|

시장보고서

상품코드

1801911

연성 내시경 시장 : 기회, 성장 촉진요인, 산업 동향 분석, 예측(2025-2034년)Flexible Endoscopes Market Opportunity, Growth Drivers, Industry Trend Analysis, and Forecast 2025 - 2034 |

||||||

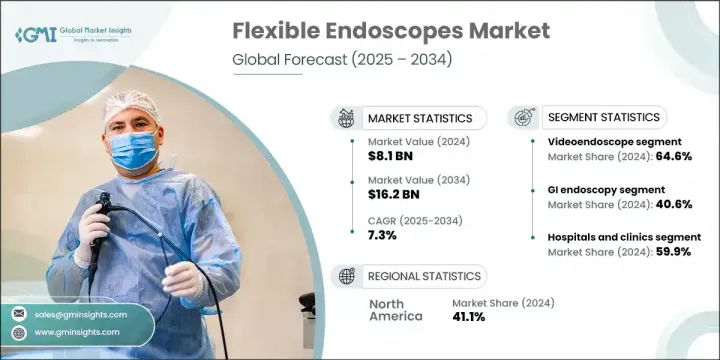

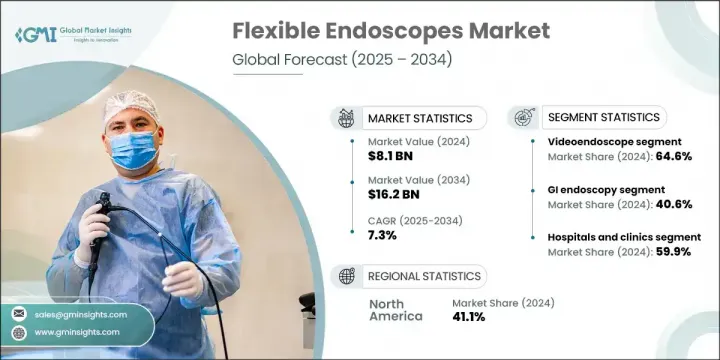

세계 연성 내시경 시장은 2024년 81억 달러로 평가되었으며 CAGR 7.3%로 성장했으며 2034년 162억 달러에 이를 것으로 추정됩니다.

이 성장 궤도는 만성 질환 환자 증가, 낮은 침습 치료로의 이동 증가, 조기 진단 관리에 대한 의식 증가에 의해 뒷받침됩니다. 더 많은 환자들이 위험이 적고, 신속하게 회복되고, 비용이 적게 드는 처치를 추구하는 동안, 연성 내시경 검사는 건강 관리 시스템 전반에 걸쳐 계속해서 자리 잡고 있습니다. 시각화 기술, 정밀 도구 강화, 환자 편의성 향상 등 끊임없는 기술 혁신도 이러한 장비의 매력을 향상시키고 있습니다. 게다가 외래환자와 외래치료의 인기가 높아짐에 따라 새로운 수요가 생기고 있으며, 연성내시경은 임상분야에 걸쳐 확장가능하고 비용 효율적인 진단 및 치료 솔루션을 제공합니다.

연성 내시경은 의사가 큰 절개를 하지 않고 진단과 수술 시 복잡한 해부학적 구조를 탐색할 수 있도록 유연한 삽입 튜브를 특징으로 합니다. 침습이 적은 건강 관리를 지원하는 역할은 급속히 확대되고 있습니다. 회복 속도, 외상 경감, 전반적인 비용 절감 등의 이점으로 인해 환자와 의사 간에 이러한 도구에 대한 선호도가 높아지고 있습니다. 이러한 장비는 특히 복잡한 경우에 정확하고 효율적인 치료 제공을 가능하게 함으로써 현대 치료 워크플로우의 기본이 되었습니다.

| 시장 범위 | |

|---|---|

| 시작 연도 | 2024년 |

| 예측 연도 | 2025-2034년 |

| 시작금액 | 81억 달러 |

| 예측 금액 | 162억 달러 |

| CAGR | 7.3% |

2024년, 비디오 내시경 부문은 세계 시장의 64.6%를 차지했습니다. 이 이점은 뛰어난 이미지의 선명도, 실시간 시각화, 광범위한 임상 전문 분야에 대한 적응성 때문입니다. 비디오 내시경은 소형화된 카메라와 고급 광학계를 사용하여 고해상도 영상을 외부 디스플레이에 비추어 진단 정확도를 크게 높여 복잡한 개입을 지원합니다. 그 사용 범위는 소화기과, 호흡기과, 부인과, 비뇨기과에 이릅니다. 이러한 기능은 낮은 침습 치료에서 정밀 의료에 필수적인 도구로서 그 지위는 확고한 것으로 되어 있습니다.

