|

시장보고서

상품코드

1782148

물류 분야 생성형 AI 시장 : 시장 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Generative AI in Logistics Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

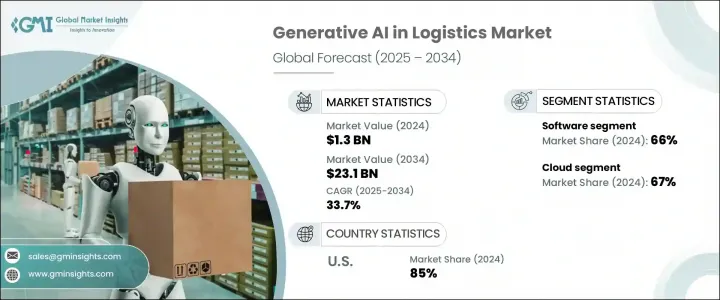

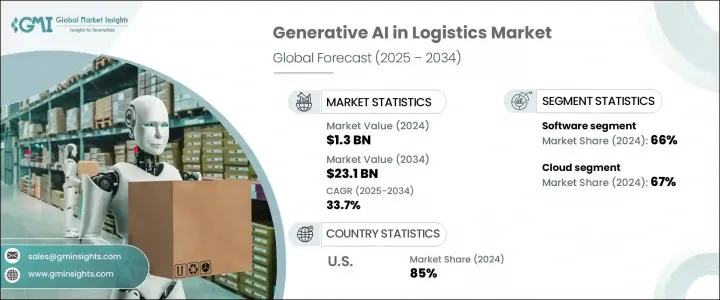

세계의 물류 분야 생성형 AI 시장 규모는 2024년에 13억 달러로 평가되었고, CAGR 33.7%로 성장할 전망이며, 2034년에는 231억 달러에 이를 것으로 예측됩니다.

이 기술은 실시간 인텔리전스와 장기적인 전략 예측을 모두 제공함으로써 공급망 운영을 근본적으로 변화시키고 있습니다. 수천 개의 배송 경로와 운송 시나리오를 시뮬레이션함으로써 물류 업체는 재고 계획을 미세 조정하고 운임을 낮추며 예기치 않은 혼란에 대비할 수 있습니다. 또한 AI를 활용한 수요 예측은 리소스 이용을 효율화하고 다이내믹 라우팅 도구는 배송 일정을 개선합니다. 업무 효율과 비용 관리가 보다 중요해지는 가운데, 시장의 미래를 형성하는 중요한 힘으로서 생성형 AI의 통합이 부상하고 있습니다.

생성형 AI는 고객의 행동과 선호도를 분석하여 물류 기업이 서비스의 개인화를 강화할 수 있도록 합니다. 이러한 지능형 시스템은 실시간 경고를 발행하고 이상적인 배달 창구를 권장하며 고객과의 상호 작용을 기반으로 서비스를 자동으로 조정할 수 있습니다. 이 수준의 사용자 정의는 고객의 만족도와 충성도를 높이는 동시에 기업이 프리미엄 가격을 청구할 수 있도록 합니다. 경쟁이 치열한 업계에서는 AI를 활용한 개인화된 물류 체험이 계속해서 기세를 늘리고 있습니다. 또한 연료 비용과 배출량을 줄이는 압력이 증가함에 따라 물류 차량은 교통 패턴, 날씨 예측 및 과거 데이터를 사용하여 최적화 된 경로를 제안하는 인공지능에 점점 더 의존하고 있으며 더 깨끗하고 슬림한 작업이 표준이 되었습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 13억 달러 |

| 예측 금액 | 231억 달러 |

| CAGR | 33.7% |

2024년, 소프트웨어 분야의 점유율은 66%로, 2034년까지 CAGR 32%로 성장할 전망입니다. 물류 팀은 재고 부족, 배송 지연, 갑작스런 수요 급증 등 다수공급망 혼란을 시뮬레이트하는 AI 주도 예측 도구를 선호합니다. 이러한 도구는 기업이 업무를 사전에 조정하고 효율성과 비용을 모두 개선하는 데 도움이 됩니다. 이러한 최신 솔루션은 오래된 모델보다 빠른 결과를 제공하고 레거시 시스템과의 통합이 쉽기 때문에 시간이 많이 걸리는 맞춤형 옵션보다 매력적입니다.

