|

시장보고서

상품코드

1773447

와인 및 그레이프 머스트 시장 기회와 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Wine and Grape Must Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

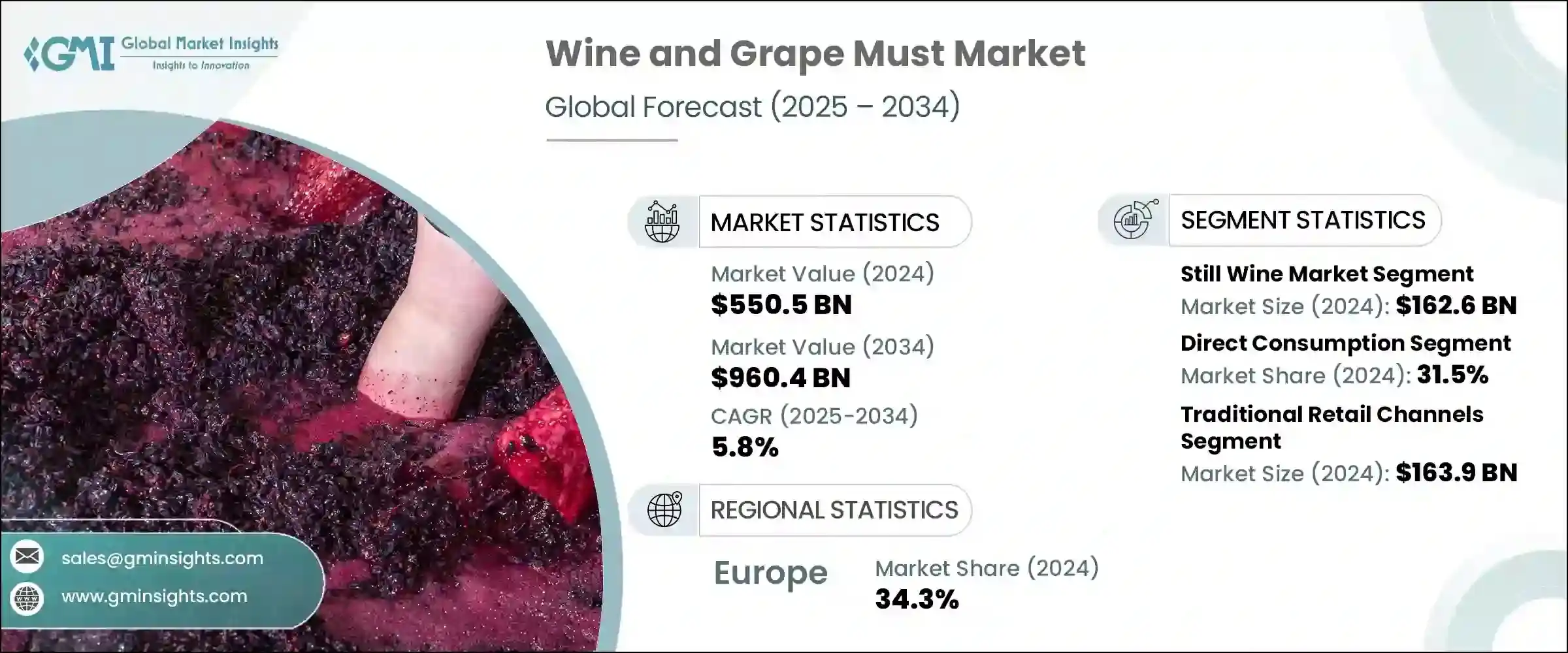

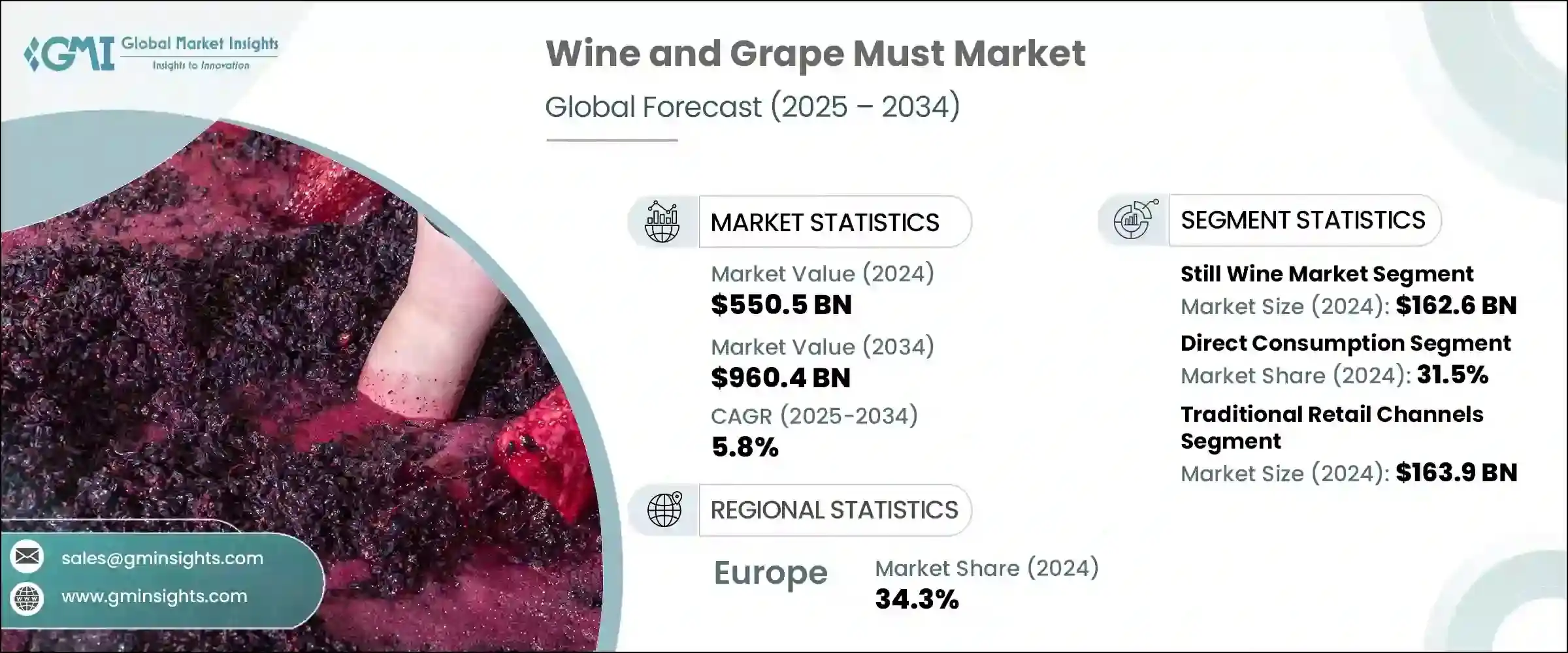

세계의 와인 및 그레이프 머스트 시장은 2024년에는 5,505억 달러로 평가되었고, CAGR 5.8%로 성장하여 2034년에는 9,604억 달러에 이를 것으로 추정됩니다.

더 많은 소비자들이 지속 가능한 방식으로 생산된 프리미엄 음료에 대한 선호도가 높아짐에 따라, 고품질의 장인정신이 깃든 와인에 대한 전 세계적인 수요가 시장 확대를 주도하고 있습니다. 포도 재배 기술의 발전과 기후 적응성 향상으로 수확량과 포도 품질이 향상되어 이 분야의 안정적인 성장을 뒷받침하고 있습니다. 건강 지향적이고 환경 친화적인 라이프스타일로 변화하는 가운데, 소비자들은 유기농, 바이오다이나믹, 지역산 포도를 선호하고 있습니다.

