|

시장보고서

상품코드

1797681

당뇨병성 케톤산증 치료 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Diabetic Ketoacidosis Treatment Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

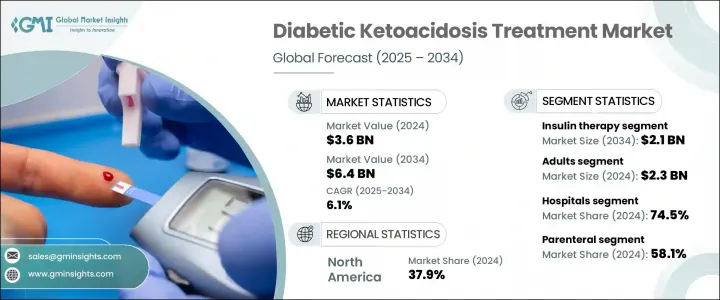

세계의 당뇨병성 케톤산증 치료 시장은 2024년에는 36억 달러로 평가되었고 CAGR 6.1%로 성장할 전망이며 2034년에는 64억 달러에 이를 것으로 추정됩니다.

이러한 성장 추세는 전 세계적으로 당뇨병, 특히 제1형 당뇨병 발병률이 증가하는 것과 기술적 발전이 반영된 인슐린 전달 솔루션 사용이 확대되는 데 크게 기인합니다. 자동화 인슐린 시스템과 연속 혈당 모니터링 도구의 혁신은 보다 정밀한 치료 제공과 환자 임상 결과 개선에 기여하고 있습니다. 수액 요법과 균형 잡힌 전해질 제형 역시 회복 가속화와 잠재적 합병증 최소화에 핵심적인 역할을 합니다.

공공 보건 자금 지원, 당뇨병 인식 제고를 위한 정책적 노력, 응급 치료 체계 강화가 수요를 상당하게 촉진하고 있습니다. 당뇨병성 케톤산증의 표준 치료 요법에는 신속 작용 인슐린 유사체, 정맥 수액, 전해질 보정이 포함되며, 모두 환자의 신속한 안정화를 목표로 합니다. 사노피, 메드트로닉, 화이자, 엘리 릴리, 노보 노디스크와 같은 업계 선도 기업들은 전 세계 입지가 확대되기를 위한 고급 제형 개발 및 협력 노력에 지속적으로 투자하고 있습니다. 인공지능 기반 인슐린 펌프와 실시간 모니터링 장비의 발전은 반응성을 높이고 회복 시간을 단축함으로써 치료 기준을 재정의하고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 36억 달러 |

| 예측 금액 | 64억 달러 |

| CAGR | 6.1% |

2024년 인슐린 치료 부문 규모는 12억 달러였으며, 2034년까지 21억 달러로 성장하여 연평균 성장률(CAGR) 5.6%를 기록할 것으로 예상됩니다. 혈당 조절과 케톤 축적 억제에 있어 인슐린의 핵심적 역할은 치료 미래에서의 지배적 위치를 뒷받침합니다. 속효성 인슐린 유사체는 신속한 작용 발현과 일관된 효능으로 인해 급성 치료 환경에서 널리 채택되고 있습니다. 이 분야의 주요 발전은 연속 혈당 모니터링과 자동 인슐린 투여 시스템을 연결하는 스마트 투여 시스템의 통합입니다. 이러한 지능형 시스템은 실시간으로 인슐린 투여를 최적화하여 저혈당 위험을 낮추고 환자 안전성을 향상시킵니다.

성인 인구 부문은 2024년 23억 달러를 창출했습니다. 성인은 제1형 당뇨병과 인슐린 의존성 제2형 당뇨병의 광범위한 발생으로 가장 큰 영향을 받는 연령층이다. 이 집단은 종종 추가적인 건강 합병증, 지연된 진단, 불규칙한 혈당 관리에 직면하여 당뇨병성 케톤산증에 더 취약하다. 이러한 복잡성은 고급 인슐린 치료 및 전해질의 면밀한 모니터링을 포함한 표적 치료 접근법을 요구한다. 맞춤형 중재에 대한 수요와 높은 치료량을 고려할 때 의약품들은 이 집단에 집중하고 있다.