클라우드 도입 분야는 2024년에 67%의 점유율을 차지했으며, 2034년까지 연평균 복합 성장률(CAGR) 32%로 강력한 성장을 유지할 것으로 예측됩니다. 물류 업무가 지리적으로 분산됨에 따라 기업은 변화하는 비즈니스 요구에 따라 즉시 확장할 수 있는 유연한 클라우드 기반 AI 솔루션을 선택하게 되었습니다. 전통적인 서버 설정과 달리 클라우드 플랫폼은 특히 수요가 급증할 때, 특히 계절 피크 및 예기치 않은 시장 이동 시 등 실시간 컴퓨팅 파워와 데이터 스토리지를 제공합니다. 이러한 적응성을 통해 클라우드 시스템은 세계 공급망에 필수적인 요소가 되어 이 분야에서의 이점을 높일 수 있습니다.

북미의 물류 분야 생성형 AI 시장은 85%의 점유율을 차지했으,며 2024년에는 3억 5,520만 달러를 창출했습니다. 이 나라는 IBM, 마이크로소프트, 아마존, Oracle, 패런티어 테크놀로지스, SAP, 엔비디아, 구글 등의 선도적인 하이테크 기업에 힘입어 공급망에 첨단 인공지능을 도입하는 핵심 기지로 부상하고 있습니다. 이러한 기업은 엔터프라이즈 지원 AI 인프라를 제공하며, 물류 제공업체는 알고리즘 개발 및 배포를 가속화하는 최첨단 기능에 즉시 액세스할 수 있습니다. 이 신속한 혁신주기로 미국은 세계 물류 AI의 전면 주자로 자리매김하고 있습니다.

물류 분야 생성형 AI 시장의 주요 기업들은 전략적 클라우드 파트너십, 확장가능한 AI 모델, 업계에 특화된 머신러닝 툴을 두배로 늘리고 있습니다. 또한 지역 및 분야별 물류 과제에 신속하게 적응하는 모듈형 AI 솔루션에 주력하고 있습니다. API 통합을 통한 사용자 접근성 향상, 플러그 앤 플레이 플랫폼 구축, 실시간 데이터 가시성 실현은 공통 목표입니다. 이러한 기업은 민첩한 개발 환경에 투자하고 실시간 물류 수요에 대응하는 저지연 컴퓨팅을 제공합니다. 고객 참여도를 높이고 운영 리스크를 완화하고 빠르게 진화하는 시장 상황에서 브랜드가 경쟁 우위를 차지하기 위해 경쟁 구도 분석, 지속가능성에 중점을 둔 경로 최적화 및 예측 분석 기능이 우선합니다.

목차

제1장 조사 방법

- 시장의 범위 및 정의

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역 및 국가

- 기본 추정 및 계산

- 기준 연도 계산

- 시장 예측의 주요 동향

- 1차 조사 및 검증

- 1차 정보

- 예측 모델

- 조사의 전제 및 한계

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 비용 구조

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 혁신

- 업계에 미치는 영향요인

- 성장 촉진요인

- 강화된 공급망 최적화

- 반복 프로세스 자동화

- 고객의 개인화된 체험

- 비용 효율적인 차량 및 루트 관리

- 업계의 잠재적 위험 및 과제

- 데이터 프라이버시 및 보안 위험

- 레거시 시스템과의 통합 복잡성

- 시장 기회

- AI에 의한 수요 예측 및 재고 최적화

- 스마트 창고를 위한 디지털 트윈 만들기

- 자율 루트 계획 및 차량 관리

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥 기술

- 사례 연구

- 이용 사례

- 비용 내역 분석

- 특허 분석

- 지속가능성 및 환경 측면

- 지속가능한 관행

- 폐기물 감축 전략

- 생산에서 에너지 효율

- 환경 친화적인 노력

- 탄소발자국의 고려

제4장 경쟁 구도

- 서문

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 전략적 전망 매트릭스

- 주요 발전

- 합병 및 인수

- 파트너십 및 협업

- 신제품 발매

- 확장계획 및 자금조달

제5장 시장 추계 및 예측 : 유형별(2021-2034년)

- 주요 동향

- 변분 오토엔코더

- 생성적 적대 네트워크

- 리커런트 신경망

- 장기 단기 기억 네트워크

- 트랜스포머

제6장 시장 추계 및 예측 : 컴포넌트별(2021-2034년)