소화기(GI) 내시경 검사 부문은 2024년 40.6%의 점유율을 차지했습니다. 소화관 질환의 발생률 증가와 정기적 스크리닝에 대한 사회적 관심 증가가 이 부문을 끌어 올리는 주요 요인입니다. GI 내시경 검사는 입원 기간을 단축하고 환자의 편안함을 향상시킬 수 있기 때문에 선호되는 진단 방법으로 성장을 계속하고 있습니다. 이 부문의 성장은 절차를 보다 효율적이고 안전하게 만드는 내시경 기술의 지속적인 진보를 반영하고 있으며 세계의 의료 서비스 제공업체에서 채택이 진행되고 있습니다.

2024년 미국의 연성 내시경 시장 규모는 32억 달러가 되었고, 이 지역은 견고한 헬스케어 인프라, 선진 의료기기의 보급, 의료 요구가 높아지는 노인 인구 증가 등의 이점을 누리고 있습니다. 미국은 조기 진단과 빈번한 스크리닝에 대한 높은 수요에 힘입어 이 지역에서 성장의 주요 기여자로 자리잡고 있습니다. 병원과 외래 센터에 대한 최신 내시경 시스템의 보급은 성숙하면서도 성장하는이 시장의 확대를 뒷받침하고 있습니다.

연성 내시경 세계 시장의 주요 기업으로는 CooperSurgical, XION, PENTAX Medical, STORZ, RICHARD WOLF, Machida, Boston Scientific, FUJIFILM, BD, ENDOMED SYSTEMS, Laborie, OLYMPUS 등이 있습니다. 연성 내시경 시장에서 사업을 전개하는 기업은 기술적으로 선진적이고 사용자 친화적인 시스템의 제품 라인업 확충에 주력하고 있습니다. R&D에 대한 전략적 투자는 조작성을 향상시키고 AI 지원을 통한 시각화를 갖춘 초박형 고화질 범위의 개발을 목표로 합니다. 제조업체 각 사는 또한 병원과 전문 클리닉과의 파트너십을 활용하여 다양한 의료 현장에서의 제품 접근과 전개를 강화하고 있습니다. 또한 규제 당국의 승인과 신흥국의 현지 제조 거점을 통해 지리적 범위를 확장하려는 노력도 진행되고 있습니다. 시장 리더는 브랜드 충성도를 강화하기 위해 애프터 영업 지원, 유지 보수 서비스 및 의사 교육 프로그램에 투자합니다.

목차

제1장 조사 방법과 범위

제2장 주요 요약

제3장 업계 인사이트

- 생태계 분석

- 업계에 미치는 영향요인

- 성장 촉진요인

- 만성 질환 증가

- 기술적 진보

- 저침습치료의 인기가 높아져

- 건강 의식의 고조와 조기 진단 수요

- 업계의 잠재적 위험 및 과제

- 엄격한 규제 프로세스

- 시장 기회

- AI와 로봇 시스템의 통합

- 헬스케어 투자 증가

- 성장 촉진요인

- 성장 가능성 분석

- 규제 상황

- 북미

- 유럽

- 기술적 진보

- 현재의 기술 동향

- 신흥기술

- 가격 분석, 2024

- 상환 시나리오

- 일회용/일회용 연성 내시경으로 전환

- 파이프라인 분석

- 시작 시나리오

- Porter's Five Forces 분석

- PESTEL 분석

- 장래 시장 동향

- 갭 분석

제4장 경쟁 구도

- 소개

- 기업의 시장 점유율 분석

- 기업 매트릭스 분석

- 주요 시장 기업의 경쟁 분석

- 경쟁 포지셔닝 매트릭스

- 주요 발전

- 합병과 인수

- 파트너십 및 협업

- 신제품 발매

- 확장 계획

제5장 시장 추정 및 예측 : 제품별, 2021년-2034년

- 주요 동향

- 비디오 내시경

- 섬유경

제6장 시장 추정 및 예측 : 용도별, 2021년-2034년

- 주요 동향

- 소화관 내시경 검사

- 폐 내시경 검사

- 이비인후과 내시경 검사

- 비뇨기과

- 기타 용도

제7장 시장 추정 및 예측 : 최종 용도별, 2021년-2034년

- 주요 동향

- 병원 및 진료소

- 외래수술센터(ASC)

