|

시장보고서

상품코드

1773400

첨단 자동차 조명 시장(2025-2034년) : 기회, 성장 촉진요인, 산업 동향 분석, 예측Advanced Vehicle Lighting Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

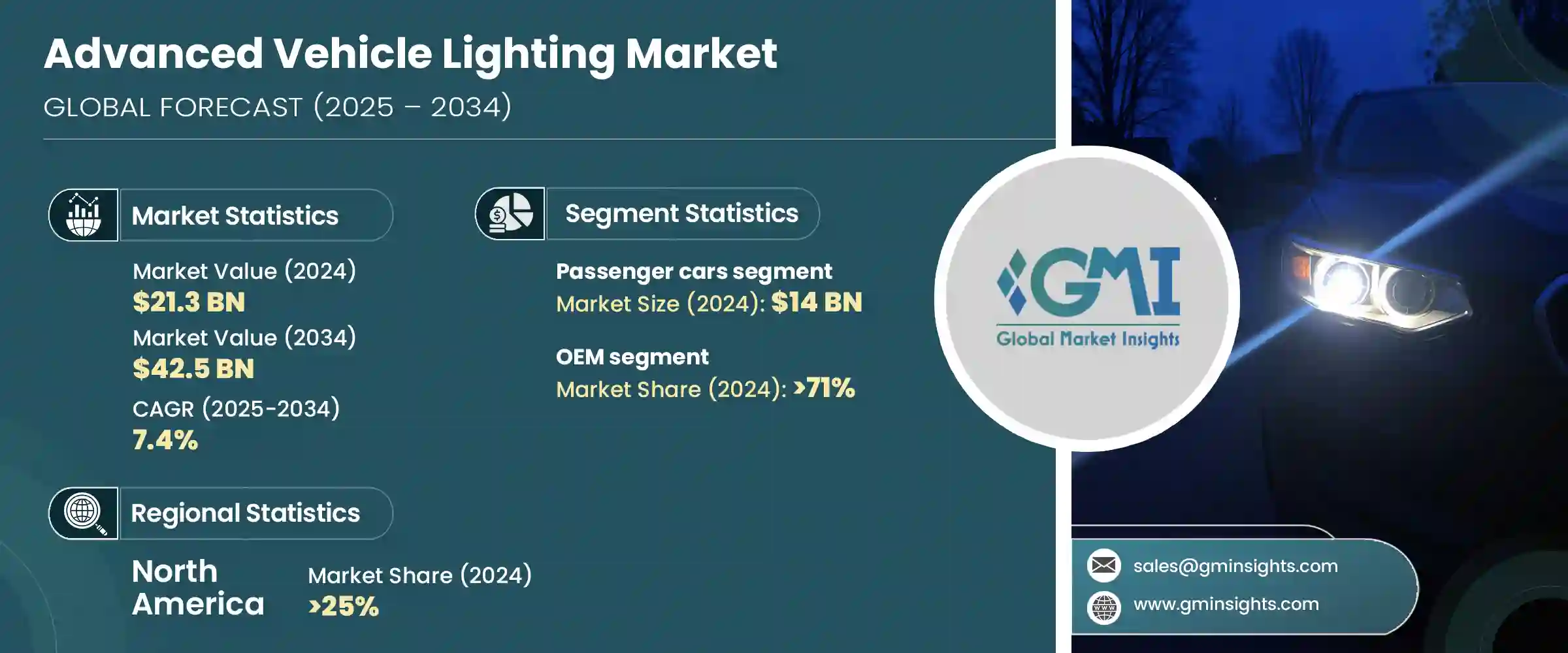

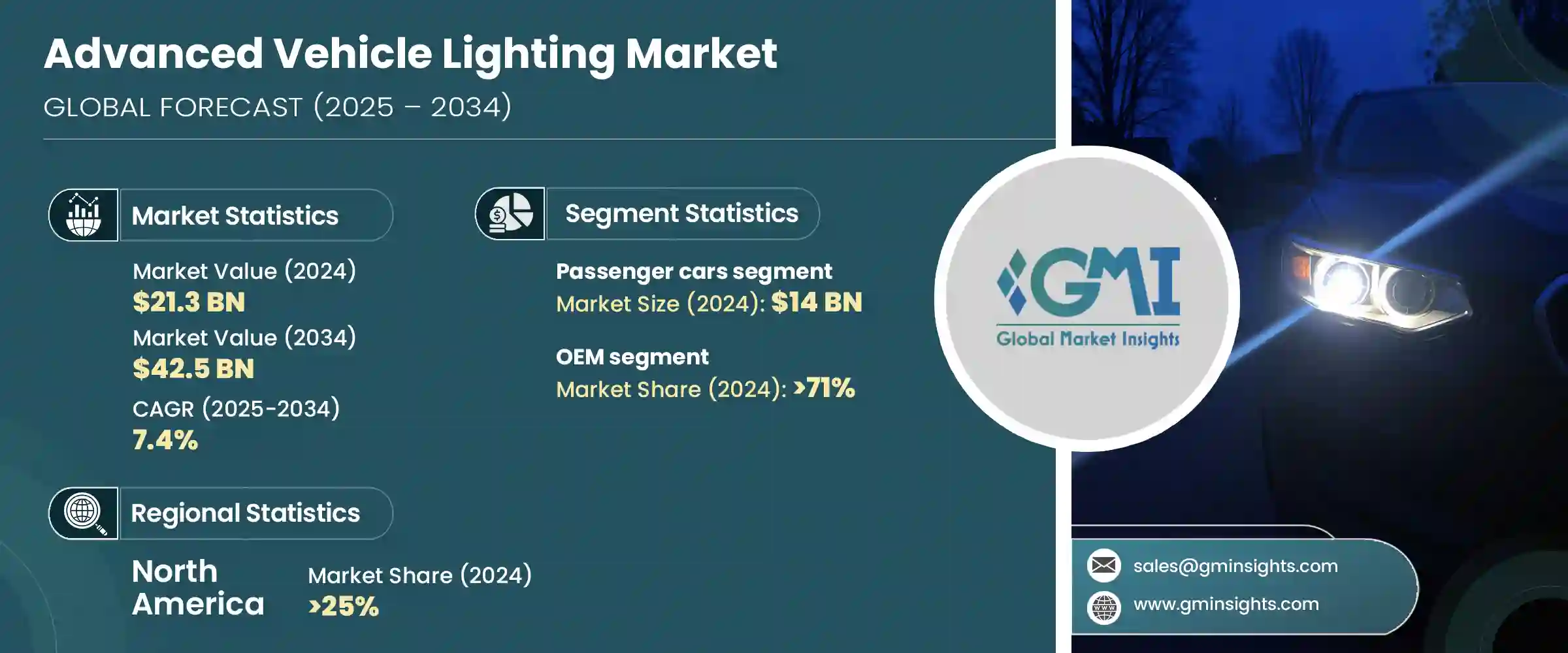

세계의 첨단 자동차 조명 시장 규모는 2024년 213억 달러에 달하였고, CAGR 7.4%로 성장하여 2034년 425억 달러에 이를 것으로 추정됩니다.

이 성장은 ADAS(첨단운전자지원시스템)와 자율주행기술의 통합이 진행되어 최신 자동차의 조명 요건이 변화하고 있는 것이 주요 요인입니다. 매트릭스 LED 및 레이저 헤드 램프와 같은 지능형 조명 솔루션은 센서 기능을 지원하고 눈부심을 줄이기 위해 실시간으로 빔 패턴을 조정할 수 있으므로 점점 더 수요가 증가하고 있습니다.

자동차 제조업체는 특히 시야가 제한된 상황에서 보행자 및 기타 차량과 통신할 수 있는 동적 조명 시스템에 많은 투자를 하고 있습니다. 자동차 분야에서의 경쟁이 격화되고 있는 가운데, 제조업체는 복잡한 조명 디자인을 브랜드의 특징으로서 활용하고 있습니다. 특히 전기차나 고급차에서는 다이나믹 턴 시그널, 3D 테일라이트, 실내 앰비언트 조명 등의 기능이 이제 필수적인 스타일링 요소가 되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작연도 | 2024 |

| 예측연도 | 2025-2034 |

| 시작금액 | 213억 달러 |

| 예측금액 | 425억 달러 |

| CAGR | 7.4% |

유연한 LED와 OLED 기술을 통해 자동차 제조업체는 고도로 맞춤화되고 애니메이션화된 조명 효과를 만들 수 있어 자동차의 정체성과 시각적 매력을 크게 향상시킬 수 있습니다. 따라서 디자이너는 경쟁 시장에서 각 모델을 두드러지게 하는 독자적인 시그니처를 자유롭게 개발할 수 있습니다.

