

제4장 경쟁구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장계획과 자금조달

제5장 시장 추계 및 예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- 세단

- 해치백

- SUV

- 상용차

- 경량작업용

- 중량작업용

- 고중량작업용

제6장 시장 추계 및 예측 : 추진력별(2021-2034년)

- 주요 동향

- 가솔린

- 디젤

- 전기

- PHEV

- 하이브리드 자동차

- 연료전지 자동차

제7장 시장 추계 및 예측 : 재료별(2021-2034년)

- 주요 동향

- 복합재료

- 금속

- 열가소성 플라스틱

- 기타

제8장 시장 추계 및 예측 : 기능별(2021-2034년)

- 주요 동향

- 미관적 엔진커버

- 기능적 엔진커버

제9장 시장 추계 및 예측 : 유통 채널별(2021-2034년)

- 주요 동향

- OEM

- 애프터마켓

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 북유럽 국가

- 러시아

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제11장 기업 프로파일

- Aisin Corporation

- Continental

- Denso Corporation

- ElringKlinger

- Futaba Industrial

- Hanil E-Hwa Automotive Systems

- Magna International

- MAHLE

- Mann Hummel

- Montaplast

- Motherson Sumi Systems

- Plastic Omnium

- Polytec Group

- Rochling Group

- Simoldes Plasticos

- SRG Global

- Toyota Boshoku Corporation

- Valeo SA

- Woco Industrietechnik

- YAPP Automotive Systems

The Global Automotive Engine Cover Market was valued at USD 1.8 billion in 2024 and is estimated to grow at a CAGR of 6% to reach USD 3 billion by 2034. This growth is driven by rising global vehicle production and the increasing need for lighter, more efficient automotive components. As industry shifts toward greater performance and fuel economy, engine covers have transformed from basic enclosures into key components that deliver thermal control, sound insulation, and visual cohesion with overall vehicle design. As both internal combustion and hybrid vehicle platforms continue to expand globally, engine covers are being engineered as critical elements in powertrain design across a wide range of models and applications.

The market is also seeing strong traction due to the shift toward advanced materials like composites and thermoplastics. These materials provide the right balance of durability, heat resistance, and weight reduction, enabling manufacturers to meet tightening emission regulations and fuel efficiency standards. Original equipment manufacturers and Tier-1 suppliers are adopting scalable, modular cover designs to support production across compact cars, sport utility vehicles, and light-duty trucks. These platforms help achieve uniform NVH (noise, vibration, and harshness) performance while accelerating time to market and reducing manufacturing complexity.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.8 Billion |

| Forecast Value | $3 Billion |

| CAGR | 6% |

The passenger cars segment held a 76% share in 2024 and is projected to grow at a CAGR of 6.8% through 2034. Engine covers have become essential components in the design of modern passenger vehicles, where tighter engine bays and higher engine outputs demand greater heat and noise management. Their integration into sedans, hatchbacks, and luxury vehicles is helping manufacturers enhance both performance and in-cabin experience. Lightweight thermoplastics and reinforced composites are used to create sleek, aerodynamic, and brand-aligned covers, combining insulation with premium aesthetics.

Gasoline-powered vehicles segment led the market with a 57% share in 2024 and is expected to register a CAGR of 7.1% through 2034. Despite the rise of electric mobility, gasoline engines continue to dominate production volumes in many regions. Engine covers in these vehicles are designed to manage high combustion heat and reduce engine noise while enhancing visual appeal. Manufacturers are turning to composite and polymer blends to offer optimized thermal shielding and lightweight benefits at lower production costs.

Asia Pacific Automotive Engine Cover Market held a 58% share and generated USD 553.1 million in 2024. The country's dominance is supported by its large-scale automotive manufacturing infrastructure, rising consumer demand, and active presence of global OEMs and domestic component manufacturers. Leading companies in China are focusing on producing thermoplastic and composite engine covers in high volume to support diverse vehicle platforms. Government policies encouraging local innovation and greener technologies are driving demand for lightweight, emission-reducing components. Local firms continue expanding through global partnerships to deliver custom-engineered engine cover systems aligned with next-gen mobility trends.