온라인 소매 및 소비자 직접 판매 채널의 영향력이 커짐에 따라 프리미엄 와인 및 포도주가 그 어느 때보다 쉽게 접할 수 있게 되면서 전체 세계 시장의 성장이 더욱 가속화되고 있습니다. 또한, 캔이나 재활용 가능한 병과 같은 혁신적인 포장 형태는 환경 부담을 줄이면서 편의성을 높이고, 지속가능성을 중시하는 구매층에게 어필하고 있습니다. 정품 지향, 클린 라벨 트렌드, 지역적 특성은 이제 주요 판매 포인트가 되었으며, 구매자들은 한 모금 한 모금 마실 때마다 진정한 경험을 원하고 있습니다. 이러한 직접 소비 트렌드는 브랜드와 최종 소비자와의 관계를 재구축하고, 보다 개인화되고 투명하게 소통할 수 있는 기회를 제공합니다. 시장의 변화는 모든 접점에서 프리미엄 품질, 추적가능성, 지속가능성에 대한 소비자의 기대에 의해 주도되고 있습니다.

| 시장 범위 | |

|---|---|

| 개시 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 개시 금액 | 5,505억 달러 |

| 예측 금액 | 9,604억 달러 |

| CAGR | 5.8% |

2024년 스틸 와인 부문의 매출은 1,626억 달러로 29.5%의 점유율을 차지했습니다. 이 분야는 지역적 특색, 유기농, 지속 가능한, 매력적인 배경을 가진 와인에 대한 수요가 증가함에 따라 계속 성장하고 있습니다. 스파클링 와인은 특히 개발도상국에서 인기가 높아지고 있으며, 고급스러움과 축하의 상징으로 여겨지는 스파클링 와인의 인기가 높아지고 있으며, 이는 향상심 강한 소비자 트렌드와도 일치합니다. 강화 와인은 전통 품종과 크래프트 칵테일 문화 및 고급 레스토랑과 관련된 고급 옵션에 대한 새로운 관심에 힘입어 애호가들 사이에서 틈새 시장으로 인기를 유지하고 있습니다.

직접 소비 부문은 2024년 31.5%의 점유율을 차지했으며, 2034년까지 5.2%의 연평균 복합 성장률(CAGR)을 보일 것으로 예측됩니다. 더 많은 소비자들이 신선하고 자연적으로 생산되고 최소한의 가공을 거친 와인과 포도즙을 선호함에 따라 이 소비 형태가 점점 더 많은 견인력을 얻고 있습니다. 와인과 포도주의 독특한 미각 프로파일과 천연 건강 증진 특성이 요리와 기능성 제품에 활용되면서 다양한 음료 및 식품 응용 분야에서 수요가 급증하고 있습니다. 소비자들이 식품 및 음료의 성분에 대한 인식이 높아짐에 따라, 자연 발효 및 클린 라벨 제품은 모든 카테고리에 걸쳐 매력적으로 다가오고 있습니다.

2024년 유럽의 와인 및 포도주 시장 점유율은 34.3%였으며, 이 지역은 품질에 대한 오랜 명성과 지리적 정체성, 유기농 인증 와인 생산에 대한 헌신으로 세계적인 리더로 자리매김하고 있습니다. 기후에 영향을 받는 포도 재배 관행과 지역적 스토리텔링은 유럽 와인의 매력을 더욱 높여줍니다. 북미에서는 지속가능성과 소량 생산의 혁신이 중요한 원동력이 되고 있으며, 특히 건강 지향적인 제품 라인에서 포도 수요가 증가하고 있습니다. 다른 지역에서는 동남아시아, 남미, 중국 시장이 빠르게 성장하고 있으며, 오랜 전통과 혁신적인 기술을 결합하여 생산과 소비를 모두 늘리고 있습니다. 지역적 다양성은 업계의 세계 성장의 특징이 되고 있습니다.