2024년 승용차 부문 시장 규모는 140억 달러에 달했습니다. 주문자 상표 부착 생산(OEM) 기업에게는 고급 조명 기술의 통합이 요구되고 있습니다. 정부기관이 조명 규제를 강화하면서 승용차의 주류는 점점 이러한 시스템을 탑재하게 되고 첨단 자동차 조명 수요는 증가하고 있습니다. 또한 프리미엄 몰입형 실내 디자인에 대한 소비자의 관심으로 인해 자동차 제조 업체는 정교한 차내 경험을 제공하기 위해 멀티컬러 LED 스트립, 동기화된 앰비언트 조명, 맞춤형 라이트 테마를 설치하고 있습니다.

OEM 부문은 2024년에 71%의 점유율을 차지했습니다. DRL, 애니메이션 웰컴 라이트, 변경 가능한 테일라이트 디자인은 혁신과 럭셔리에 중점을 둔 마케팅 캠페인을 지원하면서 자동차의 인식성을 향상시킵니다. 혼잡한 시장에서 두드러지기 위해 OEM은 조명의 연구개발에 큰 자원을 할당하여 소비자를 매료시키고 자사의 제품을 차별화하는 인상적이고 특징적인 디자인의 창조를 목표로 하고 있습니다.

북미의 2024년 첨단 자동차 조명 시장 점유율은 25%에 달했습니다. 북미에서는 첨단 기술을 허가하는 정책이 강화되고 있으며 따라서 고품질 조명 솔루션 시장 기회가 확대되고 있습니다. 또한 미국에서는 전기자동차(EV)와 자율주행차의 급속한 보급이 정부의 인센티브와 소비자의 강한 관심에 의해 추진되고 있으며 LED 매트릭스, LiDAR 내장 헤드램프, 통신에 특화한 조명 기능 등 차세대 자동차의 안전성과 성능에 영향을 미치고 있습니다.

세계의 첨단 자동차 조명 시장의 주요 기업은 OSRAM, ZKW, Koito, Lumileds, Forvia, STANLEY, Valeo 등입니다. 각사는 혁신과 전략적 포지셔닝을 통해 경쟁을 벌이면서 세계 시장 점유율의 대부분을 차지하고 있습니다. 첨단 자동차 조명 분야의 기업은 그 존재감을 확고히 하고 시장 포지션을 강화하기 위해 자율주행차나 전기자동차의 동향에 맞춘 적응형, 스마트, 커넥티드 조명 시스템의 개발 등 조명 기술의 지속적인 혁신에 주력하고 있습니다. 또한 연구개발에 거액의 투자를 실시하여 기능성, 에너지 효율, 디자인의 특징을 강화한 신제품을 투입하고 있습니다.

목차

제1장 조사방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 비용구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 차량 내 적응 조명의 채용 확대

- 차량의 전동화와 EV 생산율의 상승

- 도로와 승객의 안전 중시

- 효율적인 조명 시스템에 관한 정부의 정책

- 업계의 잠재적 위험 및 과제

- 고급 조명 부품의 높은 비용

- 차량 탑재 전자기기와의 시스템 통합의 복잡성

- 시장 기회

- 자율주행용 스마트 조명 개발

- EV 및 고급차 부문의 성장

- 신흥 자동차 제조 시장에서의 확대

- 조명과 차량 통신 시스템의 통합

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 가격 동향

- 지역별

- 제품별

- 생산통계

- 생산거점

- 소비거점

- 수출과 수입

- 코스트 내역 분석

- 특허 분석

- 지속 가능성과 환경 측면

- 지속 가능한 실천

- 폐기물 감축 전략

- 생산에서의 에너지 효율

- 환경친화적인 노력

- 탄소발자국의 고려

제4장 경쟁구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장계획과 자금조달

제5장 시장 추계 및 예측 : 제품별(2021-2034년)

- 주요 동향

- 할로겐

- 제논/HID

- LED

- 레이저

- OLED

- 매트릭스 LED

제6장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 전조등

- 후미등

- 실내 조명

- 사이드&코너 조명

- 안개등과 보조등

- 커뮤니케이션 조명

제7장 시장 추계 및 예측 : 차량별(2021-2034년)

- 주요 동향

- 승용차

- 해치백

- 세단

- SUV

- 상용차

- 라이트듀티

- 미디엄듀티

- 헤비듀티

제8장 시장 추계 및 예측 : 판매채널별(2021-2034년)

- 주요 동향

- OEM

- 애프터마켓

제9장 시장 추계 및 예측 : 추진별(2021-2034년)

- 주요 동향

- ICE

- 전기자동차

- 하이브리드 자동차

- PHEV

- 연료전지 자동차

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 스페인

- 이탈리아

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주

- 동남아시아

- 라틴아메리카

- 브라질

- 아르헨티나

- 멕시코

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 남아프리카

- 사우디아라비아

제11장 기업 프로파일

- Koito Manufacturing Co., Ltd.

