|

시장보고서

상품코드

1797805

탄소 격리용 광물 토양 개량제 시장 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Mineral Soil Amendments for Carbon Sequestration Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

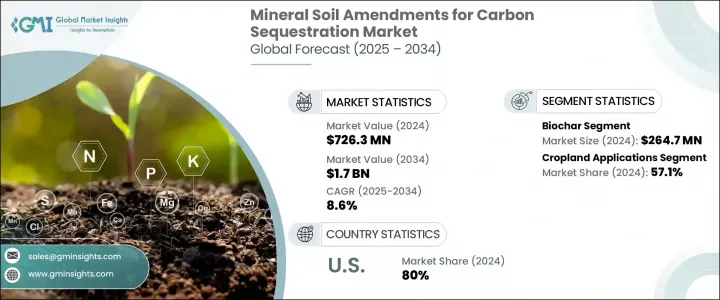

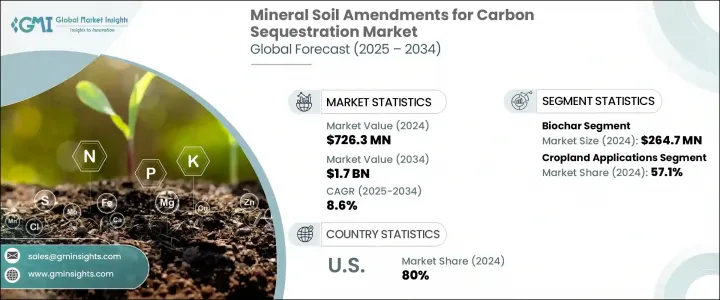

세계의 탄소 격리용 광물 토양 개량제 시장은 2024년에 7억 2,630만 달러로 평가되었으며, CAGR 8.6%를 나타내 2034년에는 17억 달러에 이를 것으로 추정됩니다.

기후 변화 완화에 대한 관심 증가는 자연 기반 솔루션에 대한 수요를 크게 추진하고 있으며, 광물성 토양 개량재는 이 변화의 강력한 도구로 부상하고 있습니다. 이러한 재료는 바이오차에서 강화 풍화 광물과 석회에 이르기까지 다양한 토양에 탄소를 고정시킬 뿐만 아니라 토양 구조와 비옥도도 개선합니다. 세계 각국의 정부는 정책적인센티브, 조사 지원, 탄소 신용 제도를 제공함으로써 이러한 움직임을 뒷받침하고 있습니다. 이와 병행하여 산업계와 농업업계도 지속가능성 목표에 따라 토지 생산성을 향상시키기 위해 이러한 관행을 채택하고 있습니다. 재생가능한 농업과 배출감소에 대한 관심이 높아짐에 따라 광물개량은 다양한 토지에서 지지를 모으고 있습니다. 토지의 열화에 대한 우려 증가와 장기적인 환경 회복력의 필요성은 이 시장을 계속 발전시키고 있습니다.

환경 및 경제면에서의 이점에 대한 인식이 높아짐에 따라 광물성 토양 개량재는 기후 변화 대책으로 뿐만 아니라 농업 시스템의 생산성 향상제로도 간주되고 있습니다. 농부와 토지 소유자들은 이러한 토양 개선이 탄소 격리를 훨씬 뛰어넘는 장기적인 가치를 가져온다는 것을 인식하기 시작했습니다. 바이오차, 현무암, 석회, 강란석 등의 광물 투입은 토양 구조를 개선하고, 양분 보유력을 높이고, 유익한 미생물의 활동을 촉진함으로써, 작물의 수율 증가와 토양의 회복력에 직접 공헌합니다. 그 결과, 물 효율이 향상되고, 화학 비료에 대한 의존도가 감소하고, 침식이나 이상 기상에 대한 내성이 높아집니다. 그 결과 토양관리계획에의 통합은 지속가능한 농업을 위한 전략적 움직임이 되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 7억 2,630만 달러 |