- 기타 최종 사용자

제8장 시장 추정 및 예측 : 지역별, 2021년-2034년

- 주요 동향

- 북미

- 미국

- 캐나다

- 유럽

- 독일

- 영국

- 프랑스

- 스페인

- 이탈리아

- 네덜란드

- 아시아태평양

- 중국

- 일본

- 인도

- 호주

- 한국

- 라틴아메리카

- 브라질

- 멕시코

- 아르헨티나

- 중동 및 아프리카

- 남아프리카

- 사우디아라비아

- 아랍에미리트(UAE)

제9장 기업 프로파일

- BD

- Boston Scientific

- CooperSurgical

- ENDOMED SYSTEMS

- FUJIFILM

- Laborie

- Machida

- OLYMPUS

- PENTAX Medical

- RICHARD WOLF

- STORZ

- XION

The Global Flexible Endoscopes Market was valued at USD 8.1 billion in 2024 and is estimated to grow at a CAGR of 7.3% to reach USD 16.2 billion by 2034. This growth trajectory is fueled by the rising number of chronic disease cases, the increasing shift toward minimally invasive procedures, and heightened awareness of early-stage diagnostic care. As more patients seek procedures with lower risks, faster recovery, and lower costs, flexible endoscopy continues to gain ground across healthcare systems. Continuous innovation in visualization technologies, enhanced precision tools, and improved patient comfort is also elevating the appeal of these devices. Additionally, the rising popularity of outpatient and ambulatory care settings is creating new demand, with flexible endoscopes offering scalable, cost-effective diagnostic and therapeutic solutions across clinical disciplines.

The flexible endoscopes feature a pliable insertion tube that allows physicians to navigate complex anatomical structures during diagnostic and surgical procedures without large incisions. Their role in supporting less-invasive healthcare is expanding rapidly. The preference for these devices is rising among both patients and physicians due to advantages such as faster recovery, reduced trauma, and lower overall costs. These devices have become fundamental in modern treatment workflows by enabling precise and efficient care delivery, particularly in complex cases.

| Market Scope | |

|---|---|

| Start Year | 2024 |

| Forecast Year | 2025-2034 |

| Start Value | $8.1 Billion |

| Forecast Value | $16.2 Billion |

| CAGR | 7.3% |

In 2024, the videoendoscope segment accounted for 64.6% of the global market. This dominance is attributed to their superior image clarity, real-time visualization, and adaptability across a wide range of clinical specialties. Videoendoscopes use miniaturized cameras and advanced optics that deliver high-definition visuals to external displays, greatly enhancing diagnostic accuracy and supporting complex interventions. Their use spans across gastroenterology, pulmonology, gynecology, and urology. These features have cemented their place as essential tools for precision medicine in minimally invasive care settings.

The gastrointestinal (GI) endoscopy segment held a 40.6% share in 2024. Increasing rates of digestive tract disorders and growing public interest in routine screening are key factors boosting this segment. GI endoscopy continues to grow as a preferred diagnostic method due to its ability to reduce hospital stays and improve patient comfort. This segment's growth also reflects ongoing advancements in endoscopic technology that make procedures more efficient and safer, driving increased adoption across healthcare providers globally.

U.S. Flexible Endoscopes Market was valued at USD 3.2 billion in 2024. The region benefits from a robust healthcare infrastructure, widespread use of advanced medical equipment, and a growing senior population with increasing healthcare needs. The U.S. remains a primary contributor to growth within the region, supported by high demand for early diagnostics and frequent screenings. Strong penetration of modern endoscopy systems across hospitals and outpatient centers continues to fuel expansion in this mature yet growing market.

Key players in the Global Flexible Endoscopes Market include CooperSurgical, XION, PENTAX Medical, STORZ, RICHARD WOLF, Machida, Boston Scientific, FUJIFILM, BD, ENDOMED SYSTEMS, Laborie, and OLYMPUS. Companies operating in the flexible endoscopes market are focusing on expanding their product offerings with technologically advanced and user-friendly systems. The strategic investments in R&D aim to develop ultra-thin, high-definition scopes with enhanced maneuverability and AI-assisted visualization. Manufacturers are also leveraging partnerships with hospitals and specialty clinics to boost product access and deployment across varied care settings. Additionally, efforts are underway to expand their geographic reach through regulatory approvals and local manufacturing hubs in emerging economies. Market leaders are investing in after-sales support, maintenance services, and physician training programs to strengthen brand loyalty.