세계 와인 및 포도주 산업경쟁 구도를 형성하는 주요 기업으로는 Treasury Wine Estates, The Wine Group, E. & J. Gallo Winery, Constellation Brands, Inc., and Pernod Ricard 등이 있습니다. 와인 및 포도 부문에서는 지속 가능한 생산 방식, 프리미엄 제품 개발, 소비자와의 직접적인 관계에 투자하는 기업이 늘고 있습니다. 원산지, 유기농 인증, 자연친화적인 제조법을 중시하는 안목 있는 소비자들을 위해 추적 가능성과 신뢰성을 중시하고 있습니다. 브랜드는 디지털 플랫폼과 전자상거래를 활용하여 개인화된 경험을 창출하고, 소비자들이 한정판 제품에 쉽게 접근할 수 있도록 돕고 있습니다. 신흥 시장에 전략적으로 진출함으로써 기업은 새로운 고객층을 개척하고, 패키지의 지속적인 혁신은 환경 목표를 지원합니다. 또한, 많은 브랜드가 지역 전통과 와인 양조 전통에 대한 스토리텔링을 강화하여 소비자와의 정서적 유대감을 강화하는 데 주력하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급업체 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 미치는 요인

- 파괴적 변화

- 업계에 대한 영향요인

- 성장 촉진요인

- 업계의 잠재적 리스크&과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품별

- 향후 시장 동향

- 기술 및 혁신 상황

- 현재 기술 동향

- 신기술

- 특허 상황

- 무역 통계(HS코드)(주 : 무역 통계는 주요 국가에 한해 제공됩니다)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경 측면

- 지속가능한 관행

- 폐기물 감축 전략

- 생산 에너지 효율

- 친환경 대처

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 인수합병(M&A)

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추산·예측 : 제품 유형별, 2021년-2034년

- 주요 동향

- 스틸 와인 시장

- 레드 와인 부문

- 프리미엄 레드 와인

- 중급 레드 와인

- 밸류 레드 와인

- 화이트 와인 부문

- 프리미엄 화이트 와인

- 중급 화이트 와인

- 밸류 화이트 와인

- 로제 와인 부문

- 레드 와인 부문

- 스파클링 와인 시장

- 샴페인 및 프리미엄 스파클링

- 프로세코 및 중급 스파클링

- 밸류 스파클링 와인

- 강화 와인 시장

- 포트 및 셰리

- 버몬트 및 아페리티프

- 기타 강화 와인

- 그레이프 머스트 시장

- 신선 그레이프 머스트

- 농축 그레이프 머스트

- 정류 농축 그레이프 머스트

- 오가닉 그레이프 머스트

- 스페셜티 와인 및 대체 와인 제품

- 오가닉 와인 및 바이오 다이나믹 와인

- 저알코올 와인 및 무알코올 와인

- 통조림 및 대체 포장

- 자체브랜드 와인

제6장 시장 추산·예측 : 용도별, 2021년-2034년

- 주요 동향

- 직접 소비

- 점내 음식(레스토랑, 바, 호텔)

- 점외 소비(소매점, 슈퍼마켓)

- 소비자 직접 판매

- 식품 및 음료 업계용 용도

- 요리용 와인 및 요리 응용

- 음료 블렌드 및 향료(Flavor)

- 식품 가공 및 제조

- 산업 용도

- 의약품 및 식이보충제로서의 사용

- 화장품 및 퍼스널케어 용도

- 화학 및 산업 처리

- 포도 과즙 특정 용도

- 와인 양조 및 발효

- 식품 및 제과 업계

- 건강식품 및 보충제 제조

- 기존 및 문화적 용도

제7장 시장 추산·예측 : 유통 채널별, 2021년-2034년

- 주요 동향

- 기존 소매 채널

- 슈퍼마켓 및 하이퍼마켓

- 와인 전문점

- 편의점

- 백화점

- On-Premise 채널

- 레스토랑 및 고급 레스토랑

- 바 및 펍

- 호텔 및 호스피탈리티

- 와인바 및 테이스팅 룸

- 직접 판매채널

- 와이너리 직접 판매

- 와인 클럽 및 구독

- 셀러 도어 세일

- 와인 관광 및 테이스팅 체험

- E-Commerce 및 디지털 채널

- 온라인 와인 소매업체

- 마켓플레이스 플랫폼

- 모바일 애플리케이션

- 소셜 커머스

- 도매 및 유통

- 기존 three-tier 시스템

- 전문 와인 판매업체

- 수출입 채널

- 브로커 네트워크

제8장 시장 추산·예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카공화국

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 개요

- E. &J. Gallo Winery

- Constellation Brands, Inc.

