|

시장보고서

상품코드

1797792

단열 유리창 유닛 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Insulating Glass Units (IGUs) Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

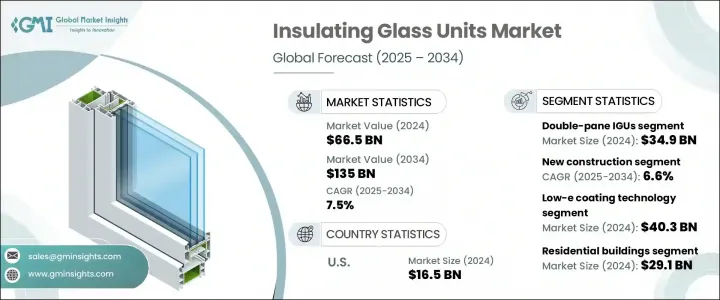

세계의 단열 유리창 유닛 시장 규모는 2024년에 665억 달러로 평가되었고, CAGR 7.5%를 나타내 2034년에는 1,350억 달러에 이를 것으로 추정됩니다.

세계 에너지 효율 규제 강화가 단열 유리창 유닛(IGU) 수요 증가에 큰 역할을 하고 있습니다. 각국 정부는 건물의 복층 성능 향상을 추진하고 있으며, 그 결과 선진 코팅을 한 단열 유리창의 설치가 증가하고 있습니다. 이러한 동향은 개정된 에너지 규범을 준수할 수 없는 주택 및 상업시설의 신축 프로젝트에서 특히 두드러집니다. 최신 건축 기준법은 U-팩터와 SHGC에 대한 규제를 엄격히 하고 있으며, Low-E 코팅과 가스 충전 IGU에 대한 투자를 건축업자에게 촉구하고 있습니다. 예산을 타협하지 않고 성능을 강조하는 경향이 강해지므로 비용에 최적화된 구성을 사용하는 것이 좋습니다.

지속가능성 벤치마크와 친환경 인증을 통해 IGU는 그린 빌딩의 컴플라이언스에 각광을 받고 있습니다. 에너지 성능에 중점을 둔 인증 제도에서는 크레딧 축적에 IGU를 이용하는 경우가 늘고 있습니다. 에너지 요금의 상승과 환경 문제에 대한 사회의 의식도 소비자를 보다 효율적인 솔루션으로 향하게 하고 있습니다. IGU는 복층성을 높여 냉난방 부하를 줄여 주택 소유자나 상업시설의 관리자에게 장기적인 절약으로 이어집니다. 친환경 아키텍처에서 IGU의 중요성이 높아짐에 따라 IGU는 에너지 효율적인 건축 전략의 핵심 요소입니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 665억 달러 |

| 예측 금액 | 1,350억 달러 |

| CAGR | 7.5% |

이중창 IGU 부문은 2024년에 349억 달러로 평가되었으며 2025-2034년에 걸쳐 CAGR 5.8%를 나타낼 것으로 예측됩니다. 이중창 IGU는 비용 효율성과 기준선 에너지 준수의 균형으로 널리 보급되고 있습니다. 특히 기후가 온화한 지역과 예산 제약이 있는 프로젝트에서 인기가 높습니다. 한편, 트리플 유리 IGU 수요는 특히 한랭지나 친환경 건물 인증을 추구하는 프로젝트에서 기세를 늘리고 있습니다. 이러한 고성능 IGU는 복층성과 방음성이 뛰어나 뛰어난 열성능을 요구하는 주택 및 상업 개발업체에게 매력적입니다. 열 기준의 요구가 엄격해짐에 따라, 보다 선진적 다층 구성으로의 이동이 진행되고 있습니다.