- 주요 동향

- 소프트웨어

- 서비스

제7장 시장 추계 및 예측 : 전개 모드별(2021-2034년)

- 주요 동향

- 클라우드

- 온프레미스

제8장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 루트 최적화

- 수요 예측

- 창고 및 재고 관리

- 공급망 자동화

- 예측 유지보수

- 리스크 관리

- 맞춤형 물류 솔루션

- 기타

제9장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 제3자물류 공급자

- 화물 운송업자

- 전자상거래 기업

- 제조업자

제10장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 러시아

- 북유럽 국가

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 동남아시아

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 아랍에미리트(UAE)

- 사우디아라비아

- 남아프리카

제11장 기업 프로파일

- Amazon Web Services

- DHL Group

- FedEx

- Flexport

- Four Kites

- IBM

- Locus

- Maersk

- Microsoft

- NVIDIA

- Open AI

- Optimal Dynamics

- Oracle

- Palantir Technologies

- Project44

- Salesforce

- SAP

- UPS

- XPO Logistics

The Global Generative AI in Logistics Market was valued at USD 1.3 billion in 2024 and is estimated to grow at a CAGR of 33.7% to reach USD 23.1 billion by 2034. This technology is fundamentally transforming supply chain operations by delivering both real-time intelligence and long-term strategic forecasting. By simulating thousands of delivery routes and transport scenarios, logistics providers can fine-tune inventory planning, lower freight expenses, and stay prepared for unexpected disruptions. AI-powered demand forecasting also streamlines resource use, while dynamic routing tools improve delivery timelines. As operational efficiency and cost control become more important, the integration of generative AI has emerged as a key force shaping the market's future.

Generative AI enables logistics firms to enhance service personalization by analyzing customer behavior and preferences. These intelligent systems can trigger real-time alerts, recommend ideal delivery windows, and automatically adjust services based on client interactions. This level of customization boosts customer satisfaction and loyalty while allowing businesses to charge premium prices. In a competitive industry, personalized logistics experiences powered by AI continue to drive momentum. Moreover, with growing pressure to reduce fuel costs and emissions, logistics fleets increasingly rely on AI to suggest optimized routes using traffic patterns, weather predictions, and historical data, making cleaner and leaner operations the standard.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $1.3 Billion |

| Forecast Value | $23.1 Billion |

| CAGR | 33.7% |

In 2024, the software segment held a 66% share and is set to grow at a CAGR of 32% through 2034. Logistics teams have prioritized AI-driven predictive tools that simulate numerous supply chain disruptions like stock shortages, delivery hold-ups, or sudden demand spikes. These tools help firms adjust operations proactively, improving both efficiency and cost outcomes. These modern solutions offer faster results than older models and integrate easily with legacy systems, making them more attractive than time-consuming, custom-built options.

The cloud deployment segment held a 67% share in 2024 and is expected to maintain strong growth at a CAGR of 32% through 2034. As logistics operations become more geographically dispersed, firms are choosing flexible, cloud-based AI solutions that scale instantly based on fluctuating business needs. Unlike traditional server setups, cloud platforms provide real-time computing power and data storage as demand surges, especially during seasonal peaks or unexpected market shifts. This adaptability makes cloud systems critical for global supply chains, reinforcing their dominance in the sector.

North America Generative AI In Logistics Market held 85% share and generated USD 355.2 million in 2024. The country has emerged as a central hub for advanced AI adoption in supply chains, backed by major tech firms like IBM, Microsoft, Amazon, Oracle, Palantir Technologies, SAP, NVIDIA, and Google. These companies offer enterprise-ready AI infrastructure, giving logistics providers immediate access to cutting-edge capabilities that accelerate algorithm development and deployment. This rapid innovation cycle positions the U.S. as a frontrunner in logistics AI worldwide.