| 예측 금액 | 17억 달러 |

| CAGR | 8.6% |

바이오차 분야는 2024년까지 2억 6,470만 달러를 창출했으며, 2034년까지 연평균 복합 성장률(CAGR)은 8.7%를 나타낼 것으로 전망됩니다. 바이오차는 탄소 격리와 토양 품질 향상 모두에서 신뢰할 수 있기 때문에 이 시장의 주요 공헌자입니다. 열분해에 의해 만들어진이 다공성 재료는 보수성을 향상시키고 미생물의 생명을 증가시키고 토양 생태계에서 영양 순환을 지원합니다. 이동식 열분해 장치 및 원료 최적화 기술과 같은 기술 혁신으로 인해 바이오차 생산이 더욱 쉽고 저렴해지고 있습니다. 따라서 대규모 농장과 지속가능성을 중시하는 기업의 채용이 확대되고 있습니다. 그러나 원료 투입의 품질이 일정하지 않거나 표준화된 인증 프레임워크가 없는 등의 과제는 보다 광범위한 시장의 신뢰성과 신용을 확보하기 위해 아직 대처해야 합니다.

2024년 기준 작물 재배 분야의 점유율은 57.1%를 기록했고, 2025년부터 2034년에 걸쳐 CAGR 8.5%를 나타낼 것으로 예측되고 있습니다. 경작지는 여전히 광물성 토양 개량재의 주요 용도 분야이며, 생산성과 탄소 격리를 높이기 위해 석회, 현무암, 바이오차과 같은 재료의 사용이 증가하고 있습니다. 농부들은 보습, 양분 안정화 및 수율 증가를 위해 이러한 투입 자재를 활용합니다. 이러한 토양 처리는 단순히 토지의 성능을 향상시킬 뿐만 아니라 탄소를 지하에 저장함으로써 배출량을 상쇄하는 데에도 도움이 됩니다. 지속가능한 농업에 대한 요구가 높아지는 가운데, 농지에의 적용은 재생가능하고 탄소를 의식한 농업시스템으로의 전환에 필수적입니다.

2024년 북미의 탄소 격리용 광물 토양 개량제 시장 규모는 2억 2,090만 달러를 기록했습니다. 미국은 80%의 점유율로 압도적인 지위를 유지해 1억 4,920만 달러에 달했습니다. 미국은 선진적인 농법과 지속가능한 농업에 대한 대처에 대한 엄청난 재정 지원으로 최고 러너로 부상했습니다. 연구기관, 비공개회사, 정부기관이 협력하여 탄소를 포착하고 토양의 활력을 향상시키는 토양 개량재의 사용을 강화하고 있습니다. 이 접근법은 이행을 지원하는 정책, 보조금 및 주 수준의 프로그램의 틀에 힘입어 미국을 이 지역 전체의 혁신과 채용을 추진하는 중요한 힘으로 삼고 있습니다.

세계의 탄소 격리용 광물 토양 개량제 시장에서 사업을 전개하는 주요 기업으로는 Indigo Agriculture, Mati Carbon, Lithos Carbon, Biochar Supreme, Nori, Pacific Biochar, Regen Network, Cool Planet, Soil Capital, UNDO Carbon Ltd., InPlanet, Dagan, Carbonfuture, Silica 등이 있습니다. 이러한 기업들은 기후 변화에 대응하는 토양 솔루션의 확대와 제품 가용성 향상에 중요한 역할을 하고 있습니다. 많은 기업들이 R&D에 투자하고 다양한 토양 유형과 기후에 맞는 고성능 광물 혼합물과 바이오차 제품을 개발하고 있습니다. 농업 협동 조합과 탄소 오프셋 플랫폼과의 전략적 파트너십은 견고한 공급망을 구축하고 새로운 고객층에 액세스하는 데 도움이 됩니다. 물류 비용을 줄이고 보급률을 높이기 위해 이동식 가공 유닛과 지역 밀착형 생산 허브 구축에 주력하고 있는 기업도 있습니다. 또한 시장 신뢰를 높이고 자사 제품을 탄소 크레딧 제도에 통합하기 위해 인증 및 검증 프레임 워크를 구축하는 기업도 있습니다. 이러한 다면적인 접근법을 통해 각 회사는 경쟁력을 유지하고 빠르게 진화하는 시장에서 도달범위를 확대할 수 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 공급자의 상황