신축 부문의 2024년 시장 규모는 325억 달러로 평가되었고 2034년 CAGR은 6.6%를 나타낼 것으로 예상됩니다. 신축 건물은 최신 에너지 규제를 충족시키는 데 필요한 건축 설계의 일부로 처음부터 IGU를 통합했습니다. 개발자는 계획 단계 초기에 IGU를 통합하여 컴플라이언스를 확보하고 에너지 신뢰를 높이는 것을 선호합니다. 또한 IGU는 규모가 커질수록 비용 효과가 높아지므로 집주택, 사무실 건물, 교육기관 등 대규모 프로젝트에 적합합니다. 에너지 규제가 점점 엄격해지고 있는 가운데, 개발자는 IGU를 사양에 통합함으로써 소급 업그레이드를 피하고 건설 허가를 간소화하고 있습니다.

미국의 단열 유리창 유닛 시장은 2024년에 165억 달러를 창출했고 2034년까지 연평균 복합 성장률(CAGR) 7.2%를 나타낼 것으로 예측됩니다. 이 지역은 성숙한 건축 기준법, 진보적인 에너지 시책, 지속가능성을 위한 강력한 추진력의 혜택을 받고 있습니다. 국가적인 틀은 신축·개축을 불문하고 고성능 글레이징 시스템에 대한 수요를 견인하고 있습니다. 신규 개발에 더해, 지역 전체의 노후화된 빌딩은 소유자가 운용 비용의 삭감과 라이프 사이클 성능의 연장을 목표로 하는 가운데, IGU 리노베이션의 비옥한 시장이 되고 있습니다. 그린 건축이 건축물의 우선순위를 형성하고 있기 때문에 주택과 상업 인프라를 중심으로 섹터를 불문하고 수요가 높습니다.

세계의 단열 유리창 유닛 시장을 형성하고 있는 주요 기업으로는 NSG Group(Pilkington), Guardian Glass, Cardinal Glass Industries, AGC Inc. 등입니다. 이들 기업의 대부분은 수요 증가에 효율적으로 대응하기 위해 건설활동이 활발해지고 있는 지역에서 생산능력을 확대하고 있습니다. 주요 진입기업은 선진적 복층·방음 특성을 가진 차세대 IGU를 개발하기 위해 연구 개발에 투자하고 있으며, 많은 경우 스마트 유리 기술과 새로운 코팅 배합을 도입하고 있습니다. 부동산 개발자, 건축가, 에너지 컨설턴트와의 제휴는 계획 단계 초기에 향후 프로젝트에 대응하는 데 도움이 됩니다. 또한 각 회사는 지속 가능한 생산 기술과 인증을 우선시하고 친환경 건설 의무에 호소하고 있습니다. 이러한 전략은 IGU 기술의 새로운 용도 부문을 개척하는 한편, 대기업의 존재감을 확고하게 하는 데 도움이 됩니다.

목차

제1장 조사 방법

- 시장의 범위와 정의

- 조사 디자인

- 조사 접근

- 데이터 수집 방법

- 데이터 마이닝 소스

- 세계

- 지역/국가

- 기본 추정과 계산

- 기준연도 계산

- 시장 예측의 주요 동향

- 1차 조사와 검증

- 1차 정보

- 예측 모델

- 조사의 전제와 한계

제2장 주요 요약

제3장 산업 고찰

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 파괴적 혁신

- 산업에 미치는 영향요인

- 성장 촉진요인

- 산업의 잠재적 리스크 및 과제

- 시장 기회

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품별

- 향후 시장 동향

- 기술과 혁신의 상황

- 현재의 기술 동향

- 신흥기술

- 특허 상황

- 무역 통계(HS코드)(참고: 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경 측면

- 지속 가능한 실습

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 친환경 활동

- 탄소발자국의 고려

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확대 계획

제5장 시장 추정·예측, 유리 유형별(2021-2034년)

- 주요 동향

- 더블 패널 IGU

- 트리플 패널 IGU

- 일렉트로크로믹 IGU

- 스마트 다이나믹 유리 IGU

- 특수 유리 IGU

- 내화 IGU

제6장 시장 추정·예측 : 기술별(2021-2034년)