Leading firms in the Generative AI in Logistics Market are doubling down on strategic cloud partnerships, scalable AI models, and industry-specific machine learning tools. They're also focusing on modular AI solutions that adapt quickly to regional and sector-specific logistics challenges. Enhancing user accessibility through API integration, building plug-and-play platforms, and enabling real-time data visibility are common goals. These companies invest in agile development environments and provide low-latency computing to meet real-time logistics demands. Customization capabilities, sustainability-focused route optimization, and predictive analytics are being prioritized to improve customer engagement and reduce operational risks, giving brands a competitive edge in a fast-evolving market landscape.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Type

- 2.2.3 Component

- 2.2.4 Deployment mode

- 2.2.5 Application

- 2.2.6 End Use

- 2.3 TAM Analysis, 2025-2034

- 2.4 CXO perspectives: strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier landscape

- 3.1.2 Profit margin

- 3.1.3 Cost structure

- 3.1.4 Value addition at each stage

- 3.1.5 Factors affecting the value chain

- 3.1.6 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Enhanced supply chain optimization

- 3.2.1.2 Automation of repetitive process

- 3.2.1.3 Personalized experience of the customers

- 3.2.1.4 Cost-efficient fleet & route management

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Data privacy and security risks

- 3.2.2.2 Integration complexity with legacy systems

- 3.2.3 Market opportunities

- 3.2.3.1 AI driven demand forecasting and inventory optimization

- 3.2.3.2 Digital twin creation for smart warehousing

- 3.2.3.3 Autonomous route planning and fleet management

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter’s analysis

- 3.6 PESTEL analysis

- 3.7 Technology and innovation landscape

- 3.7.1 Current technological trends

- 3.7.2 Emerging technologies

- 3.8 Case studies

- 3.9 Use cases

- 3.10 Cost breakdown analysis

- 3.11 Patent analysis

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

- 3.12.5 Carbon footprint considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 LATAM

- 4.2.5 MEA

- 4.3 Competitive analysis of major market players

- 4.4 Competitive positioning matrix

- 4.5 Strategic outlook matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans and funding

Chapter 5 Market Estimates & Forecast, By Type, 2021 - 2034 (USD Million)

- 5.1 Key trends

- 5.2 Variational autoencoder

- 5.3 Generative adversarial networks

- 5.4 Recurrent neural networks

- 5.5 Long short-term memory networks

- 5.6 Transformers

Chapter 6 Market Estimates & Forecast, By Component, 2021 - 2034 (USD Million)

- 6.1 Key trends

- 6.2 Software

- 6.3 Services

Chapter 7 Market Estimates & Forecast, By Deployment Mode, 2021 - 2034 (USD Million)

- 7.1 Key trends

- 7.2 Cloud

- 7.3 On-premises

Chapter 8 Market Estimates & Forecast, By Application, 2021 - 2034 (USD Million)

- 8.1 Key trends

- 8.2 Route optimization

- 8.3 Demand forecasting

- 8.4 Warehouse and inventory management

- 8.5 Supply chain automation

- 8.6 Predictive maintenance

- 8.7 Risk management

- 8.8 Customized logistics solution

- 8.9 Others

Chapter 9 Market Estimates & Forecast, By End Use, 2021- 2034 (USD Million)

- 9.1 Key trends

- 9.2 Third party logistics providers

- 9.3 Freight forwarders

- 9.4 E-commerce companies

- 9.5 Manufacturers

Chapter 10 Market Estimates & Forecast, By Region, 2021 - 2034 (USD Million)

- 10.1 Key trends

- 10.2 North America

- 10.2.1 U.S.

- 10.2.2 Canada

- 10.3 Europe

- 10.3.1 UK

- 10.3.2 Germany

- 10.3.3 France

- 10.3.4 Italy

- 10.3.5 Spain

- 10.3.6 Russia

- 10.3.7 Nordics

- 10.4 Asia Pacific

- 10.4.1 China

- 10.4.2 India

- 10.4.3 Japan

- 10.4.4 South Korea

- 10.4.5 ANZ

- 10.4.6 Southeast Asia

- 10.5 Latin America

- 10.5.1 Brazil

- 10.5.2 Mexico

- 10.5.3 Argentina

- 10.6 MEA

- 10.6.1 UAE

- 10.6.2 Saudi Arabia

- 10.6.3 South Africa

Chapter 11 Company Profiles

- 11.1 Amazon Web Services

- 11.2 DHL Group

- 11.3 FedEx

- 11.4 Flexport

- 11.5 Four Kites

- 11.6 Google

- 11.7 IBM

- 11.8 Locus

- 11.9 Maersk

- 11.10 Microsoft

- 11.11 NVIDIA

- 11.12 Open AI

- 11.13 Optimal Dynamics

- 11.14 Oracle

- 11.15 Palantir Technologies

- 11.16 Project44

- 11.17 Salesforce

- 11.18 SAP

- 11.19 UPS

- 11.20 XPO Logistics