미국의 당뇨병성 케톤산증 치료 시장은 높은 당뇨병 유병률과 정교한 의료 인프라의 결합으로 2024년 90.1%의 점유율을 차지했습니다. 이 나라는 조기 진단과 신속한 치료를 촉진하는 지원적 규제 환경, 집중적인 연구 개발(R&D) 계획, 공공 인식 캠페인의 혜택을 지속적으로 누리고 있습니다. 인공지능(AI) 및 전자의무기록(EHR) 플랫폼과 통합된 스마트 인슐린 장치의 도입이 많은 병원에서 표준화되면서 치료 프로토콜을 간소화하고 환자 회복 시간을 단축하는 데 기여하고 있습니다. 미국 내 전체 수요는 응급 상황과 장기 당뇨병 치료 모두에서 여전히 높은 수준을 유지하고 있습니다.

세계의 당뇨병성 케톤산증 치료 시장 주요 기업으로는 Sanofi, Merck & Co., Novo Nordisk, Eli Lilly and Company, Fresenius Kabi, Wockhardt, Baxter International, Pfizer 등이 있습니다. 기업들은 새롭게 대두되는 임상적 요구를 해결하기 위해 인공지능 촉진 인슐린 전달 시스템, 향후 아날로그, 복합 요법 개발을 최우선 과제로 삼고 있습니다. 병원, 연구 기관, 디지털 헬스 기업과의 전략적 제휴는 기술 통합과 치료 개인화를 가속화하는 데 기여합니다. 주요 기업들은 고부담 지역에서의 임상 시험 및 규제 승인을 통해 제품 포트폴리오 확대를 위한 막대한 투자를 진행 중입니다. 또한 전 세계 의약품 리더들은 선진 시장과 의료 취약 지역 모두에서 안정적인 접근성을 보장하기 위해 공급망을 최적화하고 유통망을 강화함으로써 경쟁적 입지를 공고히 하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 촉진요인

- 성장 촉진요인

- 제1형 및 제2형 당뇨병의 전 세계적 유병률 증가

- 인슐린 전달 및 혈당 모니터링 기술 발전

- 당뇨병성 케톤산증에 대한 인식 제고 및 조기 진단 증가

- 업계의 잠재적 위험 및 과제

- 당뇨병성 케톤산증 치료 및 인슐린 요법의 높은 비용

- 저소득 및 농촌 지역의 고급 치료 접근성 제한

- 시장 기회

- 당뇨병 부담 증가 중인 신흥 시장으로 확장

- 원격 관리를 위한 원격의료 및 디지털 헬스 도구 통합

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술적 진보

- 현재의 기술 동향

- 신흥기술

- 상환 시나리오

- 임상시험의 정세

- 장래 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측, 치료 유형별(2021-2034년)

- 주요 동향

- 체액 보충 요법

- 전해질 보충 요법

- 인슐린 요법

- 기타 치료법

제6장 시장 추계 및 예측, 연령별(2021-2034년)

- 주요 동향

- 소아

- 성인

제7장 시장 추계 및 예측, 투여 경로별(2021-2034년)

- 주요 동향

- 비경구

- 피하

- 경구

- 기타 투여 경로

제8장 시장 추계 및 예측, 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 외래수술센터(ASC)

- 재택 케어

제9장 시장 추계 및 예측, 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제10장 기업 프로파일

- Global Players

- Regional Players

- Emerging Players

The Global Diabetic Ketoacidosis Treatment Market was valued at USD 3.6 billion in 2024 and is estimated to grow at a CAGR of 6.1% to reach USD 6.4 billion by 2034. This growth trajectory is largely shaped by the increasing incidence of diabetes worldwide, especially type 1 diabetes, combined with the rising use of technologically advanced insulin delivery solutions. Breakthroughs in automated insulin systems and continuous glucose monitoring tools are helping deliver more precise treatment and improve clinical outcomes for patients. Fluid therapy and well-balanced electrolyte formulations also play a key role in accelerating recovery and minimizing potential complications.

Public health funding, policy initiatives to increase diabetes awareness, and the strengthening of emergency care frameworks in both mature and developing markets are significantly propelling demand. Standard treatment regimens for diabetic ketoacidosis include rapid-acting insulin analogs, intravenous hydration, and electrolyte correction, all aimed at quickly stabilizing patients. Industry leaders such as Sanofi, Medtronic, Pfizer, Eli Lilly, and Novo Nordisk continue to invest in advanced formulations and collaborative efforts that expand their global presence. Progress in AI-powered insulin pumps and real-time monitoring devices is redefining treatment standards by enhancing responsiveness and reducing time to recovery.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $3.6 Billion |

| Forecast Value | $6.4 Billion |

| CAGR | 6.1% |

In 2024, the insulin therapy segment was valued at USD 1.2 billion, and it is expected to grow to USD 2.1 billion by 2034, registering a CAGR of 5.6%. The pivotal role of insulin in controlling blood glucose and stopping ketone accumulation underpins its dominance in the therapeutic landscape. Fast-acting insulin analogs are widely adopted in acute care settings due to their swift onset and consistent efficacy. A major development in this area is the integration of smart dosing systems that link continuous glucose monitors with automated insulin delivery. These intelligent systems optimize insulin administration in real time, lowering the risk of hypoglycemia and improving patient safety.