- 주요 동향

- 로이 코팅 기술

- 가스 충전 기술

- 아르곤 가스 충전 시스템

- 크립톤 및 크세논 충전

- 공기 충전 표준 시스템

- 스페이서 시스템 기술

- 알루미늄 스페이서 시스템

- 웜 엣지 스페이서 기술

- 고급 스페이서 시스템

- 실란트 및 접착제 기술

제7장 시장 추정·예측 : 용도별(2021-2034년)

- 주요 동향

- 주거용 건물

- 신축

- 단독 주택

- 집합 주택

- 맞춤형 및 고급 주택

- 리노베이션 및 개조

- 창문 교체

- 에너지 효율 향상

- 역사적 건축물 리노베이션

- 신축

- 상업용 건물

- 사무실 건물

- 고층 건축

- 본사

- 복합 개발

- 소매 및 접객

- 쇼핑센터

- 호텔 및 레스토랑

- 엔터테인먼트 시설

- 기관 건물

- 교육시설

- 의료시설

- 정부청사

- 사무실 건물

- 산업용 건물

- 제조 시설

- 창고 및 유통 센터

- 데이터센터 및 기술 시설

- 특수산업 건물

- 커튼월 시스템

- 점포의 정면 및 창문 벽

제8장 시장 추정·예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 신축

- 교환 및 개조

- 리노베이션 및 개조

- 친환경 건물 및 지속가능성 프로젝트

제9장 시장 추정·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 이탈리아

- 스페인

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제10장 기업 프로파일

- Saint-Gobain SA

- Guardian Glass

- NSG 그룹(Pilkington)

- AGC Inc.(Asahi Glass)

- Cardinal Glass Industries

- Viracon

- Xinyi Glass Holdings Limited

- Vitro Architectural Glass

- PPG Industries

- Glas Trosch Holding AG

- ClearVue Technologies Limited

- Thermoseal Group

- Quanex Building Products(Edgetech)

- SAGE Electrochromics(SageGlass)

- View Inc.

- Gentex Corporation

- Pleotint LLC

- National Glass(Australia)

- ToughGlaze

- Glassfab USA

- V-Glass

- Glaston Corporation

The Global Insulating Glass Units Market was valued at USD 66.5 billion in 2024 and is estimated to grow at a CAGR of 7.5% to reach USD 135 billion by 2034. Stricter global energy efficiency mandates are playing a major role in boosting the demand for IGUs. Governments are pushing for better thermal performance in buildings, leading to greater installation of multi-pane units with advanced coatings. These trends are especially notable in new residential and commercial construction projects, where compliance with revised energy codes is non-negotiable. The newest building codes are placing tighter restrictions on U-factor and solar heat gain coefficient (SHGC), encouraging builders to invest in Low-E coatings and gas-filled IGUs. This growing emphasis on performance without compromising on budget is encouraging the use of cost-optimized configurations.

Sustainability benchmarks and eco-certifications are pushing IGUs into the spotlight for green building compliance. Certification systems that focus on energy performance increasingly rely on IGUs for credit accumulation. Rising energy bills and public awareness of environmental issues are also pushing consumers toward more efficient solutions. IGUs help to reduce heating and cooling loads by improving insulation, translating into tangible long-term savings for homeowners and commercial property managers. With their growing relevance in environmentally conscious architecture, IGUs have become a core element of energy-efficient construction strategies.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $66.5 Billion |

| Forecast Value | $135 Billion |

| CAGR | 7.5% |

The double-pane IGUs segment was valued at USD 34.9 billion in 2024 and is projected to grow at a CAGR of 5.8% from 2025 to 2034. These units maintain broad appeal due to their balance between cost-efficiency and baseline energy compliance. Their popularity is especially strong in moderate climates and projects operating within budget constraints. On the other hand, demand for triple-pane IGUs is gaining momentum, particularly in colder regions and projects pursuing green building certifications. These high-performance variants offer better insulation and soundproofing, appealing to both residential and commercial developers aiming for superior thermal performance. As thermal standards become more demanding, there is an increasing shift toward more advanced multi-layer configurations.