- 이익률

- 각 단계에서의 부가가치

- 밸류체인에 영향을 주는 요인

- 파괴적 혁신

- 영향요인

- 성장 촉진요인

- 기후정책과 인터넷 제로에 대한 헌신

- 탄소 신용 시장 개척과 가격 설정

- 농업의 지속가능성과 토양의 건전성에 관한 대처

- 기술 진보와 비용 절감

- 업계의 잠재적 위험 및 과제

- 높은 도입 비용과 경제적 장벽

- 측정, 보고, 검증의 복잡성

- 시장 기회

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- Porter's Five Forces 분석

- PESTEL 분석

- 가격 동향

- 지역별

- 제품별

- 향후 시장 동향

- 기술과 혁신의 상황

- 특허 상황

- 무역 통계(HS코드)(참고: 무역 통계는 주요 국가에서만 제공됨)

- 주요 수입국

- 주요 수출국

- 지속가능성과 환경 측면

- 지속가능한 관행

- 폐기물 감축 전략

- 생산에 있어서의 에너지 효율

- 환경 친화적인 노력

제4장 경쟁 구도

- 서론

- 기업의 시장 점유율 분석

- 지역별

- 북미

- 유럽

- 아시아태평양

- 라틴아메리카

- 중동 및 아프리카

- 지역별

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계·예측 : 개량제 유형별(2021-2034년)

- 주요 동향

- 바이오차

- 강화된 풍화 재료

- 현무암 및 감람석

- 기타 규산염 광물(예: 규회석, 사문석)

- 석회 및 석회암 용도

- 제올라이트 및 점토 광물

- 유기광물 하이브리드 개량제

- 새로운 개량 기술

- 나노 강화 광물 개량제

- 기능화 탄소 소재

- 미생물 및 광물 병용

제6장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 경작지 응용

- 연간 작물 시스템

- 다년생 작물 시스템

- 토양 건강 및 생산성 향상

- 초원 및 목초지 관리

- 가축 방목 시스템

- 사료 생산 향상

- 초원의 탄소 격리

- 임업 및 농림업

- 삼림토양관리

- 농림업 시스템

- 나무 농장 관리

- 토지 복원 및 재활

- 황폐화된 토지 복구

- 광산 부지 재활

- 습지 및 강변 복원

제7장 시장 추계·예측 : 용도별(2021-2034년)

- 주요 동향

- 상업 농업

- 대규모 농업 운영

- 정밀농업 통합

- 지속 가능한 농업 인증

- 소규모 및 가족 농업

- 소규모 생산자 용도

- 확장 서비스 통합

- 재정적 포용 및 지원

- 탄소 농업 및 상쇄 프로젝트

- 전용 탄소 격리 프로젝트

- 자발적인 탄소 시장 통합

- 컴플라이언스 탄소 시장 용도

- 연구개발

- 학술 및 연구 기관

- 민간 부문의 연구 개발

- 시범 및 실증 프로젝트

- 정부 및 공공 부문

- 국가 기후 프로그램

- 농업 정책 시행

- 토지관리기관

제8장 시장 추계·예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 기타 아시아태평양

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 기타 라틴아메리카

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

- 기타 중동 및 아프리카

제9장 기업 프로파일

- UNDO Carbon Ltd.

- InPlanet

- Silicate

- Lithos Carbon

- Mati Carbon

- Carbonfuture

- Pacific Biochar

- Biochar Supreme

- Carbofex

- Cool Planet

- Nori

- Indigo Agriculture

- Regen Network

- Soil Capital

- Dagan

The Global Mineral Soil Amendments for Carbon Sequestration Market was valued at USD 726.3 million in 2024 and is estimated to grow at a CAGR of 8.6% to reach USD 1.7 billion by 2034. Growing attention toward climate change mitigation is significantly driving demand for nature-based solutions, with mineral soil amendments emerging as a powerful tool in this transformation. These materials-ranging from biochar to enhanced weathering minerals and lime-not only help lock carbon in the soil but also improve soil structure and fertility. Governments across the globe are backing this movement by offering policy incentives, research support, and carbon credit mechanisms. In parallel, industries and farming communities are adopting these practices to align with sustainability goals and improve land productivity. With heightened interest in regenerative agriculture and emissions reduction, mineral amendments are gaining traction across varied landscapes. Rising concerns about land degradation and the need for long-term environmental resilience continue to push this market forward.