The adult population segment generated USD 2.3 billion in 2024. Adults represent the most affected age group due to the widespread occurrence of both type 1 and insulin-dependent type 2 diabetes. This population often faces additional health complications, delayed diagnoses, and inconsistent glycemic management, making them more susceptible to diabetic ketoacidosis. Such complexities require targeted therapeutic approaches, including advanced insulin treatments and close monitoring of electrolytes. Pharmaceutical companies focus their efforts heavily on this group, given the demand for tailored interventions and the high treatment volumes it commands.

United States Diabetic Ketoacidosis Treatment Market held a 90.1% share in 2024, driven by a combination of high diabetes prevalence and sophisticated healthcare infrastructure. The country continues to benefit from supportive regulatory environments, intensive R&D initiatives, and public awareness campaigns that promote early diagnosis and prompt treatment. Adoption of smart insulin devices integrated with AI and EHR platforms is becoming standard in many hospitals, helping streamline care protocols and reduce patient recovery times. The overall demand in the U.S. remains high across both emergency settings and long-term diabetes care.

Leading companies in the Global Diabetic Ketoacidosis Treatment Market include Sanofi, Merck & Co., Novo Nordisk, Eli Lilly and Company, Fresenius Kabi, Wockhardt, Baxter International, and Pfizer. Companies are prioritizing the development of AI-driven insulin delivery systems, next-gen analogs, and combination therapies to address emerging clinical needs. Strategic alliances with hospitals, research institutions, and digital health companies help accelerate tech integration and treatment personalization. Major firms are investing heavily in expanding their product portfolios through clinical trials and regulatory approvals in high-burden regions. Further, global pharmaceutical leaders are optimizing supply chains and bolstering distribution networks to ensure consistent access across developed and underserved markets, strengthening their competitive foothold.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 3600 synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Treatment type

- 2.2.3 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Rising global prevalence of type 1 and type 2 diabetes

- 3.2.1.2 Advancements in insulin delivery and glucose monitoring technologies

- 3.2.1.3 Increased awareness and early diagnosis of diabetic ketoacidosis

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of diabetic ketoacidosis treatment and insulin therapies

- 3.2.2.2 Limited access to advanced care in low-income and rural regions

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into emerging markets with rising diabetes burden

- 3.2.3.2 Integration of telemedicine and digital health tools for remote management

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Reimbursement scenario

- 3.7 Clinical trials landscape

- 3.8 Future market trends

- 3.9 Gap analysis

- 3.10 Porter's analysis

- 3.11 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Treatment Type, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Fluid replacement therapy

- 5.3 Electrolyte replacement therapy

- 5.4 Insulin therapy

- 5.5 Other therapies

Chapter 6 Market Estimates and Forecast, By Age Group, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Pediatric

- 6.3 Adults

Chapter 7 Market Estimates and Forecast, By Route of Administration, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Parenteral

- 7.3 Subcutaneous

- 7.4 Oral

- 7.5 Other routes of administration

Chapter 8 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 Hospitals

- 8.3 Ambulatory surgical centers

- 8.4 Homecare settings

Chapter 9 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Spain

- 9.3.5 Italy

- 9.3.6 Netherlands

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.6 Middle East and Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

Chapter 10 Company Profiles

- 10.1 Global Players

- 10.1.1 Baxter International

- 10.1.2 Eli Lilly and Company

- 10.1.3 Fresenius Kabi

- 10.1.4 Merck & Co.

- 10.1.5 Novo Nordisk

- 10.1.6 Pfizer

- 10.1.7 Sanofi

- 10.1.8 Wockhardt

- 10.2 Regional Players

- 10.2.1 Biocon

- 10.2.2 Julphar

- 10.2.3 Otsuka Pharmaceutical

- 10.2.4 Tonghua Dongbao

- 10.2.5 Yuria-Pharm

- 10.3 Emerging Players

- 10.3.1 Adocia

- 10.3.2 Cipla

- 10.3.3 Gufic Biosciences

- 10.3.4 Hanmi Pharmaceuticals

- 10.3.5 Yiling Pharmaceutical