- Valeo SA

- Hella GmbH &Co. KGaA(FORVIA Group)

- Marelli Automotive Lighting

- Stanley Electric Co., Ltd.

- ZKW Group GmbH

- OSRAM Continental GmbH

- Hyundai Mobis Co., Ltd.

- Lumileds Holding BV

- Nichia Corporation

- Bosch Mobility Solutions

- TYC Brother Industrial Co., Ltd.

- Texas Instruments

- Denso Corporation

- GE Lighting(Savant Systems Inc.)

- Varroc Engineering Ltd.

- Bosla Lighting

- SL Corporation

- Ichikoh Industries, Ltd.

- JW Speaker Corporation

The Global Advanced Vehicle Lighting Market was valued at USD 21.3 billion in 2024 and is estimated to grow at a CAGR of 7.4% to reach USD 42.5 billion by 2034. This growth is driven largely by the rising integration of advanced driver assistance systems (ADAS) and autonomous driving technologies, which are transforming the lighting requirements of modern vehicles. Intelligent lighting solutions, such as matrix LED and laser headlamps, are increasingly in demand because they can adjust beam patterns in real-time to support sensor functions and reduce glare.

Automakers are heavily investing in dynamic lighting systems that can communicate with pedestrians and other vehicles, especially in conditions with limited visibility. As competition intensifies in the automotive sector, manufacturers are leveraging complex lighting designs as a distinctive brand signature. Features like dynamic turn signals, 3D taillights, and interior ambient lighting are now essential styling elements, particularly in electric and luxury vehicles.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $21.3 Billion |

| Forecast Value | $42.5 Billion |

| CAGR | 7.4% |

Flexible LED and OLED technologies allow automakers to create highly customizable and animated lighting effects that significantly boost a vehicle's identity and visual appeal. These adaptable lighting solutions can be shaped and integrated into various parts of the vehicle, offering designers the freedom to develop unique signatures that set each model apart in a competitive market. The ability to program dynamic animations-such as sequential turn signals, welcoming light shows, or mood-enhancing interior lighting-adds a layer of sophistication that resonates strongly with consumers seeking futuristic and personalized features.

In 2024, the passenger cars segment held USD 14 billion. Regulatory mandates worldwide, such as the adoption of daytime running lights (DRLs) and adaptive driving beam (ADB) systems, are compelling original equipment manufacturers (OEMs) to integrate advanced lighting technologies. These features not only improve visibility during both day and night but also ensure compliance with international safety standards. As governments enforce stricter lighting regulations, mainstream passenger cars are increasingly outfitted with such systems, pushing demand for advanced vehicle lighting higher. Furthermore, consumer interest in premium, immersive interiors is driving automakers to install multi-color LED strips, synchronized mood lighting, and customizable light themes to create a sophisticated in-car experience.

The OEM segment held a 71% share in 2024. Advanced lighting systems have become crucial in defining vehicle design and reinforcing brand identity for manufacturers. Signature LED DRLs, animated welcome lights, and configurable taillight designs contribute to making vehicles instantly recognizable while supporting marketing campaigns focused on innovation and luxury. To stand out in a crowded marketplace, OEMs are dedicating significant resources to lighting research and development, aiming to create striking, distinctive designs that attract consumers and differentiate their offerings.

North America Advanced Vehicle Lighting Market held a 25% share in 2024. The U.S. National Highway Traffic Safety Administration (NHTSA) is increasingly supporting regulations that permit adaptive driving beam (ADB) headlights and other intelligent lighting technologies. These policy shifts encourage automakers to adopt advanced lighting systems that enhance on-road safety, reduce glare, and comply with evolving federal safety standards, generating greater market opportunities for high-quality lighting solutions. Additionally, the rapid growth of electric vehicles (EVs) and autonomous cars in the U.S., spurred by government incentives and strong consumer interest, fuels demand for sophisticated lighting technologies such as LED matrices, LiDAR-integrated headlamps, and communication-focused lighting features that are critical for next-generation vehicle safety and performance.