Table of Contents

Chapter 1 Methodology and Scope

- 1.1 Market scope and definition

- 1.2 Research design

- 1.2.1 Research approach

- 1.2.2 Data collection methods

- 1.3 Data mining sources

- 1.3.1 Global

- 1.3.2 Regional/Country

- 1.4 Base estimates and calculations

- 1.4.1 Base year calculation

- 1.4.2 Key trends for market estimation

- 1.5 Primary research and validation

- 1.5.1 Primary sources

- 1.6 Forecast model

- 1.7 Research assumptions and limitations

Chapter 2 Executive Summary

- 2.1 Industry 360° synopsis

- 2.2 Key market trends

- 2.2.1 Regional trends

- 2.2.2 Product trends

- 2.2.3 Application trends

- 2.2.4 End use trends

- 2.3 CXO perspectives: Strategic imperatives

- 2.3.1 Key decision points for industry executives

- 2.3.2 Critical success factors for market players

- 2.4 Future outlook and strategic recommendations

Chapter 3 Industry Insights

- 3.1 Industry ecosystem analysis

- 3.2 Industry impact forces

- 3.2.1 Growth drivers

- 3.2.1.1 Growing prevalence of chronic conditions

- 3.2.1.2 Technological advancements

- 3.2.1.3 Increasing popularity of minimally invasive therapies

- 3.2.1.4 Rising health awareness and demand for early-stage diagnosis

- 3.2.2 Industry pitfalls and challenges

- 3.2.2.1 Stringent regulatory process

- 3.2.3 Market opportunities

- 3.2.3.1 Integration of AI and robotic systems

- 3.2.3.2 Rising healthcare investments

- 3.2.1 Growth drivers

- 3.3 Growth potential analysis

- 3.4 Regulatory landscape

- 3.4.1 North America

- 3.4.2 Europe

- 3.5 Technological advancements

- 3.5.1 Current technological trends

- 3.5.2 Emerging technologies

- 3.6 Pricing analysis, 2024

- 3.6.1 North America

- 3.6.2 Europe

- 3.6.3 Asia Pacific

- 3.6.4 Latin America

- 3.6.5 MEA

- 3.7 Reimbursement scenario

- 3.8 Transition toward single-use/disposable flexible endoscopes

- 3.9 Pipeline analysis

- 3.10 Start-up scenario

- 3.11 Porter's analysis

- 3.12 PESTEL analysis

- 3.13 Future market trends

- 3.14 Gap analysis

Chapter 4 Competitive Landscape, 2024

- 4.1 Introduction

- 4.2 Company market share analysis

- 4.2.1 North America

- 4.2.2 Europe

- 4.2.3 Asia Pacific

- 4.2.4 Latin America

- 4.2.5 MEA

- 4.3 Company matrix analysis

- 4.4 Competitive analysis of major market players

- 4.5 Competitive positioning matrix

- 4.6 Key developments

- 4.6.1 Mergers and acquisitions

- 4.6.2 Partnerships and collaborations

- 4.6.3 New product launches

- 4.6.4 Expansion plans

Chapter 5 Market Estimates and Forecast, By Product, 2021 - 2034 ($ Mn and Units)

- 5.1 Key trends

- 5.2 Videoendoscope

- 5.3 Fiberscope

Chapter 6 Market Estimates and Forecast, By Application, 2021 - 2034 ($ Mn)

- 6.1 Key trends

- 6.2 GI endoscopy

- 6.3 Pulmonary endoscopy

- 6.4 ENT endoscopy

- 6.5 Urology

- 6.6 Other applications

Chapter 7 Market Estimates and Forecast, By End Use, 2021 - 2034 ($ Mn)

- 7.1 Key trends

- 7.2 Hospitals and clinics

- 7.3 Ambulatory surgical centers

- 7.4 Other end users

Chapter 8 Market Estimates and Forecast, By Region, 2021 - 2034 ($ Mn)

- 8.1 Key trends

- 8.2 North America

- 8.2.1 U.S.

- 8.2.2 Canada

- 8.3 Europe

- 8.3.1 Germany

- 8.3.2 UK

- 8.3.3 France

- 8.3.4 Spain

- 8.3.5 Italy

- 8.3.6 Netherlands

- 8.4 Asia Pacific

- 8.4.1 China

- 8.4.2 Japan

- 8.4.3 India

- 8.4.4 Australia

- 8.4.5 South Korea

- 8.5 Latin America

- 8.5.1 Brazil

- 8.5.2 Mexico

- 8.5.3 Argentina

- 8.6 Middle East and Africa

- 8.6.1 South Africa

- 8.6.2 Saudi Arabia

- 8.6.3 UAE

Chapter 9 Company Profiles

- 9.1 BD

- 9.2 Boston Scientific

- 9.3 CooperSurgical

- 9.4 ENDOMED SYSTEMS

- 9.5 FUJIFILM

- 9.6 Laborie

- 9.7 Machida

- 9.8 OLYMPUS

- 9.9 PENTAX Medical

- 9.10 RICHARD WOLF

- 9.11 STORZ

- 9.12 XION