- Treasury Wine Estates

- Pernod Ricard

- The Wine Group

- Castel Group

- Accolade Wines

- Caviro Group

- Freixenet Group

- Changyu Pioneer Wine Company

- Great Wall Wine Company

- Dynasty Fine Wines Group

- Suntory Holdings

- Sapporo Holdings

The Global Wine and Grape Must Market was valued at USD 550.5 billion in 2024 and is estimated to grow at a CAGR of 5.8% to reach USD 960.4 billion by 2034. Strong global demand for high-quality and artisanal wine continues to drive market expansion, as more consumers gravitate toward premium, sustainably produced beverages. Evolving viticulture techniques and improved climate adaptability have enhanced both yield and grape quality, supporting consistent growth in this space. Consumers are showing stronger preferences for organic, biodynamic, and locally crafted options, driven by an increasing shift toward health-aware and environmentally responsible lifestyles.

The rising influence of online retail and direct-to-consumer distribution channels has made premium wine and grape must more accessible than ever, further accelerating growth across global markets. In addition, innovative packaging formats such as cans and recyclable bottles are appealing to sustainability-minded buyers, enhancing convenience while reducing environmental impact. Authenticity, clean-label trends, and regional character are now major selling points, as buyers seek genuine experiences with every sip. This direct consumption trend is reshaping how brands connect with end-users, offering a more personalized and transparent engagement. The market's transformation is being led by consumer expectations for premium quality, traceability, and sustainability across all touchpoints.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $550.5 Billion |

| Forecast Value | $960.4 Billion |

| CAGR | 5.8% |

In 2024, the still wine segment generated USD 162.6 billion, claiming a 29.5% share. This segment continues to thrive as demand rises for regionally distinct, organic, and sustainable selections with compelling backstories. Sparkling wine is also gaining popularity, especially in developing regions, where it is seen as a symbol of luxury and celebration, aligning with aspirational consumer trends. Fortified wine remains a niche favorite among enthusiasts, supported by renewed interest in heritage varieties and high-end options connected to craft cocktail culture and fine dining.

The direct consumption segment represented a 31.5% share in 2024 and projected to grow at a CAGR of 5.2% through 2034. This mode of consumption is experiencing increased traction as more consumers favor wines and grape must that are fresh, naturally produced, and minimally processed. There is a notable surge in demand for wine and grape must in broader food and beverage applications, where their unique taste profiles and natural health-enhancing qualities leveraged in culinary and functional products. As consumers become more aware of what goes into their food and drinks, naturally fermented and clean-label offerings are becoming more attractive across categories.

Europe Wine and Grape Must Market held a 34.3% share in 2024. The region remains a global leader due to its long-established reputation for quality and its commitment to producing wines with geographic identity and organic certification. Climate-driven viticultural practices and regional storytelling further enhance the appeal of European wines. In North America, sustainability and small-batch innovation are key drivers, while demand for grapes is growing, especially in wellness-oriented product lines. Elsewhere, markets in Southeast Asia, South America, and China are rapidly expanding, combining age-old traditions with innovative technology to grow both production and consumption. Regional diversity is becoming a hallmark of the industry's global growth.

Key players shaping the competitive dynamics of the Global Wine and Grape Must Industry include Treasury Wine Estates, The Wine Group, E. & J. Gallo Winery, Constellation Brands, Inc., and Pernod Ricard. Companies within the wine and grape sector are increasingly investing in sustainable production practices, premium product development, and direct consumer relationships. Emphasis is placed on traceability and authenticity to cater to a discerning audience that values origin, organic certification, and natural methods. Brands are leveraging digital platforms and e-commerce to create personalized experiences, making it easier for consumers to access exclusive products. Strategic expansion into emerging markets allows companies to tap into new customer bases, while continuous innovation in packaging supports environmental goals. Many are also enhancing storytelling around regional heritage and winemaking traditions to build stronger emotional connections with their audiences.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Product