As awareness of the environmental and economic benefits grows, mineral soil amendments are increasingly seen not just as a climate solution but also as a productivity enhancer for agricultural systems. Farmers and landowners are beginning to recognize that these amendments provide long-term value far beyond carbon sequestration. By improving soil structure, enhancing nutrient retention, and promoting beneficial microbial activity, mineral inputs such as biochar, basalt, lime, and olivine contribute directly to increased crop yields and soil resilience. This leads to better water efficiency, reduced reliance on chemical fertilizers, and greater resistance to erosion and extreme weather conditions. As a result, their integration into soil management plans is becoming a strategic move for sustainable agriculture.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $726.3 Million |

| Forecast Value | $1.7 Billion |

| CAGR | 8.6% |

The biochar segment generated USD 264.7 million by 2024, with a consistent CAGR of 8.7% throughout 2034. Biochar is a leading contributor within this market, thanks to its reliability in both carbon sequestration and enhancing soil quality. Created through pyrolysis, this porous material improves water retention, increases microbial life, and supports nutrient cycling in soil ecosystems. Innovations in technology, such as more mobile pyrolysis units and feedstock optimization techniques, are making biochar easier and more affordable to produce. This is expanding its adoption among large-scale farms and sustainability-driven enterprises. However, challenges such as inconsistent quality of feedstock inputs and the lack of standardized certification frameworks still need to be addressed to ensure broader market reliability and trust.

In 2024, the cropland applications segment held 57.1% share and is expected to grow at a CAGR of 8.5% from 2025 through 2034. Cropland remains the dominant application area for mineral soil amendments, with increased use of materials like lime, basalt, and biochar to boost productivity and carbon sequestration. Farmers are turning to these inputs to retain moisture, stabilize nutrients, and boost yields, all while meeting climate goals. These soil treatments are not just improving the land's performance-they're also helping to offset emissions by storing carbon underground. As demand for sustainable agriculture increases, cropland applications are proving critical in the shift toward regenerative and carbon-conscious farming systems.

North America Mineral Soil Amendments for Carbon Sequestration Market generated USD 220.9 million in 2024. United States maintained its dominant position with an 80% share, translating to USD 149.2 million. The U.S. has emerged as a frontrunner due to its progressive farming practices and significant financial support for sustainable agriculture initiatives. Research institutions, private companies, and government agencies are collaborating to enhance the use of soil amendments that trap carbon and improve soil vitality. This approach is backed by a framework of policies, subsidies, and state-level programs that support implementation, making the U.S. a key force in driving innovation and adoption across the region.

Leading entities operating in the Global Mineral Soil Amendments for Carbon Sequestration Market include Indigo Agriculture, Mati Carbon, Lithos Carbon, Biochar Supreme, Nori, Pacific Biochar, Regen Network, Cool Planet, Soil Capital, UNDO Carbon Ltd., InPlanet, Dagan, Carbonfuture, Silicate, and Carbofex. These companies play a crucial role in scaling up climate-smart soil solutions and advancing product availability. Many are investing in R&D to develop high-performance mineral blends and biochar products tailored for various soil types and climates. Strategic partnerships with agricultural cooperatives and carbon offset platforms are helping to build robust supply chains and access new customer segments. Some firms are focusing on building mobile processing units and localized production hubs to reduce logistics costs and increase adoption rates. Additionally, several players are working toward certification and verification frameworks to enhance market trust and integrate their products into carbon credit systems. This multifaceted approach enables them to remain competitive and expand their reach in a rapidly evolving market.

Table of Contents

Chapter 1 Methodology & Scope

- 1.1 Market scope & definitions

- 1.2 Base estimates & calculations

- 1.3 Forecast calculations

- 1.4 Data sources

- 1.4.1 Primary

- 1.4.2 Secondary

- 1.4.2.1 Paid sources

- 1.4.2.2 Public sources

Chapter 2 Executive Summary

- 2.1 Industry synopsis, 2021-2034

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.1.1 Supplier Landscape

- 3.1.2 Profit Margin

- 3.1.3 Value addition at each stage

- 3.1.4 Factor affecting the value chain

- 3.1.5 Disruptions

- 3.2 Impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Climate policy and net-zero commitments

- 3.2.1.2 Carbon credit market development and pricing

- 3.2.1.3 Agricultural sustainability and soil health initiatives

- 3.2.1.4 Technology advancement and cost reduction

- 3.2.2 Industry pitfalls & challenges

- 3.2.2.1 High implementation costs and economic barriers

- 3.2.2.2 Measurement, reporting, and verification complexity

- 3.2.3 Market opportunities

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.5 Porter's analysis

- 3.6 PESTEL analysis

- 3.7 Price trends

- 3.7.1 By region

- 3.7.2 By product

- 3.8 Future market trends

- 3.9 Technology and Innovation landscape

- 3.10 Patent Landscape

- 3.11 Trade statistics (HS code) (Note: the trade statistics will be provided for key countries only)

