|

시장보고서

상품코드

1801819

POC(Point Of Care) CT 이미징 시스템 시장 : 기회, 성장 촉진요인, 산업 동향 분석 및 예측(2025-2034년)Point-of-care CT Imaging Systems Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

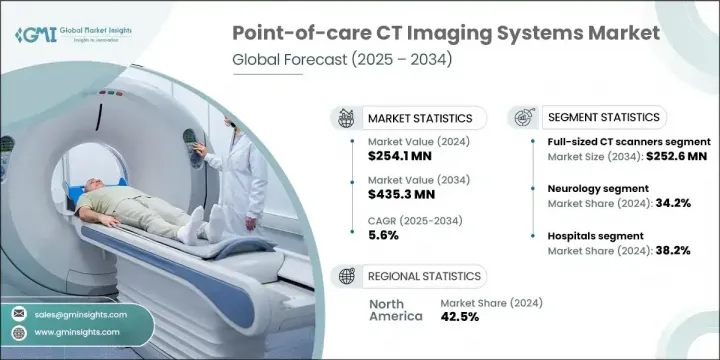

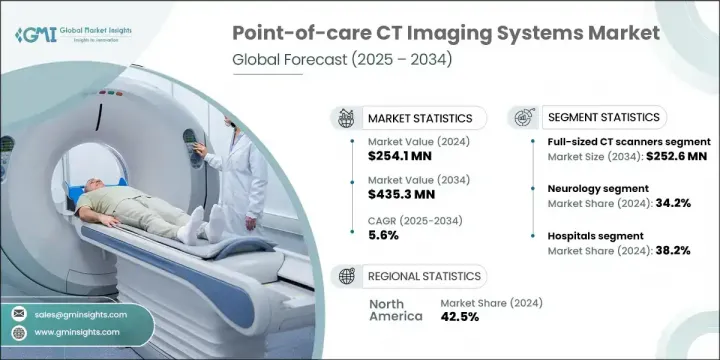

세계의 POC(Point Of Care) CT 이미징 시스템 시장은 2024년에는 2억 5,410만 달러에 달하고, CAGR 5.6%로 성장할 전망이며 2034년까지는 4억 3,530만 달러에 이를 것으로 예측됩니다.

이 시장의 성장은 주로 만성 질환 발생률 증가와 급속한 글로벌 인구 고령화에 힘입고 있습니다. 이러한 요인들은 즉각적이고 편리한 진단 솔루션에 대한 수요 증가를 촉진하고 있습니다. 현장 진단 CT 이미징 시스템은 신속하고 접근성 높은 영상 촬영을 제공하는 소형 이동식 플랫폼으로, 응급 치료, 외래 진료 센터 및 중환자 치료 환경에서 필수적입니다. 의료 모델이 환자 중심 진단으로 전환됨에 따라, 휴대용 CT 기술은 중앙 집중식 병원 시스템에 의존하지 않고 호흡기 평가를 지원하며 실시간 영상 촬영을 제공할 수 있는 능력으로 주목받고 있습니다.

호흡기 질환 사례 증가 역시 시장 성장을 가속화하고 있습니다. 조기 및 정확한 진단이 치료 결과 관리에 여전히 핵심적이기 때문입니다. 이러한 추세의 주요 원인 중 하나는 계절성 바이러스 감염 급증으로, 이는 호흡기 의료 시스템에 상당한 부담을 가중시킵니다. 결과적으로 즉각적인 치료 결정에 필요한 신속한 평가가 요구되는 다양한 임상 환경에서 POC CT 시스템의 채택이 확대되고 있습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작 금액 | 2억 5,410만 달러 |

| 예측 금액 | 4억 3,530만 달러 |

| CAGR | 5.6% |

2024년 풀사이즈 CT 스캐너 부문은 1억 4,930만 달러의 매출을 기록했습니다. 이 부문은 2034년까지 2억 5,260만 달러로 성장할 것으로 예상되며, 연평균 성장률(CAGR) 5.5%를 보일 전망입니다. 이러한 시스템은 고해상도 출력과 포괄적인 진단 능력으로 선호되며, 중환자 및 응급 치료에 최적의 선택지입니다. 풀사이즈 모델은 수술실, 외상 치료실, 중환자실에서 주로 사용되며, 영상의 속도와 세부 묘사가 환자 치료 결과에 결정적 역할을 합니다. 다양한 임상 요구를 지원할 수 있는 능력 덕분에 병원 업무 흐름에서 필수 불가결한 장비입니다.