The new construction segment was valued at USD 32.5 billion in 2024 and is expected to grow at a CAGR of 6.6% through 2034. New builds integrate IGUs from the outset as part of architectural designs that are required to meet updated energy regulations. Developers prefer to incorporate IGUs early in the planning stages to ensure compliance and boost energy credentials. These units are also cost-effective at scale, making them well-suited for larger projects such as residential complexes, office buildings, and educational institutions. With energy codes becoming increasingly strict, developers are embedding IGUs into specifications to avoid retroactive upgrades and to streamline construction approvals.

United States Insulating Glass Units (IGUs) Market generated USD 16.5 billion in 2024 and is projected to grow at a 7.2% CAGR through 2034. The region benefits from mature building codes, progressive energy policies, and a strong push for sustainability. National frameworks are driving demand for high-performance glazing systems in both new and renovated structures. In addition to new developments, aging buildings across the region are becoming a fertile market for IGU retrofits as owners look to reduce operational costs and extend lifecycle performance. Demand is high across sectors-particularly in residential housing and commercial infrastructure-as green construction continues to shape building priorities.

Major companies shaping the Global Insulating Glass Units (IGUs) Market include NSG Group (Pilkington), Guardian Glass, Cardinal Glass Industries, AGC Inc. (Asahi Glass), and Saint-Gobain S.A. These players dominate the industry through a combination of innovation, volume capacity, and global reach. Many of them are expanding production capabilities in regions with increasing construction activity to meet rising demand more efficiently. Key players are investing in R&D to develop next-generation IGUs with advanced thermal and acoustic properties, often incorporating smart-glass technology and new coating formulations. Partnerships with real estate developers, architects, and energy consultants are helping them align with upcoming projects early in the planning phase. In addition, companies are prioritizing sustainable production techniques and certifications to appeal to environmentally driven construction mandates. These strategies help major firms solidify their presence while opening new application areas for IGU technology.

Table of Contents

Chapter 1 Methodology

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional

- 2.2.2 Glass type

- 2.2.3 Technology

- 2.2.4 Application

- 2.2.5 End use

- 2.3 TAM Analysis, 2021-2034

- 2.4 CXO perspectives: Strategic imperatives

- 2.4.1 Executive decision points

- 2.4.2 Critical success factors

- 2.5 Future Outlook and Strategic Recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.2 Industry pitfalls and challenges

- 3.2.3 Market opportunities

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East & Africa

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.6.1 Technology and Innovation landscape

- 3.6.2 Current technological trends

- 3.6.3 Emerging technologies

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.9.1 Current technological trends

- 3.9.2 Emerging technologies

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and Environmental Aspects

- 3.12.1 Sustainable Practices

- 3.12.2 Waste Reduction Strategies

- 3.12.3 Energy Efficiency in Production

- 3.12.4 Eco-friendly Initiatives

- 3.13 Carbon Footprint Considerations

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 LATAM

- 4.2.1.5 MEA

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New Product Launches

- 4.6.4 Expansion Plans

Chapter 5 Market Estimates & Forecast, Glass Type, 2021-2034 (USD Billion) (Kilo Tons)

- 5.1 Key trends

- 5.2 Double-Pane IGUs

- 5.3 Triple-Pane IGUs

- 5.4 Electrochromic IGUs

- 5.5 Smart And Dynamic Glass IGUs

- 5.6 Specialty Glass IGUs

- 5.7 Fire-Rated IGUs

Chapter 6 Market Estimates & Forecast, By Technology, 2021-2034 (USD Billion) (Kilo Tons)