- 2.2.3 Application

- 2.2.4 Distribution channel

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product Type, 2021 - 2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Still wine market

- 5.2.1 Red wine segment

- 5.2.1.1 Premium red wine

- 5.2.1.2 Mid-range red wine

- 5.2.1.3 Value red wine

- 5.2.2 White wine segment

- 5.2.2.1 Premium white wine

- 5.2.2.2 Mid-range white wine

- 5.2.2.3 Value white wine

- 5.2.3 Rose wine segment

- 5.2.1 Red wine segment

- 5.3 Sparkling wine market

- 5.3.1 Champagne and premium sparkling

- 5.3.2 Prosecco and mid-range sparkling

- 5.3.3 Value sparkling wine

- 5.4 Fortified wine market

- 5.4.1 Port and sherry

- 5.4.2 Vermouth and aperitifs

- 5.4.3 Other fortified wines

- 5.5 Grape must market

- 5.5.1 Fresh grape must

- 5.5.2 Concentrated grape must

- 5.5.3 Rectified concentrated grape must

- 5.5.4 Organic grape must

- 5.6 Specialty and alternative wine products

- 5.6.1 Organic and biodynamic wines

- 5.6.2 Low and No-alcohol wines

- 5.6.3 Canned and alternative packaging

- 5.6.4 Private label wines

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Direct consumption

- 6.2.1 On-premise consumption (restaurants, bars, hotels)

- 6.2.2 Off-premise consumption (retail, supermarkets)

- 6.2.3 Direct-to-consumer sales

- 6.3 Food and beverage industry applications

- 6.3.1 Cooking wine and culinary applications

- 6.3.2 Beverage blending and flavoring

- 6.3.3 Food processing and manufacturing

- 6.4 Industrial applications

- 6.4.1 Pharmaceutical and nutraceutical uses

- 6.4.2 Cosmetic and personal care applications

- 6.4.3 Chemical and industrial processing

- 6.5 Grape must specific applications

- 6.5.1 Winemaking and fermentation

- 6.5.2 Food and confectionery industry

- 6.5.3 Health food and supplement manufacturing

- 6.5.4 Traditional and cultural uses

Chapter 7 Market Estimates and Forecast, By Distribution Channel, 2021 - 2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Traditional retail channels

- 7.2.1 Supermarkets and hypermarkets

- 7.2.2 Specialty wine stores

- 7.2.3 Convenience stores

- 7.2.4 Department stores

- 7.3 On-premise channels

- 7.3.1 Restaurants and fine dining

- 7.3.2 Bars and pubs

- 7.3.3 Hotels and hospitality

- 7.3.4 Wine bars and tasting rooms

- 7.4 Direct sales channels

- 7.4.1 Winery direct-to-consumer

- 7.4.2 Wine clubs and subscriptions

- 7.4.3 Cellar door sales

- 7.4.4 Wine tourism and tasting experiences

- 7.5 E-commerce and digital channels

- 7.5.1 Online wine retailers

- 7.5.2 Marketplace platforms

- 7.5.3 Mobile applications

- 7.5.4 Social commerce

- 7.6 Wholesale and Distribution

- 7.6.1 Traditional three-tier system

- 7.6.2 Specialized wine distributors

- 7.6.3 Import/Export channels

- 7.6.4 Broker networks

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.3.7 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 E. & J. Gallo Winery

- 9.2 Constellation Brands, Inc.

- 9.3 Treasury Wine Estates

- 9.4 Pernod Ricard

- 9.5 The Wine Group

- 9.6 Castel Group

- 9.7 Accolade Wines

- 9.8 Caviro Group

- 9.9 Freixenet Group

- 9.10 Changyu Pioneer Wine Company

- 9.11 Great Wall Wine Company

- 9.12 Dynasty Fine Wines Group

- 9.13 Suntory Holdings

- 9.14 Sapporo Holdings