Key companies operating in this industry include Rochling Group, Denso Corporation, MAHLE GmbH, Woco Industrietechnik, Montaplast, Toyota Boshoku Corporation, Aisin Corporation, Valeo S.A., ElringKlinger, and Continental. Market players are leveraging advanced manufacturing technologies to deliver lightweight, durable engine covers that align with global fuel efficiency mandates. Companies are investing in material science innovation, particularly in thermoplastics and composite formulations, to enhance heat resistance while reducing weight. Strategic alliances with automakers help manufacturers align product development with evolving platform needs. Modular and scalable design approaches are increasingly adopted to support a variety of vehicle models, minimizing tooling costs and speeding up production cycles. Digital simulation and prototyping tools allow rapid customization, helping firms meet specific OEM standards and aesthetic requirements.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis, 2021 – 2034

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Vehicle

- 2.2.3 Propulsion

- 2.2.4 Material

- 2.2.5 Functionality

- 2.2.6 Distribution Channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin analysis

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global vehicle production

- 3.2.1.2 Increasing demand for lightweight components

- 3.2.1.3 Growth in Internal Combustion Engine (ICE) vehicles

- 3.2.1.4 OEM focus on component integration

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Design complexity with integrated powertrains

- 3.2.2.2 Raw material cost volatility

- 3.2.3 Market opportunities

- 3.2.3.1 Growth in premium and luxury vehicle sales

- 3.2.3.2 Growing adoption of sustainable & recyclable materials

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn, Units)

- 5.1 Key trends

- 5.2 Passenger cars

- 5.2.1 Sedans

- 5.2.2 Hatchbacks

- 5.2.3 SUV

- 5.3 Commercial vehicles

- 5.3.1 Light duty

- 5.3.2 Medium duty

- 5.3.3 Heavy duty

Chapter 6 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Mn, Units)

- 6.1 Key trends

- 6.2 Gasoline

- 6.3 Diesel

- 6.4 Electric

- 6.5 PHEV

- 6.6 HEV

- 6.7 FCEV

Chapter 7 Market Estimates & Forecast, By Material, 2021 - 2034 ($Mn, Units)

- 7.1 Key trends

- 7.2 Composites

- 7.3 Metals

- 7.4 Thermoplastics

- 7.5 Others

Chapter 8 Market Estimates & Forecast, By Functionality, 2021 - 2034 ($Mn, Units)

- 8.1 Key trends

- 8.2 Aesthetic engine covers

- 8.3 Functional engine covers

Chapter 9 Market Estimates & Forecast, By Distribution Channel, 2021 - 2034 ($Mn, Units)

- 9.1 Key trends

- 9.2 OEM

- 9.3 Aftermarket

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn, Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 Germany

- 10.3.2 UK

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Nordics

- 10.3.7 Russia

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 Australia

- 10.4.5 South Korea

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 South Africa

- 10.6.2 Saudi Arabia

- 10.6.3 UAE

Chapter 11 Company Profiles

- 11.1 Aisin Corporation

- 11.2 Continental

- 11.3 Denso Corporation

- 11.4 ElringKlinger

- 11.5 Futaba Industrial

- 11.6 Hanil E-Hwa Automotive Systems

- 11.7 Magna International

- 11.8 MAHLE

- 11.9 Mann+Hummel

- 11.10 Montaplast

- 11.11 Motherson Sumi Systems

- 11.12 Plastic Omnium

- 11.13 Polytec Group

- 11.14 Rochling Group

- 11.15 Simoldes Plasticos

- 11.16 SRG Global

- 11.17 Toyota Boshoku Corporation

- 11.18 Valeo S.A.

- 11.19 Woco Industrietechnik

- 11.20 YAPP Automotive Systems