2024년 기준 병원 부문은 38.2%의 점유율을 기록하며 이 부문 최대 최종 사용자 그룹으로 자리매김했습니다. 병원의 우위는 확립된 진단 인프라와 숙련된 방사선 전문 인력의 가용성에 기인합니다. 이러한 기관들은 신경학, 외상, 폐 질환 치료 분야의 복잡한 사례를 일상적으로 처리하며, 모두 신속한 POC CT 이미징 시스템의 혜택을 받습니다. 병원이 진단 속도와 서비스 제공을 지속적으로 개선함에 따라 이동형 CT 시스템에 대한 수요는 더욱 강해지고 있습니다.

2024년 미국의 POC CT 이미징 시스템은 1억 190만 달러를 창출해 세계 시장에서 주도권을 유지하고 있습니다. 만성 질환이나 암의 이환율이 높고, 견고한 헬스케어 제공 체제가 지속적인 보급을 뒷받침하고 있습니다. 또한, 양호한 규제 상황, 조기 진단에 대한 의식이 높아지고, 진보된 의료 영상 처리 기술에 대한 많은 투자가 시장의 지속적인 확대를 지원합니다.

POC CT 이미징 시스템 시장을 적극적으로 형성하는 주요 기업으로는 Carestream Dental, Planmed, Xoran Technologies, CurveBeam, Siemens Healthineers, NeuroLogica, Epica International, SOREDEX, Stryker, Alineta 등이 있습니다. POC CT 이미징 시스템 시장의 주요 기업은 화질, 휴대성 및 시스템의 사용 편의성을 향상시키기 위해 기술 혁신에 많은 투자를 하고 있습니다. 차별화를 위해 많은 기업들이 진단 속도와 정확도를 향상시키는 AI 통합 플랫폼 개발에 주력하고 있습니다. 병원, 진단 센터, 텔레헬스 제산업체와의 전략적 협력은 특히 분산형 의료 환경에서 채택률을 높이는 데 도움이 됩니다. 여러 제조업체들은 외래 환자, 중환자실(ICU), 농촌 의료 환경에 맞춤화된 소형 무선 시스템으로 제품 포트폴리오를 확대되고 있습니다. 기업들은 또한 규제 승인과 신속 승인 절차를 활용하여 고급 모델을 시장에 더 빨리 출시하고 있습니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 업계 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 만성질환 유병률 증가

- 고령화 인구 증가

- 조기 진단과 치료 중요성 증가

- 이미징 시스템 기술 발전

- 업계의 잠재적 리스크 및 도전과제

- 이미징 시스템의 높은 비용

- 규제와 상환 장벽

- 시장 기회

- 농촌나 원격지로의 확대

- AI와 원격 의료와의 통합

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 기술 발전

- 현재의 기술 동향

- 신흥기술

- 공급망 분석

- 상환 시나리오

- 가격 분석(2024년)

- 장래 시장 동향

- 갭 분석

- Porter's Five Forces 분석

- PESTEL 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 북미

- 유럽

- 아시아태평양

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추계 및 예측 : 제품별(2021-2034년)

- 주요 동향

- 소형 CT 스캐너

- 풀사이즈 CT 스캐너

제6장 시장 추계 및 예측 : 용도별(2021-2034년)

- 주요 동향

- 신경학

- 호흡기

- 근골격

- 이비인후과

- 기타 용도

제7장 시장 추계 및 예측 : 최종 용도별(2021-2034년)

- 주요 동향

- 병원

- 외래수술센터(ASC)

- 클리닉

- 기타 용도

제8장 시장 추계 및 예측 : 지역별(2021-2034년)

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 인도

- 일본

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 사우디아라비아

- 남아프리카

- 아랍에미리트(UAE)

제9장 기업 프로파일

- Arineta

- Carestream Dental

- CurveBeam

- Epica International

- NeuroLogica

- Planmed

- Siemens Healthineers

- SOREDEX

- Stryker

- Xoran Technologies

The Global Point-of-care CT Imaging Systems Market was valued at USD 254.1 million in 2024 and is estimated to grow at a CAGR of 5.6% to reach USD 435.3 million by 2034. Growth in this market is primarily fueled by the increasing rates of chronic health conditions and a rapidly aging global population. These factors are driving higher demand for immediate and convenient diagnostic solutions. Point-of-care CT systems are compact, mobile platforms that offer fast and accessible imaging, making them essential in emergency care, outpatient centers, and intensive care environments. As healthcare models shift toward patient-centric diagnostics, portable CT technologies are gaining traction for their ability to support respiratory evaluations and deliver real-time imaging without depending on centralized hospital systems.