- 6.1 Key trends

- 6.2 Low-e coating technology

- 6.3 Gas fill technologies

- 6.3.1 Argon gas fill systems

- 6.3.2 Krypton and xenon fill

- 6.3.3 Air fill standard systems

- 6.4 Spacer system technologies

- 6.4.1 Aluminum spacer systems

- 6.4.2 Warm edge spacer technologies

- 6.4.3 Advanced spacer systems

- 6.5 Sealant and adhesive technologies

Chapter 7 Market Estimates & Forecast, By Application, 2021-2034 (USD Billion) (Kilo Tons)

- 7.1 Key trends

- 7.2 Residential buildings

- 7.2.1 New construction

- 7.2.1.1 Single-family homes

- 7.2.1.2 Multi-family housing

- 7.2.1.3 Custom and luxury homes

- 7.2.2 Renovation and retrofit

- 7.2.2.1 Window replacement

- 7.2.2.2 Energy efficiency upgrades

- 7.2.2.3 Historic building renovations

- 7.2.1 New construction

- 7.3 Commercial buildings

- 7.3.1 Office buildings

- 7.3.1.1 High-rise construction

- 7.3.1.2 Corporate headquarters

- 7.3.1.3 Mixed-use developments

- 7.3.2 Retail and hospitality

- 7.3.2.1 Shopping centers

- 7.3.2.2 Hotels and restaurants

- 7.3.2.3 Entertainment facilities

- 7.3.3 Institutional buildings

- 7.3.3.1 Educational facilities

- 7.3.3.2 Healthcare buildings

- 7.3.3.3 Government buildings

- 7.3.1 Office buildings

- 7.4 Industrial applications

- 7.4.1 Manufacturing facilities

- 7.4.2 Warehouses and distribution centers

- 7.4.3 Data centers and technical facilities

- 7.4.4 Specialized industrial buildings

- 7.5 Curtain wall systems

- 7.6 Storefront and window wall applications

Chapter 8 Market Estimates & Forecast, By End Use, 2021-2034 (USD Billion) (Kilo Tons)

- 8.1 Key trends

- 8.2 New construction

- 8.3 Replacement and retrofit

- 8.4 Renovation and remodeling

- 8.5 Green building and sustainability projects

Chapter 9 Market Estimates & Forecast, By Region, 2021-2034 (USD Billion) (Kilo Tons)

- 9.1 Key trends

- 9.2 North America

- 9.2.1 U.S.

- 9.2.2 Canada

- 9.3 Europe

- 9.3.1 Germany

- 9.3.2 UK

- 9.3.3 France

- 9.3.4 Italy

- 9.3.5 Spain

- 9.3.6 Rest of Europe

- 9.4 Asia Pacific

- 9.4.1 China

- 9.4.2 India

- 9.4.3 Japan

- 9.4.4 Australia

- 9.4.5 South Korea

- 9.4.6 Rest of Asia Pacific

- 9.5 Latin America

- 9.5.1 Brazil

- 9.5.2 Mexico

- 9.5.3 Argentina

- 9.5.4 Rest of Latin America

- 9.6 Middle East & Africa

- 9.6.1 Saudi Arabia

- 9.6.2 South Africa

- 9.6.3 UAE

- 9.6.4 Rest of Middle East & Africa

Chapter 10 Company Profiles

- 10.1 Saint-Gobain S.A.

- 10.2 Guardian Glass

- 10.3 NSG Group (Pilkington)

- 10.4 AGC Inc. (Asahi Glass)

- 10.5 Cardinal Glass Industries

- 10.6 Viracon

- 10.7 Xinyi Glass Holdings Limited

- 10.8 Vitro Architectural Glass

- 10.9 PPG Industries

- 10.10 Glas Trosch Holding AG

- 10.11 ClearVue Technologies Limited

- 10.12 Thermoseal Group

- 10.13 Quanex Building Products (Edgetech)

- 10.14 SAGE Electrochromics (SageGlass)

- 10.15 View Inc.

- 10.16 Gentex Corporation

- 10.17 Pleotint LLC

- 10.18 National Glass (Australia)

- 10.19 ToughGlaze

- 10.20 Glassfab USA

- 10.21 V-Glass

- 10.22 Glaston Corporation