- 3.11.1 Major importing countries

- 3.11.2 Major exporting countries

- 3.12 Sustainability and environmental aspects

- 3.12.1 Sustainable practices

- 3.12.2 Waste reduction strategies

- 3.12.3 Energy efficiency in production

- 3.12.4 Eco-friendly initiatives

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 By region

- 4.2.1.1 North America

- 4.2.1.2 Europe

- 4.2.1.3 Asia Pacific

- 4.2.1.4 Latin America

- 4.2.1.5 Middle East Africa

- 4.2.1 By region

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers & acquisitions

- 4.6.2 Partnerships & collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates & Forecast, By Amendment Type, 2021-2034 (USD Million) (Kilo Tons)

- 5.1 Key trends

- 5.2 Biochar

- 5.3 Enhanced weathering materials

- 5.3.1 Basalt and olivine

- 5.3.2 Other silicate minerals (e.g., wollastonite, serpentine)

- 5.4 Lime and limestone applications

- 5.5 Zeolites and clay minerals

- 5.6 Organic-mineral hybrid amendments

- 5.7 Emerging amendment technologies

- 5.8 Nano-enhanced mineral amendments

- 5.9 Functionalized carbon materials

- 5.10 Microbial-mineral combinations

Chapter 6 Market Estimates & Forecast, By Application, 2021-2034 (USD Million) (Kilo Tons)

- 6.1 Key trends

- 6.2 Cropland applications

- 6.2.1 Annual crop systems

- 6.2.2 Perennial crop systems

- 6.2.3 Soil health and productivity enhancement

- 6.3 Grassland and pasture management

- 6.3.1 Livestock grazing systems

- 6.3.2 Forage production enhancement

- 6.3.3 Carbon sequestration in grasslands

- 6.4 Forestry and agroforestry

- 6.4.1 Forest soil management

- 6.4.2 Agroforestry systems

- 6.4.3 Tree plantation management

- 6.5 Land restoration and rehabilitation

- 6.5.1 Degraded land recovery

- 6.5.2 Mine site rehabilitation

- 6.5.3 Wetland and riparian restoration

Chapter 7 Market Estimates & Forecast, By End Use Sector, 2021-2034 (USD Million) (Kilo Tons)

- 7.1 Key trends

- 7.2 Commercial agriculture

- 7.2.1 Large-scale farming operations

- 7.2.2 Precision agriculture integration

- 7.2.3 Sustainable agriculture certification

- 7.3 Smallholder and family farming

- 7.3.1 Small-scale producer applications

- 7.3.2 Extension service integration

- 7.3.3 Financial inclusion and support

- 7.4 Carbon farming and offset projects

- 7.4.1 Dedicated carbon sequestration projects

- 7.4.2 Voluntary carbon market integration

- 7.4.3 Compliance carbon market applications

- 7.5 Research and development

- 7.5.1 Academic research institutions

- 7.5.2 Private sector R&D

- 7.5.3 Pilot and demonstration projects

- 7.6 Government and public sector

- 7.6.1 National climate programs

- 7.6.2 Agricultural policy implementation

- 7.6.3 Land management agencies

Chapter 8 Market Estimates & Forecast, By Region, 2021-2034 (USD Million) (Kilo Tons)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Rest of Europe

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.4.6 Rest of Asia Pacific

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.5.4 Rest of Latin America

- 8.6 MEA

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

- 8.6.4 Rest of Middle East and Africa

Chapter 9 Company Profiles

- 9.1 UNDO Carbon Ltd.

- 9.2 InPlanet

- 9.3 Silicate

- 9.4 Lithos Carbon

- 9.5 Mati Carbon

- 9.6 Carbonfuture

- 9.7 Pacific Biochar

- 9.8 Biochar Supreme

- 9.9 Carbofex

- 9.10 Cool Planet

- 9.11 Nori

- 9.12 Indigo Agriculture

- 9.13 Regen Network

- 9.14 Soil Capital

- 9.15 Dagan