Rising cases of respiratory conditions are further strengthening the market, as early and accurate diagnosis remains critical in managing outcomes. One of the major contributors to this trend is the seasonal spike in viral infections, which significantly adds to the burden on respiratory health systems. As a result, there's growing adoption of point-of-care CT systems across clinical settings where fast assessments are needed to inform immediate treatment decisions.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $254.1 Million |

| Forecast Value | $435.3 Million |

| CAGR | 5.6% |

In 2024, the full-sized CT scanners segment generated USD 149.3 million. This segment is projected to grow to USD 252.6 million by 2034, advancing at a CAGR of 5.5%. These systems are favored for their high-resolution output and comprehensive diagnostic capabilities, making them the preferred option for critical and emergency care. Full-sized models are commonly used in surgical theaters, trauma units, and intensive care departments where speed and detail in imaging play a vital role in patient outcomes. Their ability to support a wide range of clinical needs makes them indispensable in hospital workflows.

The hospitals segment held a 38.2% share in 2024, remaining the largest End user group in this segment. The dominance of hospitals is attributed to their established diagnostic infrastructure and the availability of trained radiology staff. These institutions routinely handle complex cases in neurology, trauma, and pulmonary care, all of which benefit from rapid point-of-care imaging solutions. As hospitals continue to enhance their diagnostic speed and service delivery, the demand for mobile CT systems grows stronger.

U.S. Point-of-care CT Imaging Systems Market generated USD 101.9 million in 2024, maintaining its leadership in the global space. The country's high incidence of chronic illnesses and cancer, paired with its robust healthcare delivery systems, drives ongoing adoption. Furthermore, a favorable regulatory landscape, increasing awareness of early diagnostics, and substantial investments in advanced medical imaging technologies support sustained market expansion.

Key players actively shaping the Point-of-care CT Imaging Systems Market include Carestream Dental, Planmed, Xoran Technologies, CurveBeam, Siemens Healthineers, NeuroLogica, Epica International, SOREDEX, Stryker, and Arineta. Leading companies in the point-of-care CT imaging systems market are investing heavily in innovation to improve image quality, portability, and system usability. To differentiate themselves, many are focusing on the development of AI-integrated platforms that enhance diagnostic speed and accuracy. Strategic collaborations with hospitals, diagnostic centers, and telehealth providers help boost adoption, particularly in decentralized care settings. Several manufacturers are expanding their product portfolios with compact, wireless systems tailored for outpatient, ICU, and rural care environments. Companies are also leveraging regulatory approvals and fast-track clearances to bring advanced models to market faster.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Increasing prevalence of chronic disorders

- 3.2.1.2 Growing aging population

- 3.2.1.3 Rising emphasis on early diagnosis and treatment

- 3.2.1.4 Technological advancements in imaging system

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 High cost of imaging systems

- 3.2.2.2 Regulatory and reimbursement barriers

- 3.2.3 Market opportunities

- 3.2.3.1 Expansion into rural and remote areas

- 3.2.3.2 Integration with AI and telemedicine

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.4.3 Asia Pacific

- 3.4.4 Latin America

- 3.4.5 Middle East and Africa

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Supply chain analysis

- 3.7 Reimbursement scenario

- 3.8 Pricing analysis, 2024

- 3.9 Future market trends

- 3.10 Gap analysis

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn)

- 5.1 Key trends

- 5.2 Compact CT scanners

- 5.3 Full-sized CT scanners

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 Neurology

- 6.3 Respiratory

- 6.4 Musculoskeletal

- 6.5 ENT

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals

- 7.3 Ambulatory surgery centers

- 7.4 Clinics

- 7.5 Other end use

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 India

- 8.4.3 Japan

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 Saudi Arabia

- 8.6.2 South Africa

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 Arineta

- 9.2 Carestream Dental

- 9.3 CurveBeam

- 9.4 Epica International

- 9.5 NeuroLogica

- 9.6 Planmed

- 9.7 Siemens Healthineers

- 9.8 SOREDEX

- 9.9 Stryker

- 9.10 Xoran Technologies