Leading players in the Global Advanced Vehicle Lighting Market include OSRAM, ZKW, Koito, Lumileds, Forvia, STANLEY, and Valeo. Together, these companies hold a significant portion of the global market share, competing vigorously through innovation and strategic positioning. To solidify their presence and strengthen market positions, companies in the advanced vehicle lighting space are focusing on continuous innovation in lighting technologies, such as the development of adaptive, smart, and connected lighting systems that align with autonomous and electric vehicle trends. They are investing heavily in research and development to introduce new products that offer enhanced functionality, energy efficiency, and distinctive design features. Strategic partnerships and collaborations with automotive OEMs allow these companies to integrate their lighting solutions seamlessly into vehicle platforms, ensuring early adoption and long-term contracts.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Vehicle

- 2.2.4 Propulsion

- 2.2.5 Sales Channel

- 2.2.6 Application

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Key decision points for industry executives

- 2.4.2 Critical success factors for market players

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factor affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing adoption of adaptive lighting in vehicles

- 3.2.1.2 Rising vehicle electrification and EV production rates

- 3.2.1.3 Increasing emphasis on road and passenger safety

- 3.2.1.4 Government mandates for efficient lighting systems

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of advanced lighting components

- 3.2.2.2 Complexity in system integration with vehicle electronics

- 3.2.3 Market opportunities

- 3.2.3.1 Development of smart lighting for autonomous driving

- 3.2.3.2 Growth in EV and luxury vehicle segments

- 3.2.3.3 Expansion in emerging automotive manufacturing markets

- 3.2.3.4 Integration of lighting with vehicle communication systems

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Technology and Innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Price trends

- 3.8.1 By region

- 3.8.2 By product

- 3.9 Production statistics

- 3.9.1 Production hubs

- 3.9.2 Consumption hubs

- 3.9.3 Export and import

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.12.5 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans and funding

Chapter 5 Market Estimates & Forecast, By Product, 2021 - 2034 ($Mn & Units)

- 5.1 Key trends

- 5.2 Halogen

- 5.3 Xenon/HID

- 5.4 LED

- 5.5 Laser

- 5.6 OLED

- 5.7 Matrix LED

Chapter 6 Market Estimates & Forecast, By Application, 2021 - 2034 ($Mn & Units)

- 6.1 Key trends

- 6.2 Front Lighting

- 6.3 Rear Lighting

- 6.4 Interior Lighting

- 6.5 Side & Corner Lighting

- 6.6 Fog and Auxiliary Lights

- 6.7 Communication Lighting

Chapter 7 Market Estimates & Forecast, By Vehicle, 2021 - 2034 ($Mn & Units)

- 7.1 Key trends

- 7.2 Passenger Car

- 7.2.1 Hatchback

- 7.2.2 Sedan

- 7.2.3 SUV

- 7.3 Commercial Vehicle

- 7.3.1 Light-duty

- 7.3.2 Medium-duty

- 7.3.3 Heavy-duty

Chapter 8 Market Estimates & Forecast, By Sales Channel, 2021 - 2034 ($Mn & Units)

- 8.1 Key trends

- 8.2 OEM

- 8.3 Aftermarket

Chapter 9 Market Estimates & Forecast, By Propulsion, 2021 - 2034 ($Mn & Units)

- 9.1 Key trends

- 9.2 ICE

- 9.3 BEV

- 9.4 HEV

- 9.5 PHEV

- 9.6 FCEV

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 ($Mn & Units)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Spain

- 10.3.5 Italy

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 Australia

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Argentina

- 10.5.3 Mexico

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 South Africa

- 10.6.3 Saudi Arabia

Chapter 11 Company Profiles

- 11.1 Koito Manufacturing Co., Ltd.

- 11.2 Valeo S.A.

- 11.3 Hella GmbH & Co. KGaA (FORVIA Group)

- 11.4 Marelli Automotive Lighting

- 11.5 Stanley Electric Co., Ltd.

- 11.6 ZKW Group GmbH

- 11.7 OSRAM Continental GmbH

- 11.8 Hyundai Mobis Co., Ltd.

- 11.9 Lumileds Holding B.V.

- 11.10 Nichia Corporation

- 11.11 Bosch Mobility Solutions

- 11.12 TYC Brother Industrial Co., Ltd.

- 11.13 Texas Instruments

- 11.14 Denso Corporation

- 11.15 GE Lighting (Savant Systems Inc.)

- 11.16 Varroc Engineering Ltd.

- 11.17 Bosla Lighting

- 11.18 SL Corporation

- 11.19 Ichikoh Industries, Ltd.

- 11.20 J.W. Speaker Corporation